Monthly spending via crypto cards rose from $100m in early 2023 to $1.5bn by late 2025, according to Artemis.

BREAKING: We just published the most comprehensive report on crypto cards in the industry.

Not because it’s a niche. But because it quietly became an $18B market.

In early 2023, crypto cards were doing ~$100M per month.

Today, they’re doing >$1.5B.So we spent weeks digging… pic.twitter.com/gEsYU3jTlc

— Artemis (@artemis) January 15, 2026

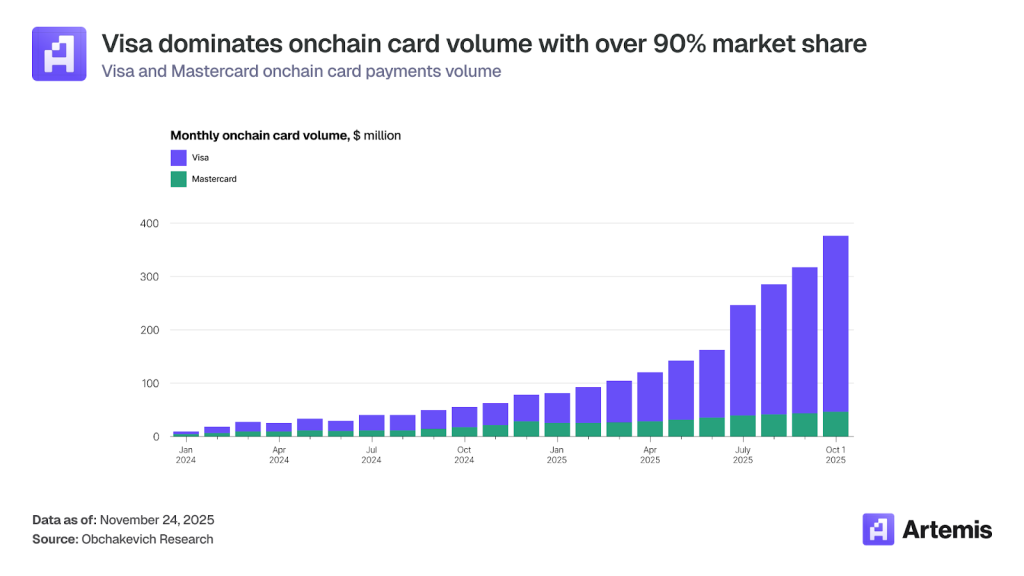

On an annualised basis the market reached $18bn, nearly matching direct P2P transfers in stablecoins ($19bn).

Analysts call cards a key driver of bringing digital assets into the real economy. They have pushed stablecoins beyond exchanges and turned them into a convenient means of payment.

The main reason for the segment’s sudden growth is that most businesses still do not accept crypto. Cards ride existing Visa and Mastercard rails, automatically converting stablecoins to fiat at the point of payment.

Strategic role

For centralised exchanges and DeFi protocols, issuing crypto cards has become a way to compete for users, though their economics differ.

- CEX (for example, Gemini, Coinbase) pay cashback in fiat or liquid crypto, incurring real costs that they cover with trading fees and interest income. A card can be loss-making yet effective for retention;

- decentralised projects such as Ether.fi reward users with native tokens, driving marginal costs towards zero. That allows higher cashback (on average ~4.08% at Ether.fi versus “up to 4%” at many CEX).

