AFX vs Hyperliquid

Why the market needs another perp-DEX

By spring 2026, Hyperliquid had become the de facto standard in the perp-DEX segment. According to CoinGecko, in April the platform processed $190.28 billion in trades (about 3.9% of the total volume), ranking ninth among all perpetual futures venues, including centralized exchanges.

Yet the infrastructure problems of on-chain derivatives have not gone away. Meme-coin manipulation and unstable mark-price behavior under heavy load remain weak spots, and competitors are trying to answer them with their own architectural designs.

On May 18, 2026, AFX joined the race — an L1 network built specifically for perpetual futures trading. Together with the project team, ForkLog examines how AFX is designed and how its approach differs from Hyperliquid.

Hyperliquid sets the bar

Hyperliquid combined a full on-chain order book with the user experience traders are used to from centralized exchanges. In October 2025, the protocol activated the HIP-3 upgrade, which allows any developer to launch a perpetual futures market on top of HyperCore by staking 500,000 HYPE. The market creator defines the contract specifications, oracles, leverage limits and settlement parameters, and can claim up to 50% of the fees.

This mechanic quickly pushed Hyperliquid beyond the crypto-native perimeter. The platform became a round-the-clock venue for macro-risk trading: during the escalation of the Middle East conflict, the CL-USDC contract tied to WTI crude reached $1.1 billion in volume with open interest above $274 million.

The segment leader has been through several stress tests. In March 2025, Hyperliquid faced manipulation around the meme-token JELLYJELLY: attackers exploited features of the liquidation mechanism and the asset’s thin liquidity, leaving the Hyperliquidity Provider Vault (HLP) with roughly $12 million in unrealized losses. The team had to halt trading manually and delist the contract.

A new incident happened in November of the same year, this time with the meme-coin POPCAT. According to on-chain analysts, the attacker withdrew about $3 million in USDC from OKX, split the funds across 19 wallets and opened a combined long of roughly $30 million. When the trader pulled the wall of buy orders, his $20–30 million position was liquidated within seconds. The losses passed to the exchange’s liquidity provider (HLP), which lost $4.9 million. Amid manipulation suspicions, Hyperliquid temporarily paused deposits and withdrawals.

These episodes did not break the business model, but they marked specific scenarios in which Hyperliquid behaves differently from how its documentation reads. They also became reference points for the next generation of projects.

An L1 built for the order book

AFX positions itself as a Sovereign Trading Layer — dedicated infrastructure for professional derivatives trading. The team rejected a general-purpose blockchain and assembled its own stack: a custom execution layer, the Mysticeti consensus based on DAG BFT, and a modular structure built on ABCI/Cosmos SDK. Execution and consensus are separated, so the order flow is handled independently of other network processes.

Hyperliquid also runs on its own L1 and builds its infrastructure around HyperCore — an on-chain engine for spot and perpetual markets with an order book and price-time priority matching. Through HyperEVM, developers can tap into HyperCore liquidity and build applications inside the ecosystem.

AFX took the opposite direction: instead of an ecosystem horizontal, it focused on the trading-stack vertical — blockchain validator, mempool, DAG consensus, ABCI communication layer, virtual machine, accounts module, bridge and trading engine are packaged into a single system where the matching logic is physically separated from consensus and cannot be slowed down by it.

The venue added two more elements geared toward professional flow:

- Zero gas fees remove friction from placing and canceling orders, so traders’ decisions no longer depend on transaction cost.

- Protection against MEV is built through a dedicated mempool and an execution architecture that separates the order sequence from regular on-chain traffic.

A dedicated trading layer gives AFX more control over mempool behavior, transaction flow and execution logic than a DEX deployed on top of a congested general-purpose blockchain.

At launch, four contracts went live: bitcoin and Ethereum with up to 40x leverage, plus gold (XAU) and crude oil (CL) with up to 25x. At the time of publication, the venue had added Solana, XRP, silver (XAG) and HYPE. Margin is in USDC.

Deposits go through the Arbitrum network, with connection via MetaMask, Rabby, Coinbase Wallet or the WalletConnect protocol. The starter set of assets is telling: AFX is moving into the same niche where Hyperliquid is already setting records on macro assets and RWA.

