Key Takeaways

- Outflows of Ethereum from centralized platforms continued amid liquidity inflows into the project’s DeFi ecosystem.

- The number of Bitcoin whale addresses fell to mid-2019 levels.

- On-chain indicators signal improving market sentiment and the potential for further market recovery.

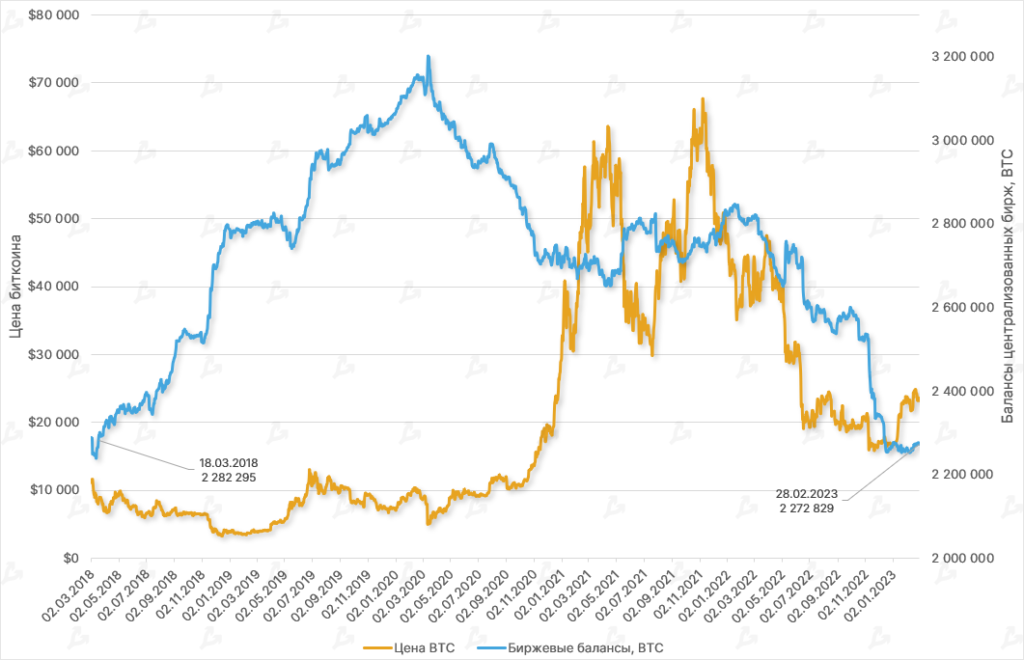

- Bitcoin balances on centralized exchanges declined to March 2018 levels.

- Hash rate and mining difficulty hit new highs.

- Total value locked in DeFi smart contracts rose by 25%.

- The Arbitrum L2 network approached Ethereum in terms of average daily transactions processed.

- Capitalisation of BUSD fell by $5.4 billion, bringing the overall stablecoin market close to $130 billion.

- Amid competition between Blur and OpenSea in the NFT space, user activity picked up again.

Dynamics of leading assets

- In February the leading cryptocurrencies consolidated after a sharp rise earlier in the year.

- For the month, Bitcoin and Ethereum posted modest gains — up 0.03% and 1.26% respectively.

Publicly traded crypto-related stocks

Mining stocks’ performance

Marathon Digital (MARA):

-0.98%

After a strong start to the year, mining- and crypto-related stocks traded in mixed directions, largely moving in step with Bitcoin.

Market mood, correlations and volatility

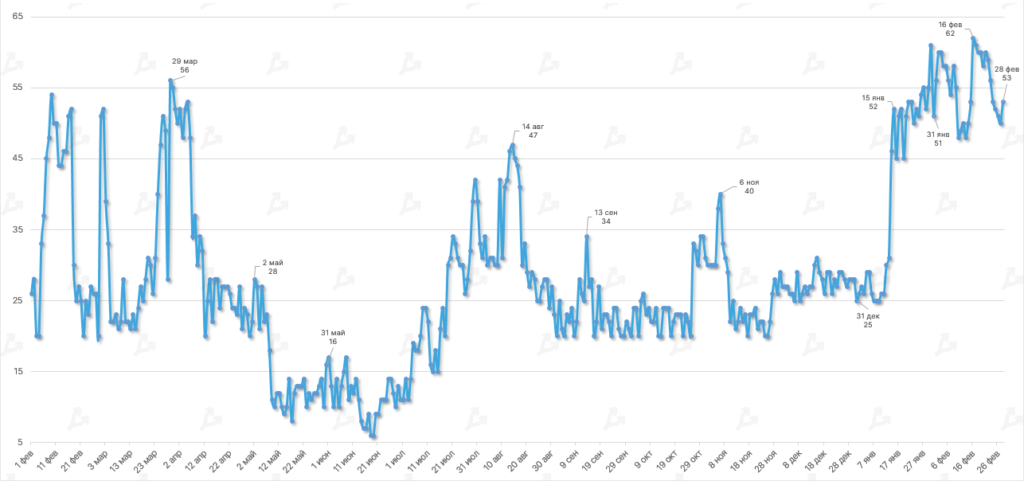

- During February the Fear and Greed Index largely stayed in the Greed zone. In mid-month Bitcoin prices tested the $25,000 level — the index reached a yearly high of 62.

- The indicator’s minimum reading was 48, the average 53.3. This pattern signals investor optimism despite a rise in the Federal Reserve’s rate and an uptick in inflation in the United States.

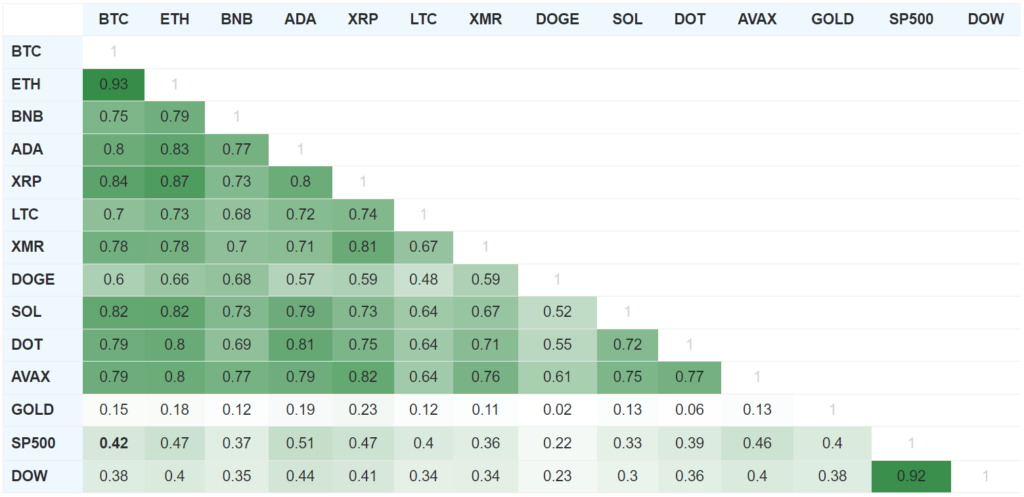

- In February the statistical relationship between Bitcoin and the US stock market rose slightly. Correlation with the S&P 500 reached 0.42, and with the Dow Jones — 0.38.

- The movement of Bitcoin and gold prices trended in the same direction, but their correlation remains relatively low.

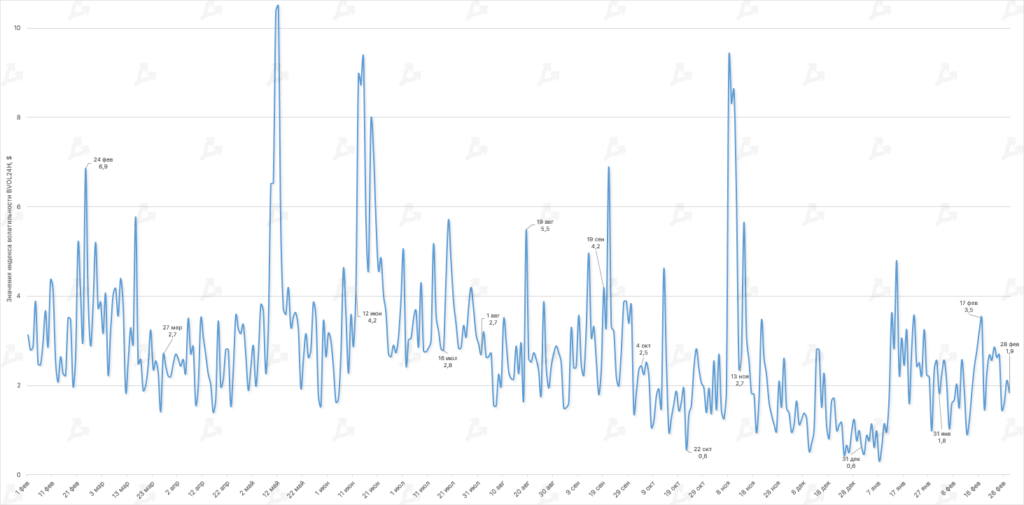

- The average BVOL24H over the last month stood at $2.1, somewhat above January’s figure.

- The index peaked at $3.5 on 17 February when prices touched $25,000.

