US sanctions against Tornado Cash have had a significant impact on the crypto community, exposing the fragility of the DeFi ecosystem.

Soon after the mixer‑linked addresses were blocked, MakerDAO founder Rune Christensen proposed a radical idea — to make the DAI stablecoin freely floating, unpegged from the US dollar. In his view, this is the only viable solution, as the project cannot fully comply with regulatory requirements.

Christensen’s proposal drew sharp criticism and surprised many in the crypto community. Many viewed his plan not only as utopian but also potentially damaging for the project, the DeFi ecosystem and the wider industry.

ForkLog examined the features of the founder’s controversial idea, highlighted the main opposing forces within the project and weighed the potential risks associated with the “depegging” of one of the largest stablecoins.

- The MakerDAO founder Rune Christensen regards sanctions against Tornado Cash as extremely serious — a risk faced by his project and the DeFi sector as a whole.

- Most market participants see stablecoins as a means of preserving value and a “safe harbour” in conditions of global uncertainty.

- The DeFi segment is often described as “financial LEGO,” because applications are highly interconnected. Therefore a potential collapse of the high‑capitalized DAI poses a threat to the ecosystem and the crypto industry as a whole.

MakerDAO and the DAI stablecoin: features

To understand the core of the problem, one should recall the main features of how the service operates. It is also important to understand the stability mechanism of DAI — the first decentralised stablecoin and a key element of the ecosystem.

MakerDAO is a smart‑contract platform on Ethereum that allows issuing a dollar‑pegged DAI backed by crypto assets.

The stablecoin is backed by Ether and various digital tokens. The emission scheme can be likened to the issue of money backed by gold. The difference is that instead of a noble metal, crypto assets are used: a user deposits some amount of ETH or other tokens into a smart contract, which then issues the token. The system is called Vaults.

An important feature of the system — requirements for “over‑collateralisation” to issue the stablecoin. For example, a Vault with a liquidation ratio of 150% would require at least $1.50 of collateral value for every $1 created DAI.

If the collateral value falls to $1.49, it is liquidated to cover the generated DAI. In addition, a so‑called liquidation penalty is applied.

DAI tokens effectively represent a debt backed by collateral. The collateral always exceeds the loan size.

If the collateral value drops below a certain amount relative to the loan, an auction begins during which network participants, called liquidators, buy the collateral for DAI. The system then burns the acquired stablecoins, reducing the supply. This mechanism is designed to maintain the dollar peg.

The Maker Foundation was founded by Danish Rune Christensen in 2014. The following year he, together with other developers, began work on a decentralised platform that would allow borrowing against crypto collateral in the form of stablecoins.

In the first iteration, the central element was Single Collateral Dai (SCD, “monozalogovy Dai”), issued in December 2017. The only asset used as collateral for loans was Ethereum.

Subsequently, the project’s creators moved to the Multi Collateral DAI (MCD) concept with a multi‑collateral DAI token. The new version of the stablecoin began operation in November 2019.

The first additional collateral option was Basic Attention Token (BAT). The old version of the stablecoin was renamed Sai.

On 12 March 2020, amid a collapse in Ethereum prices, attackers drained over $8 million from MakerDAO. One of the main reasons for the incident was the weaknesses of the Auction Keeper system. The episode spurred the community to accelerate the full transition to MCD.

On 3 May 2020, MKR holders approved the use of tokenised Bitcoin Wrapped Bitcoin (WBTC) and tBTC as collateral.

Thanks to the transition from SAI to DAI, it became possible to issue the stablecoin not only against Ethereum but also against ERC20 tokens: WBTC, tBTC, BAT, LINK, LRC, COMP and centralised stablecoins Pax Dollar (USDP) and USD Coin (USDC). The share of the latter in collateral has grown significantly over time.

In addition to the DAI stablecoin, the platform uses Maker (MKR) — the governance token of the Maker Protocol.

When the system’s liquidation reserve exceeds the minimum threshold, MKR is taken out of circulation. The tokens are also burnt when surpluses of DAI are sold at auction. Conversely, when the Maker Protocol has a deficit and the system’s debt exceeds the maximum threshold, MKR tokens are created and sold at auction to recapitalise the system.

The main responsibility of MKR holders is to ensure the stability of DAI’s price and the health of the system as a whole.

Additionally, MKR serves a governance function — the token is used in votes on risk‑management mechanisms and changes to the platform’s business logic. Native token holders are the ultimate authority in MakerDAO. They govern the system and participate in profit distribution, although they must bear losses if decisions prove unsuccessful.

