Financial micro-matters: what lies behind MicroStrategy’s bold bet on Bitcoin

The public company MicroStrategy burst onto the Bitcoin scene last year when it began purchasing the first cryptocurrency. Initially with its own money, and then with borrowed funds, the software vendor acquired 90 859 BTC. Many regard this as a prescient bet on Bitcoin’s scarcity properties and laud Michael Saylor’s investment acumen. But, as is well known in finance, you have to watch the hands as well as the words.

For ForkLog, Sergey Kalinin, Head of Product at the cryptocurrency exchange Kuna, explains possible hidden motives of MicroStrategy and its shareholders in the big bet on Bitcoin.

In recent times, the information space has seen an exponential rise in upbeat views about the “massive influx of institutional investors” into cryptocurrencies, led by Bitcoin. MicroStrategy, Tesla, Square have become the headline names in financial news. I deliberately exclude Grayscale here, as it cannot be described as an investor. It is a trust that holds other people’s money and does not purchase on its own. And that explains a lot—but more on that later. Let’s start by unpacking the concepts and numbers.

Who are institutional investors? A brief primer on terminology

What should be understood by “institutional investor”? I will use the most precise formulations as understood by the United States Internal Revenue Service (IRS), the Securities and Exchange Commission (SEC) and GAAP.

To be precise, the SEC operates with the terms “qualified institutional buyer” (QIB) under Rule 144A of the Securities Act (1933) and “accredited investor” under Rule 501(a) Regulation D of the same Act. It is worth noting that such investors’ transactions are viewed solely through the lens of securities. This partly explains why financial institutions prefer to deal with virtual currencies through security-linked derivatives rather than through straightforward purchases.

The IRS interprets definitions more broadly, as it considers all sources of income subject to taxation. The term “institutional investors” is more of a catch-all and includes financial intermediaries whose aim is to invest capital. They include:

- banks;

- credit unions;

- insurance companies;

- pension funds;

- broker-dealers;

- hedge funds;

REIT ;- investment advisers, funds that invest their own funds and

- mutual funds, whose substantial activity is buying and selling financial assets.

For example, QIBs must continuously hold exposure to securities totaling at least $100 million, and broker-dealers must hold unaffiliated securities of $10 million or more.

As for operating companies, such as MicroStrategy and Tesla, they can be considered institutional investors only if they invest free (surplus) capital in investment assets. Moreover, there are clear requirements regarding the company’s activity and the competence of its investment managers.

If Tesla can be classified as such a company due to its large cash surplus (rather than capital), then MicroStrategy, which issued unsecured notes to fund the Bitcoin purchase with the proceeds from their sale, is, in my view, hardly eligible.

On 26 August 2020, the SEC amended the definitions of “qualified institutional buyer” and “accredited investor,” expanding the roster of those who can be considered such. In particular, now “accredited investor” can include, alongside Native American tribes, limited liability companies (LLCs) with assets of $5 million or more, not for the purpose of owning such assets. But again, through securities.

According to the IRS, cryptocurrencies are an investment asset in the form of property, which lies at the heart of the corporate hype around Bitcoin. If for Tesla this was more of a joke and deliberate manipulation of the asset’s price, into which they entered some time ago (which will be the subject of an SEC investigation, I am 100% sure), the MicroStrategy situation is much more intricate. The company itself is little more than a conduit for financial engineering and equity operations for more serious actors and firms. To understand the whole picture, one must take a step back.

From mediocrity to a star in six months — how MicroStrategy piled on debt

What is known about MicroStrategy? It has existed since 1998 and operates in the information technology sector. At the peak of the dot-com bubble, the stock price rose to $3300, but then the company languished for a long period in a range between $100 and $200 per share. And then the crypto hype appeared, and investment managers decided to play the card of this middling company.

Monthly chart of MSTR. Data: TradingView.

Why average? Because the company’s operating and investment figures are fairly lacklustre when viewed against the balance sheet and income statement.

Let’s start at the top—with the CEO Michael Saylor, who has shown notable wisdom in shielding his assets from inflation in a time when the Fed’s printing press shows no sign of stopping. Direct quote:

«We are trying to protect our reserves. The purchasing power of fiat money is rapidly falling»

