The launch of spot bitcoin ETFs in the United States marked recognition of cryptocurrencies as a financial asset class and their true mainstream adoption. Yet die-hard critics of digital gold such as Jamie Dimon and Peter Schiff still dismiss the evidence.

For example, JPMorgan’s CEO recently said bitcoin lacks the fundamentals of a currency, calling it “a decentralized Ponzi scheme.” In a similar vein, the president of Euro Pacific Capital argues the first cryptocurrency has no intrinsic value.

Yet contrary to the sceptics’ forecasts, bitcoin has been around for more than 15 years. Digital gold is held by millions of people worldwide, by large companies, by Fidelity and BlackRock clients and even by some states.

ForkLog offers an adapted translation of the report Your wealth is melting by Unchained, which highlights the distinctive properties and advantages of digital gold versus other asset classes.

- Unchained specialists warn of the risks of “wealth erosion” amid rapid technological innovation and economic uncertainty, positioning bitcoin as the most reliable alternative to traditional assets.

- Experts believe fiat currencies, bonds, equities and other popular stores of value are subject to inflationary pressures.

- Accelerating technological progress and competitive forces affect multiple industries, underscoring the need to hold assets that can preserve value over time.

Innovation’s double-edged sword

“Bitcoin is the hardest money ever invented: rising value cannot increase its supply.”

Saifedean Ammous. The Bitcoin Standard

In an era of breakneck technological progress and exponential productivity gains, saving for the future faces growing uncertainty. The prevailing view is that investing in the “Magnificent Seven” tech stocks or in single-family homes promises hefty returns. That approach has served market participants for decades, but will the trend persist?

Many instinctively answer “yes,” citing the constant stream of innovation. The rapid advance of technology over the past two centuries has materially raised social welfare. Human ingenuity has sharply lifted our productivity in everything from food to housing, and it seems logical to invest in that relentless progress.

Yet innovation can be a double-edged sword. Traditional ways of preserving the income generated by rising productivity run into obstacles. So, although one might reap sizeable gains in the short run, all asset classes are vulnerable to what might be called the “innovation trap” — market forces, driven by human action, that erode the capacity to accumulate wealth over the long term.

Until now we have had no proper vehicle to carry wealth through time without leakage. For too long, people have relied on assets that can be produced without limit and are naturally debased by competitive markets.

Bitcoin restores the ability to draw a clear line between investing and saving. Holding the first cryptocurrency in cold storage may deliver the highest risk-adjusted returns over the long run.

In a world where digital gold is spreading, it sets new benchmarks for judging investment performance, allowing savings to compound faster than those tied up in producers and other traditional assets.

Bitcoin may be the only instrument capable of shielding your wealth from the inevitable attrition wrought by market forces.

Abundance and deflation

Calculators were once luxury items in wealthy households. In the early 1970s the first devices cost around $400, or roughly $3,000 in today’s money. Today they are free on every computer, in Google search, on the iPhone and even through smart-home devices.

While investing in calculator manufacturers may have made sense at the time, over the long run the financial gains and new wealth did not accrue to the firms making such devices and their software. Instead, the consumer came out ahead, enjoying the convenience of a free calculator.

Technological advances radically changed the design and distribution of these simple computing tools, sharply reducing production costs. Companies now often bundle free calculators into their services as a complement to core products. This means users can access as many such apps as they like at no extra cost.

Competitive markets inexorably squeeze value out of traditional assets and industries. Imagine a raft of advances in AI and robotics that fully automate the growing and distribution of strawberries, transferring decades of digital innovation to the physical world and eliminating the need for human labour.

Companies deploying such technology would initially see production costs plunge (by ~99%) while still selling berries at prevailing market prices. That would generate a surge in income, attracting hefty investment and interest in the sector.

But such high profits would be unlikely to persist for long. As new entrants adopt the same technology, competition intensifies and the selling price of strawberries falls for everyone. A market bent on efficiency would gradually compress profits to zero.

As with calculators, the principal beneficiaries of such technological progress are not necessarily producers or investors, but consumers.

In a world with a fixed money supply, prices should fall as abundance rises, reflecting the roll-out of new technologies, greater market efficiency and lower production costs.

“With abundance comes deflation. It is simple supply-and-demand economics: the more abundant something is, the more likely its price will fall,” writes Jeff Booth in The Price of Tomorrow.

