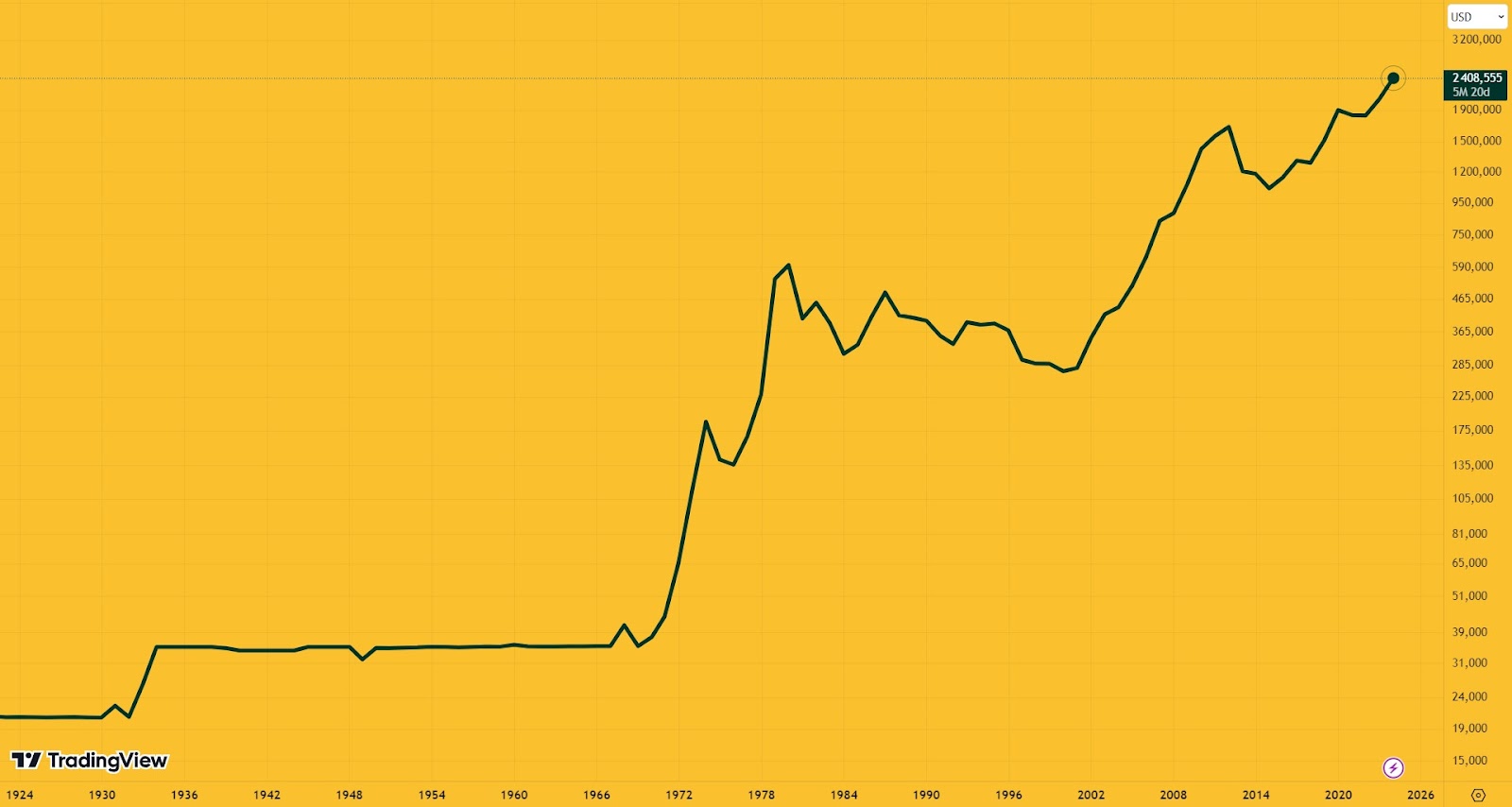

Gold has long been a haven in any economic weather, shielding investors’ cash from devaluation, inflation and market crashes. Its price rose during the dotcom crisis, amid global turmoil and during the pandemic, gaining 1,000% by 2024, by price.

This article surveys the main ways to own gold, explains the value of tokenised precious metals in Web3, and reviews the shiniest, highest-capitalisation projects.

Who guards the treasure

Every market has its standards and rules. The benchmark for precious metals is the LBMA.

The Bank of England began standardising bars and drawing up the first lists of acceptable market participants in 1750. A century later London had five major firms trading gold.

On September 12th 1919, ten months after the end of the first world war, representatives of several banks met at NM Rothschild & Sons to determine a fair price for gold. The Rothschilds set an opening price of £4.92 per troy ounce.