Macro backdrop

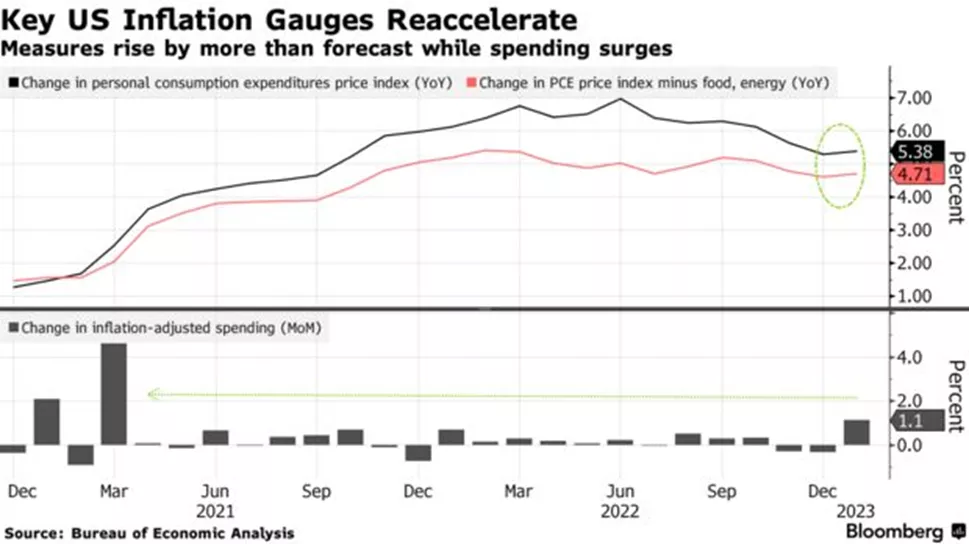

- US consumer expenditure inflation in January rose from 5.3% year-on-year to 5.4%, versus a 4.9% forecast; core inflation rose from 4.6% to 4.7% (4.6%). CPI rose by 6.4% with expectations for a slower 6.5% to 6.2%, core — up 5.6% (from 5.7% to 5.5%). The slower inflation backdrop is also visible in fresh PPI data.

- In January, US nonfarm payrolls rose by 517,000 versus a forecast of 188,000. Over the prior two months, the gain was 71,000 higher. Unemployment, contrary to expectations, fell to the lowest since 1969 — 3.4%. Yearly wage growth slowed to 4.4% vs 4.3% expected. Retail sales jumped by 3% against a 2% forecast.

- Fed officials, including the chair, signalled the need “for further work” — elevating the policy rate and keeping it high for an extended period. This prompted a revision of expectations about its ceiling and timing for a shift to easing policy.

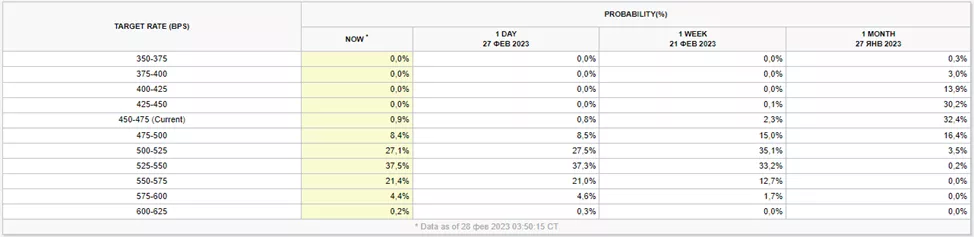

- Options traders now price in a 50 bps hike in March with a 23.3% probability. A month ago odds were 1 in 5 that rates would stay at 4.5-4.75%.

- Investors also revised expectations for the Fed’s next steps. If a month ago the market doubted whether rates would exceed 5.25% and saw a 76.5% chance of returning to the current level by year-end, now a peak of 5.75% is priced in with 42.8% probability and a 5.25-5.5% range by year-end (73.7%).

On-chain data

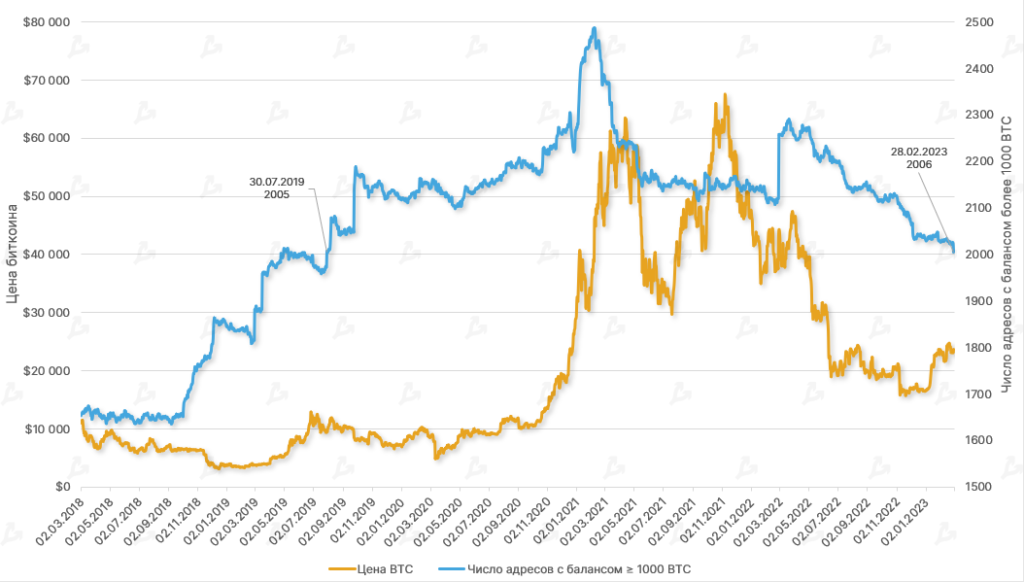

- The number of addresses with 1,000 BTC or more fell to mid-2019 levels. As of 28.02.2023, such whale addresses stood at 2,006; the similar peak of 2,005 was recorded on 30.07.2019.

- The count in this category peaked near 2,500 in February 2021. Since then, despite Bitcoin’s rally to a new high around $69,000, the metric declined.

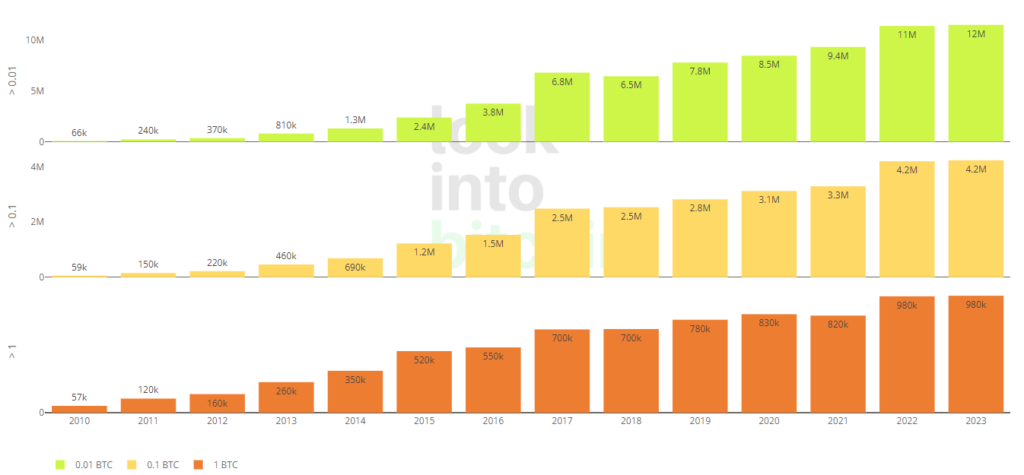

- Smaller-address categories (>0.01, >0.1 and >1 BTC) show a more optimistic picture — these groups have rarely seen declines, signalling gradual growth in the number of crypto investors and their drive to accumulate more digital gold, regardless of volatility and cycles.

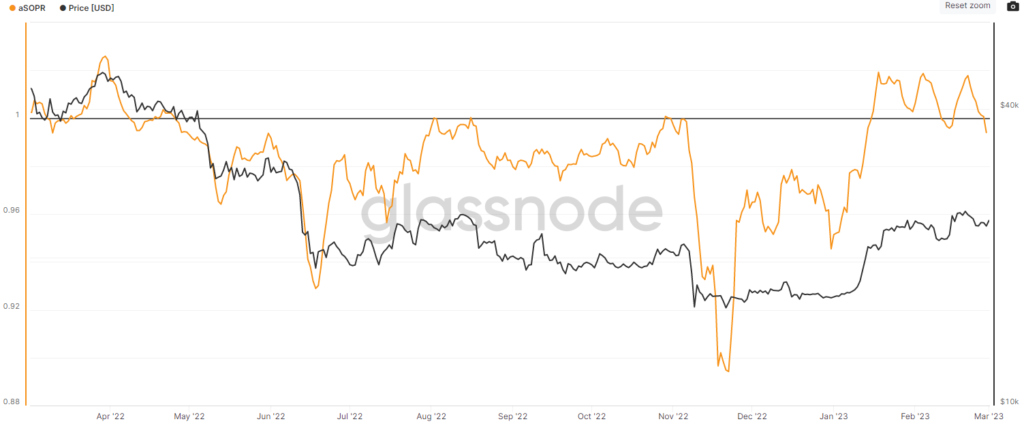

- The aSOPR indicator spent most of February above 1, signaling improved sentiment and profit-taking by many investors.

- Decentrader analysts believe that short-lived dips below key levels present a good “buy the dip” opportunity.

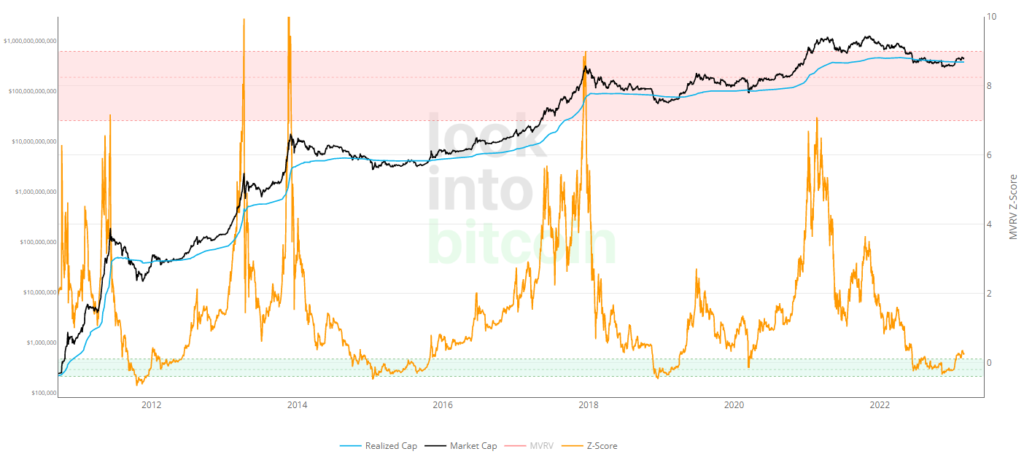

- The recently released MVRV Z-Score that re-entered territory below zero indicates potential for further price gains and overall market recovery.

