Have you seen America’s national debt? What the stablecoin market says

The global economy is undergoing a transformation, with new trends emerging in central banks’ monetary policy. One promising avenue for crypto is investment in US Treasury securities. ForkLog examines how America’s public debt became collateral for stablecoins and the prospects for RWA projects in this corner of traditional finance.

How public debt builds up

According to data from the Institute of International Finance, in the first quarter of 2024 global debt exceeded $315 trillion, or 333% of GDP. About two-thirds of this came from developed economies, with the largest shares in the US and Japan.

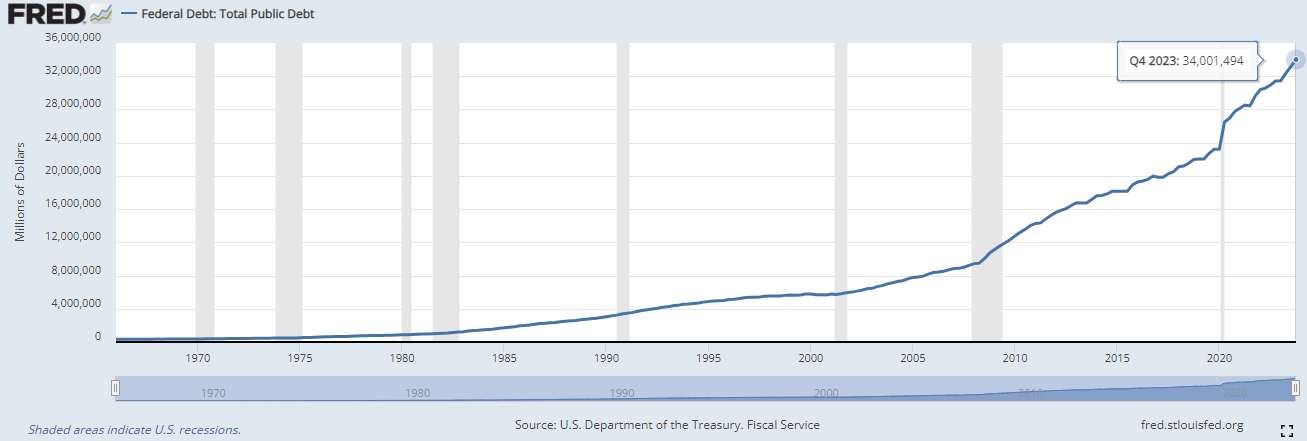

At the start of June 2024 US public debt surpassed $34 trillion, an all-time high. Its growth has accelerated. From 2010 to 2020 the debt rose by $10 trillion—from $13 trillion to $23 trillion. By a comparable amount ($10.8 trillion, or 46.5%) it grew in just four years since the pandemic began.

The main driver is the persistent budget deficit. The interest burden is also rising. Statista analysts forecast a $1.5 trillion annual deficit through 2029. As of April 2024 debt service cost $624 billion per year. And with the Fed policy rate above 5%, this sum will continue to climb.

