Unlike the turmoil of the previous year, 2023 was short on drama. The standout events were Binance’s settlement with US authorities and the departure of Changpeng Zhao as head of the world’s largest crypto exchange.

DeFi has yet to recover from the collapse of Terra and the implosion of Sam Bankman-Fried’s empire, both of which had far-reaching consequences for the industry. For most of the year the “financial Lego” languished in stasis, with signs of life only emerging late in the autumn.

Developers nevertheless kept building, launching new products and refining existing ones despite market conditions. Promising areas include L3 solutions, Web3 social networks, appchains and account abstraction. Rollups and other layer-2 scaling technologies also continued to advance in 2023.

- Despite a broader market rebound, the TVL of decentralised finance remains roughly 70% below the all-time high near $200bn reached in December 2021.

- Ethereum still tops the ecosystem rankings by TVL, while Uniswap leads in trading volumes.

- New technological avenues (L3, rollups, account abstraction) and segments (RWA, Web3 social) are gathering steam.

- Institutions remain wary of DeFi, chiefly because of frequent hacks and scams, strict KYC/AML requirements and regulatory uncertainty.

Stagnation

The dramatic events of 2022 dealt a heavy blow to crypto, triggering a plunge in TVL and a prolonged DeFi slump.

As of 1 January 2023, the sector’s TVL stood at $43.7bn—around 80% below its ATH.

In April the figure climbed above $60bn, but the rally was brief—by October TVL had slipped below its level at the start of the year.

In November, as the broader market recovered, sector liquidity began to grow again. Yet as of 24 December the aggregate DeFi TVL remained a modest $60bn.

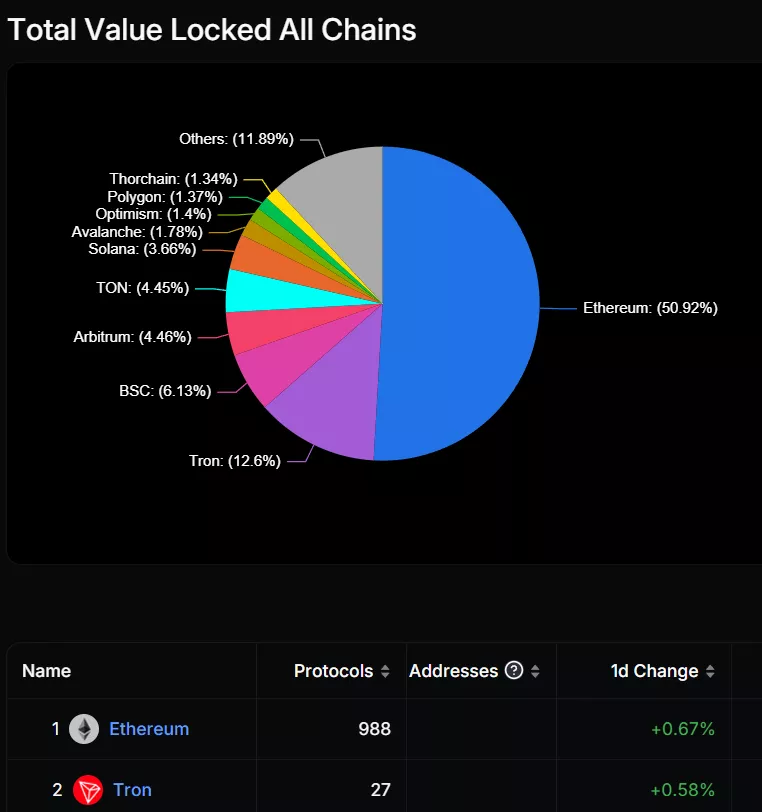

As before, DeFi built on Ethereum dominates the segment, accounting for just over half of total TVL.

The second-largest ecosystem is Tron with roughly 1.4m active addresses, compared with around 490,000 for Ethereum.

The largest aggregate TVL sits in liquid-staking protocols (LSD) at about $31.9bn. Lending is next ($22.22bn), followed by cross-chain bridges ($14.4bn) and DEX ($14.22bn).

