Which trading strategy—futures or spot—best matches today’s crypto market? Oleg Cash Coin shares his answer with ForkLog readers.

HODL as a philosophy

The cryptocurrency market has brought not only a new technological asset class with the potential to change the world, but has also given the wider public access to professional trading tools. Among the most used are options, futures and other derivatives.

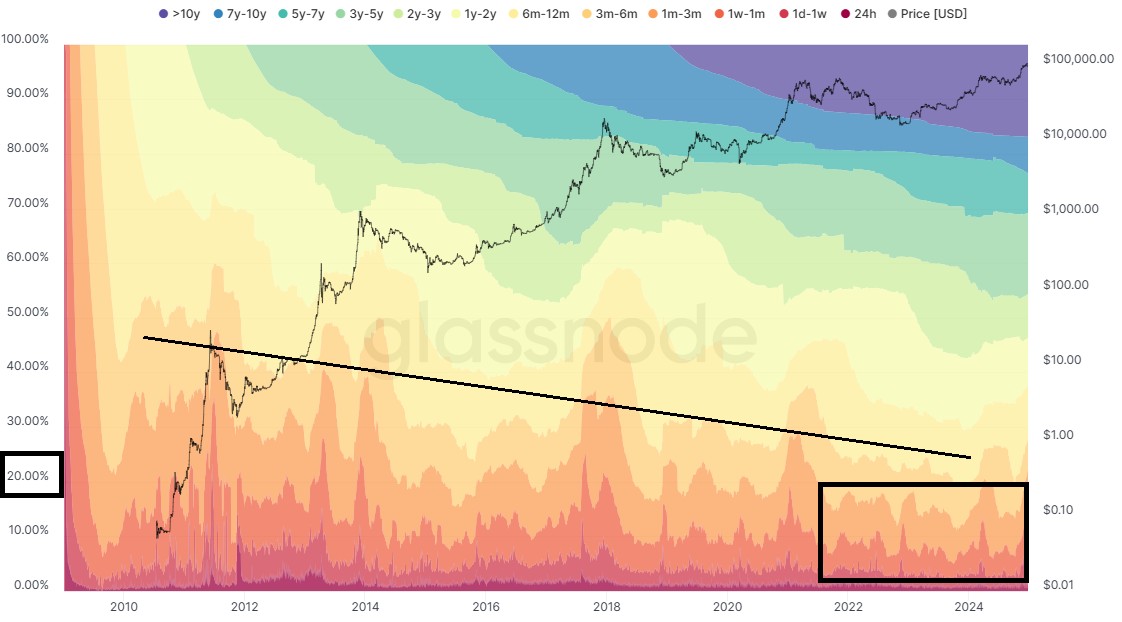

According to IntoTheBlock, cumulative Bitcoin futures trading volume in December 2024 was almost $1.8 trillion, while the dollar value of on-chain transactions in the first cryptocurrency stood at $1.7 trillion over the same period. In other words, real-world use of digital gold, measured in fiat, is already below the speculative component of the BTC market. For comparison, spot volumes are roughly six to seven times smaller than futures.

And if around 20% of coins are in active, constant circulation, one can, with some stretch, derive a conditional market multiplier of about 1 to 5, which is shrinking over time. In effect, only about 20% of actually moved bitcoins provide liquidity for the entire market.

The futures market has grown steadily since about 2019, with a brief dip after FTX’s collapse in 2022. Notably, the pulling of liquidity and the “locking up” of bitcoin have coincided with the popularisation of HODL.

“Buy and hold” is not only an economic strategy but a philosophy dear to many investors. It removes the need to speculate on short-term volatility—the fuel the market has used for derivatives in recent years.

Buy physical bitcoin (spot) and hold it as long as possible in a personal cold wallet—that is the essence of HODL. Yet this approach is far from universal, as the colossal size of the derivatives market attests.