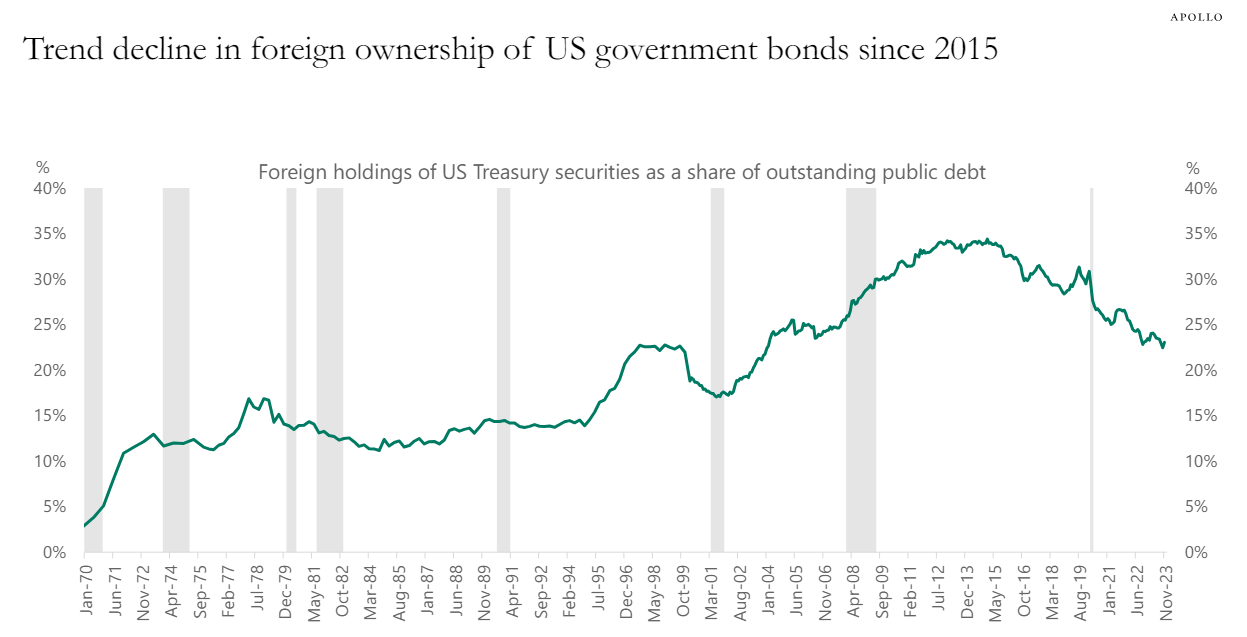

To cover the deficit, the US Treasury resorts to printing additional money to repay loans. Until about 2015 America increased the share of its debt held by foreign governments; at the peak this reached 35%. Recently the trend reversed, falling to 23% by the end of 2023.

If this trend persists, new funding sources will be needed. One hypothetical route is RWA—specifically, the growth of regulated stablecoins pegged to the US dollar.

The two biggest stablecoins—USDT and USDC

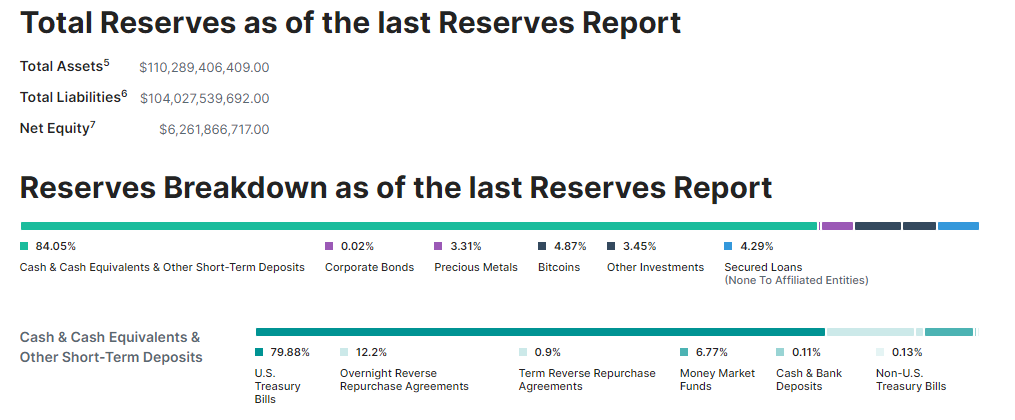

Consider Tether, issuer of USDT. According to the company’s report dated March 31, 2024, its reserves stood at $110.3 billion. Over 84% ($92.6 billion) were held in “cash, cash equivalents and other short-term deposits.” Of these, nearly 80% ($74 billion) sat in US Treasuries. That means USDT’s assets are at least 67% backed by US public debt.

A similar report from USDC issuer Circle as of June 4, 2024 shows that 90% ($29.1 billion) of reserves are backed by assets in the BlackRock-managed Circle Reserve Fund, which also invests in US Treasuries.

Some 41.65% of assets ($12.12 billion) are invested directly in US public debt. The remaining 58.35% ($16.98 billion) are placed in repo transactions for the repurchase of such securities.