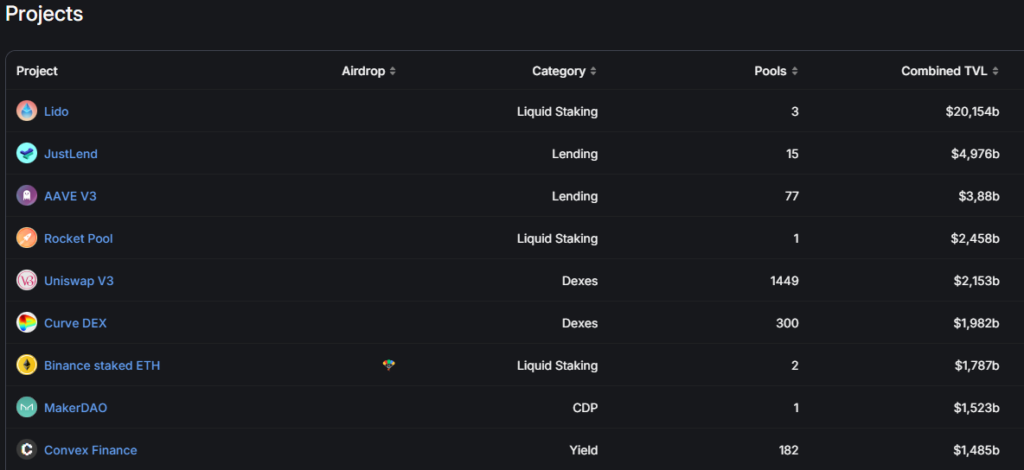

Lido remains the undisputed leader among liquid-staking protocols, with TVL above $21bn (as of 24 December). Its nearest rival, Rocket Pool, stands at $2.71bn.

Lido leads not only within its category but across all DeFi projects by TVL.

In October the Lido Finance community decided to end support for Solana. It is also considering dropping liquid staking for Polygon’s token.

LSD protocols are so popular they materially influence Ethereum’s supply structure and issuance dynamics. On lending platforms, derivatives such as stETH were more attractive than ETH in 2023.

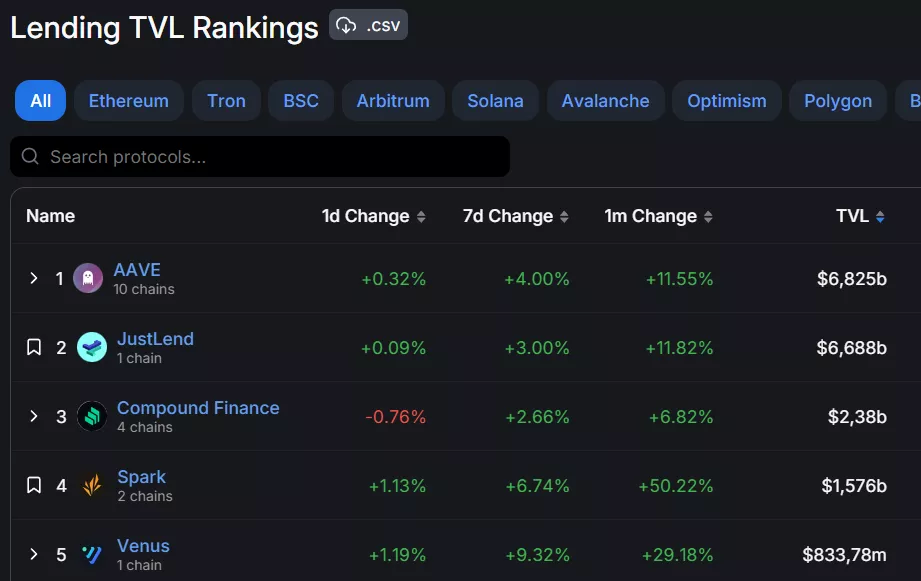

Competition is fiercer among lenders—Tron’s JustLend trails Aave by a small margin despite the latter supporting ten different networks.

Third place among lending projects goes to a DeFi veteran, Compound, whose TVL lags the leaders by more than $4bn.

In September Compound Labs launched a lending service for institutional investors.

A month earlier, developers integrated Base, Coinbase’s layer-2 network.