Not just speed

Hyperliquid set a high bar: orders are filled in about 0.2 seconds on average, and even in rare cases of heavy delay, in roughly 0.9 seconds. AFX claims about 0.12 seconds to process a typical order, more than 50,000 operations per second and headroom to scale to 100,000–200,000.

But comparing raw numbers does not show the whole picture. In quiet periods almost any large exchange runs fast. The real test comes during sharp market moves, when positions are closed en masse, funding rates change abruptly and trading bots fire off massive numbers of orders at once.

“In moments like that, what matters is not just peak system speed but how stably the platform performs under load: how fast it processes and cancels orders, how it manages the order queue and how predictably it executes trades. AFX’s trading system is built first and foremost to preserve stability and predictability during peak load,” AFX contributors say.

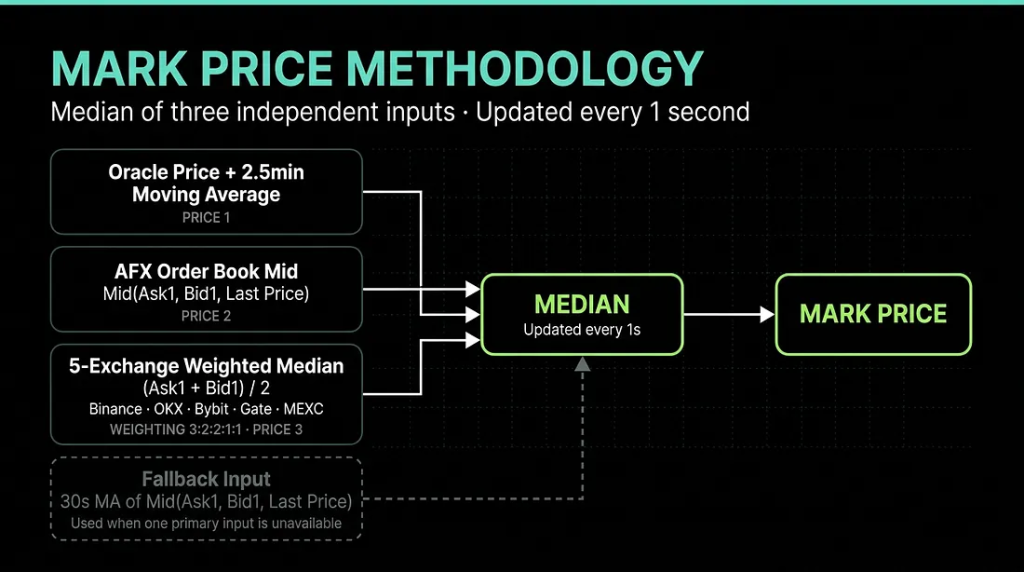

Mark price from three sources

Mark price is the contract’s reference price that the exchange uses to calculate margin, PnL, liquidations and conditional-order triggers. On thin markets, the last-trade price can be moved sharply by a single large order. If mark price depends too heavily on the local order book, it opens the door to manipulation and forced liquidations.

AFX calculates mark price as the median of three independent components:

- an external oracle price for the underlying asset, smoothed by a 2.5-minute moving average;

- the mid of AFX’s own order book;

- a weighted median of the mid for the same contract on the centralized exchanges Binance, OKX, Bybit, Gate and MEXC, with weights of 3:2:2:1:1 respectively.

If one of the sources returns abnormal data because of order-book manipulation, an oracle failure or a stuck feed from an external exchange, the median simply ignores it and takes the middle value. To shift the mark price noticeably, an attacker would have to influence at least two independent sources at once. The calculation refreshes once per second.

In practice, this reduces the risk of false liquidations during short-term dislocations in the local order book. A stop-loss triggered by mark price will not fire on a single spike in AFX’s order book if the rest of the market remains stable.

Orders triggered by the last trade price, on the contrary, react to that local move. The user chooses the trigger type, but the mark-price architecture makes the classic single-book manipulation attack significantly harder.