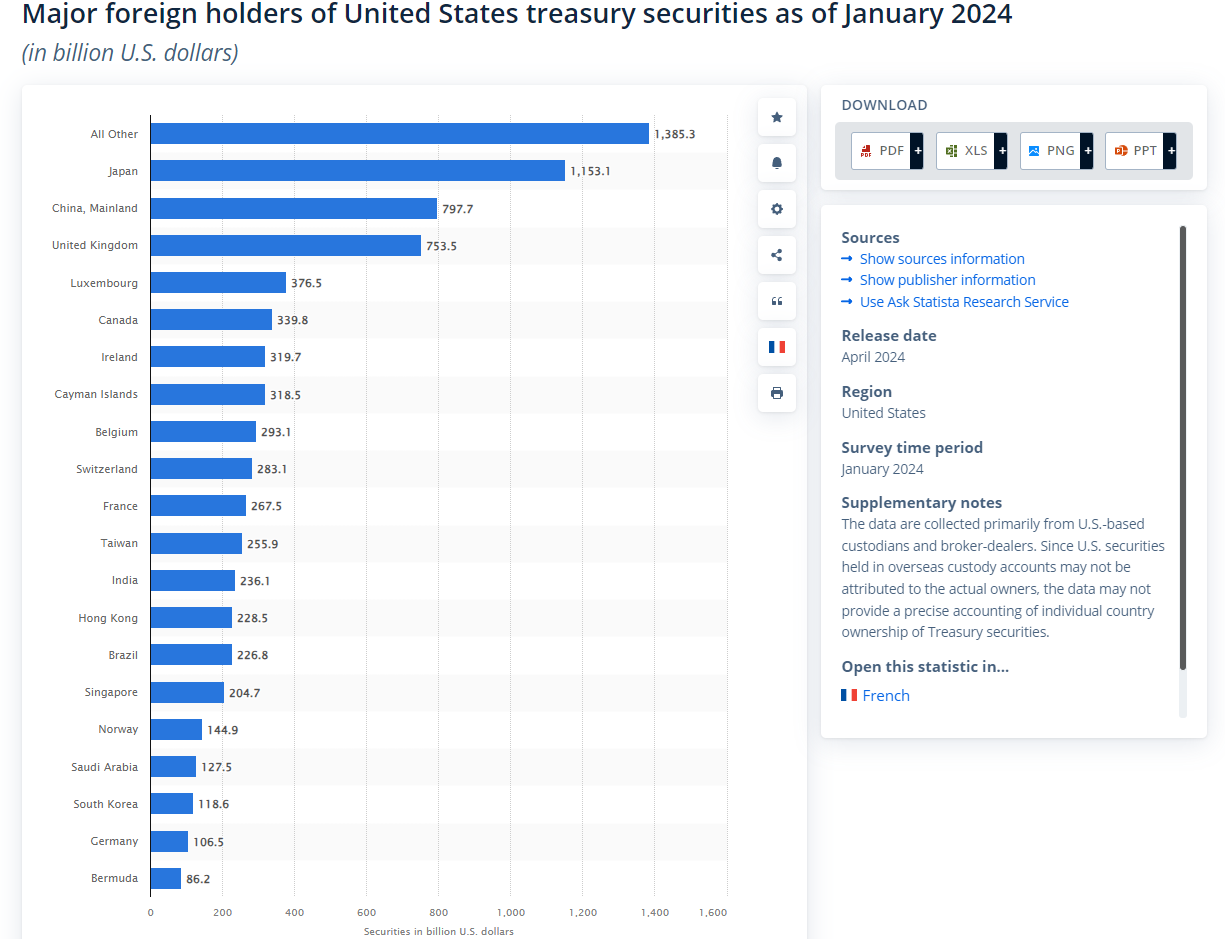

Aggregating the US public-debt backing of USDT and USDC yields $103.1 billion. Compared with data from Statista for January 2024, the two largest stablecoins hold a slightly smaller share of US Treasuries than Germany.

Though small relative to total public debt, stablecoins’ distributed nature means they can help offset the declining share held by foreign firms.

Adoption could be propelled by restrictions and sanctions affecting fiat, as well as simpler cross-border settlement.

One sign of rising interest: Russian metals producers. In June 2024 media reported that two companies not under sanctions began using USDT and other cryptocurrencies for international payments—mainly with Chinese clients and suppliers.

The need for such mechanisms is likely to grow, as will the capitalisation of regulated stablecoins whose issuers will keep adding US government debt to reserves.