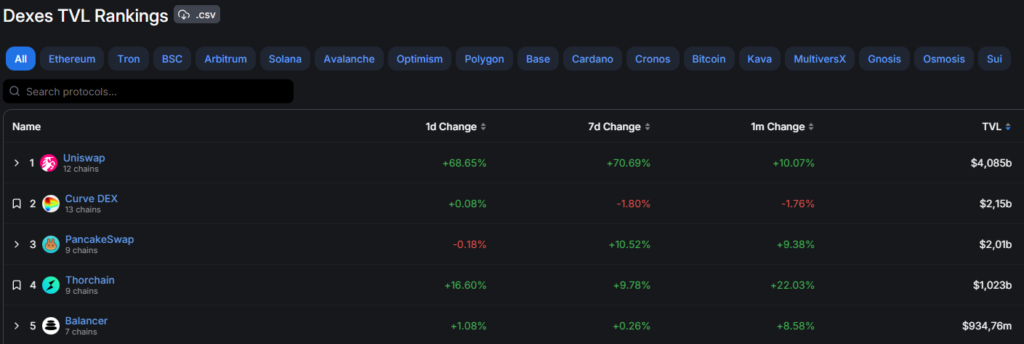

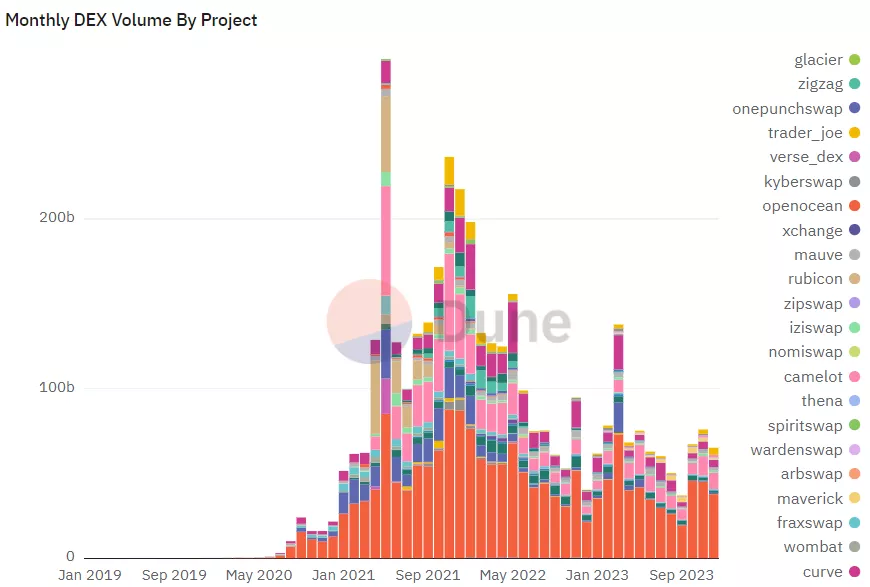

Among DEXs, Uniswap has long been the unchallenged leader. Curve, focused mainly on stablecoins, ranks second by TVL. PancakeSwap is third; in November it launched a gaming marketplace.