Accelerating production

As technology has advanced, industries have been transformed, dramatically boosting labour productivity. Since 1900, for example, global energy output has increased many times over.

Agriculture

Another example of rapid productivity growth is agriculture. In the 1930s a single American farmer could feed four people. By the 1970s that figure had risen to 73 thanks to mechanisation and more efficient processes.

By the 2010s, one farmer fed 155 people. Thanks to new technologies, the risk of famine fell from 7% in the 1930s to less than 1%.

Data storage

The history of data storage also shows accelerating production.

Ancient civilisations used clay tablets, each holding about 1KB of information. Modern SSDs using NVMe technology allow data to be written at more than 6,000MB per second. That means 1GB, which once took days or years to store, can now be saved in the blink of an eye.

Oil, gas and forestry

Productivity in America’s oil and forestry sectors showcases striking technological progress. In 1860 it took roughly 3,000 workers to produce a thousand barrels of oil; by 2022, one person could manage 100 barrels a day.

Wood processing tells a similar story: since 1900 the number of workers needed to produce 1m cubic feet of output has fallen by more than threefold thanks to automation and modern management. The data attest to a significant lift in labour productivity and better use of materials.

Bitcoin: rethinking saving for the digital economy

As humanity excels at producing goods, services, knowledge and financial assets, an uncomfortable truth emerges: our savings are inefficient — almost everything we save in can be produced in greater quantities and/or cheapened by competition.

Bitcoin is a novel tool for storing value. Unlike traditional assets, the first cryptocurrency has an unchangeable, fixed supply of just 21m coins. That makes it resistant to the inflation that afflicts fiat currencies and other asset classes.

Bitcoin operates on a programmatically declining issuance schedule. This both bootstraps initial distribution and entrenches long-term scarcity. It also ensures that as more miners try to produce more coins, mining difficulty rises to keep issuance on its preset track.

Immutable scarcity underpins bitcoin’s value proposition as a savings instrument. In contrast to the “melting” assets people use to store value, the first cryptocurrency is akin to a “deep freeze at absolute zero.”

The value of digital gold lies not only in its limitation but also in its superior monetary traits: it is fungible, portable, durable and divisible. These characteristics make it a stronger savings tool, reframing traditional approaches to wealth accumulation.

Your wealth is melting

“There has always been a fundamental difference between saving and investing; savings are held in the form of money, and investments are savings put at risk. The lines may have blurred with the financialization of the economic system, but bitcoin makes the difference obvious again. Money with the right incentive structure will crowd out demand for complex financial assets and debt instruments.”

Parker Lewis. Gradually, then suddenly

Human ingenuity and technological innovation increase the efficiency of producing goods and services. Yet we keep storing value in assets whose quantities can be increased.

Traditional savings vehicles — fiat currencies, bonds, equities, gold and property — are exposed to inflation or are tied to financial instruments that can be impaired:

- Is it sensible to hold the US dollar when, as production of consumer goods increases, the Federal Reserve must respond to maintain its 2% inflation target?

- Bonds are merely contracts for future dollar sums. Is it prudent to hold them given fiat inflation and the potential risk of default?

- Is Apple a reliable long-term vehicle with a P/E of 30 when many consumer-electronics firms can produce similar devices and chip away at its walled ecosystem, diminishing uniqueness and income?

- Despite physical scarcity, gold is a commodity that can be mined endlessly with sufficient technology. Is it wise to hold what can be produced without limit?

- Should one plough capital into multifamily housing as a long-term asset given the risk of oversupply, where new projects intensify competition and compress rental yields?

All of these investments may make sense for a time. Over the long haul, however, they face the “innovation trap” — future cash flows or income are competed away or diluted by added supply in free markets.

None of the above instruments guarantees capital preservation over long periods. You will therefore have to hire — or become — an asset manager.

Bitcoin, with its limited quantity, shows how traditional assets can lose value over time — especially in a world where productive capacity is expanding rapidly and markets are ever more global, interconnected and competitive.

The dollar and other fiat currencies

Dollars and other fiat currencies are a common store of value. They may be stable in the short run but lose purchasing power over time relative to basic consumer goods.