Sadly, futures themselves have changed beyond recognition. Originally, the instrument was used as a contract for the delivery of goods at a pre-agreed price at a set time. Agree in spring to deliver a tonne of grain in autumn at price X—that is the futures contract.

But on today’s crypto market, for the masses a futures contract means leveraged trading to amplify returns, where anyone can turn $10 into several thousand in a couple of clicks. Yet there is another side: “On 19 December, the volume of forced liquidations in the cryptocurrency market totalled $1.01bn, including $844m in longs.”

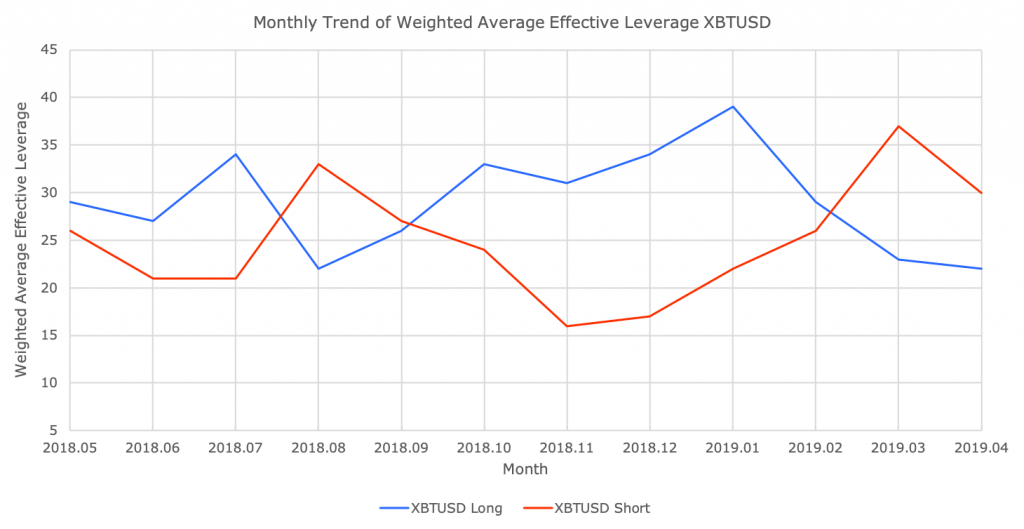

What such stories lack is the average level of leverage used in trading. It is a pity exchanges no longer publish such statistics—it would be interesting to see them. Some historical figures, though, remain.

BitMEX data for 2018 and 2019 show that users’ effective leverage ranged between 20–30x. That is quite a lot for a period when spot and futures trading volumes were roughly 1 to 1.

On highly volatile yet most-liquid bitcoin at the time, the concentration of effective leverage up to 50x is striking. What then to say of meme tokens that now arrive on, say, Binance with leverage up to 50x or even 75x.

Returning to the HODL concept, which excludes the gambling element, one can only guess what the market—and bitcoin’s price—would look like if only spot coins were traded.

Of course, many will point out that miners, for example, need futures to plan business processes, and that is a fair remark. Yet such instruments are interesting and useful chiefly to professional traders, who are very few in the overall user base.

Almost 100 years ago, analysts had already concluded that even without futures, one can lose a fortune trading only spot by succumbing to volatility. Human emotions and temptations such as greed and fear have scarcely changed over the years.

“I would have gone broke if I had been confused and distracted by minor changes in the market. Real movements do not end on the day they begin,” wrote Jesse Livermore in his 1940 book “How to Trade in Stocks.”

Why spot, after all

The dispute between spot and futures trading comes down to the difference between investment and speculation. When a market participant plans to invest in a promising direction that provides value over the long term, he will not use leverage. He does not need the ability to open short positions or other derivatives.

By contrast, a futures trader is not interested in the prospects of a project or asset as a whole—only in price movement and volatility from which profit can be extracted.

Following this logic, we are dealing with two quite different types of people. Some remain conservative market participants who value personal ownership; others follow new trends such as the sharing economy, in which there may be nothing personal at all—everything is rented for a time, with no thought for the future.