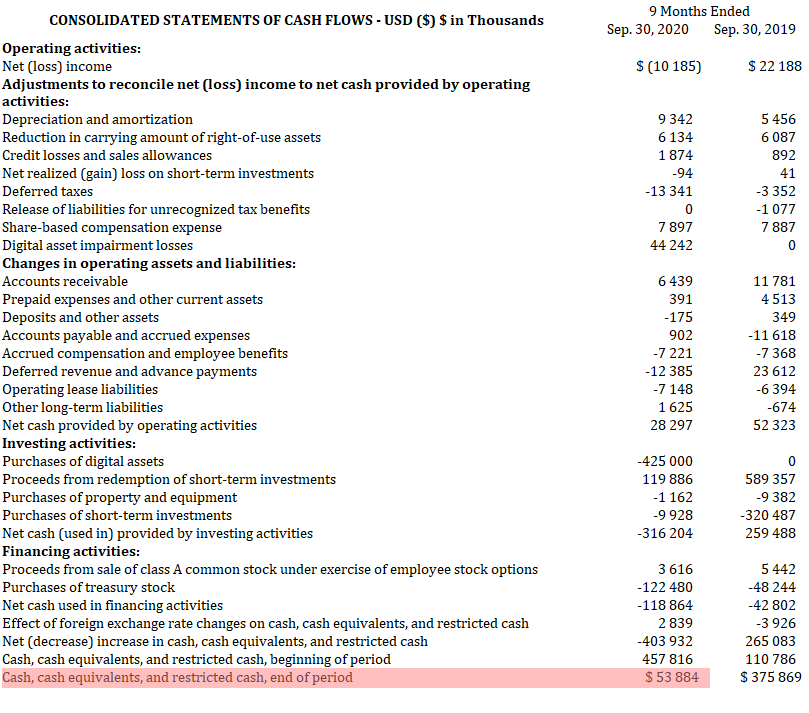

In short, he is protecting the treasury from inflation. However, the cash flow statement filed with the SEC shows that after the initial Bitcoin purchase there remained only a pittance of their own money. By the end of Q3 2020, the document indicates the company had just $53 million — including cash and equivalents. Where did the funds for the “salvation” in Bitcoin of more than $1 billion come from?

Data: MicroStrategy Inc (Filer) CIK: 0001050446.

Again, Saylor insists that “we want to safeguard our treasury and keep the money in Bitcoin.” On the one hand, it’s their money; let them do as they wish.

On the other hand, a December 7 press release announced the issue of Convertible Senior Notes for $550 million and an option for initial purchasers to buy notes for a further $100 million.

It is worth noting that these are not corporate convertible bonds that give the holder either debt or shares at expiry. They are convertible unsecured notes, and Bitcoin is not an asset or collateral for these notes.

With a maturity date of December 15, 2025 and a coupon of 0.75% in dollars, MicroStrategy has, from 2023, the right to cash-settle the issued notes, and from June 15, 2025 they may be exchanged not only for cash (under terms publicly unavailable).

This instrument is often used to finance startups in early stages when it is unclear whether to take equity or demand repayment. But it is by no means a tool for serious institutional investors.

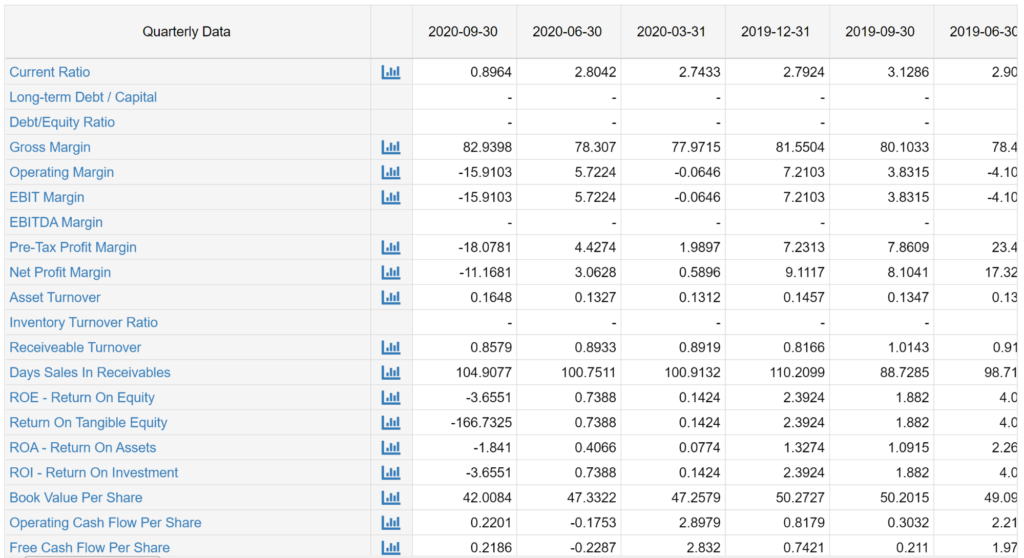

The numbers for MicroStrategy are not good across the board. You can check for yourself, but as of the end of Q3 nothing pointed to success. Especially EBITDA, Book Value per Share and ROE.