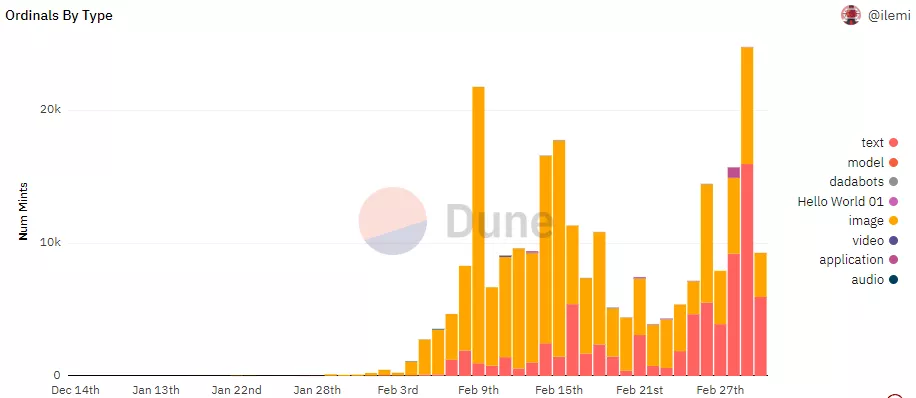

- In February there was a notable uptick in Taproot‑sig shares in Bitcoin’s blockchain — on 15 February the share rose above 12%, before retreating.

- The trend is tied largely to the Ordinals project, which enables digital artifacts on Bitcoin. The number of Bitcoin NFTs surpassed 228,000, according to a Dune dashboard by @dataalways.

- Total digital gold on centralized exchanges fell to March 2018 levels. The pullback from exchanges intensified in 2022 amid Terra’s collapse, FTX’s demise and broad market contagion. The persistent decline in this metric suggests many investors are moving to non-custodial wallets for safety.

Ethereum

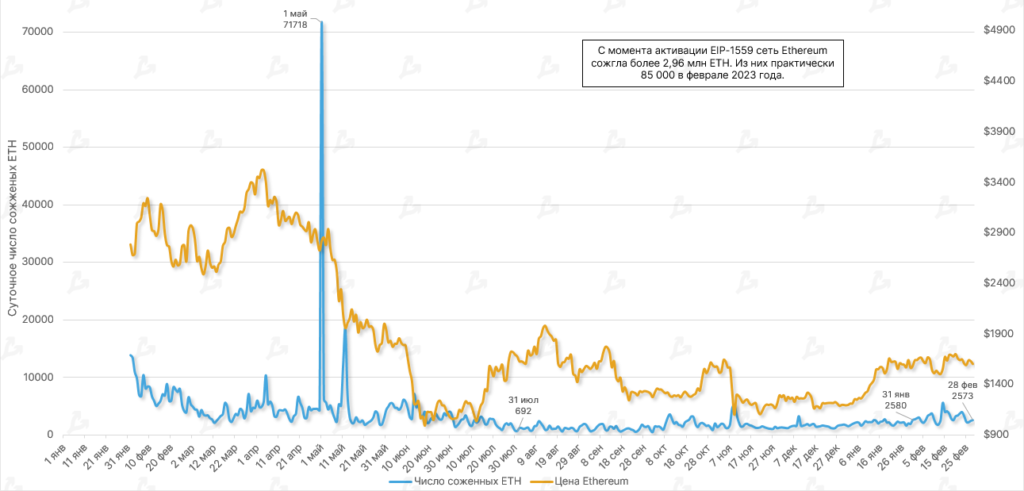

- Since activation of EIP-1559, Ethereum has burned more than 2.96 million coins. Around 85,000 ETH burned in February, up 30% from January. The rate of coins leaving circulation accelerated for a second month, driven in part by DeFi activity and the tit-for-tat between two NFT marketplaces — OpenSea and Blur.

- According to Ultrasound Money, over the last 30 days the Ethereum supply contracted by 35,400 ETH. The largest single‑holder outflow was ~9,100 ETH linked to Uniswap, with OpenSea ~6,100 ETH close behind.

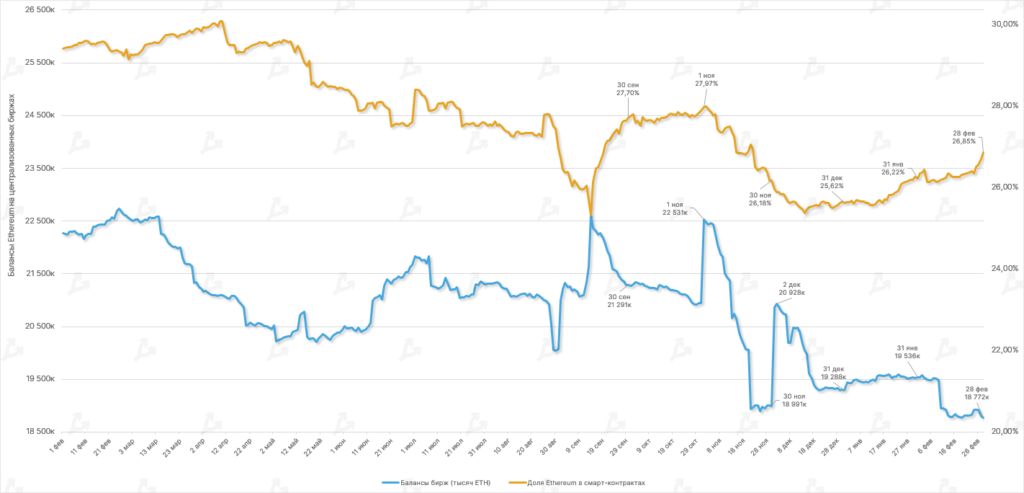

- By February end, the share of ETH locked in smart contracts across DeFi apps rose to 26.85%.

- In the period under review the total Ethereum on centralized platforms fell by 4%. The two latest metrics point to rising DeFi interest. The likely catalyst is the Shanghai upgrade slated for March 2023, enabling withdrawals of staked assets.

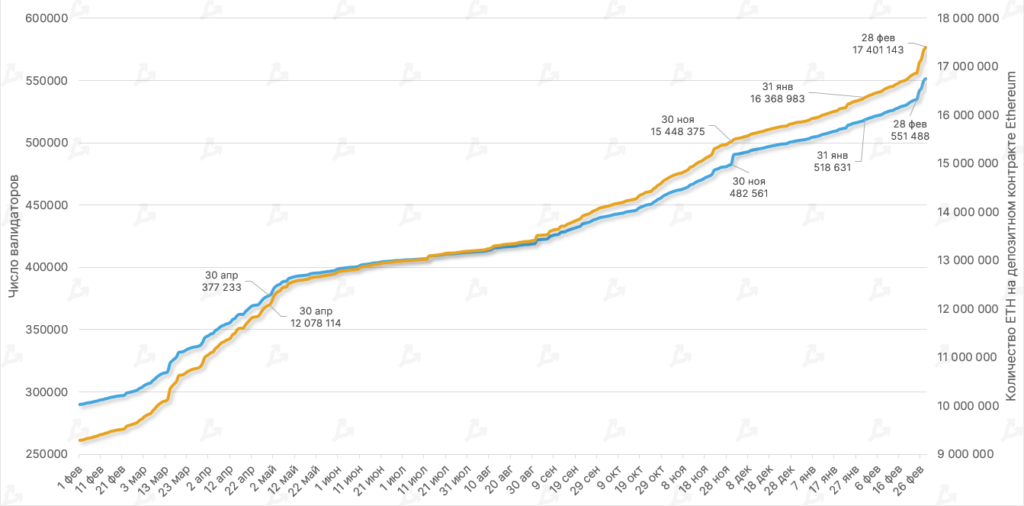

- In February the number of Ethereum validators rose 6%, to 551,488. The amount staked rose to 17.40 million ETH — up more than 6% over the period.

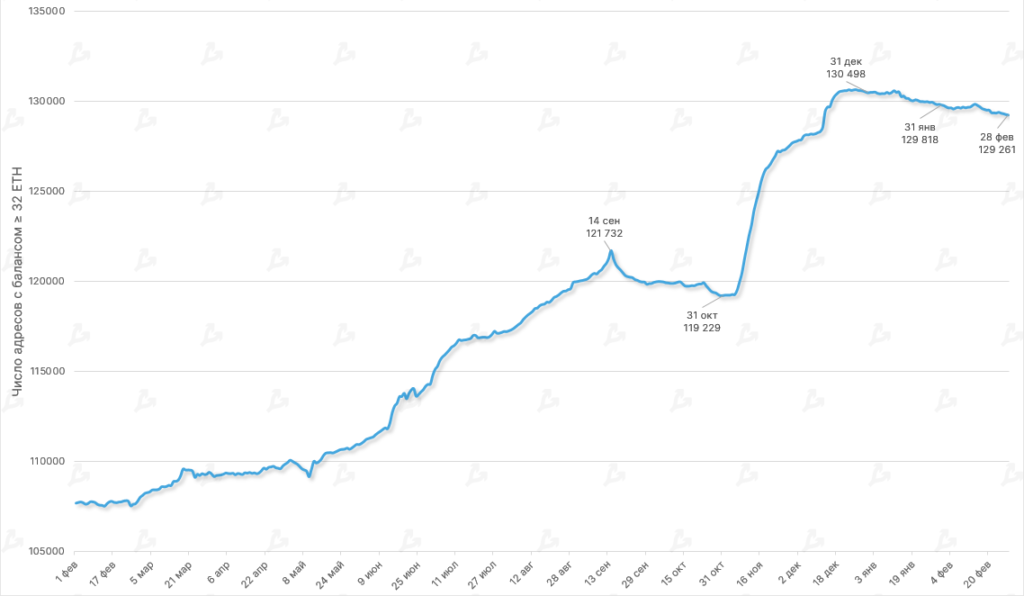

- The number of unique addresses depositing 32 ETH or more into the staking deposit contract declined slightly, to 129,261. The trend reflects growing popularity of liquid staking services such as Lido, which enable users without enough funds to operate as validators to participate.

