In just a few months, during the Winter Games in China, the digital yuan – e-CNY – could be launched. Accordingly, experts and market participants ask a natural question: how will this affect the current leaders in mobile payments in mainland China — Alipay and WeChat? In the People’s Bank of China (PBoC) drive to offer a currency that operates without intermediaries, a direct threat to these firms becomes evident.

Does the digital yuan threaten Alipay and WeChat Pay?

Currently, more than 90% of mobile payments in China are accounted for by two duopolistic systems: Alipay from Alibaba and WeChat Pay from Tencent. According to Fitch Ratings analysts, at present the digital yuan’s impact on these companies’ financial results is minimal. However, in the long run their market positions will depend mainly on the government’s regulatory policy toward non-bank mobile-payment providers.

And here one must consider already existing measures taken to prevent dominance by the two private players. In November last year, the $34.4 billion IPO of Ant Group – the operator of Alipay – was halted. And in spring this year, a antitrust penalty of $2.8 billion was imposed on Jack Ma’s group of companies.

Officials at the People’s Bank of China either decline to comment on the impact of e-CNY on Alipay and WeChat’s positions, or state that there is no competition and that various options will complement and coexist. This was stated, in particular, by Mu Changchun, director of the PBoC Institute of Digital Currency Research, at the BIS Information Security Summit. He noted that in the event of technical or financial problems for Alipay and WeChat, threats could arise to the stability of the entire country’s financial system. That is why authorities must accelerate the adoption of a real alternative to these market players.

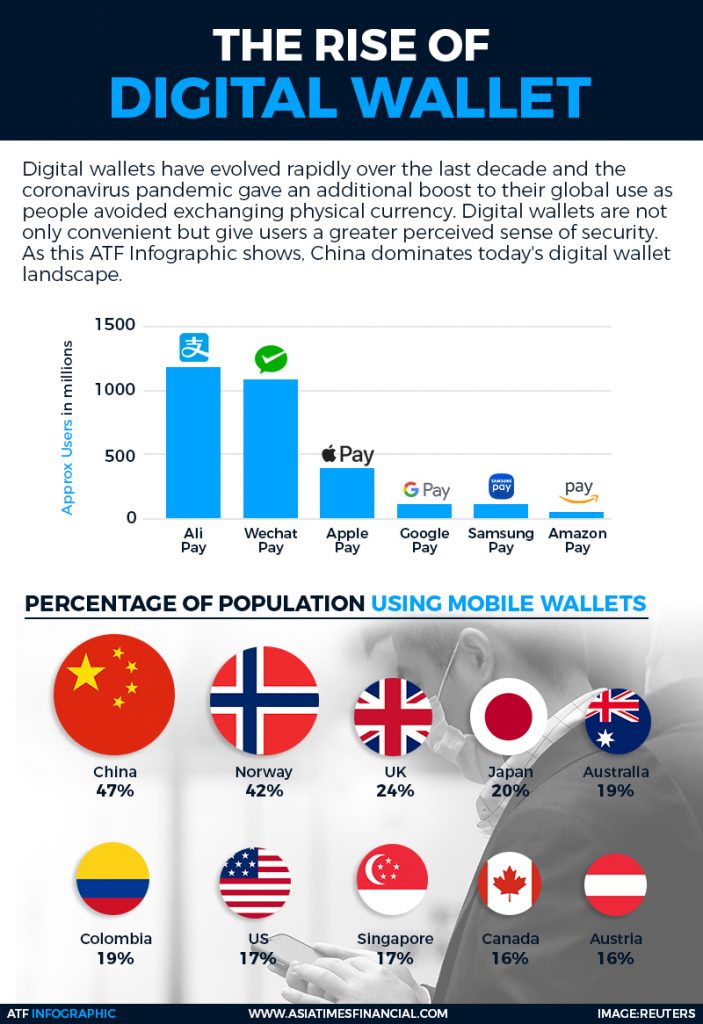

Another goal of the e-CNY rollout is broader population participation in the cashless system. Although China is currently the world leader in mobile-wallet adoption—with 47% of the population using them and handling transactions totaling over 2 trillion yuan annually—225 million people, or 20% of the country’s adult population, do not have a bank account.

