“Buy when everyone is fearful, and sell when everyone is greedy.” This Warren Buffett principle is familiar to anyone with even a passing interest in investment theory.

How best to apply it to bitcoin has been examined by Oleg Cash Coin.

ForkLog is not responsible for readers’ investment decisions or the outcomes that may result from using the investment recommendations presented in this article.

Saylor’s method

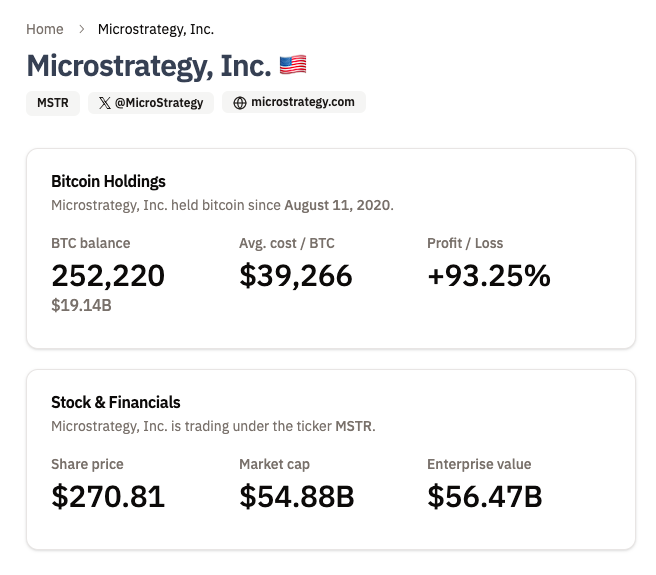

One of the leading evangelists of applying the HODL concept among institutions was MicroStrategy’s chief, Michael Saylor. By raising debt, diluting its equity and using derivatives, the company has accumulated more than 252,000 BTC since 2020.

Japan’s Metaplanet offers a recent example: in less than a year in 2024 it added 850 BTC to its assets. To achieve this it used borrowed funds as a hedging instrument for its digital-gold position in the options market.

The firepower of large public firms is hardly available to ordinary users who want to accumulate the first cryptocurrency. They may, however, find modified DCA strategies—dollar-cost averaging—useful.

DCA entails buying or selling an asset gradually in small, equal tranches rather than deploying the full amount at once. This reduces trading and psychological risks, enabling a clear, workable plan.

Most investors pick simple entry intervals—daily, weekly or monthly. That helps budget funds and build a realistic long-term accumulation plan.

Taking bitcoin’s average annual return over the past 13 years yields roughly 99%. Over the past ten years the average return was 66%, and over five years 51%.

These are not the “x” multiples some influencers tout, but what other asset delivers an average of 50% a year? Moreover, bitcoin simply sits in a cold wallet with no obligations to anyone. That is what Saylor means when he talks about the returns of digital gold:

“I consider it far more rational to borrow $1bn in the fixed-income market and put it into bitcoin at 50% per annum with no counterparty risk than to look for someone willing to pay me 12–14%.”

As a more down-to-earth example, consider the optimal way to buy a set amount of bitcoin once a month—say, after payday.

Although DCA is simple and quickly becomes a habit, many try to refine rough edges that could lift returns without increasing risk over long stretches.

Buying the fear

The idea of optimising DCA via market sentiment rests on the premise that buying assets during panic and fear is the most “advantageous” investor behaviour. You probably know this as Warren Buffett’s oft-advertised formula: “Buy when everyone is fearful, and sell when everyone is greedy.”

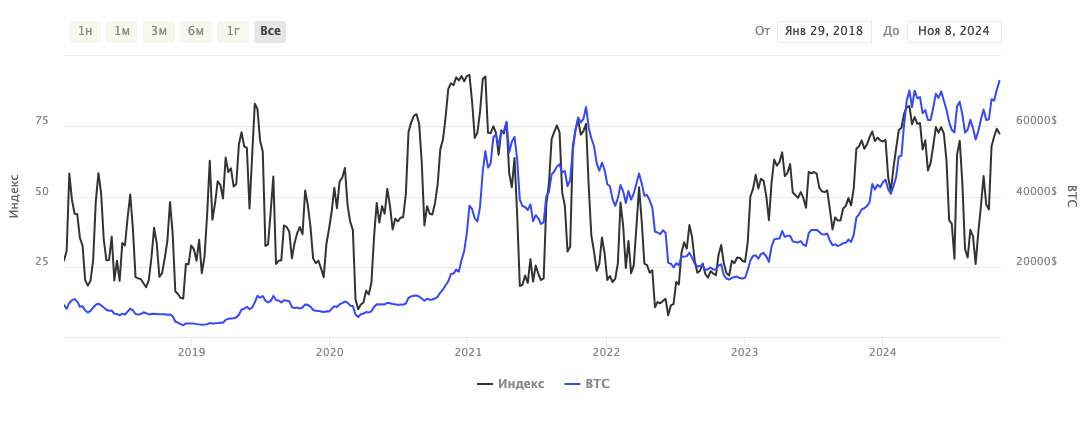

Crypto has a simple gauge for this—the fear and greed index. On that basis one may assume that readings from 0 to 26 are optimal moments for investing.

This hypothesis can be tested statistically over one-, three-, five- and six-year horizons by comparing standard once-a-month DCA with DCA during “Extreme Fear”.

The cardinal rule is to invest the same amount every time; otherwise averaging behaves differently, altering the logic of the calculations.

Classic DCA shows returns of roughly 366% over the past six years (the period is chosen because the fear and greed index has been around only since 2018) and 220% over the past five. Over three years the figure is about 104%, while a year of monthly bitcoin purchases yields 26%.

It is easy for early bitcoiners to preach HODL when any $1,000 move today means only ~1.5% of a new user’s deposit. For “old hands”, the same price change can mean 2x or more.

It must be acknowledged: early HODLers are on the far side of a chasm from the average user who is just starting to accumulate bitcoin. Unrealistic promises of easy wealth only push newcomers away, disappointing them before they begin.

To reduce noisy fluctuations in the index, let’s set a rule: buy bitcoin on the second day after the gauge drops below 26 (“Extreme Fear”). That way the market is clearly in panic, rather than an accidental dip into the critical zone.

The snag is that during bull phases chances to invest are scarce: prices spend most of the time in the “green zone” and fear is rare.

Results

Over the past year since October 2023 there were only two opportunities to invest, which would have produced roughly 8% annualised—a modest figure even for the traditional banking sector.

The three years since October 2021 would have allowed 22 entries at an average bitcoin price of $31,700, delivering around 211%.

Five years of investing only on the second day of “Extreme Fear” would have offered 35 entry points at an average digital-gold price of $19,300, yielding 347%.

Over six years, fear-index investing would have provided 62 chances to enter the market at an average bitcoin price of $10,140 (around 660% on the deposit).

Thus, classic DCA trails the returns from buying when everyone is afraid. The strategy has a serious drawback, however: few opportunities to purchase during a rising market. It is likely optimal for prolonged bear trends.

Sentiment-based investing can also be optimised on the sell side—liquidating part of one’s holdings during “Extreme Greed”. These observations suggest that Buffett’s principles are quite applicable to bitcoin.

It is, of course, convenient to crunch numbers in hindsight. But over the past six years, market panic could have multiplied the returns from bitcoin allocations.

The three-year period is particularly striking: plain DCA would have delivered 104%, whereas fear-based DCA exceeded 200%. The difference is colossal, even for a statistical sample.