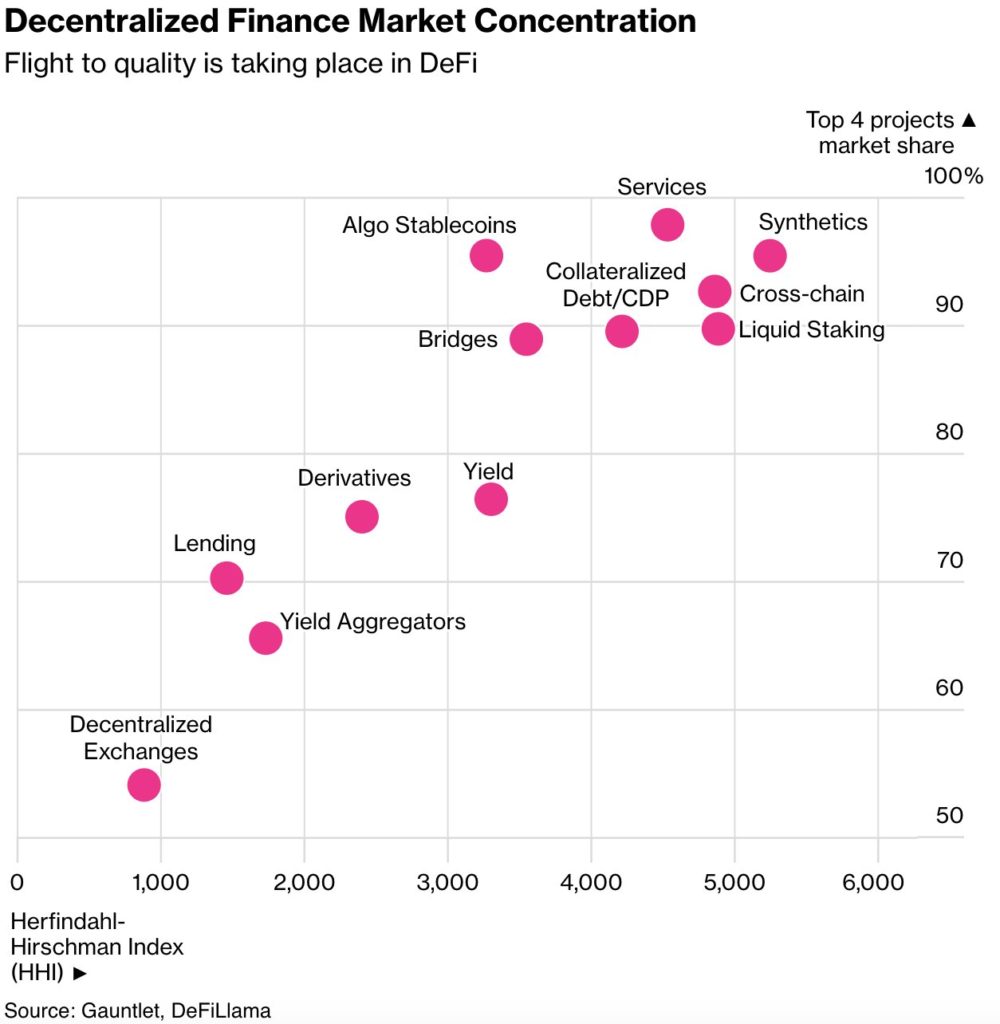

According to Gauntlet, competition is fiercest among decentralised exchanges.

For two years DEX volumes steadily declined from the May 2021 peak. The downtrend is shown below:

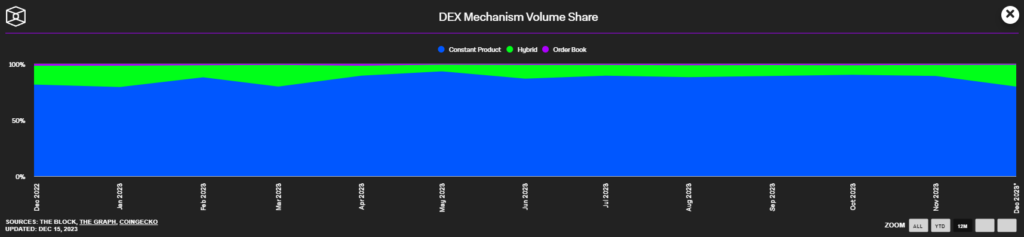

About 80% of non-custodial exchanges use automated market makers.

By late December, order-book DEXs accounted for less than 1% of volume, while “hybrids” made up about 19.4%.

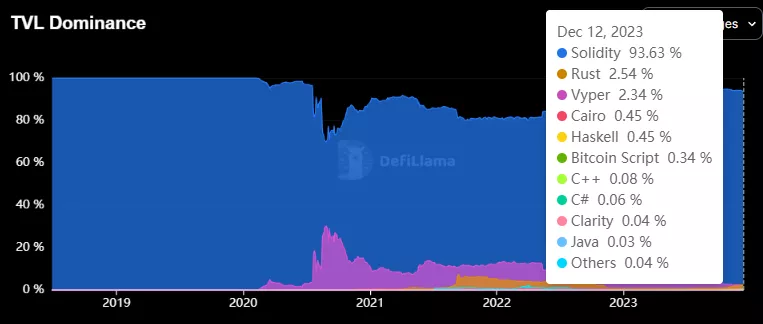

The vast majority of dapps are written in Solidity:

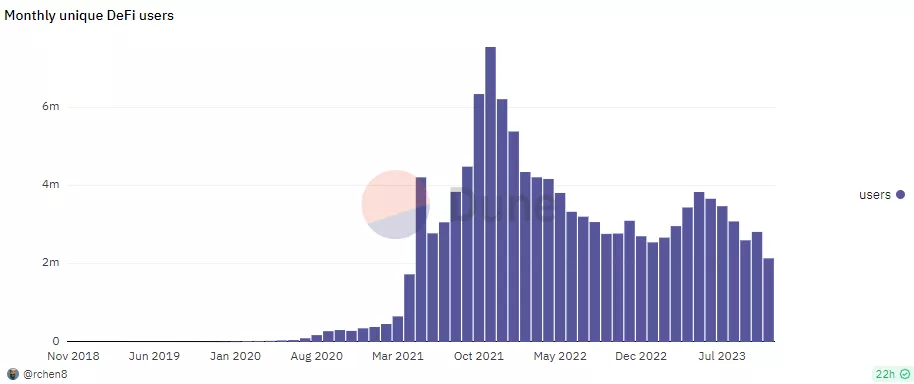

Stagnation shows not only in TVL: user growth also fell. December 2021 recorded over 6.2m users; two years later there were just 2.49m (-60%).