The Fed, for instance, targets about 2% inflation a year. That figure does not reflect the direct growth of the money supply. In the United States, the long-run growth of money on current and savings accounts is around 7%, while 2% is merely the rate of consumer-price inflation.

The dollar is designed to depreciate over time against goods whose production we can ramp up ever faster. These include housing, food and energy — three of the four biggest categories in the consumer-price index.

Most people recognise that a currency that weakens against essentials is a poor savings vehicle. They therefore try to preserve purchasing power through other assets.

Debt instruments

The story is similar for bonds and other IOUs.

Such instruments are a promise to pay a fixed dollar sum in future. But fiat money, as we know, weakens over time relative to consumer goods.

Bonds typically offer a positive nominal return — with the risk of default. Will the borrower’s business prosper? Will there be a default? Will repayment be made with newly printed money? Will inflation outrun expectations?

Thus, even with positive nominal returns in a currency that is losing purchasing power, there is a risk of loss from a borrower’s potential insolvency.

Moreover, in global free markets bent on efficiency, the long-run potential for alpha from bonds tends towards zero. As investors seek safe bonds with high yields, demand rises and prices go up.

That, in turn, makes these instruments less attractive for new buyers, reducing the scope for outsized gains. Over time, as more investors enter and information becomes more available and accurately reflected in bond prices, the opportunity for excess return shrinks.

There is no free lunch in competitive markets. If one appears, it does not last — the market quickly eats it.

Equities

Adam Smith’s “invisible hand” describes how the pursuit of self-interest can yield positive outcomes for society as a whole. In free markets, competition pushes businesses to innovate and cut prices, ultimately benefiting everyone.

Investing in equities is a bet on companies’ future cash flows, but the hard-edged competition of capitalism can compress those flows. As markets become more efficient, excess returns are driven towards a minimum.

This is borne out by research by McKinsey showing that the average lifespan of S&P 500 companies has fallen from 61 years in 1958 to less than 18 today. That underlines the hazards of very long-term stock-picking: even successful firms can quickly lose their edge.

By investing in Apple and Nvidia, society encourages the creation of better, cheaper electronics and GPUs. Over time, competition will compress these firms’ cash flows, while consumers gain from innovation and falling prices.

The traditional, or “Buffett-style,” approach to investing may lose viability as creative destruction accelerates. Markets are becoming globally interconnected and more competitive.

That also weighs on passive investing, exposing investors to the risk of holding outdated assets in fast-changing industries and, consequently, to underperformance.

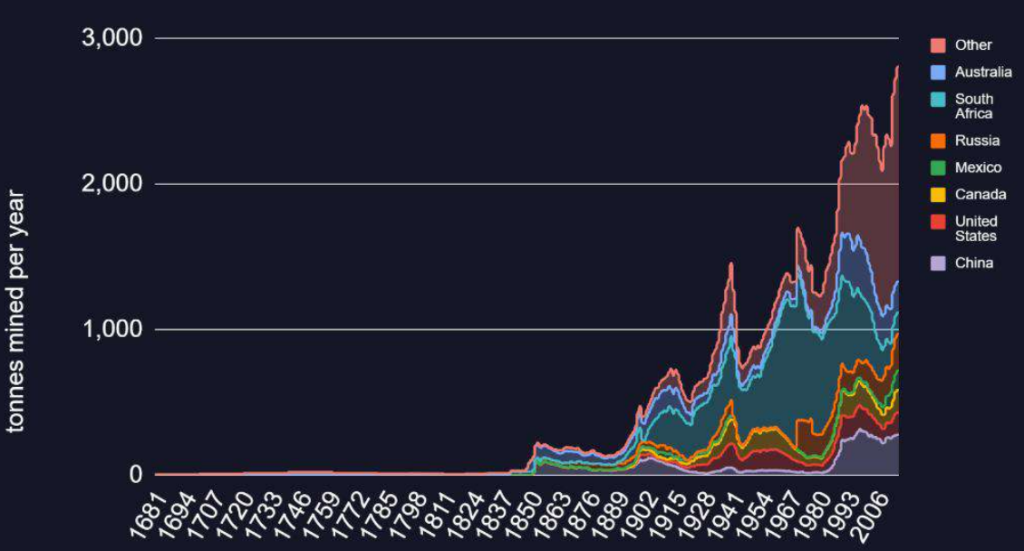

Gold and silver

Even precious elements such as gold and silver are not immune to rising productive capacity. Innovation in extraction and processing makes these resources easier and cheaper to obtain. Their supply grows over time.