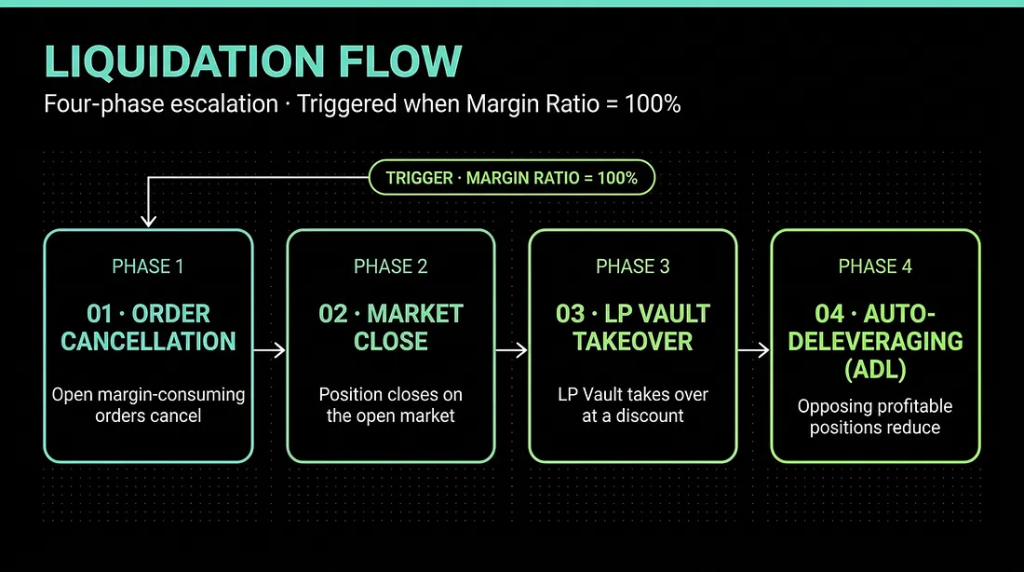

Four phases of liquidation and the role of the LP Vault

Cascading liquidations are one of the main stress tests for on-chain venues. AFX uses a four-step defense system that gradually tightens as the value of assets in the trader’s account approaches the minimum collateral threshold for the position.

The first step cancels open orders that have funds reserved against them. The system first tries to free up capital without forcibly closing the position itself.

If that is not enough and account equity drops below the maintenance margin, the second step kicks in — forced closure of the position on the open market. If any funds remain after the close, they are returned to the trader.

The third step is triggered if a normal liquidation can no longer stabilize the account — for example, during a sharp market move, when a position races into deep loss. At that point the LP Vault (or ALP) takes on the open position and the trader’s remaining funds, becoming the counterparty to the trade and assuming the risk.

The fourth step is the auto-deleveraging mechanism (ADL). It is used only as a last resort: if the LP Vault’s own funds go negative after absorbing a losing position, the system begins to cut profitable opposing positions of other participants to cover the remaining loss.

The LP Vault is the system’s main protective buffer in this model. The pool supplies liquidity to the order book, absorbs liquidated positions and takes on part of the risk during sharp market moves. ADL remains a backstop for cases where even the LP Vault cannot cover the losses in full.

Pro-grade orders and cross-margin

In cross-margin mode, AFX lets traders use unrealized profit as additional collateral. If an open position moves into the green, available margin increases automatically — there is no need to close the trade and withdraw the profit first. That makes capital handling more flexible: a trader can scale into a position, add a hedge or rebalance a portfolio without extra steps.

Hyperliquid also develops its margin system: its documentation describes margin tiers that set maximum leverage and maintenance margin requirements.

“The difference is in emphasis. Hyperliquid built one of the strongest on-chain perpetuals ecosystems. AFX enters the market with capital efficiency as a core architectural principle, targeting traders who run a portfolio of several positions and expect margin logic at the level of a professional trading system,” AFX representatives comment.

The platform offers three order types. Market orders let the user cap allowed slippage in a 0.5%–5% range. Limit orders support the main execution modes — GTC, IOC, FOK and Post-Only. Conditional orders (stop-market and stop-limit) can be triggered by either the last trade price or the mark price. The roadmap also lists TWAP execution and a hedge mode with a simultaneous long and short on the same pair, but these features are not yet available at launch.

Base fees are 0.01% for makers and 0.06% for takers. Under the VIP program, the rates drop as 30-day volume grows — both the main account and sub-accounts count toward the total. Users at the top VIP tiers also receive a share of the platform’s fee revenue.

The referral program works through wallet attribution: after following a unique link, a user is bound to the inviter, and rewards are recalculated daily based on the referred network’s total trading volume.

