Layer-2 (L2) solutions are a crucial pillar of Ethereum’s roadmap, and airdrops have stoked interest in them. But how sound is this strategy, and does it really lure new active participants into the segment?

Oleg CashCoin studied the statistics of four leading L2 projects and found the opposite.

How it began

Thanks to the personal efforts of Ethereum’s founder, Vitalik Buterin, and backing from venture firms Pantera Capital and Andreessen Horowitz (a16z), a network effect for L2 development took hold in 2021. The launch spree for such blockchains peaked in 2022–2023, coinciding with the vogue for airdrops as a means of token issuance.

Buterin offered the technical and theoretical foundation for L2s, calling them a core element of the roadmap for the world’s second-largest cryptocurrency. The funds, for their part, helped channel capital flows in the desired direction.

The airdrop playbook was outlined by a16z in January 2020 and included a full guide for venture firms and projects.

In essence, it was a manual for steering around regulation and “cashing out” without selling coins to the general public. L2s and issuing a governance token via a “free” distribution fit neatly into a16z’s recommendations.

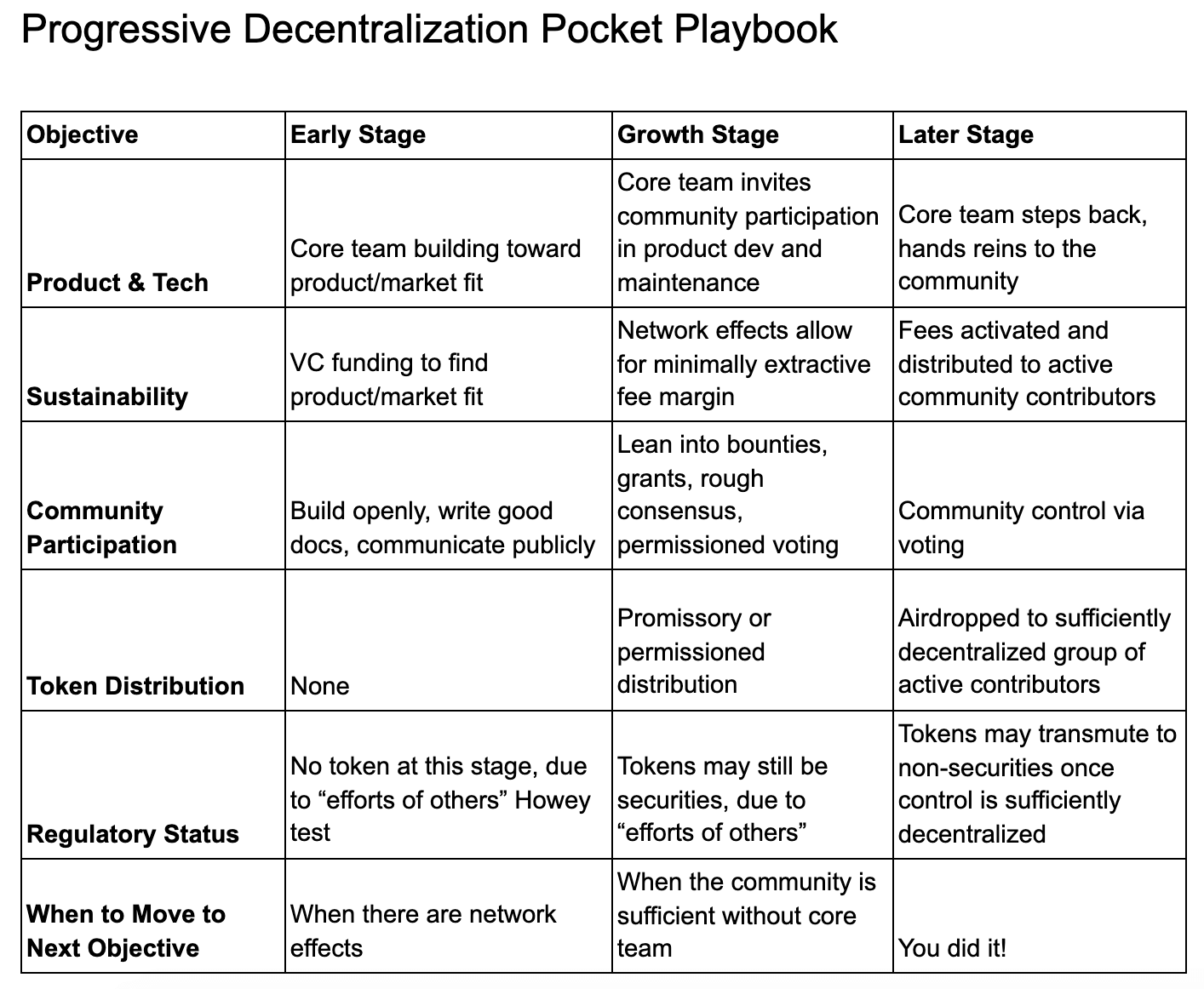

In simplified form, the main stages involved early financing and centralized control by the project team alone. Next came building network effects and engaging the community in both development and use of the L2. Retroactive airdrops helped: users’ pursuit of profit created the necessary buzz for a token launch.

The trouble is that retroactive airdrops turned out to be artificial network activity aimed at maximizing profit and then exiting the project. This may reflect technology adoption constrained to speculation. Alternatively, competition in the segment has become so intense that it erodes even the strongest network effects.

As the authors of a report from Fidelity noted, the L2 market is oversaturated, and the ways to create value for their governance tokens are highly uncertain.

“L2 tokens are not even base money in their own ecosystems,” wrote the analysts.

Though the firm sees the sector’s potential swelling to $1trn by 2030, it also argues the market cannot accommodate so many protocols.

