Crypto treasuries lose steam as blockchains hit a technical ceiling

Some lack capital; others lack speed

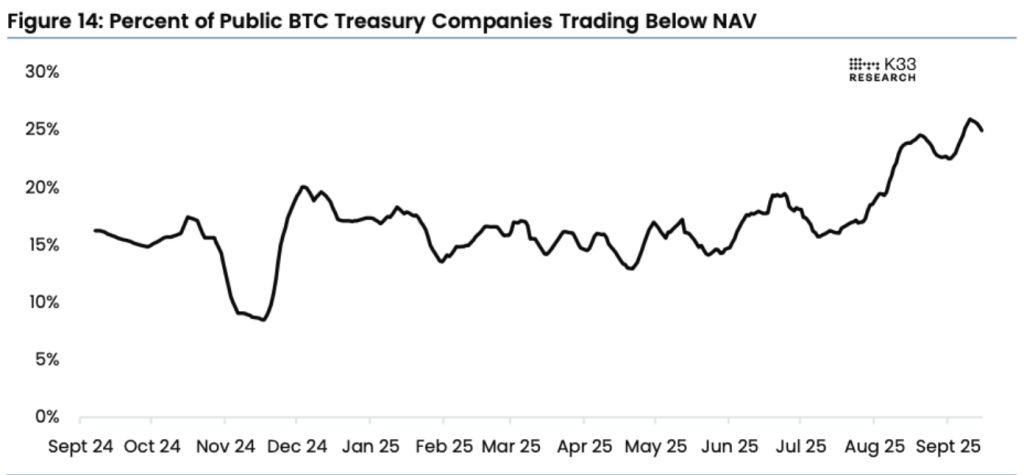

According to the September report from K33, the value of public companies with bitcoin on their balance sheets has fallen markedly. About one in four trades at a market capitalisation below the value of the digital assets they hold.

According to K33’s head of research, Vetle Lunde, the gap between mNAV and the price of BTC means companies are effectively giving away more ownership than they receive in return.

Issuing new shares at a discount dilutes equity, limiting some corporate buyers’ ability to raise fresh treasury funds.

The crypto firm Nakamoto, created by merging KindlyMD and Nakamoto Holdings, has suffered a sharp share-price collapse. NAKA lost more than 95% of its market value from the peak; its mNAV plunged from 75 to 0.7.

According to Bitcoin Treasuries, discounted-stock holders also include Twenty One, Semler Scientific and The Smarter Web Company.

On 16 September, GD Culture Group, a streaming and e-commerce firm, saw its share price fall. After announcing the purchase of 7,500 bitcoin from Pallas Capital Holding for $875 million, it dropped 28%. At the time of writing, GDC is recovering.

The firm has refocused on building a diversified reserve of cryptoassets, but investors reacted cautiously. The sell-off underscored fears about significant equity dilution and the risks of a speculative crypto portfolio.

In September, the average mNAV among public treasury firms was 2.8, down from 3.76 in April, K33 said.

Lunde noted that the distribution is skewed: smaller firms increasingly sit in discount territory, while capital leaders still trade at hefty premia.

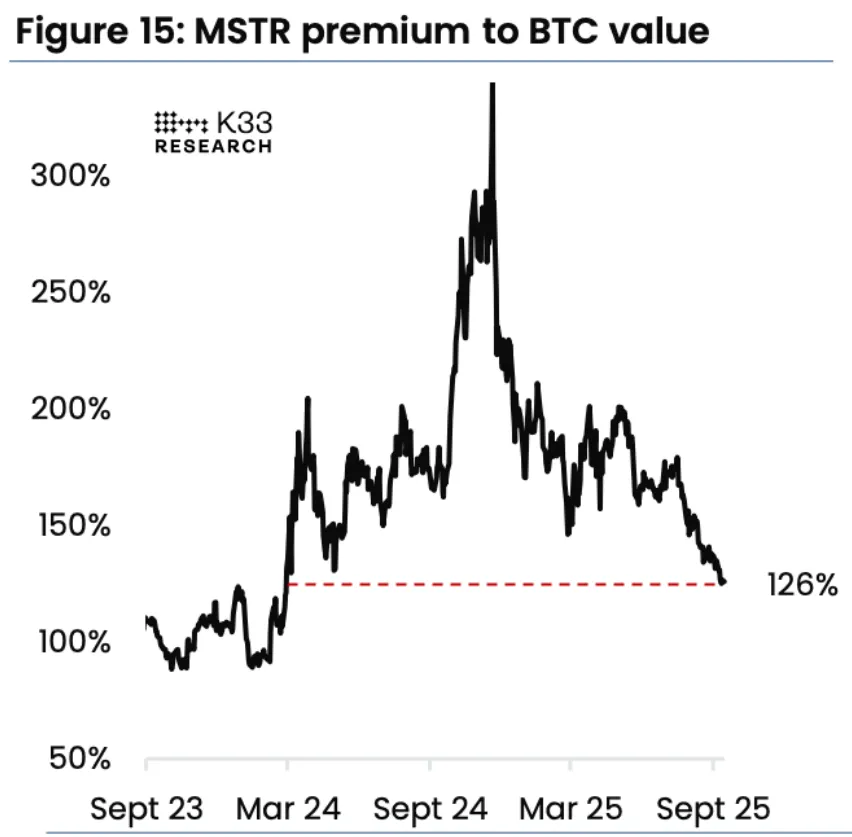

Strategy makes up roughly 64% of the bitcoin-treasury cohort, with a balance of 638,985 BTC at the time of writing. But the “number one” also shows discouraging trends.