DeFi and its impact on public debt

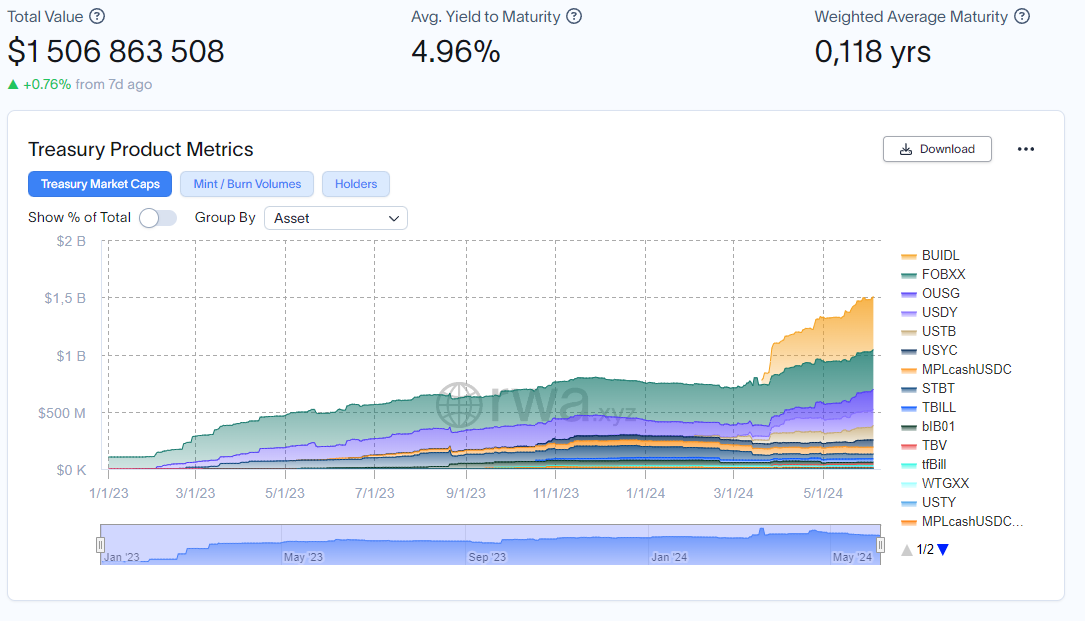

Also noteworthy are DeFi applications that invest in Treasuries and issue tokenised assets on-chain. As of June 2024 the market capitalisation of such products exceeded $1.5 billion. The sector grew from $100 million in early 2023 in less than 18 months.

The largest issuers of tokenised Treasury products are BlackRock and Franklin. These firms are also active in the market for spot bitcoin- and Ethereum-ETFs.

Unlike centralised stablecoins such as USDT and USDC, these RWA platforms distribute yield to token holders. If stablecoin issuers keep all profits, the latter build businesses on intermediation, earning processing fees.

For example, Tether’s net profit in the first quarter of 2024 reached $4.5 billion, of which roughly $1 billion came from interest on US Treasuries. Holders of the stablecoin, of course, received no payouts.

From the standpoint of attracting capital to buy public debt, RWA platforms look more appealing. Investors could deploy these tokens in other DeFi applications, potentially boosting returns and bringing additional liquidity to the crypto market.

Meanwhile, more experimental stablecoins are emerging. In early June 2024 Paxos, issuer of PayPal USD (PYUSD), Pax Dollar (USDP) and Pax Gold (PAXG), introduced Lift Dollar. Pegged to the US dollar, it will offer users a 5% yield—those very interest payments from Treasuries.

The algorithmic stablecoin DAI

DAI is issued by MakerDAO. The asset is collateralised by coins and tokens including ETH, WBTC, USDC and UNI. However, as part of its RWA strategy, MakerDAO extends loans secured by traditional securities.

Since 2022 the organisation has been buying short-term US Treasuries and corporate bonds. By mid-2023, thanks to a partnership with DeFi-focused consultancy Monetalis, MakerDAO’s investments in US public debt reached $1.2 billion.

Beyond direct investments in Treasuries, the token is backed by USDC. Given that Circle holds assets in government bonds, the US government’s obligations underpinning DAI are even greater.

Why investing in public debt benefits the crypto market

It has been more than 15 years since the creation of bitcoin’s first block. Its hash contains the headline “Chancellor on brink of second bailout for banks,” published by London’s The Times at the end of the 2008 financial crisis.

The shortcomings of the traditional economy helped bitcoin and its analogues gain traction. For a long time they were seen as an alternative—or even a replacement—for the existing financial system.

Yet despite ideological differences between crypto and traditional markets, the two economies are gradually converging. Companies have learned to extract value from both worlds, in a symbiosis that benefits all participants.

Thus, in May 2023 Tether announced it would allocate up to 15% of profits to buy bitcoin. According to reporting for the first quarter of 2024, the company’s investment in the first cryptocurrency exceeded $1.7 billion.

It follows that the US government, as the centre of global monetary policy, by paying interest on public debt, not only underpins the stability of USDT but also indirectly finances bitcoin purchases. This has also enabled Tether to invest in adjacent markets: AI infrastructure, P2P communications, and renewable energy and mining.

In short, sovereign debt is feeding the bitcoin ecosystem and helping it grow more resilient.

Text: Oleg Cash Coin

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!