Traditional financial institutions have long and successfully invested in the crypto market. Despite foundational ideological contradictions, banks have done much to foster the digital economy and, lately, have publicly put resources into decentralised projects, individual coins and trading instruments.

ForkLog recalls how classical financial institutions not only helped to shape the crypto market but also infected it with some of their chronic ailments.

JPMorgan — in Ethereum’s shadow

“Even before the very first block of ether was mined and ConsenSys was created, we collaborated with JPMorgan on concepts and production systems,” said Ethereum co-founder Joseph Lubin in August 2020.

The ETH genesis block was mined in late July 2015. Accordingly, JPMorgan — one of the world’s largest banks — has been involved in developing the market far longer than it might seem at first glance.

ConsenSys stands behind the MetaMask wallet and ETH infrastructure provider Infura, whose nodes handled more than 50% of Ethereum transactions in 2022.

It then emerged that, since 2020, ConsenSys has belonged to JPMorgan. This became known from a lawsuit filed by shareholders: they believed that the flagship company — the developer of the Ethereum blockchain — had been unfairly transferred into the bank’s hands.

Against this backdrop, the words of JPMorgan CEO Jamie Dimon sound especially striking: he called bitcoin “a public decentralised Ponzi scheme”. At the same time, he acknowledged the practical utility of blockchain for efficient transactions and data transfer, expressing optimism about Ethereum.

Today, the outspoken critic of digital gold profits not only from ETH but also processes buy-and-sell orders for BlackRock and Valkyrie within their spot bitcoin ETFs. JPMorgan, alongside Jane Street, became an authorised participant supplying BTC to these funds. This means the bank buys and sells the bitcoin that backs the ETFs’ shares.

Where else have banks reached?

The Ethereum blockchain is the largest and most vivid example of how long financial institutions have been involved in building the crypto industry. If JPMorgan has largely operated in the shadows, bankers at Goldman Sachs came in through the front door, investing in USDC stablecoin issuer Circle.

The start-up launched its coin in 2018. Today USDC is the second-largest stablecoin by market capitalisation after Tether’s USDT. In April 2024 it even overtook its rival by monthly transactions: 166.6 million in USDC versus 163.6 million in USDT.

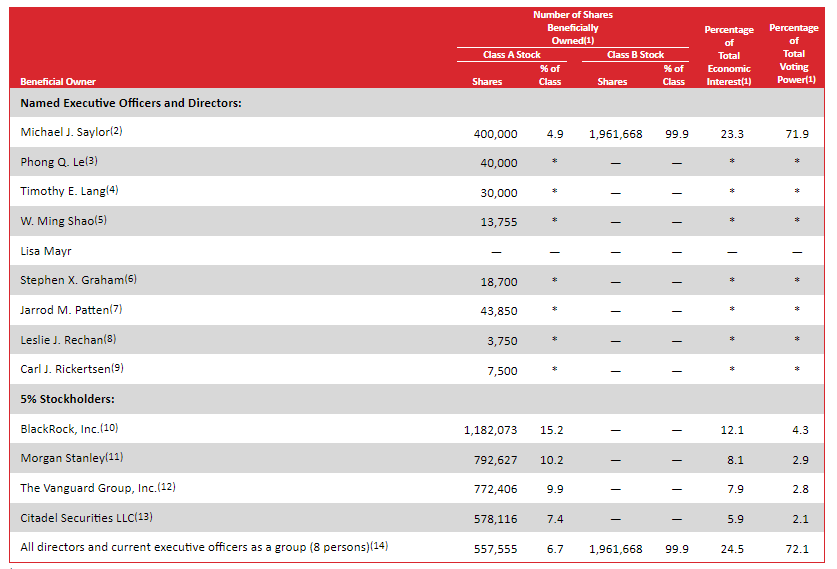

Bitcoin was no exception. One of the first companies to publicly announce purchases of digital gold for its balance sheet was Michael Saylor’s MicroStrategy. According to filings at the start of 2021, the biggest shareholders of the most publicised bitcoin HODLer were BlackRock, Morgan Stanley, The Vanguard Group and Citadel Securities.

Without these shareholders’ consent, Saylor could not have instituted a policy of BTC purchases. The implication is that these institutions knew what was happening and approved the company’s approach to spending its money.

A few years ago, such strategies seemed exceptional. In effect, it is banks and financial institutions like BlackRock that created the conditions and set the fashion for investing in cryptocurrencies.

They now hold sway over infrastructure that handles a substantial share of processing in the crypto market.

A baleful influence

The embrace of technology by traditional financial institutions also brought speculative schemes and higher-risk strategies. In 2022 we were reminded of the dangers inherent in a banking system based on loans and collateral — and saw the chief drawbacks of centralising liquidity flows.

The collapse of America’s Silvergate Bank has become a textbook case. Since 2016 the bank had offered services tied to cryptocurrencies, and its CEO Alan Lane personally invested in digital gold back in 2013.

The institution set the trend for lending against bitcoin collateral. In 2022, for example, mining firm Marathon Digital Holdings secured a $100m credit line on that basis. Even MacroStrategy (a MicroStrategy subsidiary) raised $205m against bitcoin collateral.