While gold and silver output may not immediately respond to price rises — one reason they have traditionally been considered solid stores of value — volumes nonetheless keep creeping up.

As humanity and technology advance, new ways of extracting gold emerge. The universe contains practically limitless reserves of the metal. For example, Earth’s oceans alone hold about $771 trillion worth (roughly 70 times the current above-ground stock).

Gold reserves are virtually inexhaustible. This implies savings will be endlessly diluted as humanity becomes more productive at mining it.

Total worldwide #Gold supply per year.

2009 -> 165,000

2010 -> 168,000

2011 -> 171,000

2012 -> 173,000

2013 -> 176,000

2014 -> 179,000

2015 -> 182,000

2016 -> 185,000

2017 -> 189,000

2018 -> 192,000

2019 -> 195,000

2020 -> 198,000

2021 -> 201,000

2022 -> 204,000

2023 -> 207,000— Willy Woo (@woonomic) April 23, 2024

Real estate

Property is often seen as a worthy investment because everyone needs shelter. People need oxygen even more, yet no one stores wealth in it.

Given advances in construction technology and the availability of untouched land, the supply of real estate can expand, putting pressure on its value. Even relatively scarce land in ideal climates can depreciate, as is already happening with some artificial islands.

If land were to become scarce, humanity has ways to enlarge available space on the planet — or to step up space exploration.

People can also build upward. The Burj Khalifa, for instance — the world’s tallest building at 828 metres — has 164 floors. The ability to construct such skyscrapers owes much to Henry Bessemer, who revolutionised the production of inexpensive, high-quality steel.

Ploughing a large share of society’s wealth into property can run counter to the human drive for innovation and entrepreneurship, which tends to expand markets and lower the cost of physical assets.

Bitcoin and the new economic reality

“We can ignore reality, but we cannot ignore the consequences of ignoring reality.”

Ayn Rand

Bitcoin’s arrival in January 2009 laid the foundations for a new economic reality. It is an innovative tool for saving, trade and economic calculation.

Ignoring digital gold and continuing to allocate to less efficient, overvalued assets risks letting competitors switch to cryptocurrency and outpace you.

Consider MicroStrategy, founded by Michael Saylor, which outperformed the S&P 500 and big tech after betting on the first cryptocurrency. Or a friend who started saving in bitcoin five years ago, is now debt-free, and can afford to take risks building a business.

If you ignore bitcoin, it can be as dangerous as ignoring gunpowder once was. Those who did not use it lost to those who did.

Bitcoin is as important as gunpowder. Bows and arrows will not protect you. Gunpowder is objectively better than bows and arrows. Bitcoin is objectively better than gold or the US dollar. Failing to recognise this does not make it less effective. It simply means you lose and others win.

We live in an era of hyperbitcoinization, and you can already begin to measure your wealth in the first cryptocurrency — objectively better money.

The point is not merely that we may eventually find more efficient ways to mine gold, build homes, or manufacture and sell GPUs. Unlike bitcoin holders, the owners of those assets must factor in that supply can increase in future — or that creative destruction will impair the present value of their future cash flows.

When investors see bitcoin as a reliable instrument that does not debase and possesses all the traits of good money, they will start moving capital into it. That can drive other assets to fall in value relative to digital gold even before any major market shifts occur.

Bitcoin has had a compound annual growth rate of 234% over the past 14 years. The world is shedding less efficient assets and directing capital into a higher form of property.

Thus, the only way to invest safely in innovation is to adopt bitcoin as a unit of account and evaluate opportunity costs accordingly. Digital gold in cold storage is one of the few truly reliable investments.

Conclusions

An age of blistering technological progress ruthlessly exposes the flaws of traditional saving. Most assets can be reproduced without limit or debased by the natural forces of free markets. All except bitcoin.

Digital gold is becoming not merely an alternative but arguably the best store of value in this new era, embodying ideal money. Its strictly limited issuance, coupled with superior monetary traits, sets it apart as a solution to the “innovation trap” that confronts humanity.

It may be the only asset capable of protecting your wealth from the market’s inexorable “melting.”