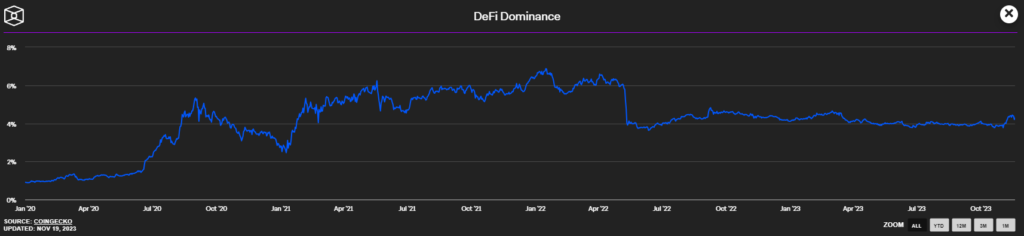

DeFi Dominance has barely budged since May 2022—the month Terra collapsed. In December 2023 it was around 4.4%.

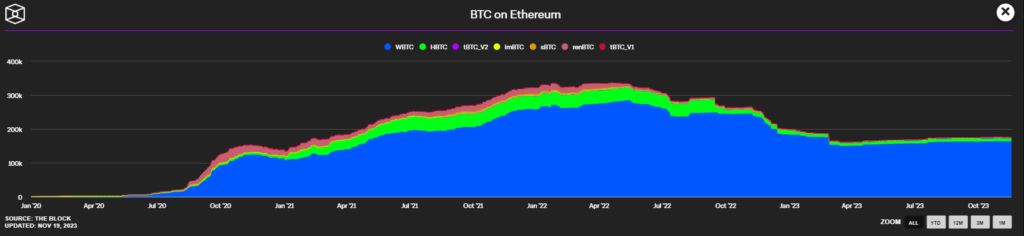

The supply of “bitcoin on Ethereum” also fell in spring 2022. It stabilised around 164,000 a year later, then began to climb gradually as the broader market recovered.

Ubiquitous hackers

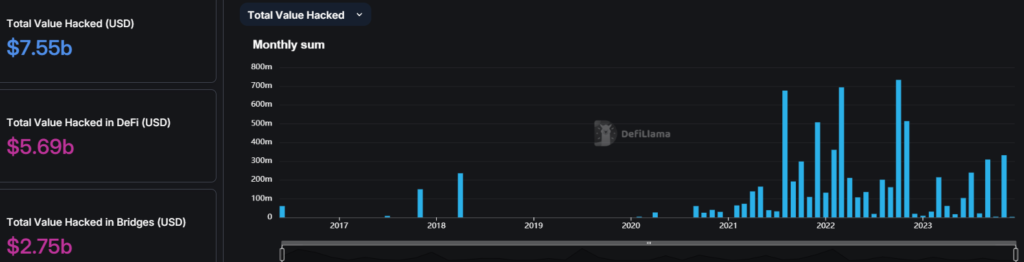

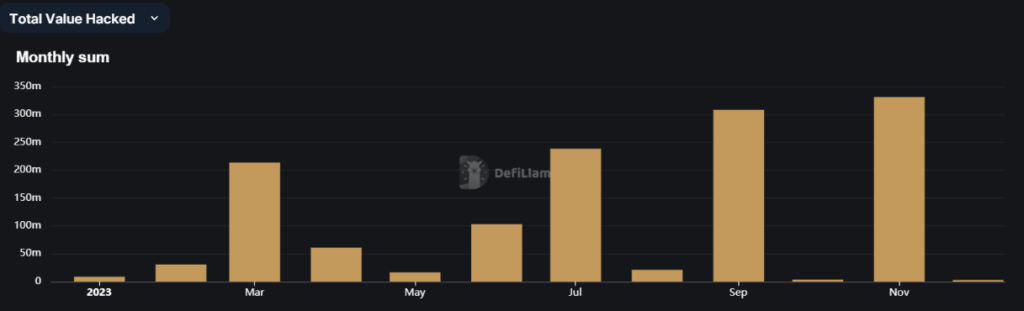

In 2023 reports of platform breaches landed almost daily. According to DeFi Llama, total losses to users of decentralised apps from hacks exceed $5.69bn.