Yet even by that metric, MicroStrategy is hard to classify as a QIB. Yet it is becoming one of the largest Bitcoin buyers, financed by debt rather than equity, not even secured bonds but unsecured notes with near-zero yields. Isn’t it odd that investors who have already sunk more than $1.5 billion into “promises” could simply have bought Bitcoin? Or was there something else to “pull off”?

Hidden beneficiaries — who stands to gain from MicroStrategy’s stock surge

Digging deeper, more intriguing details emerge — even more intriguing than the debt raised to buy Bitcoin. These details suggest we are dealing with a financial scheme rather than an investment.

‘The notes can be converted into cash, into MicroStrategy Class A shares, or a combination of these assets — at MicroStrategy’s discretion.’

It is MicroStrategy that decides how to settle the notes. They could be paid in cash, in shares, or a mix of both. In my view, the devil lies in these details. If logic holds, they will return whatever is most advantageous to the company and its shareholders at the moment. Debt holders have no say until maturity. Their priority is low, lower than secured bonds, should the company choose to issue them. If the stock falls, they are paid in shares; if it rises, in cash. It’s a no-lose proposition.

Who could have orchestrated such a combination or would be interested in it? To find out, look at the list of holders of the notes (Class A shareholders — editor’s note).

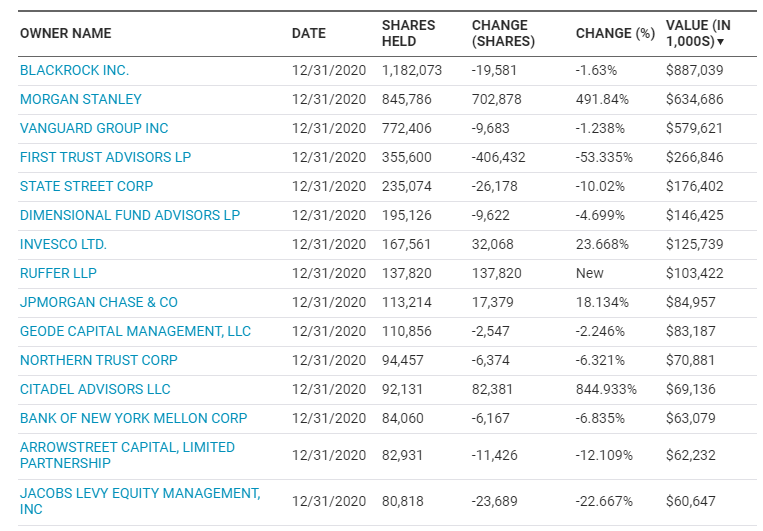

As of writing, the quarterly report on share ownership exists only for the end of 2020. Here is who we see among the largest holders:

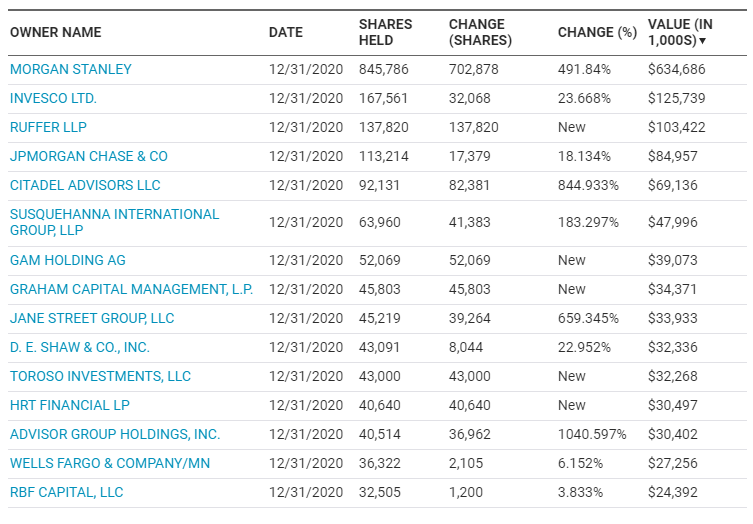

But more importantly, who has boosted the portfolio:

We see a dramatic surge in the stakes held by Morgan Stanley and Citadel. With all due respect, I would not classify them as adherents of cryptocurrency or decentralisation.

Companies must file daily with the SEC for certain transactions. In the documents from February 4, I found an interesting event: legendary quant Ken Griffin and Citadel-affiliated structures together own 24.3% of all Class A ordinary shares. And those are only the stakes traceable by known names. It is a huge figure and clearly different from the December ownership figures.

If you dive into Griffin’s history, you will see that this renowned Wall Street figure is one of the best “vultures” in the proper sense. And I sense that Morgan Stanley or JPMorgan were investment bankers and underwriters for MicroStrategy’s note placement. They may also be market-makers. Since such private placements do not have to be disclosed, there is a strong likelihood that the banks mentioned conceived the whole story.