Four participants wanted to buy all available bars. Strong demand added two pence to the price—thus the gold fixing was born. For nearly a century industrial firms, central banks, jewellers and traders used it for bullion transactions and for pricing shares and derivatives.

In 1987 the Bank of England created an independent body to service and regulate the gold and silver markets—the London Bullion Market Association. In 2015 its members replaced the gold fixing with LBMA Gold Price auctions, held twice daily at 10:30 and 15:00 London time.

As of July 15th 2024, the price for 1 ounce of gold is about $2,361. Year to date, it has risen by more than 35%.

Bars, coins and gold ETFs

Once upon a time you could mine or buy gold yourself; over time more investment options appeared. Here are the main ways to acquire it in traditional finance.

Bars—gold from 1 gram to 12.4kg (400 ounces), available from banks, exchanges and private sellers. Quality depends on the proportion of pure gold to alloy metals and ranges from the most valuable 999.9 (99.9% gold content) and 999 to the less expensive 750 fineness.

One advantage is the low barrier to entry. At the time of writing, the international price of a 1-gram 999 bar is about $78.

Drawbacks include storage: banks may discount damaged bars by up to 20%. In the worst case they must be sold as scrap. In some countries purchases are subject to VAT—for example, 10% in Japan and 20% in Russia.

For those who prefer something tangible, there are also investment coins. They are sold by banks, numismatic shops and at auctions. Prices for rare series can soar on the secondary market as collectors pile in. Coins require even more careful storage than bars: damage hurts their price more.

Beyond physical bullion, the market offers other ways to participate:

- futures. Contracts obliging the buyer to purchase an asset from the seller at a set date and price. A high-risk, high-return instrument for short-term bets with low spreads and fees. Futures prices track gold’s moves on the global market;

- gold ETF. Exchange-traded funds whose shares trade on exchanges and whose quotes are tied to gold holdings in their portfolios. Some are backed by physical gold, but not all traders can redeem it: at SPDR Gold Shares redemptions are available to investors with positions from $22m at the current GLD price. ETFs are traded like ordinary securities, but with lower risks;

- gold-mining equities. Their value is driven primarily by the gold price, much as bitcoin moves drive mining stocks. At the time of writing, the top producers are Newmont, Barrick Gold and Agnico Eagle Mines;

- gold mutual funds. Investors buy units; managers allocate to gold-mining stocks and futures. As a result, fund quotes may diverge from the gold price and rebalance participants’ portfolios. The manager decides how to invest for the best returns.

Tokenised gold

The idea is simple: tokenisation unlocks the value of gold reserves, bridging virtual and physical worlds much like the RWA sector. The digitised bullion sits in vaults, typically at banks or other third parties. Most projects let holders redeem tokens for bars.

Gold-tokenisation startups emerged in 2014, when DigixDAO introduced DGD. The first big player came in 2019, when Paxos launched PAX Gold (PAXG). A year later it was joined by Tether Gold (XAUT) from Tether, issuer of the largest dollar stablecoin, USDT.

By now, asset tokenisation is routine in blockchain and has drawn interest from global finance. In April 2023 Zimbabwe’s central bank announced plans for a gold-backed digital currency as legal tender. A year later the British commercial bank HSBC minted “gold tokens” for Hong Kong retail investors.

Advantages of tokenised gold include:

- no need for physical storage;

- tokens are transferable and divisible, lowering entry barriers;

- less volatile pricing than most cryptoassets, aside from fiat-pegged stablecoins;

- the ability to hedge portfolios quickly in times of stress;

- access to derivatives and DeFi mechanics for extra yield.

On CoinGecko, the “Tokenised Gold” category is dominated—at 90%—by Tether Gold and PAX Gold. Here is a closer look at each.