Cross-chain bridges remain a prime target; cumulative losses in this niche exceed $2.7bn.

A recent high-profile case was the Heco Bridge hack and, as if in addition, the compromise of exchange HTX’s hot wallet. Analysts put the loss at $110m.

September and November 2023 were especially “productive” for hackers, with $308m and $331m respectively stolen from DeFi protocols.

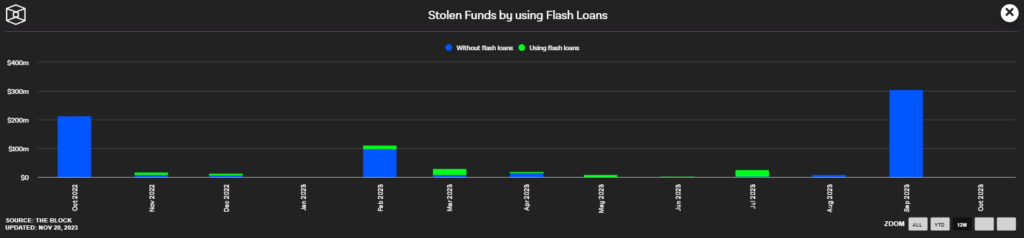

At the start of autumn, attackers actively exploited flash-loan vulnerabilities.

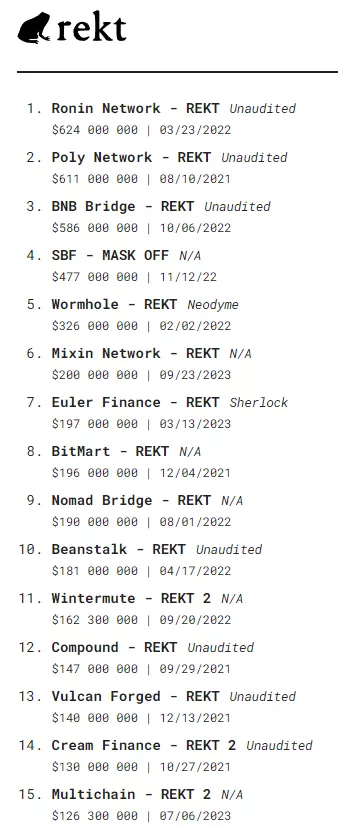

However, per rekt, the biggest exploits occurred in 2021–2022: Ronin Network ($624m), Poly Network ($611m) and BNB Bridge ($586m).

The biggest hacks of 2023 were Mixin Network ($200m) and Euler Finance ($197m). These are hefty sums and, given the still-high frequency of such incidents, risk exposure remains a pressing concern.

At times attackers are brazen with victims. After breaching KyberSwap in late November, the hacker demanded full control of the project, including all assets and documents.

November was the most lucrative month of the year for criminals: hacks and fraud cost crypto projects $343m, 15.4 times October’s tally.

On the other hand, the main vector of attacks in November was CeFi, accounting for 53.8% of total losses.

By chain, BNB Chain led with 22 incidents and 53.7% of total losses. Ethereum recorded 12 incidents and 29.3%.

Developers and security specialists are not idle, devising new safeguards for user funds. In October the MetaMask team, in partnership with Blockaid, added security alerts to the Web3 wallet’s browser extension to proactively block malicious transactions and protect users from scams, phishing and hacks.

Obstacles and prospects

Institutional scepticism

In 2023 talk of institutional adoption returned amid hype over potential approval of spot ETFs based on bitcoin and Ethereum.

Many analysts predict strong inflows into these instruments, if approved by the SEC, alongside significant growth in digital assets.

With large players refocusing on the industry, a likely side-effect of launching spot ETFs in America would be a revival in DeFi.

Yet several barriers still stand in the way of institutional DeFi adoption. Chief among them:

- security. Crypto is rife with cases of multimillion-dollar losses from code errors and smart-contract vulnerabilities. That spooks many financial institutions exploring the sector;

- data privacy. Some traditional players prefer not to disclose trading history, open positions and other information competitors might exploit. Blockchain data are public and traceable, which will not suit all institutions. On the other hand, zero-knowledge-based innovations are advancing, promising private transactions and effective verification and authentication;

- regulatory uncertainty that leaves DeFi looking like the “Wild West”. The risk of supervisory scrutiny remains a serious deterrent for many traditional firms;

- strict AML/KYC obligations, which can run counter to DeFi’s permissionless nature.