Lightning Network

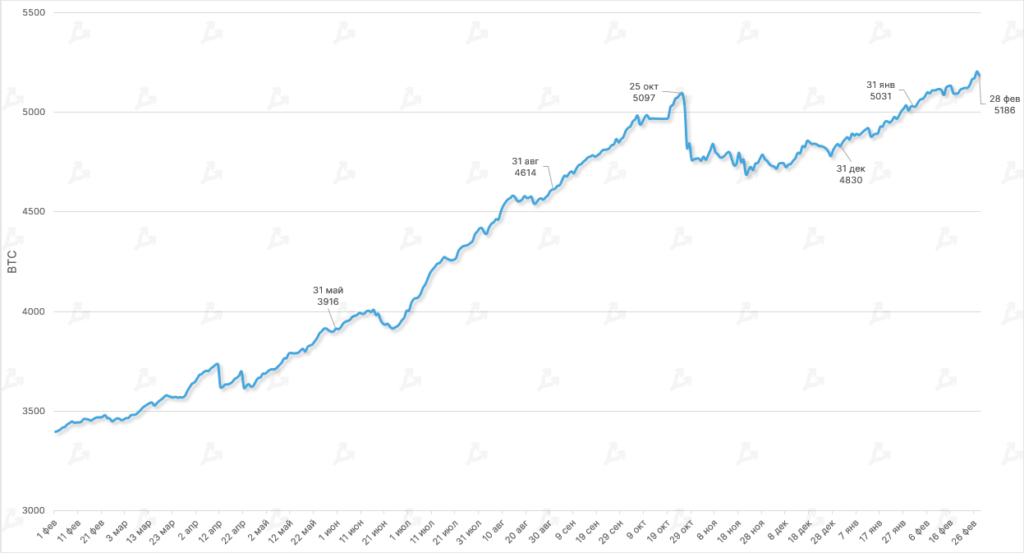

- In February Lightning Network capacity grew by 3% and reached a new peak of 5,206 BTC (5,186 BTC as of 28 February).

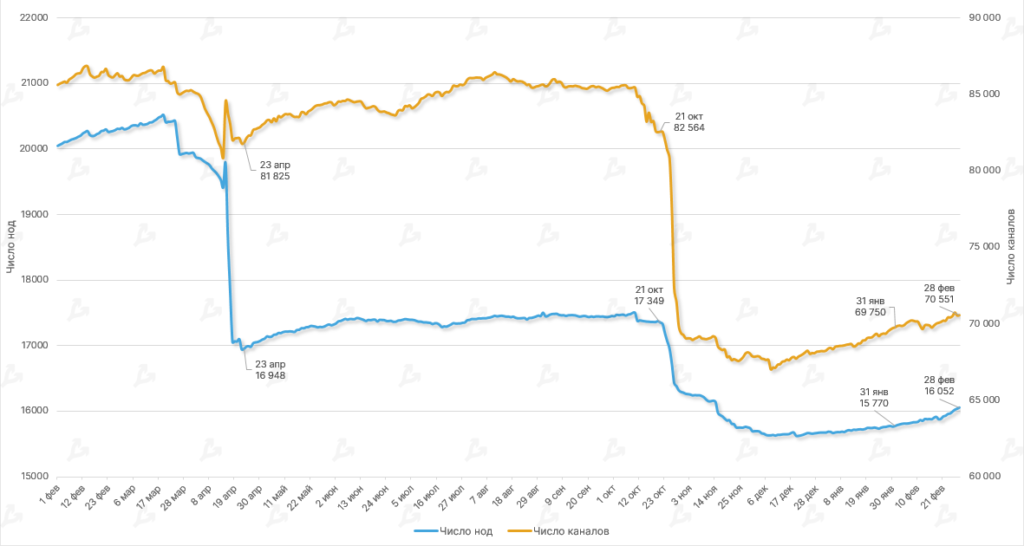

- The number of nodes and channels rose slightly, standing at 16,052 and 70,551 respectively (15,770 and 69,750 in January).

Mining, hash rate, fees

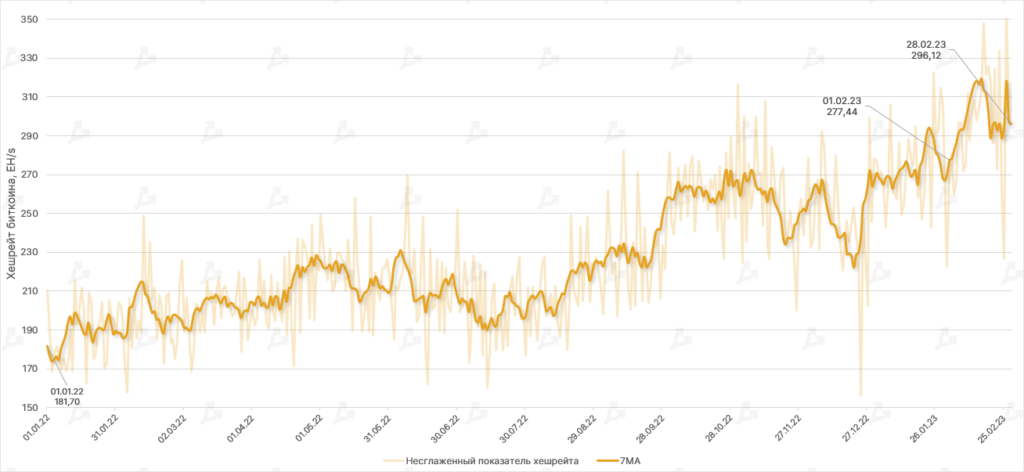

- Against a backdrop of gradual market recovery, Bitcoin’s hash rate (7‑day MA) rose 6.73%, reaching a new high of 319.4 EH/s. The consistently upward trend signals industry participants’ confidence in Bitcoin’s long-term prospects and mining generally.

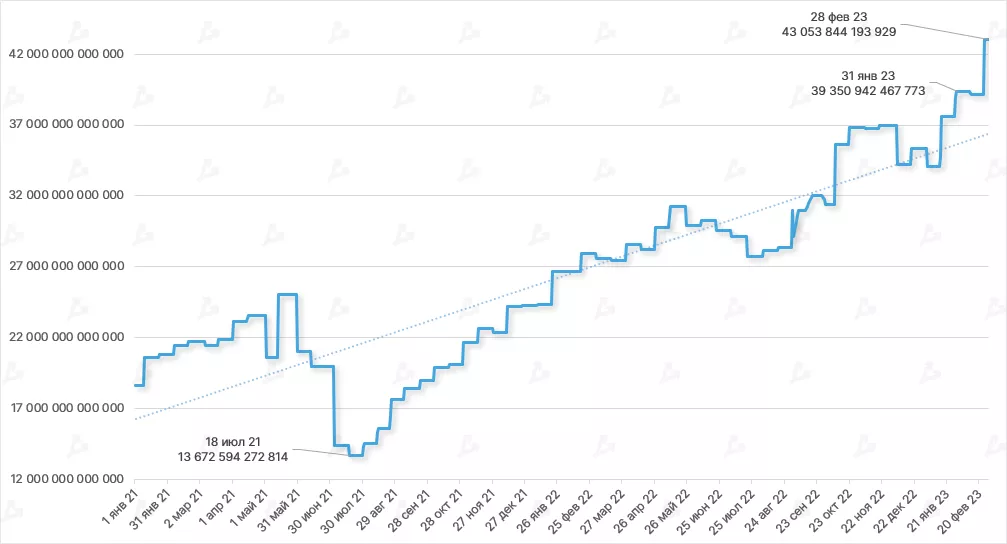

- The hash-rate-related difficulty climbed to a new record — 43.05 T. After the latest retarget, the metric rose by 9.95%.

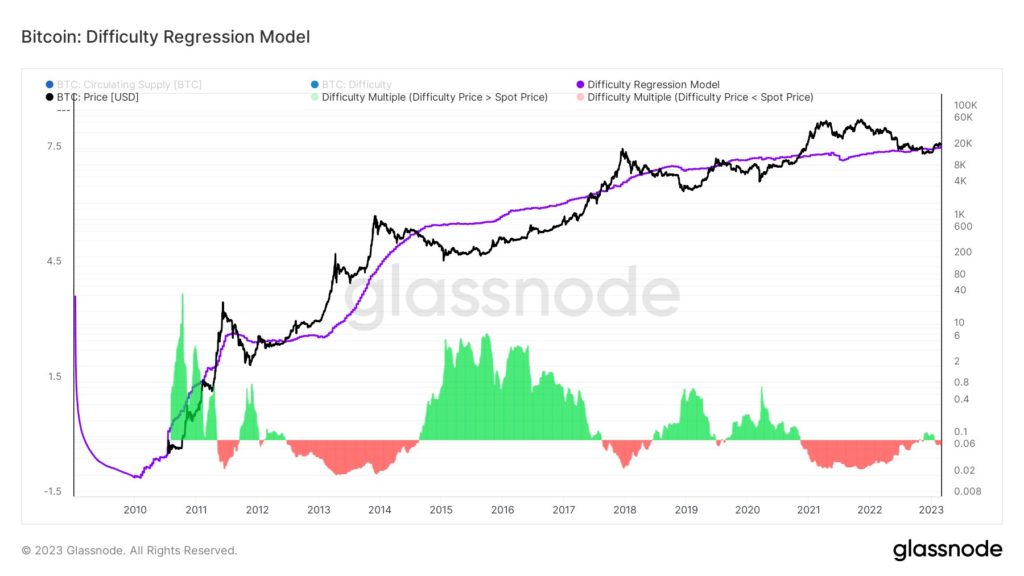

- Despite rising difficulty, hashprice of Bitcoin recovered — mid-February hashprice reached $0.079 per TH/s-day, roughly the same as early October last year before the market downturn caused by FTX.