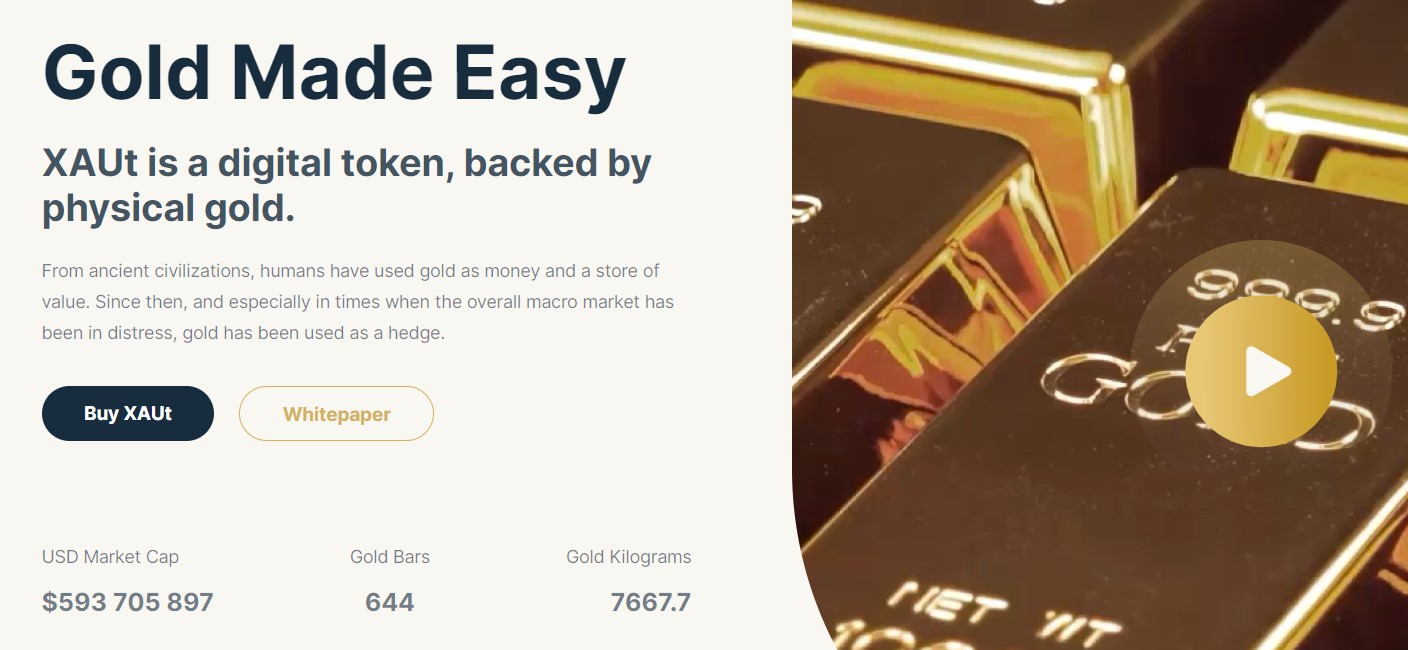

Tether Gold

Tether Gold is issued by TG Commodities Limited, which grants holders an undivided ownership right to specific bars. Each token is backed by one LBMA-standard ounce of gold in Swiss vaults.

XAUT trades on Huobi, Bitget, OKX and other crypto exchanges. Large investors can buy from 50 tokens (~$121,000 at the time of publication) via Tether’s official dapp after creating an account and paying 150 USDT for verification. Redemption from 430 XAUT (~$1m) is also available to them.

The project’s ecosystem includes Tether (USDT), Euro Tether (EURT) and aUSDT, a dollar stablecoin backed by XAUT.

According to CoinGecko, as of July 15th 2024 XAUT’s market capitalisation exceeds $596m, with daily trading volume around $19m.

PAX Gold

PAX Gold is an ERC-20 token from Paxos Trust Company, backed by physical gold and broadly similar to XAUT. Each PAXG is backed by one ounce taken from 400-ounce bars held in Brinks’ London vaults.

The minimum purchase is 0.01 PAXG ($24). The tokenisation fee depends on the amount of gold in a contract but does not exceed 1%. Storage is free; transaction costs are 0.02%.

PAXG holders can stake tokens, earn on centralised exchanges such as Binance, Kraken and KuCoin, and provide liquidity to related pairs on DEX.

At the time of publication, the APY in the PAXG-WETH pool on Uniswap is 3.75%, and PAX Gold’s capitalisation exceeds $443m with daily trading volume above $12m.

Other approaches

According to CoinGecko, at the time of publication tokenised metals have a market capitalisation of $1.28bn, including a digital version of silver. Roughly $30m is accounted for by firms chasing the leaders: VeraOne (VRO), tGOLD (TXAU), and VNX Gold (VNXAU). The first two, in addition to gold and silver, offer tokenisation of palladium and platinum.

Many companies are tapping Web3’s added capabilities and multiple blockchains. Consider a few of them.

Australian financial platform Kinesis Money lets users buy, store and spend precious metals digitally. Its ecosystem includes Kinesis Gold (KAU) and Kinesis Silver (KAG) ERC-20 tokens, each backed by one gram of gold and silver respectively, plus the Kinesis Velocity Token (KVT). Holders of the latter receive a monthly distribution of 20% of the service’s revenue from metal operations.

For transparent, fast cross-border payments Kinesis Money uses the Kinesis Blockchain Network, built with Stellar technology. The main liquidity provider is the precious-metals exchange ABX.

The firm aims to build a new international payments system and is striking partnerships in various countries. In 2021, for example, it integrated its solutions into Indonesia’s state postal service.

As of July 15th 2024, the prices of KAU and KAG are about $77 and $31 respectively. Their combined capitalisation exceeds $214m.

The Comtech Gold platform from the UAE tokenises gold in compliance with Shariah norms and runs on the XinFin blockchain via the XDC Network.