According to Forbes, by the end of 2022 Silvergate counted around 900 institutional crypto clients and 94 exchanges. The organisation tried to issue its own stablecoin, buying from Meta the development work behind the Diem payments network. The product later underpinned the Aptos blockchain, while regulators blocked the coin’s issuance.

Silvergate’s bankruptcy stemmed from a confluence of adverse factors. As the Fed raised rates, clients began withdrawing deposits in search of higher yields. That forced the bank to sell government bonds at a loss. It then emerged that Silvergate was a creditor to the FTX exchange, which held about $1bn on its accounts.

All this damaged the bank’s reputation and finances, and several crypto platforms began to cut ties. Coinbase, for instance, refused its services due to concerns about its solvency.

The fallout soon reached Silicon Valley Bank (SVB) and Signature Bank (SBNY), bringing not only uncertainty and disruption to liquidity flows, but also a temporary USDC depeg. It turned out that $3.3bn of USDC reserves were held at SVB.

The situation normalised after regulators activated the BTFP facility. Ironically, the crypto market was helped by the Fed rescuing banks — and, by extension, their clients. Otherwise we might have seen even more bankruptcies and deeper consequences than in the cases of FTX and Terra (Luna).

Prospects and consequences

On the one hand, banks are helping companies develop fintech based on blockchain and cryptocurrencies. Their attention benefits young start-ups and mining firms that, in various ways, enhance bitcoin’s security.

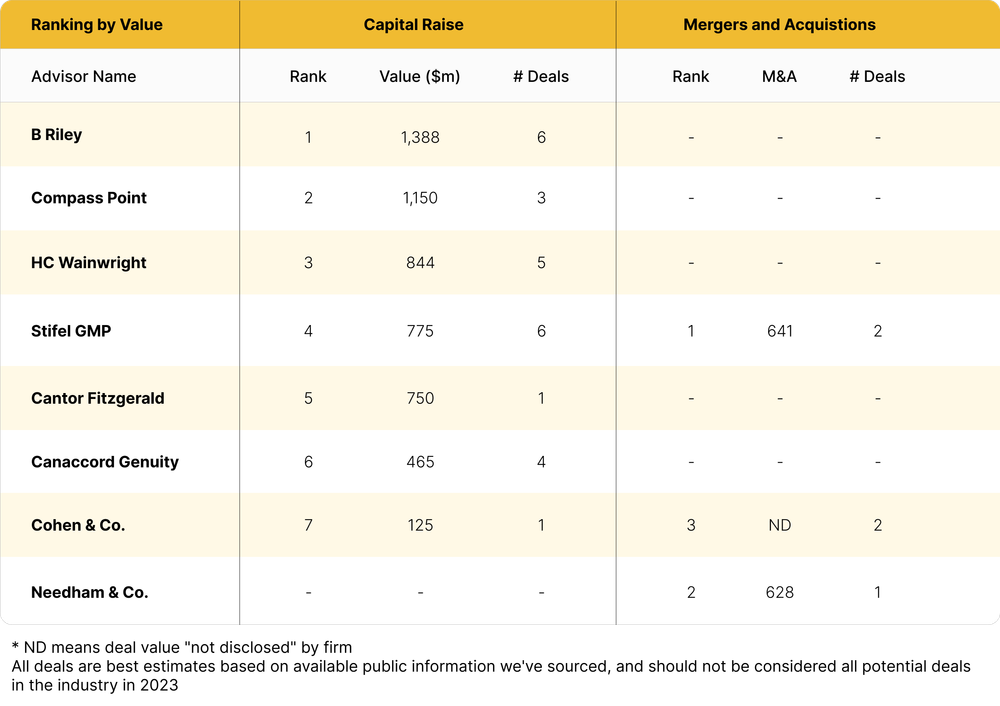

Analytics platform Hashrate Index noted the positive impact of bankers on the sector. Aggregate capital raised by the industry in 2023 amounted to about $5.5bn.

The evolution of the crypto market is influencing traditional financial mechanisms. In late 2023, for instance, payments giant Visa disclosed that it had recognised the potential of stablecoins and already uses digital currencies in fiat settlements.

On the other hand, the old financial system’s problems are “quietly” spreading into crypto. The arrival of banks and other institutions has brought the same unsecured debts and intermediated ownership.

The principle laid down by Satoshi Nakamoto — “Not your keys — not your coins” — is attracting fewer new users, whose attention is fixed on trends such as meme tokens and so‑called “tapalki” in Telegram bots. Despite significant shifts in institutional adoption, none of this solves the problems of existing currencies and the monetary policies of most countries’ central banks.

A deeper symbiosis between fiat and crypto makes the latter vulnerable to the same crises afflicting the modern economy. A hard-edged approach to controlling user transactions is also evident, which could lead to negative and even repressive outcomes given the nature of blockchain technology.

One example is the recent partnership between Tether and Chainalysis — in April 2024 they began building a system to track activity on the secondary market. Although the initiative aims to combat fraud and crime, it implies deeper monitoring of ordinary users’ transactions.

Text: Oleg Cash Coin