- Using a regression model, CryptoSlate researcher James Van Straten estimated a rough cost of production for Bitcoin at about $21,100. With market price above this level, miners are returning to the game and increasing hash rate, he said.

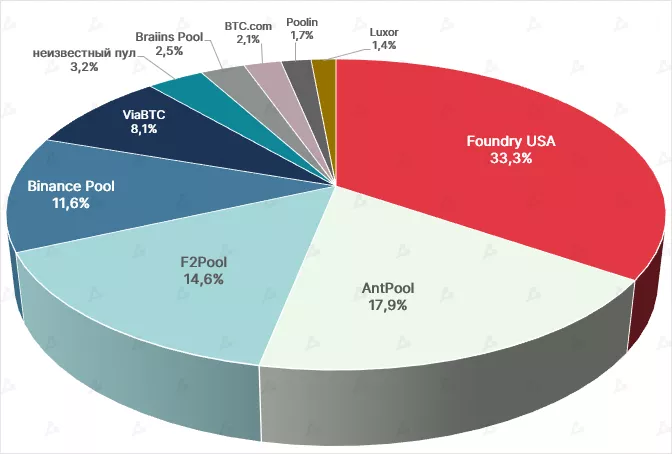

- The share of the largest pool — Foundry USA — reached one third of total Bitcoin hash rate (33.3%). AntPool’s share fell from 19.7% to 17.9%, and Poolin from 2.3% to 1.7%.

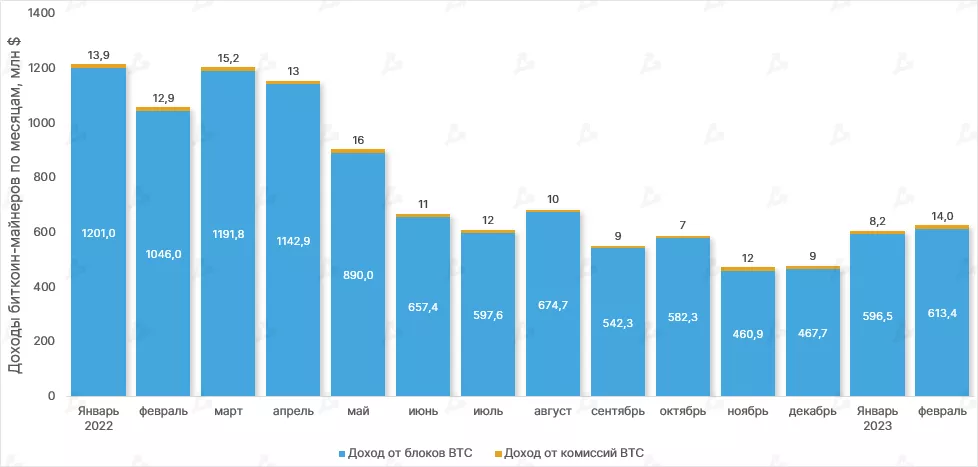

- Total miner revenue rose by just 4% year-on-year, reflecting slower Bitcoin price growth and the shorter February month.

- Conversely, the share of fees in miner revenue rose to 2.28% (January was 1.38%). This is largely linked to higher on-chain activity driven by Ordinals transactions. As a result, Bitcoin blocks have been busier, fees have risen and blocks often fill to capacity.

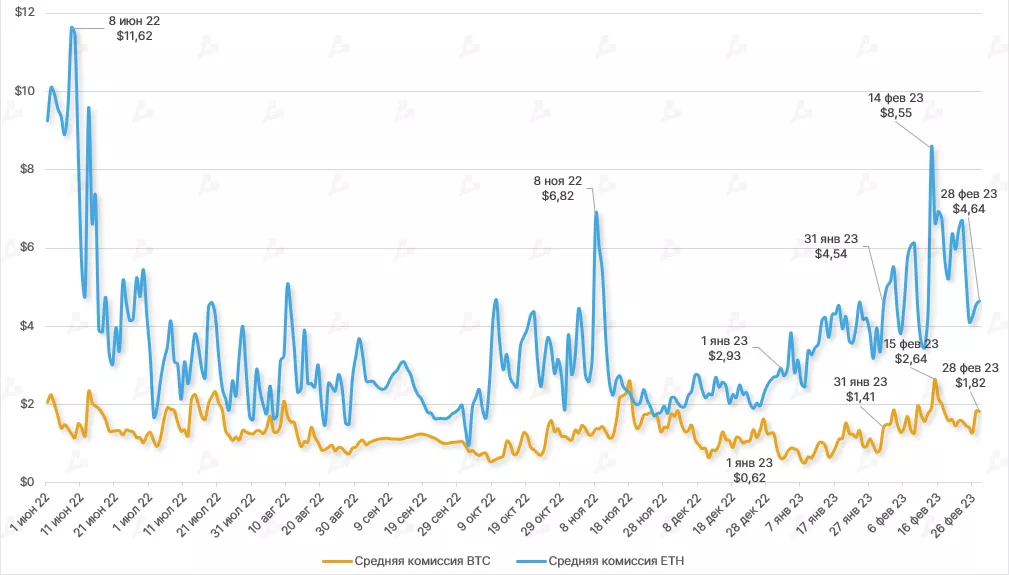

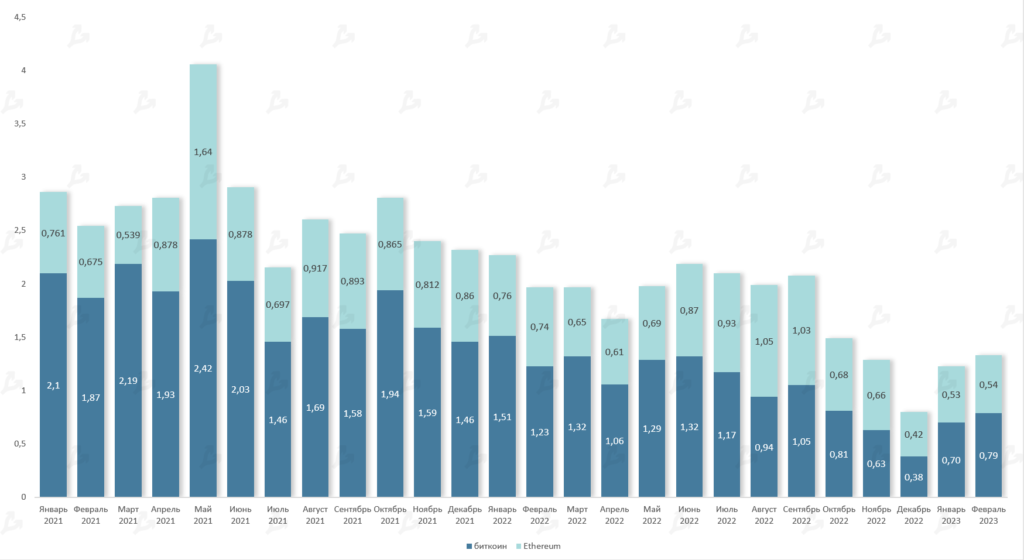

- Средняя комиссия за биткоин‑транзакцию в феврале выросла на 22% — с $1.49 до $1.82. Аналогично для Ethereum — во всем периоде комиссия снизилась на 7.2% — с $5 до $4.64.

- 14 февраля средняя комиссия за транзакцию в сети Ethereum достигла локального пика в $8.55. В последний раз подобный уровень наблюдался в июне 2022 года.

- Хотя ончейн‑активность выросла из-за Ordinals, февральский пик по биткоину составил лишь $2.64 (15 февраля). Это говорит о том, что NFT нового типа пока не оказывали существенного влияния на транзакции первой криптовалюты. Небольшой рост средней комиссии может быть связан с активным использованием Taproot‑подписей, которые также способствуют удешевлению транзакций.

Trading Volume

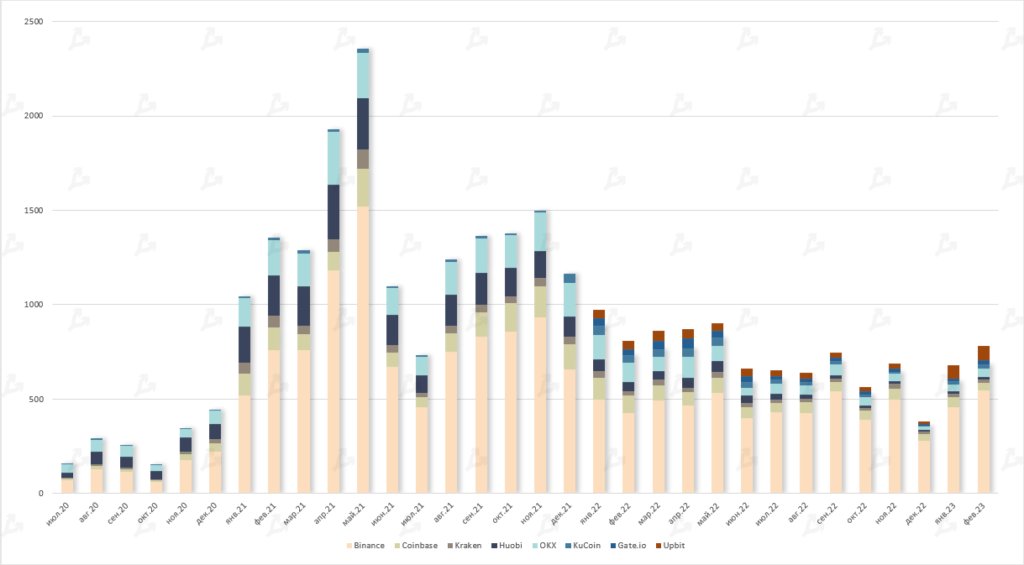

- Trading volume on the major crypto exchanges tracked by ForkLog rose 15% in February, to $782 billion.