According to L2BEAT, as of mid-September roughly 80 L2 networks are live, with about as many preparing to launch. More than 50 projects have their own token, with a combined market capitalization nearing $18bn.

What happens after the airdrop?

The L2 conundrum is the lack of universal levers to sustain interest in a token once it starts trading. What does exist are problems born of flawed tokenomics—namely, outsized fully diluted valuations (FDV) at launch.

This practice implies a small initial float—often in the low double digits as a percentage—with supply increasing gradually over several years.

By Binance Research estimates, around $150bn worth of tokens will unlock by 2030, creating immense price pressure.

Moreover, a chunk of the active user base assembled for a retrodrop often simply leaves. Projects tried to fix this by offering incentives through multiple airdrop “seasons,” as Optimism did. Users, however, did not warm to the strategy.

The point is illustrated by some of the best-known L2s that came to market via retrodrops: Optimism, Arbitrum, Starknet and zkSync.

The key metric of community interest in an L2 is not active addresses but deposits into the network from Ethereum’s base chain. That is the chief indicator of liquidity for L2s because it is the only source of capital arriving as ETH.

Optimism

The chart below shows that the peak range of unique deposits coincided with the May 2022 airdrop—around 2,000 transactions a day. That level lasted only a year and began to stagnate in April 2023. Deposits now number only a few dozen a day.

Arbitrum

The ARB airdrop took place in March 2023, after which activity fell immediately from several thousand deposits a day to a few dozen. Although TVL for both networks (Optimism and Arbitrum) follows a different, more positive curve, that reflects “old money” cycling within the network rather than inflows from new, active users.

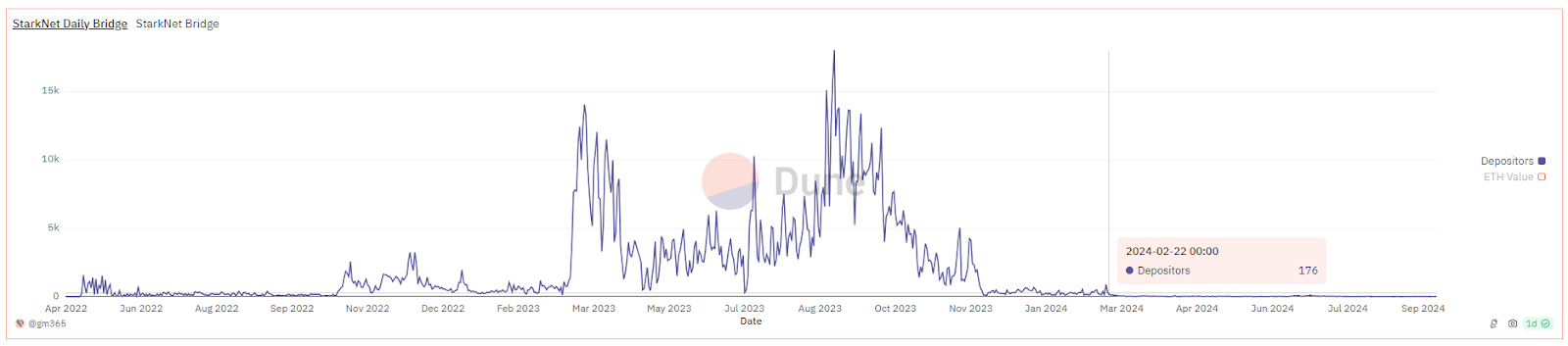

Starknet

Of the projects examined, Starknet behaved most intriguingly: it lost momentum even before its token giveaway. Peaks in the second half of 2023 faded long before the airdrop.