The Comtech Gold (CGO) token, an XRC-20 asset, is backed by one gram of the metal. At the time of publication its capitalisation stands at around $11m.

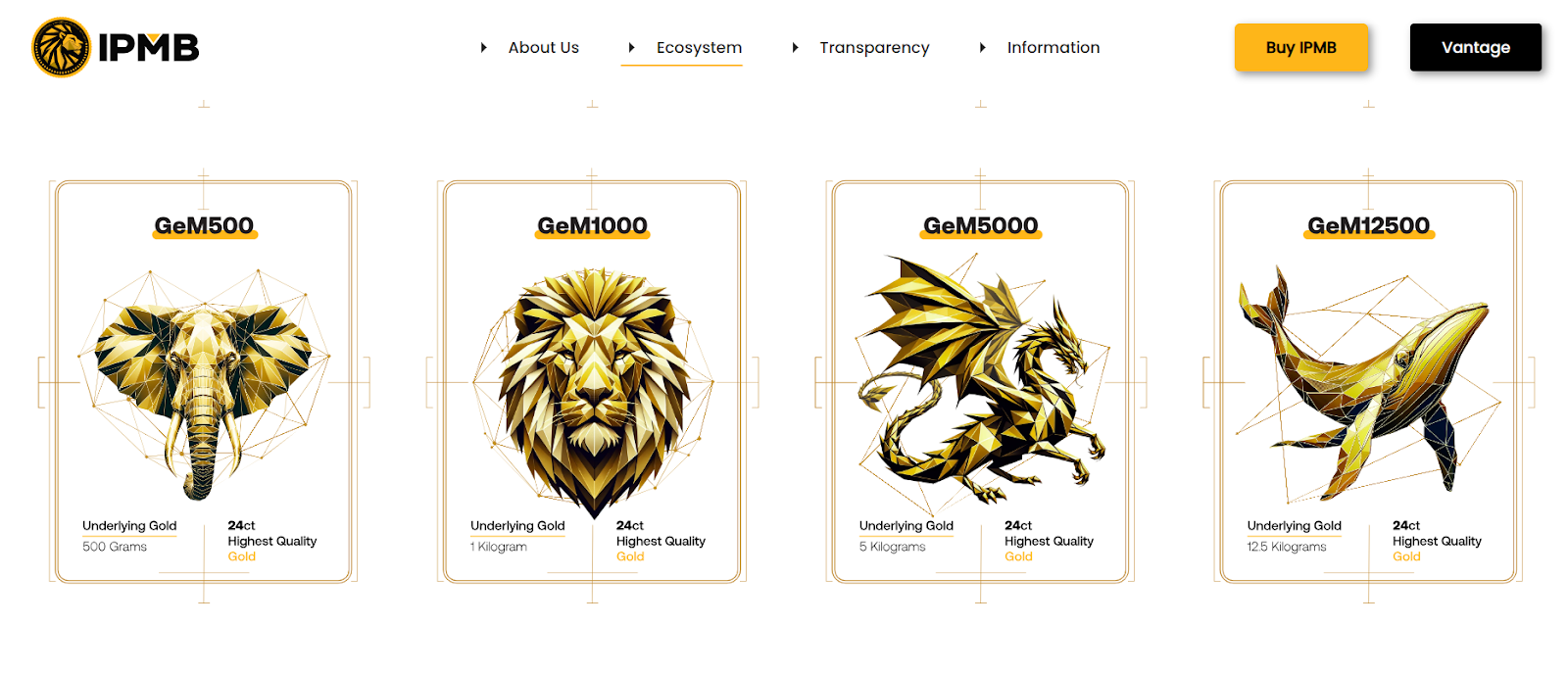

Czech company IPMB offers two types of assets:

- Gem—NFT certificates of ownership of gold, from 1 gram to 12.5 kilograms;

- IPMB—a utility and payment token backed by one gram of the metal, but not pegged to its price.

According to the project’s official page, as of July 15th 2024 IPMB trades above $86, with a market capitalisation approaching $299m.

Startup Meld Gold from Australia tokenises gold and silver. In June 2024 the team struck a partnership with Ripple Labs.

According to Meld Gold, in the third quarter the service will add support for the XRP Ledger (XRPL) alongside Algorand.

Conclusions

Gold-backed tokens are still a relatively new concept, so there is no guarantee they will preserve value or that issuers will meet their obligations. Some projects also struggle with liquidity owing to limited listings on leading exchanges.

On the other hand, such tokens remove frictions that plague traditional gold trading and offer more advantages than products like ETFs.

Fractionalisation lowers the barrier to entry for tokenised precious metals. As the technology matures, expect broader use-cases and added DeFi mechanics, including borrowing and lending.

Text: Sergey Golubenko