Since 2020 a clear correlation has emerged between net liquidity, bitcoin and the S&P 500. The latter abruptly broke from the pattern amid the US election campaign.

Oleg Cash Coin unpicks what this means and where the stablecoin market comes in.

What global liquidity tells us

In markets, liquidity usually means money being injected into the economy and, as a result, flowing into cryptocurrencies and securities (or the reverse, with funds withdrawn from intangible assets).

An increase indicates how quickly assets can be turned into cash, improving safety for market participants by lowering costs and allowing them to deploy capital at any time.

In America’s financial system this process is steered by the the Fed via changes in the policy rate. To raise it, the agency goes into the open market and sells, say, US Treasuries, keeping “cash” on its balance sheet. That drains liquidity from the market.

When a cut is needed, the reverse happens. In that case the Fed goes into the market and starts buying bonds, injecting liquidity. The agency influences rates directly to create optimal conditions for lending by making credit dearer or cheaper.

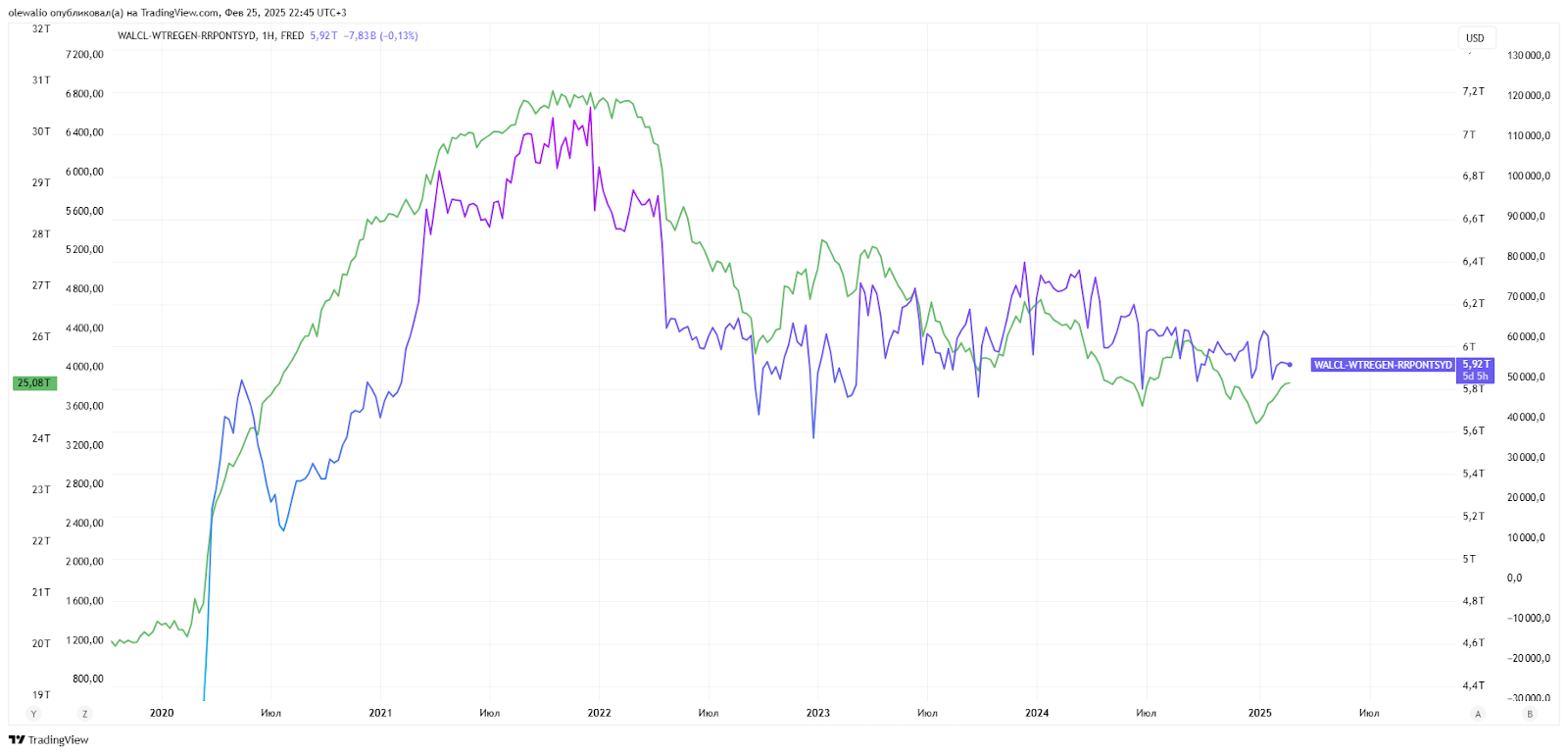

This involves the Fed’s balance-sheet as well as the accounts of the US Treasury and the Fed. Together they form the chart of so‑called net liquidity—that is, money flows from the monetary authorities into the financial system.