In the winter of 2021 the Peg Stability Module (PSM) began operation.

«Peg Stability Module gives users the ability to exchange a certain type of collateral directly for DAI at a fixed rate instead of borrowing the stablecoin», — according to the description on the project’s community site.

Among the other features of PSM are a zero Stability Fee and a 100% Liquidation Ratio for Vaults.

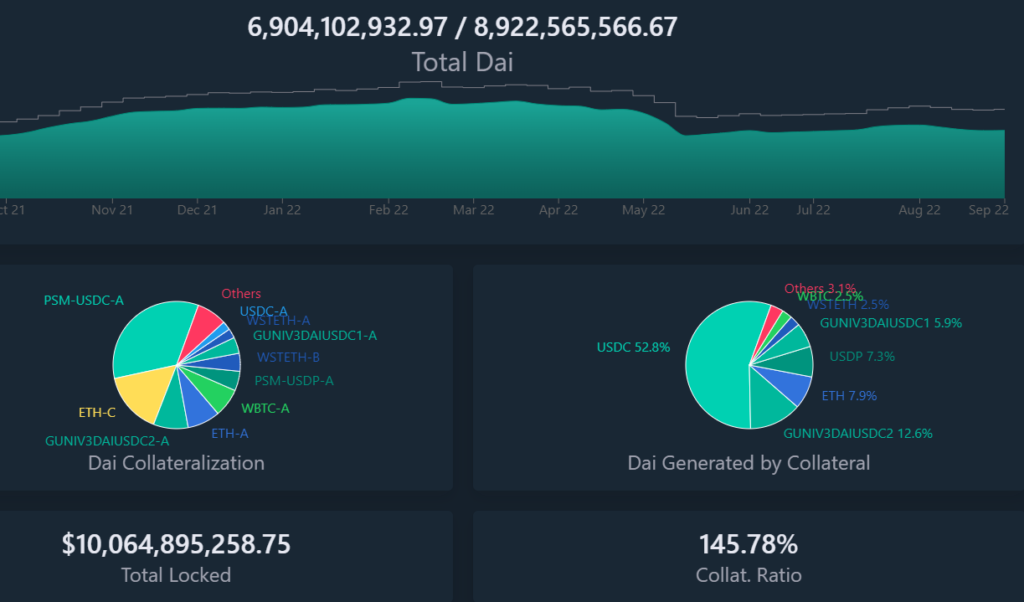

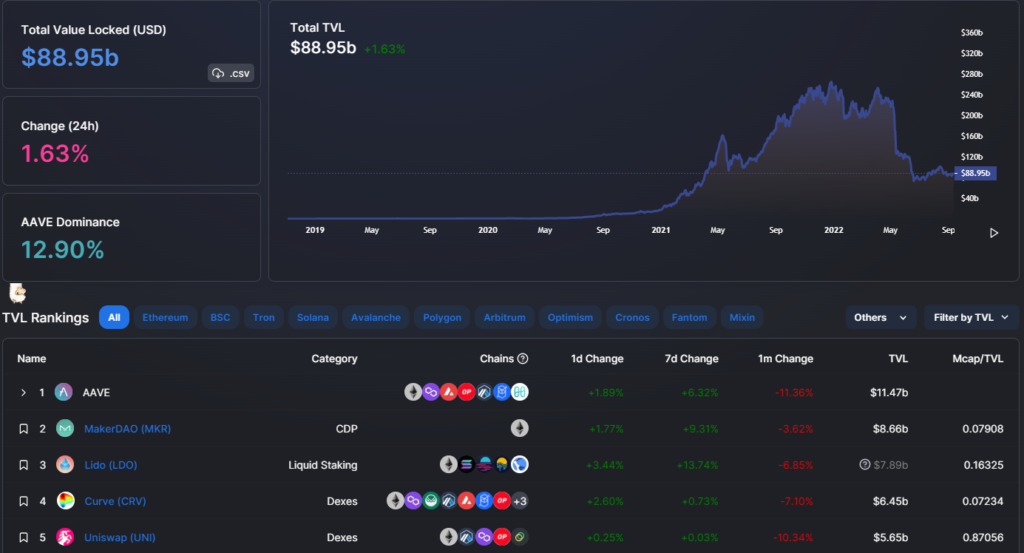

MakerDAO remains one of the first DeFi apps to gain broad adoption. The platform remains among the largest in the Ethereum sector with a TVL of $8.6 billion (as of 11.09.2022).

