“A whale that slept for 100 years transferred all the world’s bitcoins to FTX”: a critical look at on-chain analytics

The rise of crypto has spawned entire business lines and disciplines. One of the most popular is on-chain data analytics.

This field uses information about the behaviour of users and investors to anticipate price moves. Such analysis is built on, or incorporates, data taken from blockchains.

Despite its convenience for professional traders and casual users alike, it carries many risks. Here is how such data are used to manipulate communities and markets.

When on-chain analysis becomes a problem

Most often, on-chain analysis means monitoring transactions. The premise is that movements of coins and tokens, along with other information extractable from a blockchain, can reveal the motives of users from an investment or speculative standpoint.

The trend took off with the first on-chain indicators. Their boom came in 2016–2017, when most of today’s staples appeared, including Hodl Waves, NVT Ratio, MVRV Ratio, the Puell Multiple and Hash Ribbons.

Yet the popularity of on-chain data—and the influx of new observers and participants—can itself become a problem for crypto. Here is why.

As of June 2024, Whale Alert had more than 2.4m followers on X, and its posts can prompt buying or selling of assets. Despite the vast user base, the platform periodically flags transactions as suspicious at its own discretion and spreads inaccurate information.

On April 1 2022 Whale Alert posted that 6,800 BTC had been moved from an address belonging to Mt.Gox to an unknown wallet.

? ? ? ? ? ? ? ? ? ? 6,800 #BTC (318,980,017 USD) transferred from #MtGox Cold Wallet to unknown wallethttps://t.co/sYczH1c8ho

— Whale Alert (@whale_alert) April 1, 2022

Soon it emerged that the transaction had nothing to do with the exchange, but the media had already amplified the “leak”. Disinformation spread fast. It helped that, days earlier, the exchange’s chief, Mark Karpelès, had said he planned to redistribute $6bn worth of BTC to creditors. It is hard to count how many users may have made panic trades on the back of this.

Whale Alert often errs during bouts of market stress. In 2020 the service pointed to BTC moving from a Mt.Gox address on the very day BitMEX announced a leadership change. That came a week after America’s authorities charged the firm’s founders.

95 #BTC (1,006,164 USD) transferred from #MtGox Cold Wallet to unknown wallet

Tx: https://t.co/GIzKcAHtYe whale_alert

— Crypto Bert (@CryptoBert1) October 8, 2020

These two episodes are only a small sample of many mistakes. All Mt.Gox addresses had been known to the community for years, yet Whale Alert labelled them at its discretion, later citing mislabelling.

This matters: unreliable data warp the understanding of market conditions and can cause financial and reputational damage.

Quite often such services simply do not know who owns the bitcoins. In December 2018 the leading American exchange Coinbase moved 5% of BTC, 8% of ETH and 25% of LTC of the then total supply. No one knew whose assets they were until the exchange said so.

The on-chain analytics market has matured, but the same mistakes persist. And as blockchain data grow more popular, credulous users may internalise these misconceptions and apply them to future trading or investment decisions.

The main logical errors in reading transactions

To understand the basic mistakes in analysis—and in forming opinions based on token movements—you need to know how deposits and withdrawals work at exchanges and other platforms.

As the diagram shows, before funds are moved to an exchange hot or cold wallet, they are credited to a personal address the platform created for the user. Assets land there first and, depending on the platform’s algorithms, can sit for a long time before moving to a known wallet.

Everyone has seen headlines that “an unknown whale sent N thousand BTC to exchange X”. This is the first, central mistake in transaction analysis. Services like Whale Alert are usually showing a transaction that an exchange is making between its own addresses—from a user’s deposit address to its hot or cold wallet.

In such cases the assets may have been on the exchange for some time; the user may already have traded or withdrawn them elsewhere. Observers are merely seeing an internal operation in which client deposits are consolidated and sent to another hot wallet—or to cold storage.