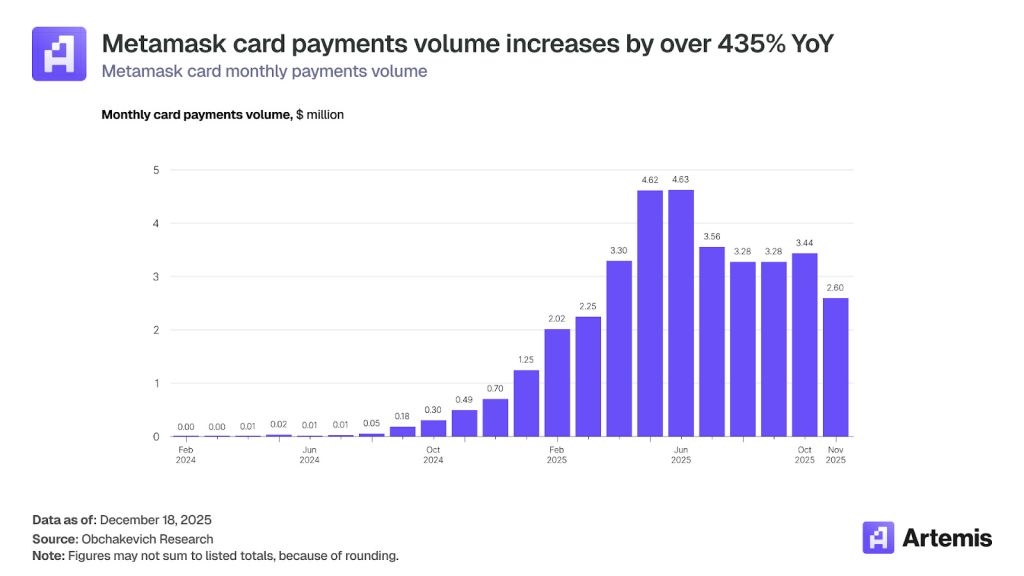

For non-custodial services such as MetaMask and Phantom, cards diversify revenue. Their core swap-fee model is cyclical, whereas cards provide steadier income via interchange and subscription fees.

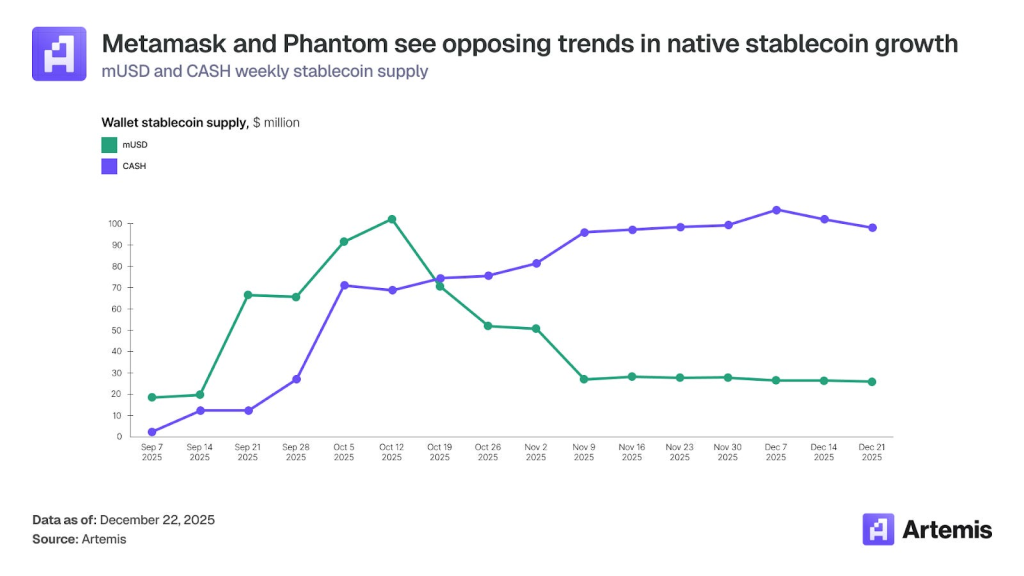

MetaMask and Phantom have issued their own stablecoins (mUSD and CASH) as the basis for their cards, creating closed ecosystems. That yields two advantages:

- extra margin (rather than Circle/Tether);

- user lock-in (the stablecoin becomes a retention tool).

Results vary. Issuance of Phantom’s CASH grew steadily through the quarter, reaching $100m by year-end. MetaMask’s mUSD moved the other way: after an October peak of $100m, supply fell fourfold to $25m.