- In the top three, OKX overtook Coinbase by volume ($44bn vs. $40bn, respectively). Gate’s volume was $78bn, while Binance remained the leader with $545bn.

Futures & Options

Trading volumes in the crypto derivatives space continued to rise, a trend that began in 2023. Options activity outpaced futures — the measure reached the highs seen in May last year, while futures hovered around October levels. In absolute terms this is $32 bn in options and $1.23 tn in futures (covering only Bitcoin- and Ethereum-based contracts).

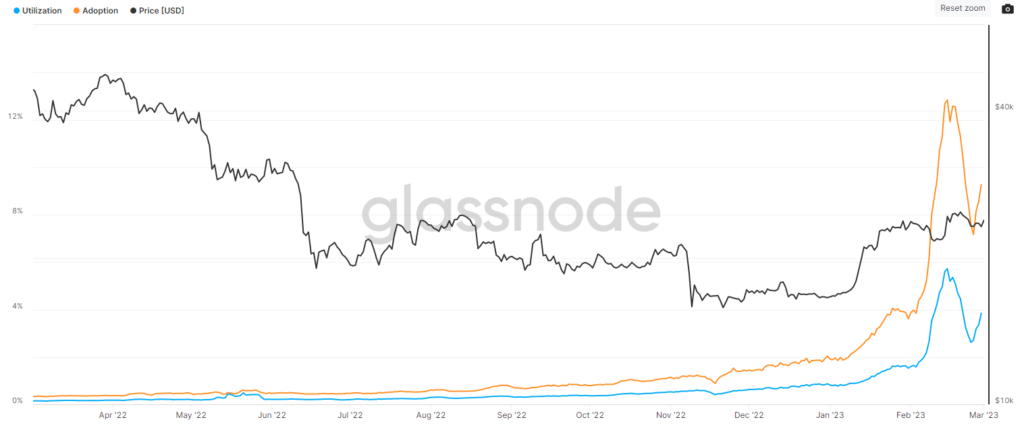

DeFi

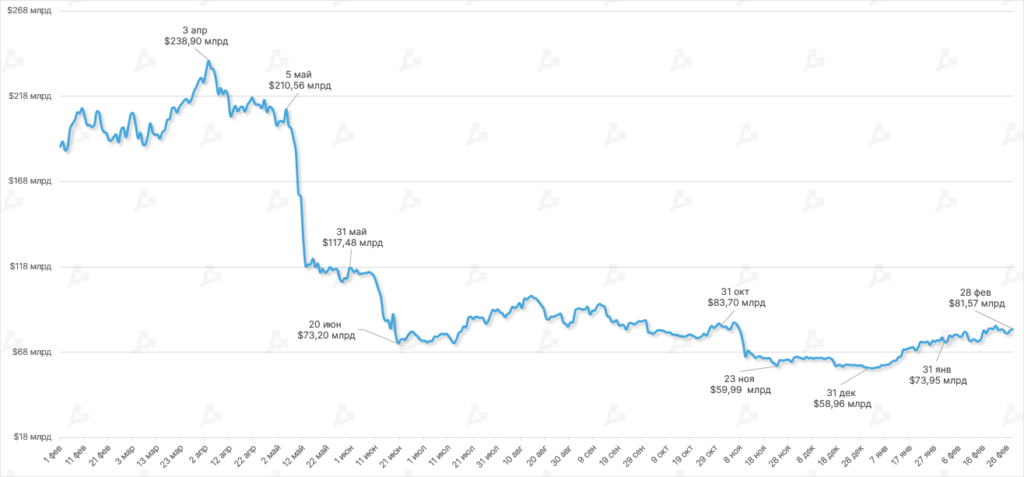

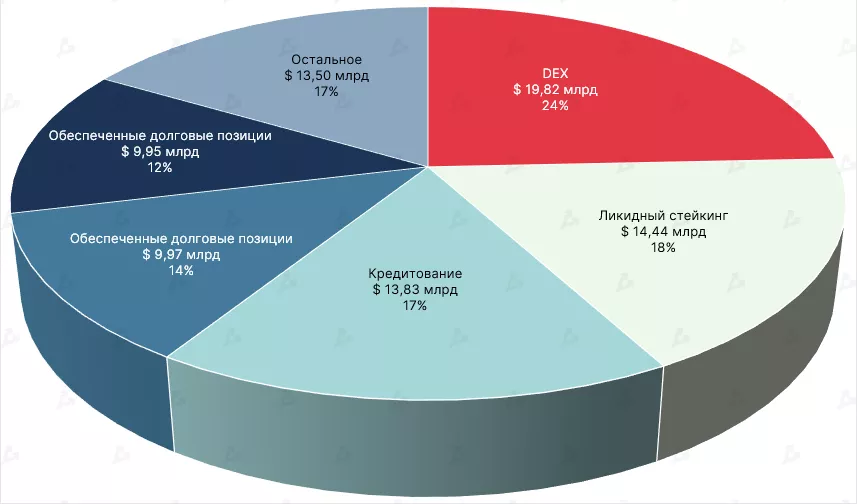

- In February the TVL locked in DeFi rose by 25% to $81.57 bn, driven in part by liquidity inflows into the Ethereum ecosystem (+14% during the period) and growing demand for Arbitrum.

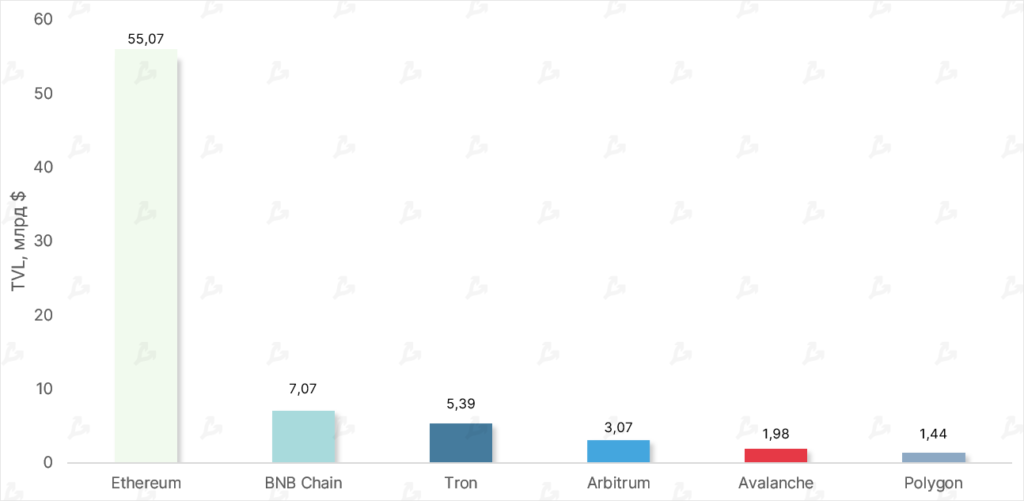

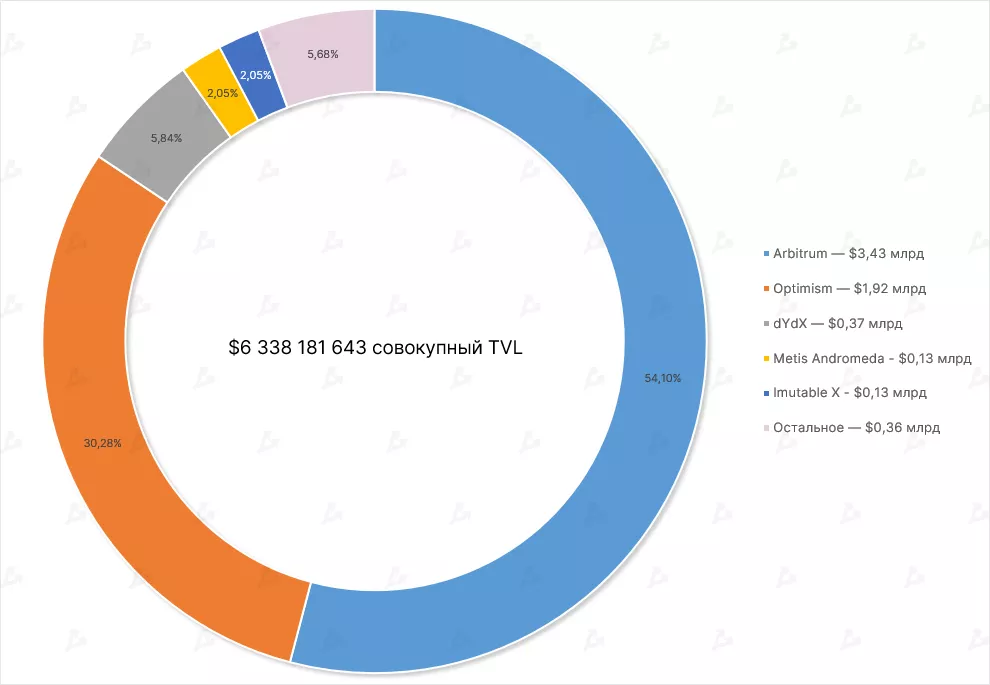

- At month-end the share of L2‑transactions on the Ethereum network approached the mainnet’s level, at times exceeding it. In February, the project’s TVL rose 62%, allowing it to overtake Avalanche on this metric.

