The correlation between bitcoin and S&P 500 futures widens as price swings in the first cryptocurrency intensify. Analysts at DBS, Singapore’s largest bank, пришли to that conclusion.

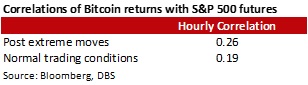

Researchers noted a positive statistical correlation between daily bitcoin price changes and S&P 500 futures dating back to November 2020. While modest, the correlation coefficient stood at 0.2.

According to a more granular analysis, the measure climbs to 0.26 during sharp price swings in the digital gold. The analysts counted +/- 10% moves on an hourly interval, which occurred on December 28, 2020, January 4 and 29, and May 19, 2021.

“This suggests that overall market sentiment may reflect the increasing correlation with Bitcoin dynamics over a limited period (60 hours), leading to unusually large moves.” — the specialists explained.

Other statistical observations confirmed the hypothesis that after substantial Bitcoin price swings, stock market volatility was noticeably higher than usual.

“Bitcoin is no longer a ‘peripheral’ asset as it once was. Given the recent sell-offs, market participants may wish to monitor developments in this space as part of risk and sentiment monitoring.” — the experts concluded.

In January 2021, the chief economist at Bank of Singapore said that digital assets could to secure a safe-haven status and become rivals to gold.

Subscribe to ForkLog news on Telegram: ForkLog Feed — the full feed of news, ForkLog — the most important news, infographics and opinions