But there is another important point: who gains from these deals. Is it proprietary trading by its own traders or client operations? Such information is extremely hard to find on the surface.

How accurate are the claims that institutional investors, which I still regard as financial intermediaries rather than operating companies, invest in Bitcoin? Here we should recall the Dodd-Frank Act, passed after the 2008 crisis. It sharply limited how much risk investment banks can take with their own capital, primarily to curb losses. That is why Morgan Stanley and JPMorgan predominantly operate on behalf of clients—operating with client money rather than their own.

Of course, Ken Griffin’s Citadel or Paul Graham’s Graham Capital are classic hedge funds, but their aim is to maximise the returns of their limited partners. In effect, they are not investors but professional speculators, spotting and exploiting market inefficiencies. And Bitcoin, with its ostensibly flexible regulation and the prospect of unlimited financial engineering, together with loss-offset rules for future periods, opens the door to schemes like MicroStrategy with its unsecured notes.

If Morgan Stanley is involved in inflating the MicroStrategy bubble, they did so professionally. At the time of building the position (they began long before the hype), there began an information campaign that Counterpoint Global, a unit of Morgan Stanley Investment Management, is reported to be considering investing in Bitcoin to the tune of $150 billion. That pushed the price higher still. No commitments were stated by the firm. Notably, Reuters reported that the investment bank declined to comment. As the saying goes, “the newspapers print, the caravan moves on.”

Many mistake trading on news for trading on fundamentals. They are two different businesses—the fundamentals rest on verified historical economic data. Bitcoin today lives on expectations, and the sole “fundamental” is the rising price, which should reflect fundamental changes in the asset, not the other way around.

Beyond media noise and Tesla’s pledge to sell cars for Bitcoin, there is no fundamental that professional players rely on. It is worth noting that financial media and analysts earn their bread, with estimates ranging from $4 to $5 billion in annual inflows. So the news market can be created, and it’s not bad at that.

Such “trend-following” outfits as Graham Capital can (and will) remain in assets in a supercharged uptrend because quantitative strategies dictate it. They do not care about fundamentals; they operate by numbers. They are not investors but speculators.

In this context I became curious about PDT Partners, which used to be Morgan Stanley’s trading arm before the Dodds-Frank split. It would not be surprising if Morgan Stanley itself only allocates client money, and trading is conducted through affiliated entities. Peter Muller, another legendary quant since 2012, after leaving Morgan Stanley, runs his own business. What NASDAQ’s portfolio report on PDT Partners shows: MicroStrategy has been sold to zero. Coincidence? I don’t think so.

Such firms are not investors; they are highly skilled traders, as demonstrated by driving MSTR to $1300 purely through deft crowd management and pricing expectations of Bitcoin.

The machine is in operation, the machine is well-oiled and working. In my view, MicroStrategy is simply a façade in an interesting and professional operation of the “wolves of Wall Street” and the crowd that feeds off it, from bought bloggers to Michael Saylor. I would urge a rereading of the well-known book “Quants: How the Wizards of Math Made Billions and Almost Destroyed the Stock Market,” which contains much about Muller and Griffin.

Watch the hands — tax optimisation remains in play

To finish, a word on the evergreen topic—taxes. Not being a certified GAAP auditor, but understanding how the tax system works for investment gains and losses, I can venture that for some MicroStrategy holders, as for the company itself, potential losses from investment activity could be used to offset gains in future or past periods—three years back and five years forward. The main provisions of IRS Form 8949 on capital gains and losses, including those relating to virtual currencies, are available to study for interested readers.

For most corporations, short- and long-term investment gains or losses are reported on Form 8949 (Sales and Dispositions of Capital Assets), which is part of Form 1120 Schedule D (Capital Gains and Losses).

First, short-term gains and losses are summed in Part I of Schedule D, long-term in Part II. Then short-term are netted with long-term. The resulting gross capital gains or losses are treated as short-term. For example, a $50 loss and a $10 gain yield a net loss of $40, which can be carried forward to other long-term periods. There are also rules about when and how to account for which period, but that is beyond the scope of this article.

The key point is that gains or losses from one investment can offset gains or losses from another, and across a fairly wide time horizon. Given the ingenuity of American financiers, I am 100% sure that gains or losses from MicroStrategy shares, which are now heavily Bitcoin-dependent, will be used for tax optimisation.

In closing this piece, based on facts and open-source analysis rather than speculation, there is no single manifestation of finance and investment. There is a complex set of often invisible events and transactions that can radically alter your investment history. Always read between the lines.

Follow ForkLog news on Telegram: ForkLog Feed — the full feed of news, ForkLog — the most important news and polls.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!