From the pandemic onwards, risk assets, including crypto, tracked net liquidity closely. That held until the 2024 US election campaign. Then the S&P 500 stepped out of line for several months, leaving bitcoin to keep correlating with net liquidity.

One might object that America is a big financial centre but not the whole world. True. Yet the global liquidity gauge (the US, the UK, Japan, China and the euro area) looks much the same as in the States.

Thus markets found themselves in a world where their long‑standing correlation with system liquidity vanished with the start of the US campaign. After Donald Trump’s victory the divergence only widened.

Where the money for the rally comes from

As the co‑movement of risk assets (bitcoin and equities) faded, monetary aggregates began to rise. Analysts often point to M2, which reflects the amount of readily accessible money in the economy.

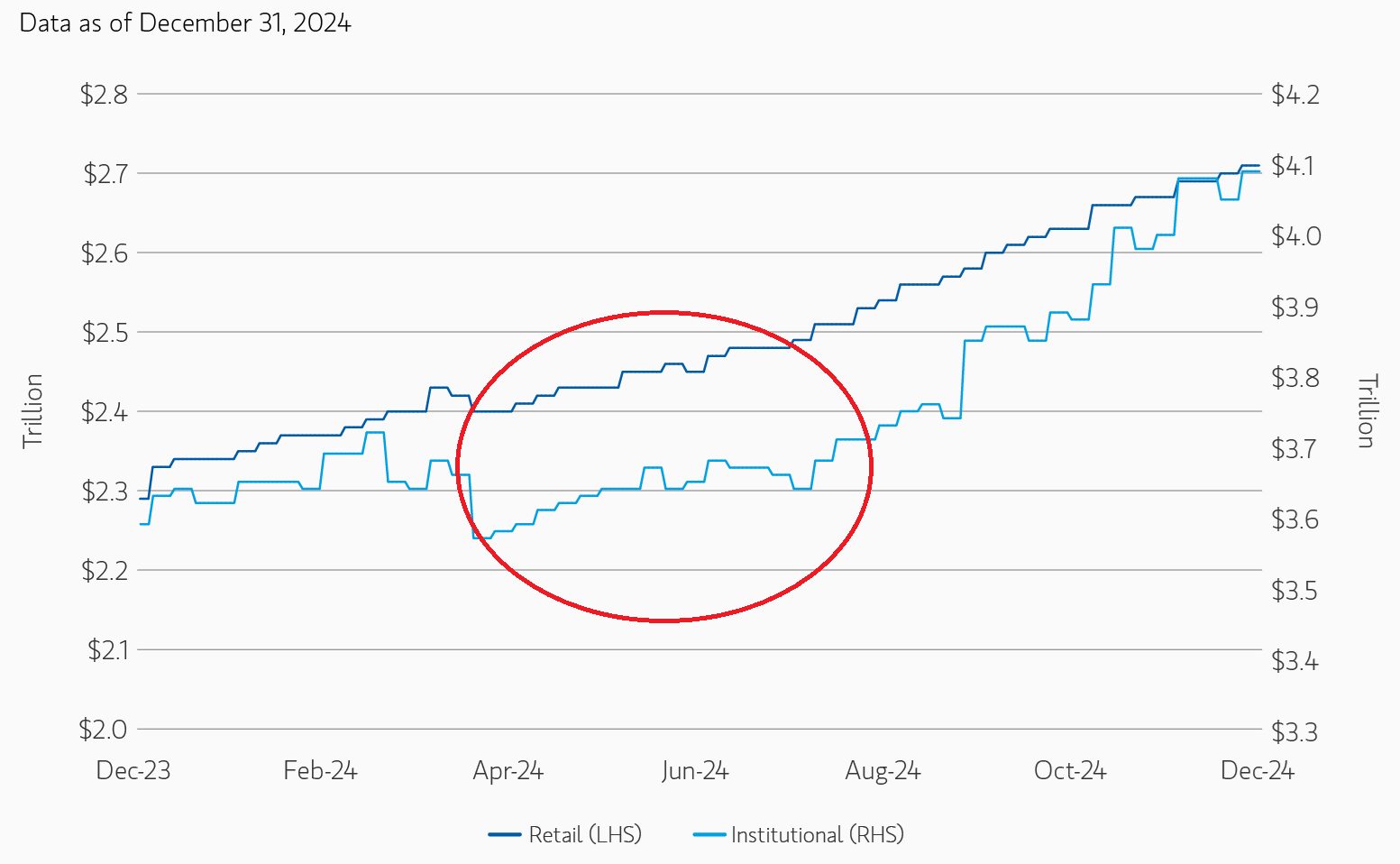

But its rise may be driven by huge inflows into money‑market funds (MMFs), which are included in the aggregate. MMFs invest only in short‑term, highly liquid instruments. They may also be counted on banks’ deposits as collateral for lending.

Just as net liquidity decoupled from risk assets, these markets quickened their pace of growth:

As Morgan Stanley’s analysts noted in a 2024 report, the initial assumption was that investors might rotate out of MMFs into other asset classes, but economic uncertainty and other factors boosted demand. In the US MMF assets reached $7trn. Notably, retail funds even outpaced institutional ones by inflows.

That still does not explain what propelled equities and crypto through most of 2024 and into the start of the current year.