Betting on quant traders and market makers

In the AFX team’s view, the bulk of on-chain derivatives volume over the coming years will be generated not by retail traders through the interface, but by market makers, quant traders, copy-trading communities and AI agents.

Hyperliquid has mature documentation and API infrastructure, yet that same documentation spells out the limits advanced users hit. Each account gets 1,000 open orders by default, with a ceiling of 5,000 as volume grows. When the 1,000-order cap is reached, the platform may reject reduce-only and trigger orders.

“AFX is designed around the needs of professional clients from day one. The long-term goal is to attract not the trader looking for a decentralized alternative to Binance or Bybit, but the trader who wants to run a full trading operation on-chain without giving up execution quality,” AFX emphasizes.

A token economy without VC

On the token side, AFX leans on the absence of a venture round, private allocations or pressure from future unlocks. The project frames the launch as oriented toward active traders, liquidity providers and the community rather than early-round investors. The token itself has not been issued yet.

At launch, the team rolled out trader incentive programs: a VIP system that cuts maker and taker fees as volume grows, and a referral model with wallet attribution and fee sharing.

The approach echoes the Hyperliquid model: launch the infrastructure and build liquidity first, then distribute the token through user activity rather than classic venture rounds.

“Hyperliquid has one of the strongest communities in DeFi, and that is one of the reasons it became the segment leader. AFX can build on the lessons of the first wave with a sharper focus on community-driven economics,” AFX adds.

Trading activity before the token appears forms the base for the future genesis distribution, and traders building volume and liquidity now are positioning themselves for an airdrop. Hyperliquid walked a similar path: its November 2024 distribution became the most generous in history, valued at around $10.8 billion at the asset’s peak. The platform has grown steadily in trading volume since then, and the HYPE token continues to set new all-time highs in June 2026.

The experience of dozens of other projects, however, shows that liquidity that arrives for a drop often leaves in the first weeks after distribution.

Two things will be critical for AFX: the structure of the genesis distribution, and whether it can retain professional participants once the early-stage incentives run out. Without the latter, even a technically excellent order book risks being left with a thin book.

AFX and Hyperliquid: comparison table

| Parameter | AFX | Hyperliquid |

|---|---|---|

| Positioning | Sovereign Trading Layer for professional on-chain derivatives | On-chain order-book perp-DEX + spot + app ecosystem |

| Order book | Fully on-chain | Fully on-chain, price-time priority matching |

| Consensus and architecture | Mysticeti DAG BFT, ABCI + Cosmos SDK, modular structure | HyperBFT, HyperCore + HyperEVM |

| Latency | ~120 ms P50 | 0.2 s median for co-located clients |

| Throughput | 50,000+ TPS; theoretical ceiling 100,000–200,000 TPS | HyperCore optimized for high-performance on-chain trading |

| Execution model | Execution and consensus separated | HyperCore handles trading logic natively |

| Margin | Reuse of unrealized PnL, cross-positions, real-time risk control | Margin tiers and maintenance margin system |

| MEV protection | Dedicated mempool and execution architecture | On-chain order book and transaction-sequencing rules |

| Target audience | Professional traders, quants, HFT, market makers, trading communities | Retail traders, professional traders, developers, ecosystem users |

What time will show

AFX’s tech stack addresses specific bottlenecks of on-chain perps: a three-component mark price reduces the risk of price manipulation, the four-step liquidation system with an LP Vault adds an extra buffer between a losing position and the rest of the market, and the reuse of unrealized profit in cross-margin mode improves capital efficiency for professional trading strategies.

The coming months will show what marketing materials could not:

- whether AFX holds its stated latency and mark-price behavior during episodes comparable to JELLYJELLY and POPCAT on Hyperliquid;

- whether the LP Vault can absorb liquidated positions in the first genuinely massive cascade without triggering ADL;

- whether professional market makers come in before and after the genesis token distribution;

- how the token distribution structure plays out.

The gap to Hyperliquid is unlikely to close quickly in the near term. The segment leader has built a full ecosystem, and its token keeps setting new all-time highs above $60. The very interest in platforms of this kind and the growth of the biggest player can also be a positive signal for AFX, confirming sustained demand for on-chain derivatives.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!