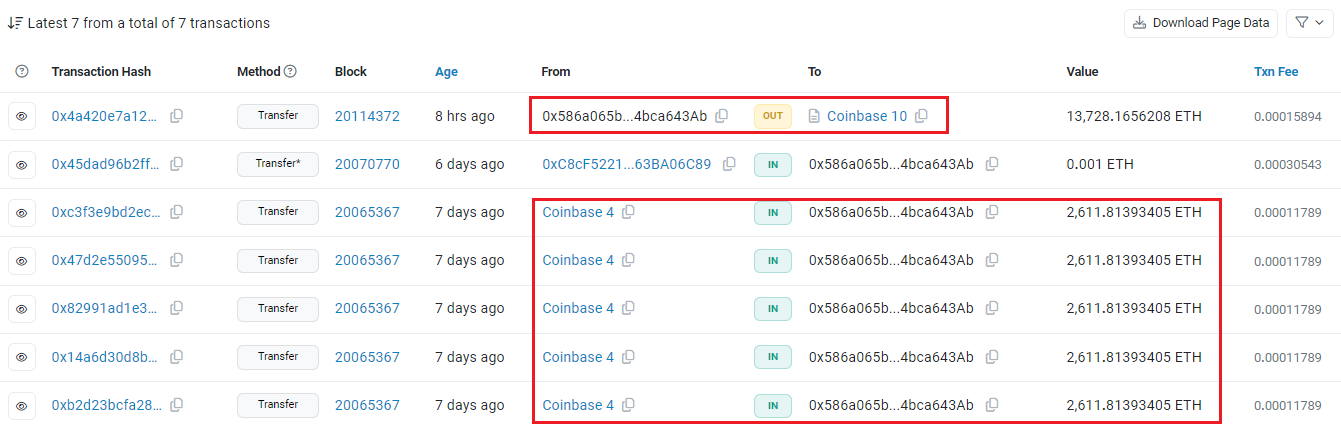

A recent example of such posts: 13,728 ETH were moved from an unknown wallet to Coinbase.

? ? 13,728 #ETH (47,338,996 USD) transferred from unknown wallet to #Coinbasehttps://t.co/475jGqQ9ln

— Whale Alert (@whale_alert) June 18, 2024

These are often packaged as: “Whales are sending ETH to exchanges to sell.” This is especially common during market stress. Look under the hood of the transactions and the address history, though, and a different picture emerges.

Etherscan showed the address was topped up directly from a Coinbase wallet seven days earlier, and then sent back in a direct transfer. It is therefore highly likely to be a routing address used by the exchange—unrelated to users and not a fresh external deposit.

Another common error is to ascribe an intention to a transaction. A blockchain does not reveal motives. At best, we are guessing.

In DeFi applications a user’s actions are visible step by step; a simple transfer from one address to another leaves too many possibilities. We cannot see what is happening inside a centralised venue. For the Coinbase example above, possibilities include:

- the exchange replenishing a hot wallet amid elevated ETH withdrawal demand;

- an over-the-counter buy or sale;

- a Coinbase Prime client requesting an ETH withdrawal from custody or making a deposit;

- a block buy or sale;

- routine internal rebalancing between addresses.

Shaping public opinion

Such data are hugely popular with retail users. That creates fertile ground for manipulating public opinion for gain.

Even if guesses about a transfer’s purpose are correct, the lack of a full picture can still lead to poor decisions. The information will be used to sway the crowd.