MakerDAO’s success is largely conditioned by the stability of DAI. The chart below shows that even amid the highly volatile March 2020 period, the token deviated from its $1 target by only a few cents.

As of 12.09.2022, DAI’s market capitalisation stands at around $6.4 billion. The asset ranks 4th in CoinGecko’s stablecoins category, behind USDT, USDC and BUSD.

Christensen’s concerns

At the start of August the US Treasury added Tornado Cash to the sanctions list, along with 39 Ethereum addresses and 6 USDC addresses linked to it.

The agency suspects the platform of laundering around $7 billion since 2017, of which more than $455 million was linked to North Korean hackers.

This event sparked a significant reaction in the crypto community. In response to Tornado Cash, the MakerDAO team began developing a contingency plan in case the protocol’s core smart contracts fall under regulatory action. Mechanisms to reduce dependence on USDC are also being considered by other DeFi projects.

Rune Christensen soon after the Tornado Cash incident stated that he intends to shed $3.5 billion worth of USDC from DAI collateral — presumably to minimise regulatory risk.

According to yEarn Finance developer going by the handle banteg, the founder’s idea envisions buying ETH “on the market” by converting all USDC from the PSM module. As noted, Circle’s USDC accounts for a large share of DAI collateral.

Vitalik Buterin called the MakerDAO plan a terrible idea.

Errr this seems like a risky and terrible idea. If ETH drops a lot, value of collateral would go way down but CDPs would not get liquidated, so the whole system would risk becoming a fractional reserve.

— vitalik.eth (@VitalikButerin) August 11, 2022

«If Ethereum falls in price, collateral value plummets, but CDPs are not liquidated. The whole system could become a fractional reserve» — Ethereum cofounder commented.

And Rune might want to «yolo» the PSM $USDC into $ETH lmaooo pic.twitter.com/tVugbNlyaj

— Westie 🟪 (@WestieCapital) August 11, 2022

Christensen wrote in the MakerDAO Discord that the sanctions are far more serious than he could have anticipated. He also voiced the idea of decoupling DAI from the dollar as a viable path.

According to him, converting the collateral USDC into ETH is seen as an “obvious suicide.” On the other hand, “the risk‑and‑reward balance of partial de‑coupling of USDC may prove acceptable.” Along with Buterin, many other community members criticised Christensen’s proposal as radical. Some even compared the potentially “depegged” DAI with Terra’s failed algorithmic stablecoin UST.

Terrable idea, agree pic.twitter.com/BQUYvMnBh1

— Raja (@RajaZuberi) August 11, 2022

Crypto‑industry researcher Mika Honkasalo, in discussion with Blockworks, noted that regulatory risk is not limited to MakerDAO. In his view, potential sanctions threaten any other DeFi protocol using USDC as collateral.

«What if a smart contract for an automated market maker using USDC, which is effectively a market, ends up on the sanction list?» — Honkasalo asked.

In a post on the MakerDAO forum, Rune Christensen expressed the view that a freely floating DAI is the only path to decentralisation and regulatory compliance.

«The coercive repression of the crypto industry can occur without notice and without the possibility of restoration even for law‑abiding, innocent users» — he emphasised.

Maker cannot create a blacklist, therefore the platform cannot comply with the regulations, Christensen argued.

«The only choice is to limit the attack surface by reducing Real World Asset (RWA) exposure to a minimal fixed percentage of total collateral. This requires freeing it from USD», — shared the MakerDAO founder.

In his view, two main tools will support the operation of the new system: MetaDAO and Protocol Owned Vault.

Yield farming DAI via MetaDAO will enable users to adopt the coin’s floating-to-dollar rate. The tokens earned will incentivise the supply of the stablecoin through decentralised collateral, Christensen suggested.

The Protocol Owned Vault storage will allow the platform to earn income from negative target rates on DAI and set their cap.

Subsequently, the MakerDAO founder published a post with a timeline and more detailed description of the plan to decouple DAI from the dollar.

Key points:

- DAI will remain pegged to the dollar at a 1:1 ratio for at least three years;

- The transition of the stablecoin to a freely floating rate will be postponed in the absence of an “immediate authoritarian threat”;

- The 1:1 peg to the dollar will remain indefinitely if decentralised collateral in the protocol reaches 75% and stays at that level;

- During the first three years the protocol will effectively double the RWA volume to accumulate as much Ethereum as possible and increase the share of decentralised collateral.