To address these challenges, Haven1 Foundation head Akash Mahendra proposed several strategic steps to reduce “institutional uncertainty” around DeFi:

- top priority is stronger security: regular, in-depth smart-contract audits; bug-bounty programmes to find vulnerabilities; and wider use of multisig wallets;

- reducing regulatory uncertainty through constructive dialogue between “DeFi pioneers” and supervisors to legitimise the sector in the eyes of traditional participants;

- integrating KYC/AML solutions and striking an “optimal balance between protecting user privacy and meeting stringent regulatory standards”. This, he argues, would enable a “more secure and accountable ecosystem”;

- education and evangelisation. Misunderstanding breeds mistrust, Mahendra says; large-scale education should help institutions navigate DeFi “with renewed confidence”, deepen knowledge and debunk myths;

- interoperability and standardisation. DeFi “can benefit enormously from cross-chain solutions”, enabling “smoother and more predictable interactions between platforms”;

- transparent governance. Open, decentralised governance empowers communities by giving everyone a voice. “Collective oversight inspires trust” because decisions are made transparently.

Is another ‘DeFi summer’ near?

Despite institutional caution, JPMorgan analysts detected “preliminary” signs of recovery in DeFi and NFTs. In their view, anticipation of a spot bitcoin ETF has improved market sentiment and “the worst is behind us from a medium-term perspective”.

According to JPMorgan, the main driver of DeFi’s rebound is a pickup in DEX trading activity. Liquid staking via Lido Finance has also had a significant impact.

The popularity of Ordinals and similar protocols has buoyed NFTs, they argue. Avalanche, Fantom and Polygon have already implemented their own “inscriptions”.

JPMorgan stressed that Ethereum will benefit less as liquidity shifts to newer projects such as Aptos, Sui, Pulsechain, Tenet, Sei and Celestia. The problem also relates to Ethereum’s “scalability, lower transaction speeds and higher fees”.

MN Trading founder Michaël van de Poppe expects the return of “DeFi summer” in 2024. He observes that an increasing number of projects in the segment “are starting to rally”.

#Bitcoin still consolidating above $35,000.

Slowly, but surely, more #DeFi projects start to rally.

I wouldn’t be surprised if we get a renewed DeFi summer in 2024.

The bear market is behind us.

— Michaël van de Poppe (@CryptoMichNL) November 2, 2023

The analyst also forecasts outperformance by relatively new platforms over older ones.

By contrast, Messari founder and CEO Ryan Selkis thinks a tightening environment makes strong growth unlikely. In 2023, he notes, the rare surges in trading volumes were driven mainly by memecoins rather than breakthrough projects or broader usage.