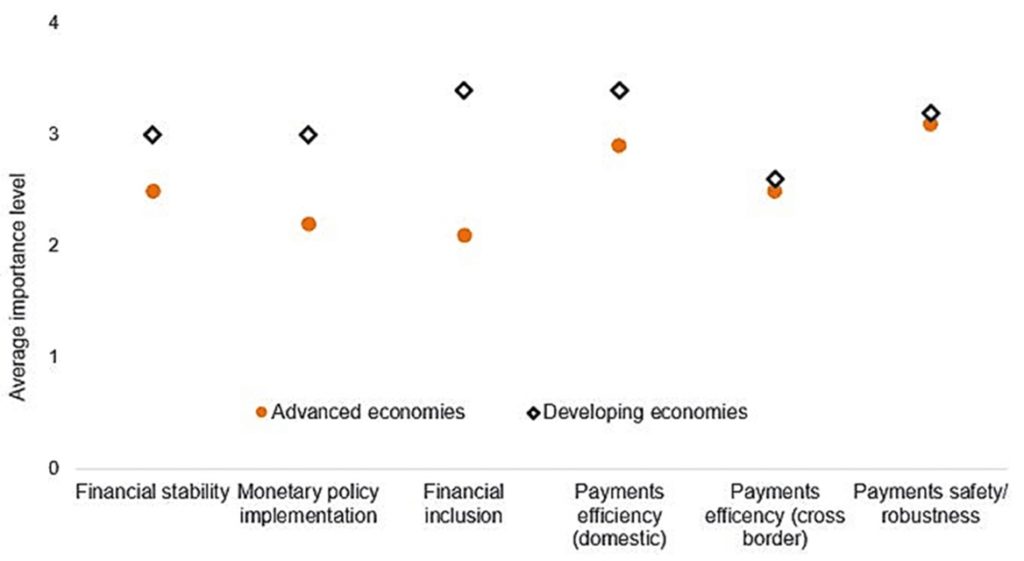

Overall, as the diagram below shows, the relevance of introducing a digital currency as a new, more efficient instrument of monetary policy and a means to bring people into the cashless economy is markedly higher in developing countries. Perhaps that explains why the leading financial markets—the United States, the European Union, and Japan—are willing to concede first place to China to study its experience and avoid mistakes, offering their citizens a more advanced “product”.

How e-CNY payments differ from traditional mobile payments

No intermediaries. The issuance of the digital yuan operates on a two-tier scheme. The PBoC allocates e-CNY under 100% cash yuan backing among participating banks, which then exchange digital currency for cash at 1:1.

Using a dedicated app, users can make payments and transfers directly, without recourse to intermediaries or even a bank account. As a result, no fees are charged.

Offline payments. For accepting and debiting payments, users only need to generate or scan a QR code without an internet connection.

Moreover, besides mobile apps, wallets embedded in gear, for example ski gloves, were tested.

Instant settlement. Funds are credited and debited instantly.

Programmable money. As a digital currency, e-CNY can be ‘programmed’ for targeted use, for example for transportation costs or groceries, which could simplify the delivery of targeted aid to households, businesses and non-profit organisations.

What experts see as challenges for e-CNY adoption

Despite the potential benefits for users of being able to transact in the digital yuan, there are a number of factors that curb the spread of the e-CNY as an alternative to the traditional yuan and even more so to the dollar.

Increased state control. Increased transparency of payments, centralized storage of user data, the ability to block funds, and other restrictions—all of this will allow the authorities to enhance the effectiveness of officially stated measures to prevent terrorist financing, tax evasion, and money-laundering. Yet how transparent, predictable, and justified will the authorities’ actions be? After all, where there are opportunities for abuse, there are those who will seek to exploit them.

‘Controlled anonymity’. This is how the PBoC defines its approach to data disclosure. For small payments, a phone number suffices at registration, and for larger sums, KYC—’Know Your Customer’—rules apply. The more personal data a user provides, the wider the functionality available to them. Yet the question remains whether rules will be changed when the initial period of e-CNY’s popularisation ends, and whether the new currency will weaken the competitors in Alipay and WeChat?

Eclipsing small and private players. Removing intermediaries from the payments system will weaken smaller and especially private companies; if Alipay and WeChat exit the market, this would undermine the competitive environment, reduce private players’ ability to analyse consumer behaviour and offer personalised services.

What’s at stake?

Formally, e-CNY is supposed to supplant cash, including physical banknotes and coins, whose share in the broad money supply is no more than 10%.

However, the main prize to be fought over is user data. Today Alipay and WeChat accumulate massive amounts of information about the behaviour of hundreds of millions of consumers, and such data is of considerable practical interest to the Chinese authorities.

Moreover, the more e-CNY is used domestically, the greater its chances of securing a meaningful place in cross-border settlements.

Strengthening the position of China’s currency as a reserve and reshaping the global financial architecture, long dominated by the dollar, are among Beijing’s strategic policy objectives.

In conclusion

The absolute dominance of Alipay and WeChat in the retail mobile-payments market remains a reliable guarantee that, for now, the PBoC will refrain from imposing restrictive measures against them in the interests of maintaining financial stability.

Nevertheless, it should be noted that Chinese authorities are pursuing a targeted policy of de-monopolisation. According to the five-year plan presented by the CPC Central Committee and the State Council of the PRC to strengthen oversight in national security and technological innovation, by 2025 the authorities will enact regulations governing the tech sector, data governance, antitrust, and other areas. Among the aims are to ensure the rule of law and the healthy development of new forms of business.

Thus, regulatory changes are expected to be directed at supporting e-CNY and progressively reducing Alipay and WeChat’s share in the market. The digital currency’s features, allowing the use of administrative resources, will assist in this. For example, targeted budget payments could be issued in the new currency with spending restrictions. Users may have no choice but to settle subsidies and grants in the digital currency.

For other consumer categories, the main factors in choosing between familiar Alipay with WeChat and the e-CNY will be ease of use, features, and absence of fees (it is not inconceivable that under competitive pressure Alipay and WeChat will also reduce or waive fees).

The issue of centralized government access to personal data and ‘managed anonymity’ is unlikely to be a major deterrent for Chinese citizens adopting the new payment instrument—at least until there are precedents of discriminatory data use in the implementation of state policy.

Subscribe to ForkLog news on Telegram: ForkLog Feed — all the news, ForkLog — the most important news, infographics and opinions.