Despite significant inflows into BTC-ETFs, arbitrage strategies between spot and derivative markets are restraining buyer pressure, according to Glassnode.

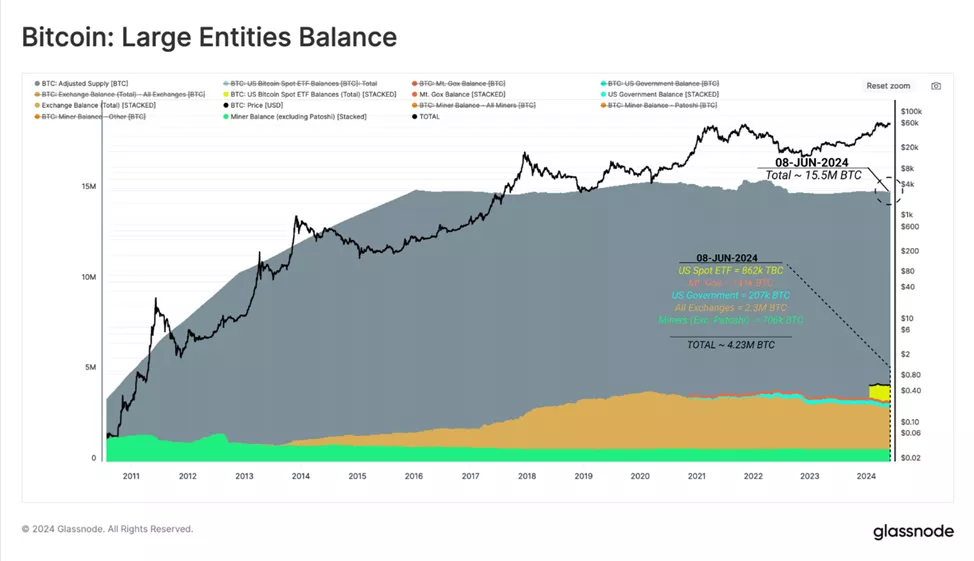

To substantiate and assess ETF demand, analysts compared the balance of product issuers (862,000 BTC) with other major exchange structures:

- Mt.Gox trustee = 141,000 BTC;

- US government = 207,000 BTC;

- all exchanges = 2.3 million BTC;

- miners (excluding Satoshi Nakamoto) = 706,000 BTC.

The combined balance of these holders is estimated at ~4.23 million BTC, equivalent to 27% of the total adjusted available supply (excluding coins inactive for over seven years).

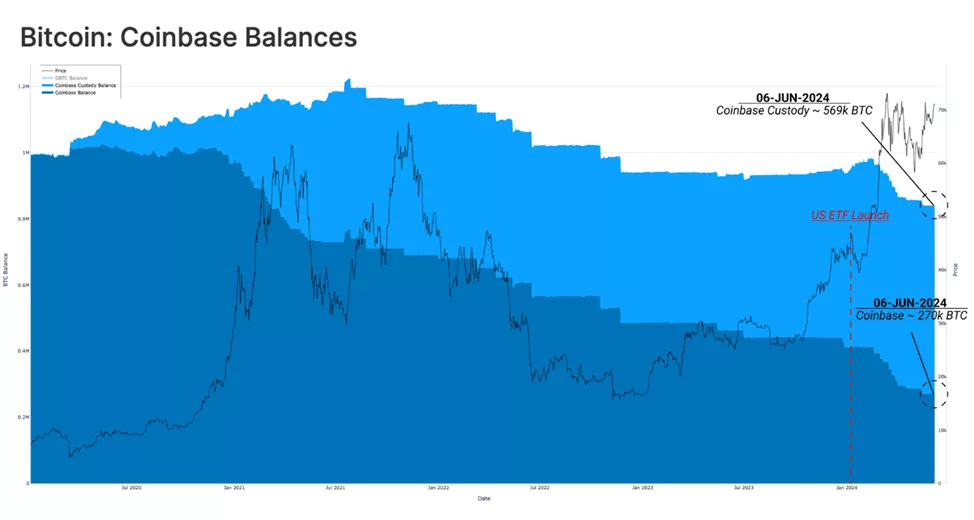

Among exchanges, Coinbase stands out. The platform has strengthened its position following the ETF launch, acting as custodian for eight of the 11 products. Coinbase Custody holds 569,000 BTC, while the exchange itself holds 270,000 BTC.

Evaluating the number of whale deposits in Coinbase’s exchange wallets, analysts noted a significant increase in this metric following the ETF launch.

A substantial portion of transactions is linked to the outflow of funds from Grayscale’s GBTC address cluster.

In addition to GBTC’s selling pressure amid the market rally to new ATH, the rise in the use of the cash and carry strategy also contributed to the reduced demand for ETFs.

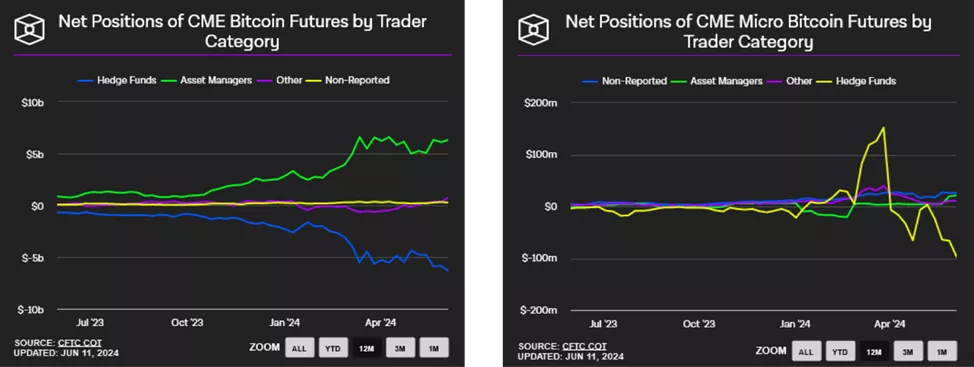

This hypothesis is supported by the stabilization of open interest in bitcoin futures on the CME at $8 billion after a record high of $11.5 billion in March 2024.

This arbitrage strategy involves a market-neutral position, formed by going long on the spot market and shorting futures on the same underlying asset trading at a premium.

Analysts observed an increase in net short positions on digital gold by hedge funds.

This led experts to suggest that the cash and carry trading structure could be a significant source of ETF demand, where exchange-traded products serve as a tool for obtaining a long position on the spot market.

On the CME, there is also a sharp increase in both open interest and the platform’s share to highs not seen since 2023. This indicates that hedge funds prefer trading futures through this venue, analysts added.

According to Glassnode’s calculations, this category of participants has formed a net short on the CME in standard and micro bitcoin contracts amounting to $6.33 billion and $97 million, respectively.

As noted by K33 Research, the significant inflow into BTC-ETFs largely reflects demand rather than arbitrage between spot and futures markets.

Previously, analyst Ali highlighted signs of a volatility spike and significant risk.