So what is going on?

The answers likely lie in the formation of new correlations that are only just being discussed. Echoes of such analysis can be found in reports from traditional financial institutions.

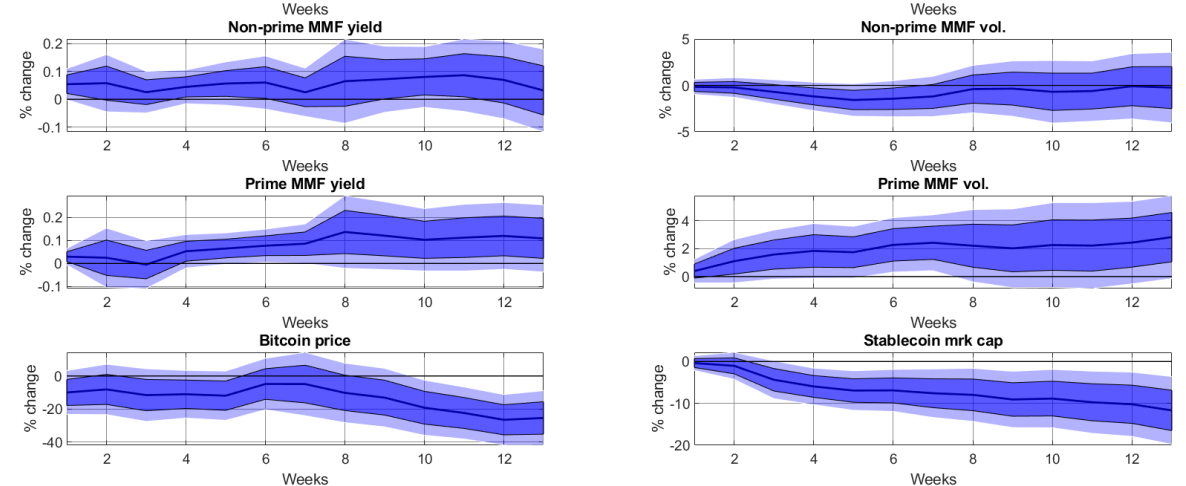

For example, the Bank for International Settlements (BIS) published an intriguing observation about MMF assets and the stablecoin market. Analysts found that US monetary policy negatively affects “stable coins” in particular. In its end‑2024 report, BIS experts concluded that tightening affects MMFs and stablecoins in different ways.

“Prime MMFs generally grow after a restrictive monetary policy, while the market capitalisation of stablecoins declines,” the document says.

BIS noted that stablecoins’ market capitalisation fell by roughly 10 percentage points over three months. The drop is statistically significant and persistent, and monetary policy’s impact on stablecoins is far stronger than that of stresses that drive bitcoin prices down by a similar magnitude.

Specifically, the experts said the fall in aggregate stablecoin capitalisation was driven by the responses of Tether and USDC, which are in some sense akin to MMFs because of the reserve structures backing their issuance.

Any early guesses about liquidity’s influence on crypto markets should consider the effect of US monetary policy on stablecoins, which have become central to the digital‑asset market. Activity in the coming years will probably revolve around them. That, at least, is suggested by the actions of the Donald Trump administration, which has chosen “stablecoins” as the main instrument for spreading the dollar to the masses.