According to K33, the premium on Michael Saylor’s company’s shares hit its lowest since March 2024, at 1.26.

“This significantly reduces Strategy’s ability to buy bitcoin and points to a notable decline in buy-side demand from one of the most important absorbers of supply over the past year”, the expert explained.

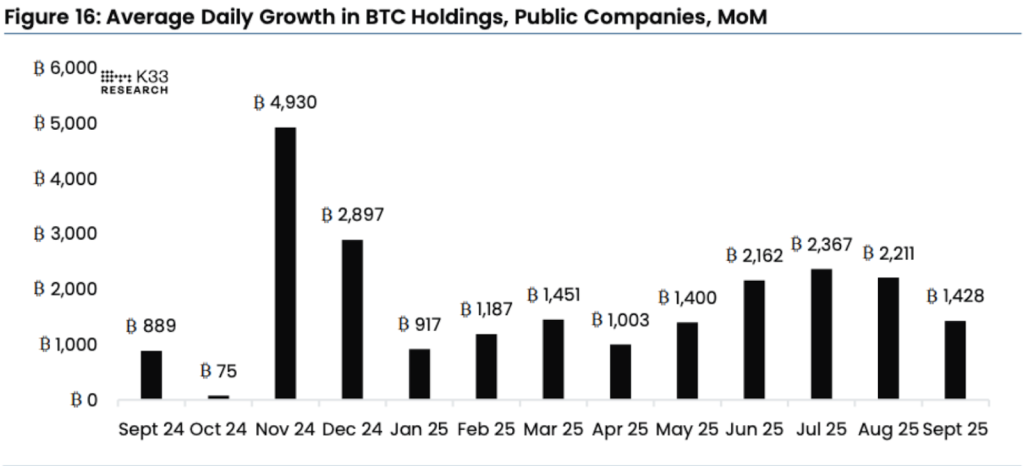

The pace of accumulation of the first cryptocurrency has also slowed, the report said. In September, crypto-treasury firms added just 1,428 BTC per day, the weakest since May.

Lunde called the compression of premia “rational”. He attributed it to high advisory fees, insider incentives and complicated capital structures. He also expressed hope for firms that can deploy their bitcoin holdings in other parts of their business.

Analysts suggest that spot ETFs and retail flows are becoming the main drivers of demand.

A new wave of crypto adoption and a technical ceiling

The next wave of institutional crypto adoption is arriving as well-known fintech firms begin building their own blockchains, co-founder of Altius Labs Annabelle Huang told Cointelegraph.

Huang has seen crypto converge with traditional markets first-hand. She began her career as a trader in New York, then joined Amber Group in Hong Kong as a managing partner. At Altius Labs she has focused on creating a modular execution layer designed to plug directly into existing blockchains, boosting throughput without forcing projects to rebuild their infrastructure.

The Robinhood financial-services app recently announced it is developing its own L2 blockchain to support tokenised stocks and real-world assets, while Stripe followed suit with plans for Tempo — a payments-oriented network built with Paradigm.

“What we are seeing now — and I expect it to continue even more in the future — is a trend of institutional investors adopting stablecoins or even building their own blockchains for specific use cases”, the expert said.

In Huang’s view, such initiatives are the next stage of institutional blockchain adoption. Their weak point, like that of many existing crypto platforms, is low throughput.

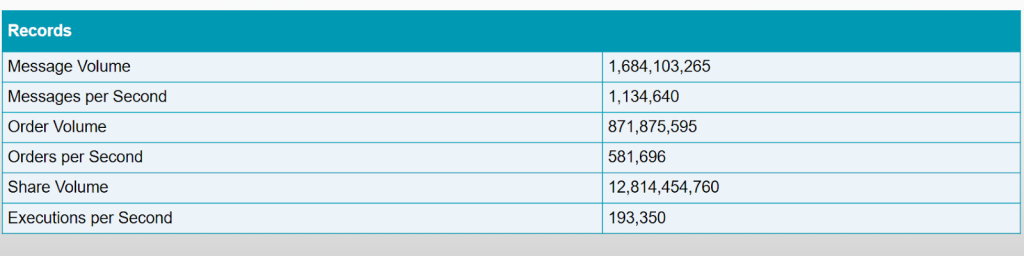

According to Nasdaq, its peak speed is 581,696 orders and 1,134,640 messages per second. Huang considers these figures incomparable with the characteristics of one of the fastest networks — Solana.

She called speed “a bottleneck in execution” and said it must be fixed before fintech-built blockchains can bear the weight of institutional capital.

“The industry should not expect new ‘Ethereum killers’ or general-purpose blockchains. Users prefer to coalesce around a few dominant platforms rather than scatter across dozens of new networks”, Annabelle Huang told Cointelegraph.

The specialist also commented on bitcoin treasuries. She sees shifts to cryptoassets on balance sheets as risky, especially for retail investors, because not all corporate bitcoin strategies are structured the same way. Comparing share-price spikes to token launches, Huang thinks demand for proxy assets such as ETFs and treasury strategies will persist.

She added that although exchange-traded fund options exist for bitcoin and Ethereum, investors who want exposure to altcoins often turn to debt strategies.

Previously, the expert warned that chasing high yields from holding Ethereum carries serious risks for companies.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!