Geography of use

Crypto cards are most popular in emerging economies. Their appeal is driven by unstable local currencies, inflation and limited access to banking. In such conditions, stablecoins act as a store of value.

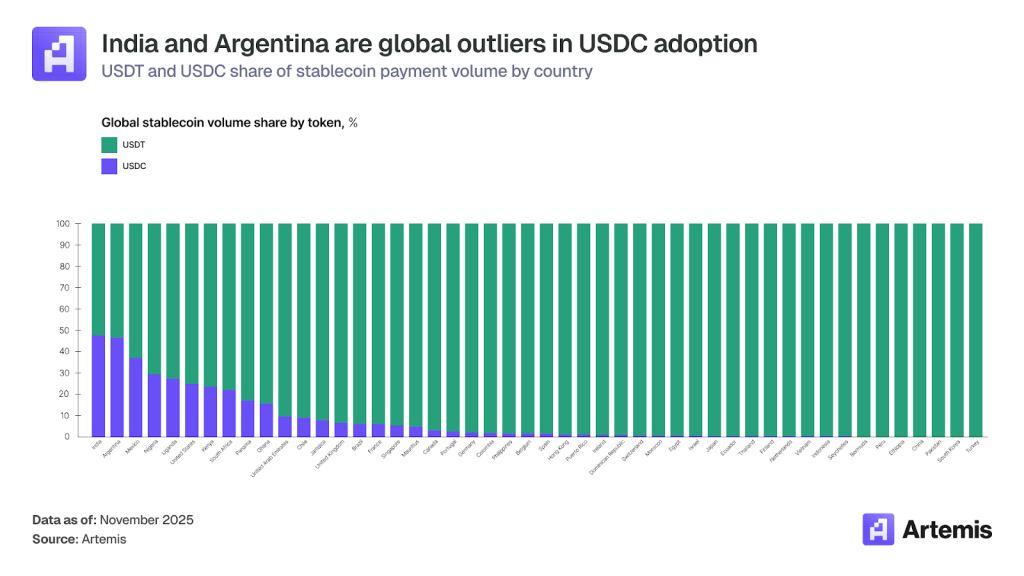

Analysts highlight the leaders in adoption of USDT and USDC:

- India, the largest crypto market in Asia-Pacific by inflows at $338bn. High taxes (30%) have pushed much of the industry offshore and into the shadows. Crypto cards have become a legal bridge between shadow liquidity and the real economy, integrating with the local popular payment system UPI.

- Argentina, where “stable coins” serve as a digital analogue of the dollar, protecting savings from devaluation. Locals use them actively for everyday spending. Notably, Argentines prefer USDC, considering it a more reliable and transparent asset than USDT.

In developed economies such as the United States and the EU, traditional payment systems work well. Stablecoins therefore do not solve fundamental problems and are used mainly by:

- tech‑savvy users;

- crypto investors;

- freelancers and businesses;

- companies working with digital assets.

Outlook

Despite growing options for paying directly in stablecoins, crypto debit and credit cards will remain pivotal for years and continue to outpace the broader industry, Artemis argues.

Analysts point to three structural factors:

- Ready infrastructure. Card networks reach more than 150m merchant locations. Building a comparable system for stablecoin acceptance would take years and heavy investment in POS integration, merchant training and legal frameworks. Crypto cards grant instant access to that network.

- Service and protection. Card networks offer consumers services that “stable coins” by design do not: fraud protection and chargebacks, unsecured consumer credit, loyalty programmes, additional insurance.

- Ease for merchants. Especially for small and medium-sized firms, it is simpler to use familiar acquiring than to rework accounting and implement new payment gateways.

Experts foresee a split in use cases. Crypto cards will remain the dominant tool for everyday spending (retail, restaurants, travel, subscriptions), where convenience, credit, protection and rewards matter. Direct stablecoin payments will find mass adoption in B2B and cross-border business payments.

In October, fintech service Square, part of Block, launched an integrated solution for payments in the first cryptocurrency.