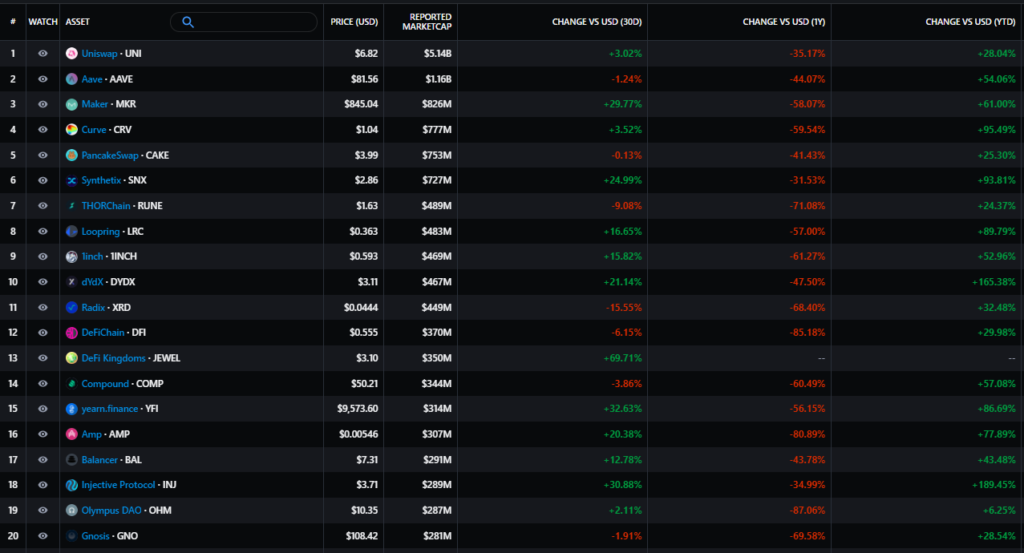

- With few exceptions, nearly all DeFi assets in the top-20 by market cap ended February in the green. The worst performer was Radix (XRD), down 15.5%.

- Within Ethereum, Lido remains the dominant TVL; ahead of Shanghai, its TVL rose again — up 18% (22% in January).

- Decentralised exchanges continued to dominate the sector’s aggregate TVL — currently accounting for 24% or $19.82 billion.

- In February liquidity- and yield-centric DeFi assets outpaced lending protocols. The category’s TVL rose 16% during the month to $14.44 billion.

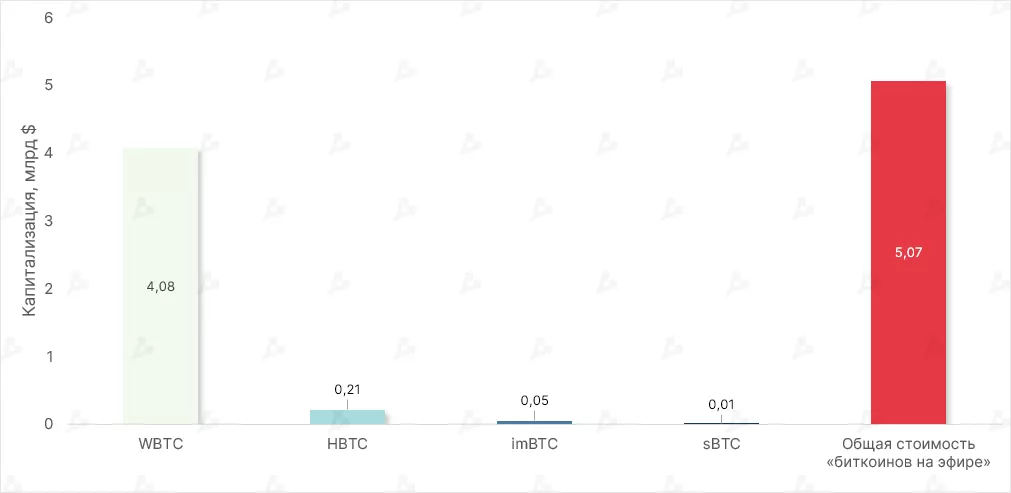

- During the period the total market value of “Bitcoin on Ethereum” fell 23%. This is likely linked to Celsius actions, which late in the month repaid more than 22,700 WBTC.

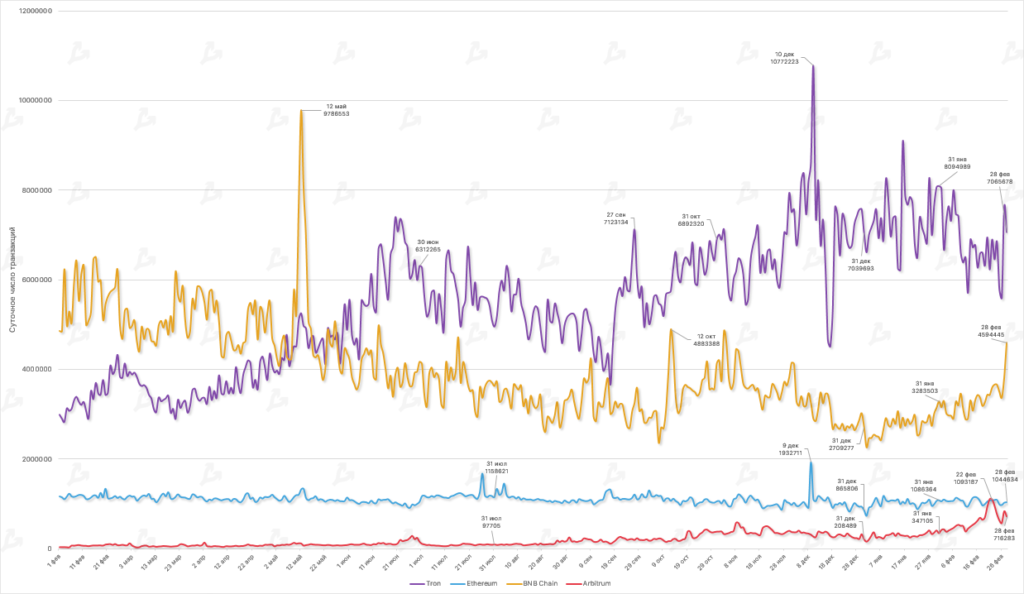

- Tron remains the leader for on-chain activity in February, processing an average of 6.8 million daily transactions, down from January’s 7.36 million.

- Arbitrum’s metric doubled — the L2 solution processed 616,719 transactions on average, still below Ethereum’s 1.1 million.

- Meanwhile, on 22 February the network surpassed second-placed blockchain in terms of activity. The rise was driven by growth in non-custodial and lending platform usage.

DEX and L2

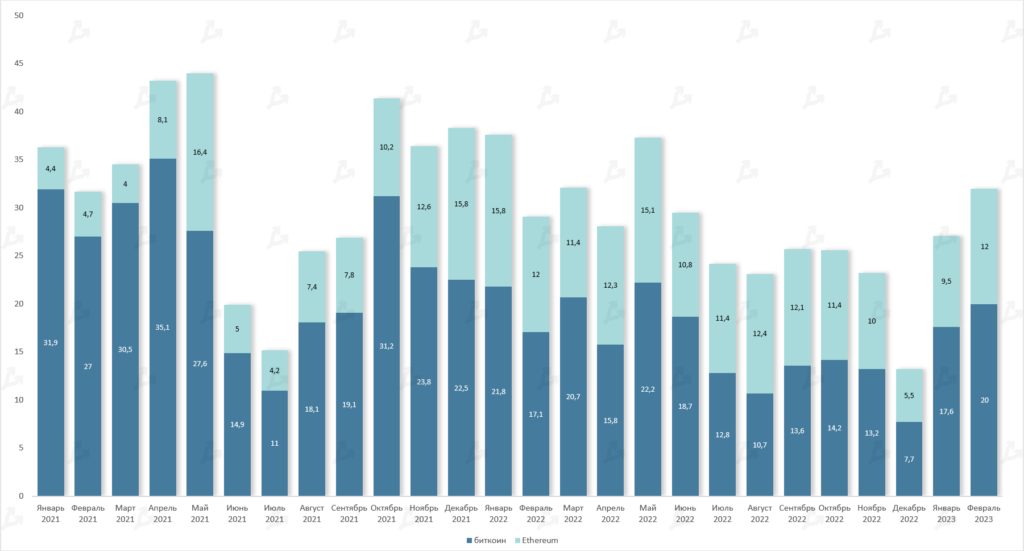

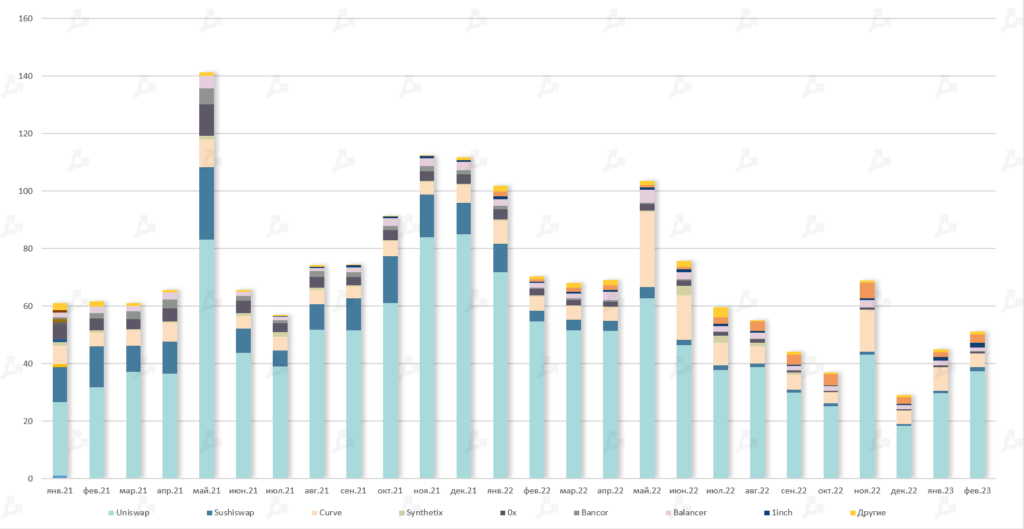

- In January, trading volume on decentralised Ethereum exchanges reached $51bn.