The number of new deposits fell from tens of thousands of transactions to mere dozens. And on 17 September 2024 it set an anti-record—one deposit in a day.

zkSync

As with Starknet, zkSync shed new users even before its June 2024 drop. By mid-September there were days when nobody wanted to bring money into the network at all.

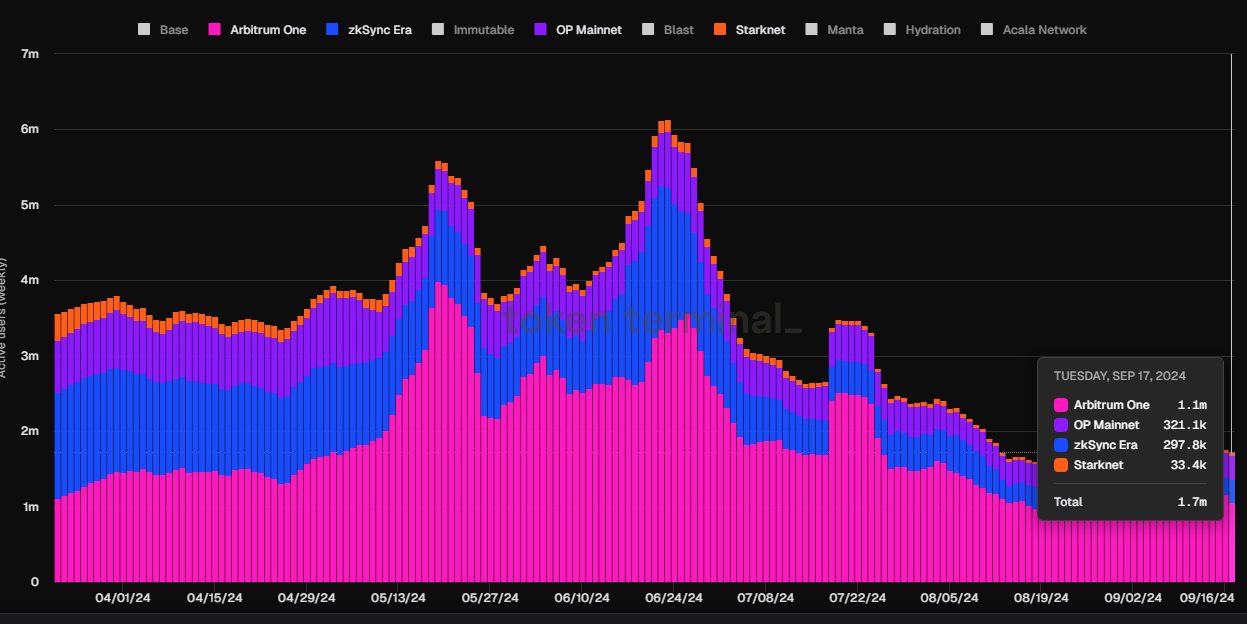

Stats and takeaways

According to Token Terminal, the total number of weekly active addresses by mid-September stood at 1.7m.

Such activity, alongside near-zero inflows of fresh liquidity into L2s, may signal a crisis in the segment—both technological and psychological. While some incumbents still “work” on-chain, newcomers are simply not interested.

If the trend continues, the view of CryptoQuant CEO Ki Young Ju about the market’s “dopamine” character will be vindicated. He argues that digital assets constantly need new narratives to keep participants excited, as older ones are dulled by the influx of more conservative players and regulatory actions.

If Fidelity’s forecasts come true, L2s will be left with few advantages or user incentives, and high competition will dilute already thin liquidity—most of which has been captured by older projects such as Arbitrum and Optimism.

Who needs zkSync with $500m in venture funding when Binance can list the NEIRO memecoin with a $16m capitalization and lift it to $500m in two days instead of several years of hard engineering?