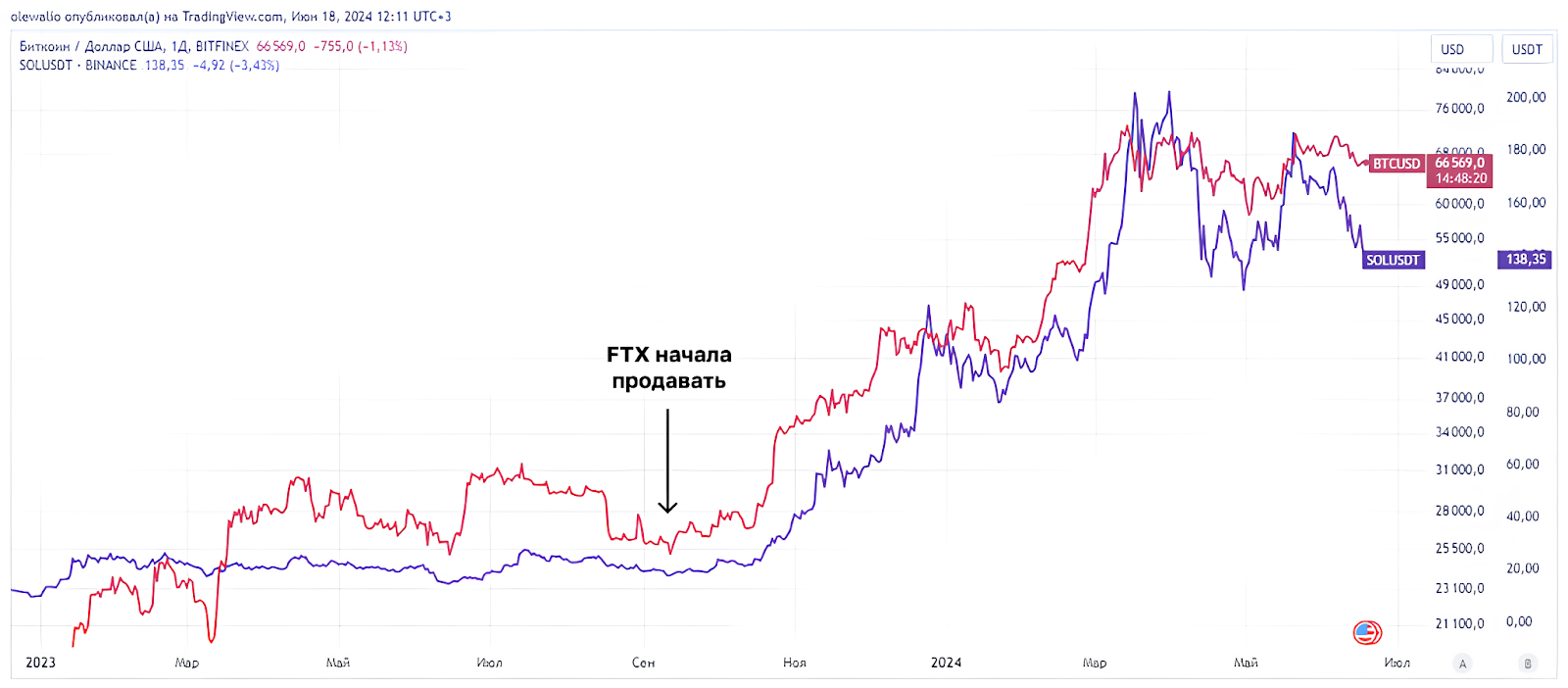

Consider what influencers and analysts cited in autumn 2023 when discussing asset sales by the bankrupt exchange FTX.

“More than $1.5bn in SOL, SPL tokens and ‘wrapped’ bitcoins are moving on the FTX address in Solana. It looks like they are preparing for potential sell-offs. Watch this, especially the ~$200m in bitcoins on Solana,” said Pump House.

The plan envisaged the exchange being allowed to sell up to $100m of tokens per week, with scope to raise the cap. The assets were worth around $7bn in total.

Now look at the price of bitcoin and SOL after those moves began.

From early September 2023 the prices of bitcoin and SOL multiplied. The forecasts about FTX sales diverged sharply from what the market did.

Traders and investors swayed by panic—and by taking analysts and influencers at face value—may have chosen poor strategies and lost money.

Author — Oleg Cash Coin.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!