3/ He highlights three different “stances” of collateral backing, each at a different point in this timeline and contingent upon the threat of an authoritarian attack. pic.twitter.com/UP25i1O3PX

— Westie 🟪 (@WestieCapital) August 31, 2022

Christensen highlighted three situational approaches for implementing the plan:

- “Dove” — maximum but unstable growth. Unlimited use of RWA; all income used to buy Ethereum;

- “Eagle” — balance of growth and stability. RWA limited to 25%. “Most likely” freely floating DAI;

- “Phoenix” — maximum stability at the expense of growth. RWA volumes are small. Freely floating DAI is highly likely.

Notably, MakerDAO had previously actively partnered with traditional financial institutions. For example, in July the Maker DeFi community approved the creation of a vault with a limit of 100 million DAI for the Huntingdon Valley Bank (HVB), an American bank founded in 1891.

Greg Di Prisco, former head of business development at the Maker Foundation, said the HVB deal was the culmination of roughly six months of work with various Core Units and stakeholders, not to mention the real‑world service providers required to complete the transaction flow.

The HVB deal was the culmination of approximately 6 months of work with various Core Units and stakeholders, not to mention the various real‑world service providers required to complete the transaction flow. (7/38)

— Greg Di Prisco | gdip.eth (@g_dip) August 30, 2022

In early September, the cryptocurrency exchange Coinbase put a MakerDAO proposal to a community vote, shifting a third of the $1.6 billion USDC from the PSM module to Coinbase Prime at up to 1.5% annual yield.

If approved, MakerDAO could earn about $24 million annually under the institutional investors program.

Coinbase is a partner of Circle in the Centre consortium, which issues USDC.

Intra‑community tensions

Di Prisco says the MakerDAO community is not homogeneous — it can be categorised into several rival groups:

- Futurists. Christensen is among them, as are supporters of his radical plans;

- Centralists. Venture investors who hope to expand the protocol’s lending capacity. In their view, this will make the DAO profitable;

- Decentralists — seek “zero dependence” on centralised assets.

Di Prisco emphasised that there are other political ideologies too. Yet the balance of power among the three groups above “determines the fate of the protocol.”

When the bull market was raging, all of these underlying ideological differences were swept under the rug. Everyone was doing well. This worked until the market pulled back and the DAO started losing money. The mythical end of this era was the closing of the HVB deal. (20/38)

— Greg Di Prisco | gdip.eth (@g_dip) August 30, 2022

«When the bull market raged, all these fundamental ideological differences were swept under the rug. Everyone was doing well. This worked until the market corrected and the DAO started losing money. The mythical end of that era was the HVB deal’s closure,» explained the expert.

DeFi commentator rekt wrote that during the bull cycle, growth was the priority for any protocol. Fresh fiat poured into the ecosystem, and regulatory threats were often ignored.

He added that after the UST and Terra collapse, price stability became the main priority for stablecoin issuers. USDC and USDT became a “safe harbour” for investors during market downturns.

«DAI remained strong despite the chaos», — noted rekt.

According to Di Prisco, Christensen’s MetaDAO plans are supported by the futurists and decentralists. Centralists, however, “insist the radical plans are impractical. They believe a dollar‑decoupled DAI would become useless.”

A MakerDAO community member known as monet-supply wrote the following:

«Why would an authoritarian government ban fiat‑pegged stablecoins, but allow the use of floating stablecoins (or even volatile underlying crypto assets) if they still undermine state control over the monetary system?»

The idea that Maker has no choice but to prepare for a freely floating DAI clashes with the recent proposal to deposit USDC from the PSM to Coinbase Prime to earn interest.

«This plan implies that a substantial portion of the platform’s collateral could be frozen if the government takes control of Coinbase and USDC», — noted rekt.

In his view, a leading US crypto exchange, such as Coinbase, and similar to Circle, could take this step at any time.