- The main share is held by three protocols — Uniswap ($37.2bn), Curve ($4.7bn) and DoDo ($2.8bn).

- In February Arbitrum’s share among L2 solutions exceeded 50%. The main competing product — Optimism — accounted for over 30% of total TVL.

Stablecoins

- The NY Department of Financial Services opened an investigation into Paxos, the issuer of USDP and BUSD, against which the regulator (later joined by the SEC) ordered Binance to cease minting BUSD. Paxos subsequently severed ties with Binance but committed to honoring redemptions for the next year.

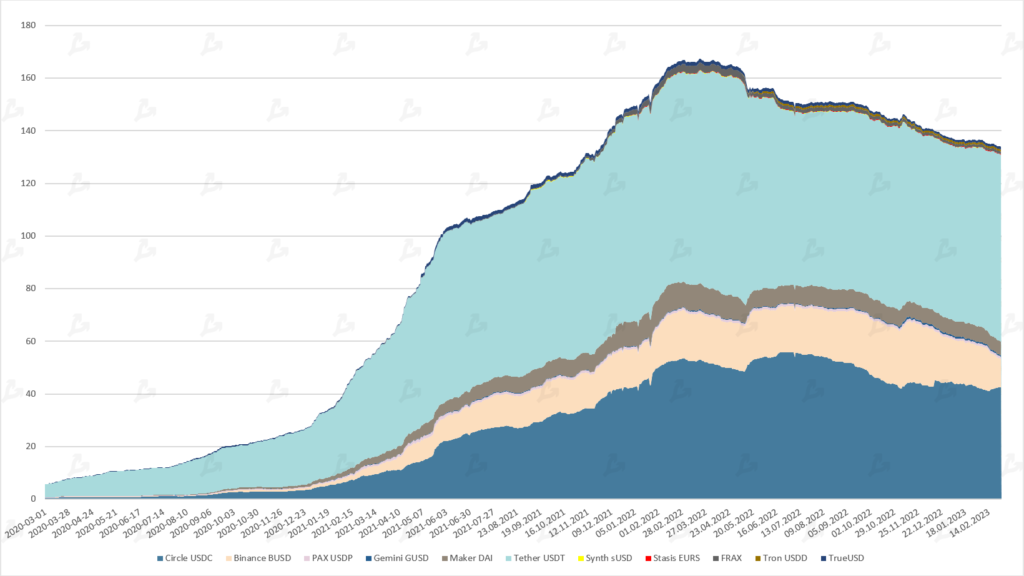

- As a result, BUSD’s market cap fell by $5.4bn, and the overall stablecoins market dropped to $133.8bn, matching late-2021 levels.

- Binance’s CEO acknowledged that BUSD will eventually depart from exchanges, while the firm plans to support alternatives, including non-dollar-pegged ones. True USD emerged as one such option, with issuance exceeding $1bn for the first time.

- In light of demand for stablecoins, the USDT supply increased to $70.9bn from $67.8bn. USDC’s market cap remained flat.

- Towards month-end the Frax Finance community decided to abandon the algorithmic backing of the FRAX stablecoin.

NFT

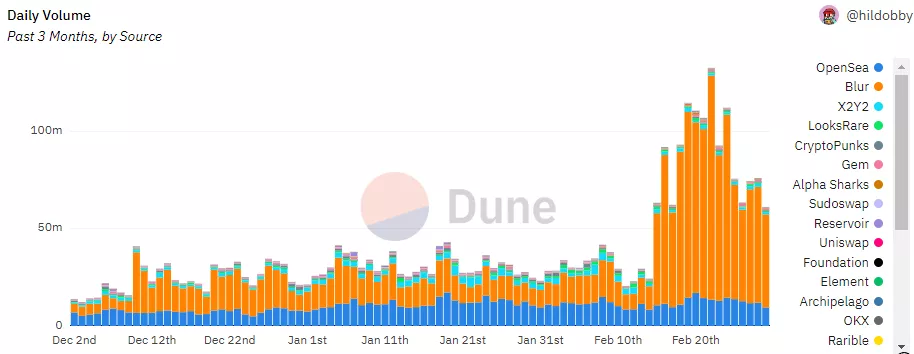

- Trading volume on NFT marketplaces rebounded as Blur challenged OpenSea. Blur drew attention in February with a generous airdrop of its native token BLUR, which promptly appeared on leading platforms, with Binance notably absent. Reports say Blur is raising funds at a $1bn valuation.

- In February Blur’s volume reached $1.21bn versus $333m for OpenSea. The newcomer announced an additional distribution of 300m tokens, and the revealed CEO urged a boycott of the flagship. The result was that the leading marketplace had to alter its royalty model.

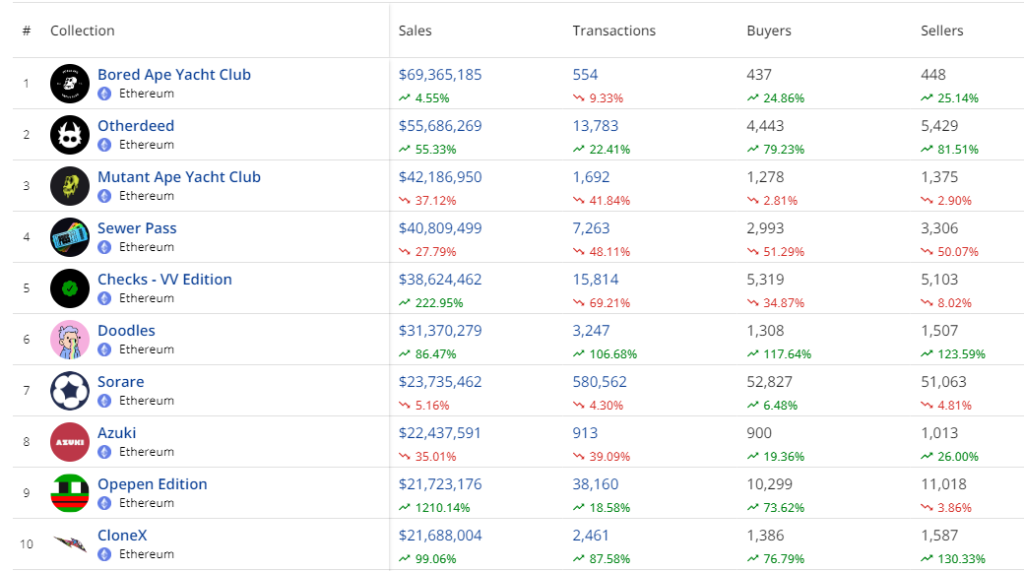

As the segment revived, new leading collections emerged while legacy premium collections remained in play. In some cases volumes and transactions rose by tens or hundreds of percent. The same pattern was seen across blockchains, with Ethereum remaining the undisputed leader.

- In February the Ordinals protocol launched — “attacks on the network” according to supporters of Bitcoin. Ordinals allow recording up to 4 MB of data in a Bitcoin block. Network activity surged mempool, and the average block size grew from 1.5–2.0 MB to 3.0–3.5 MB.

- By month-end the total NFT count on Bitcoin exceeded 250,000, and the Ordinals fork was launched on Litecoin.

Activity of major players

- Most public company digital holdings were unchanged in February. One of the largest Bitcoin holders, MicroStrategy, did not acquire or announce purchases of Bitcoin in early 2023.

- In February the software company reported that its Q4 2022 net loss was $249.7m. The write-down of Bitcoin holdings and the price drop weighed on MicroStrategy’s results. The company sold 704 BTC but remains the owner of 132,500 BTC, whose value fell by $197.6m.

- Nevertheless, MicroStrategy managed to raise $46.6m since September 2022 by selling its securities.

- Last month it emerged that Marathon Digital sold 1,500 BTC in January to cover some costs. CEO Fred Thiel said additional sales would follow to finance monthly operating expenditures this year.

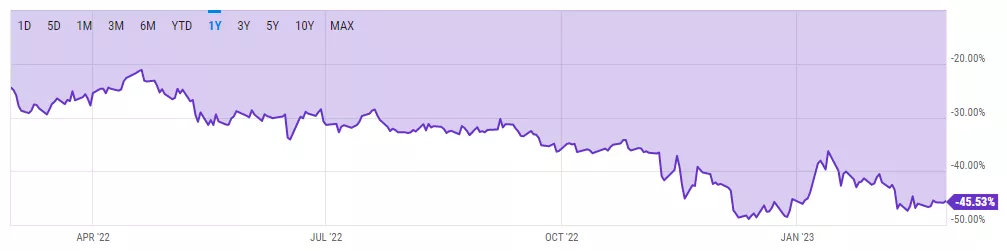

- BTC Trust (GBTC) quotes remain at a very low level relative to NAV — around -45.5%. The situation is worsened by Digital Currency Group (DCG)’s deteriorating finances.

- According to the Financial Times, DCG began selling shares in major crypto funds managed by Grayscale at a substantial discount.

- In 2022 Digital Currency Group reported a net loss of $1.1bn.

Major venture rounds

Chain Reaction, a hardware company focused on blockchain devices and privacy chips, completed a Series C round led by Morgan Creek Digital.

Taurus, a European custodian for institutions, closed a Series B round led by Credit Suisse.

Coincover, a цифровых активов protection and insurance service. Round led by Foundation Capital.

Superplastic, a 3D studio that previously released an NFT on Ethereum in collaboration with a fashion brand Gucci. Investment round led by Amazon’s venture arm.

Kratos, an Indian Web3 startup, valued at $150m. Round led by Accel.

Regulation