New directions

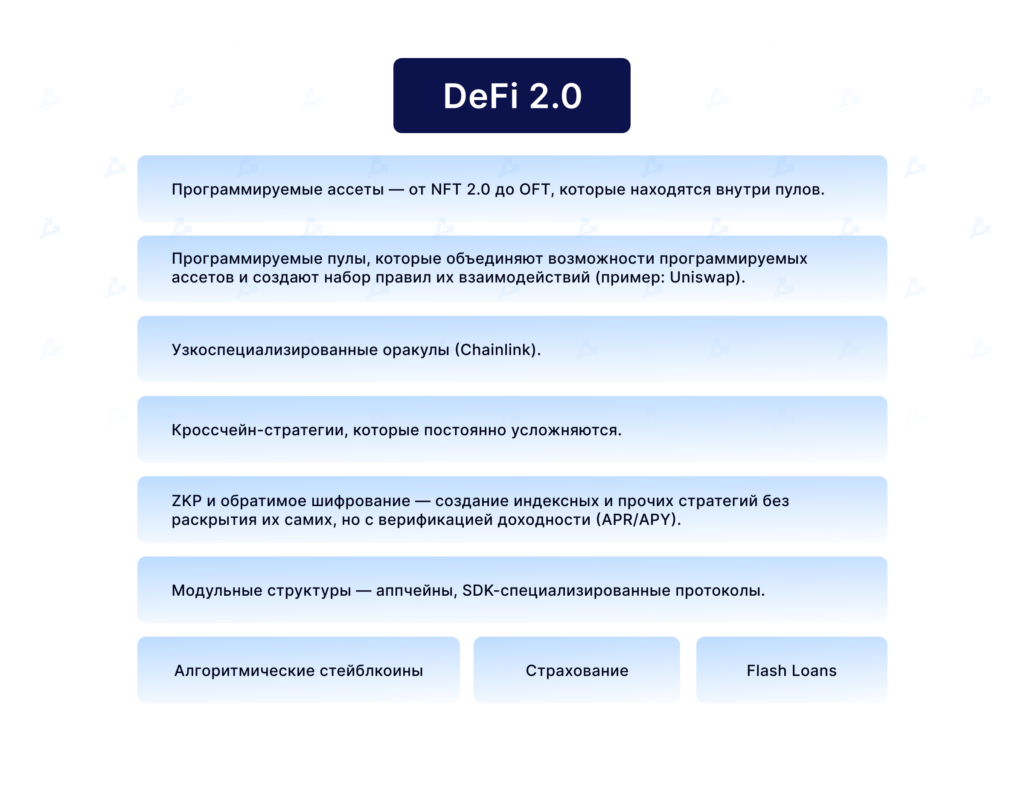

Next-generation decentralised services—DeFi 2.0—are gathering pace. Such projects aim to fix “version one” shortcomings via more efficient capital use, mechanisms to stabilise liquidity and long-term user incentives.

Web3 entrepreneur Vladimir Menaskop outlined the main building blocks of DeFi 2.0. They are shown below:

The Real World Assets (RWA) category shows particular promise, having grown despite wider market torpor.

The aggregate TVL of RWA stands at $5.6bn (as of 24 December). That exceeds the “Derivatives”, “Yield Aggregators” and “Cross-Chain” categories in the DeFi Llama rankings.

Demand for tokenised US Treasuries is rising. The total capitalisation of these products is approaching $800m. The most popular blockchain ecosystems are Ethereum, Stellar and Polygon.

Despite brisk growth even through the crypto winter, RWAs remain early-stage. Still, the segment is maturing and holds substantial potential, especially given its tiny size relative to traditional finance. Bank of America, for instance, called RWA “a key driver of digital asset adoption”.

Another emerging trend is regenerative finance (ReFi), which emphasises environmental and social outcomes.

Key ReFi themes include:

- climate initiatives;

- preservation of cultural heritage;

- renewable energy;

- building a “more equitable and sustainable” financial system.

Jasper van Brakel, CEO of San Francisco–based RSF, emphasised that the goal of the movement is “positive change, where financial return is a by-product”.

“Regenerative finance views money as a means, not an end. It is about circulation, not accumulation,” the expert explained.

Analysts at Andreessen Horowitz believe developers will increasingly focus on:

- improving user experience, including via account abstraction and in-app wallets;

- building a modular tech stack that “enables limitless innovation”;

- integrating blockchains with AI;

- zero-knowledge-based solutions.

They also remain optimistic about P2E and NFTs.

Analysts at VanEck offer equally intriguing forecasts. Highlights for DeFi include:

- KYC-enabled decentralised platforms led by Uniswap will outperform rivals without such features;

- DEXs will capture a record share of spot trading, helped by “fast blockchains such as Solana and wallets that enable automated transactions”;

- after protodanksharding (EIP-4844) goes live, layer-2 networks will take the lion’s share of trading and TVL in EVM-compatible protocols;

- NFT activity will rise to record highs; Ethereum will lead, while bitcoin’s network will continue to grow the niche via Ordinals.

Ryan Selkis sees promise in non-financial niches of decentralisation such as DePIN, DeSoc and DeSci. These projects will not soon scale to the size of their traditional counterparts, but even small market-share gains would translate into meaningful inflows.

Conclusions

Markets are cyclical. If bitcoin enters a vigorous bull phase, an “altseason” will likely follow—lifting DeFi TVL with it.

DeFi’s trajectory is tightly linked to broader market conditions and big industry headlines. Approval of a US spot ETF could embolden risk-tolerant investors and rekindle interest in the “financial Lego”.

Ethereum developers have slated the Dencun hard fork for 2024. It aims to improve scalability, lower gas fees, bolster security and deliver other refinements.

Successful implementation would open new opportunities for L2s and individual dapps. The upgrade should be a powerful growth driver for Ethereum’s flagship ecosystem and the wider DeFi market over the medium to long term.