Not a novel concept

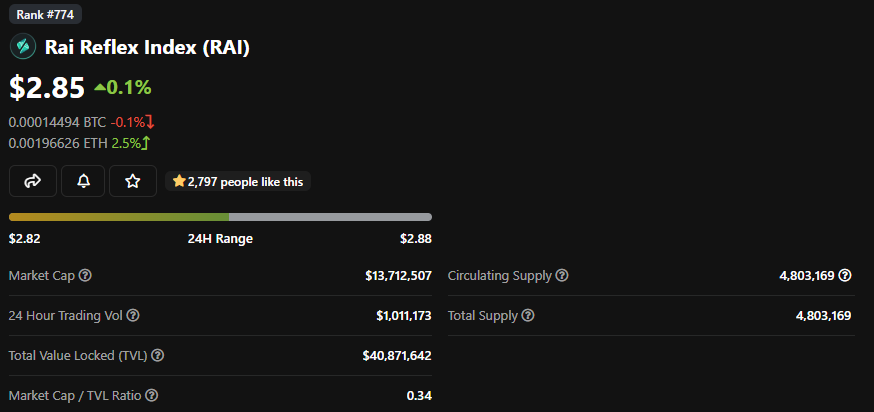

One of rekt’s anonymous authors wrote that the “unpegged” DAI conceptually resembles Reflexer Labs’ low‑volatility token, RAI, launched in 2021.

«An asset focused on unpegged stability, backed only by ETH and with minimal governance, attracted the attention of ardent decentralisation supporters», — noted the expert.

However, after recent market declines and fears of sanctions, the “unpegged stability” model has not gained traction. Most users still feel most comfortable with dollar‑based assets, noted rekt.

As of 16.09.2022, the RAI token ranks 774th in CoinGecko’s market cap ranking. Its market value is only $13.7 million, and its 24‑hour trading volume is $1 million.

In May 2022, Ethereum founder Vitalik Buterin labelled RAI as relatively stable algorithmic stablecoins.

«The security of RAI depends on an external asset (ETH) backing the system. Therefore RAI is much easier to unwind safely», — he noted.

Buterin stressed that in Reflexer Labs’ instrument one can implement a negative interest rate. For example, such an option did not exist in UST.

At the same time he added that implementing this condition does not make the asset “safe”:

«It can still be unstable for other reasons (e.g., insufficient collateral ratio), have bugs or governance‑mechanism vulnerabilities».

The rekt columnist conceded that holders of high‑capitalisation DAI may not soon get used to a “new definition of stability.”

«Time will be required, and perhaps some unwanted volatility, before users of DAI get used to operating in a fully alternative economy», — the expert shared.

Do or DAI

Because the DeFi ecosystem is highly interconnected, a sudden transition of DAI to a floating rate could trigger systemic risks across the board.

The author at rekt is convinced that every project will sooner or later have to address the challenges MakerDAO has faced.

«It is encouraging to see some of the most foundational DeFi protocols taking steps to address complex problems and negotiating how to continue existing in the face of existential threats», — the expert wrote.

In his view, Christensen’s controversial plan could form the basis of a new paradigm — “dollar immunity” that would render DeFi inaccessible to regulators and other opponents of the crypto industry.

The expert stressed that the MakerDAO founder risks destroying DAI by his own hands. On the other hand, given the real‑world situation with depreciating fiat currencies, the new concept represents a window of opportunity that is closing fast.

In his view, modern society is in a state of “irreversible, accelerating decline,” with factors including overproduction, overpopulation, climate change, peak oil, resource scarcity, post‑truth in the media, etc.

«The world is entering a new, more chaotic and unpredictable equilibrium in which anarchy, eco‑fascism, deglobalisation and human suffering on a massive scale prevail», — wrote the author.

He is convinced that “modern global capitalism” will barely cope with these challenges, and that politics will become more polarised and unstable over time.

«The true spirit of the cypherpunk could prove to be a lifeline as we move toward an increasingly unstable future», — the expert shared.

In conclusion, the author notes that competition in the sector is tightening as Aave and Curve prepare to launch their own stablecoins with surplus decentralised collateral.

Conclusions

The Tornado Cash sanctions shook the DeFi sector and the crypto industry as a whole. Many developers have recognised the fragility of their projects in the face of authoritarian threats.

Given the scale of MakerDAO and DAI, Christensen’s idea is radical but not novel. To date there are no highly capitalised projects using the concept of “unpegged stability.”

It is evident that most stablecoin holders have grown used to thinking in dollars. Moreover, many seek a “safe harbour” during market downturns and global uncertainty.

Participants of the community largely remain sceptical of Christensen’s proposal, deeming it radical, utopian and highly risky.

Because DeFi is highly interconnected, a potential collapse of DAI could threaten the ecosystem of decentralised applications and the crypto industry as a whole. The impact could be comparable to the consequences of the UST/Terra collapse, from which the market has yet to recover.

Read ForkLog’s Bitcoin news in our Telegram — crypto news, prices and analysis.