For ForkLog, DappRadar analyst Ilya Abugov outlined the most significant events in the decentralized applications sector over the past month.

July was a banner month for DeFi. With the emergence of governance tokens and liquidity mining, the sector demonstrated impressive momentum both in transaction activity and in asset capitalization, which in turn benefited other sectors, including gaming.

The bulk of activity was concentrated on Ethereum, but the ecosystem’s development has already run into network-operational constraints. Against this backdrop, Tron and EOS sought to close the gap with the leading competitor.

Regulators watched closely but have so far refrained from active intervention.

The governance-token boom

Compound saw rapid growth after the release of COMP. Others including Curve and Balancer sought to replicate this success. In July, they were joined by bZx, Akropolis and yEarn.finance.

The core idea of governance mechanisms remained the same: rewards for providing liquidity. The governance token also allows holders to vote on changes to the protocol.

The idea of a DAO inspired projects that already had native tokens: Kyber Network, Aave, and Synthetix. For some this is an additional way to increase liquidity, for others a way to reduce regulatory risk.

Decentralised exchanges — the backbone of the ecosystem

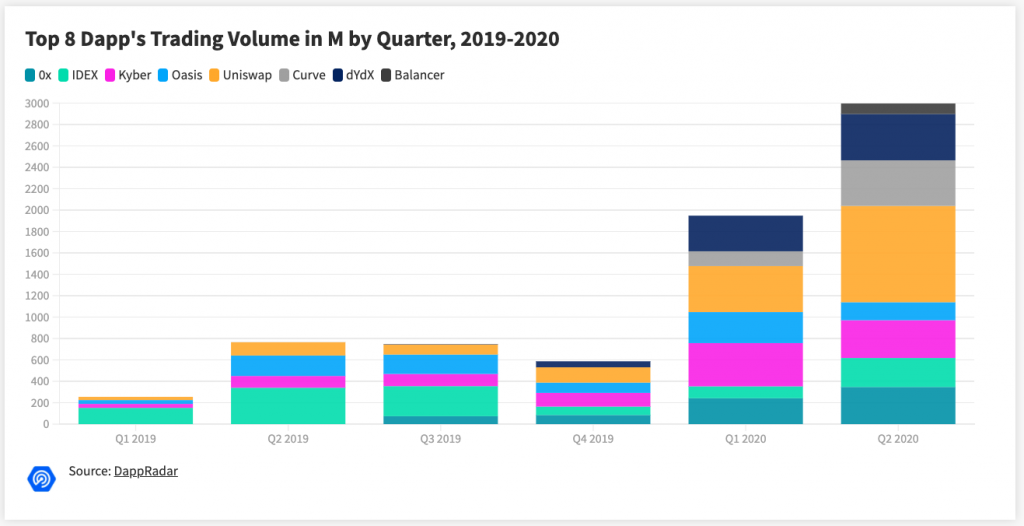

The economy of tokenised assets requires liquid markets to sustain a free flow of capital. As interest in DeFi rises, activity on major decentralized exchanges (DEX) has noticeably grown.

According to the quarterly DappRadar report, the top eight surpassed 5,000 active addresses per day and reached $3 billion in turnover.

Source: DappRadar.com

Uniswap unsurprisingly turned out to be in the lead. Strong positions for Balancer were established quickly. This protocol is used in many algorithmic yield-farming loops. The same applies to Curve. It can be assumed that upcoming DeFi projects will seek not merely to launch a liquidity-mining analogue but to integrate more fully into existing applications.

https://forklog.com/chto-takoe-dohodnoe-fermerstvo-v-defi-i-kak-na-nem-zarabatyvayut/

Problems in governance-token distribution

The initial version of the COMP distribution model rewarded higher yields, meaning higher asset yields yielded a larger share of COMP. In this way yield farmers could earn not only from deposits but also from borrowings. When COMP prices were high, the high borrowing costs could become expensive.

While this applied to DAI and USDC, the risks were theoretically manageable; the situation became perilous when the queue reached the volatile BAT. The response to this challenge was a change in the distribution model — rewards tied to the amount of capital in the system. The environment around Compound stabilised, but there may be risks for MakerDAO in relation to changes in demand for Dai.

The sector shows growing algorithmic vulnerabilities, where the flaws lie less in code and more in logical design. A telling example was the Balancer incident: the attacker did not break the system, but exploited its logical imperfections to drain capital.

The same logical flaws extend to bots. While governance-token distributions are meant to support users, the greatest gains often accrue to a limited number of participants. An example is the bZx IDO, where bots probably played a significant role.

Given the rise of IDOs, this dynamic poses serious risks and calls into question the decentralisation of ecosystems.

What governance tokens really are

Governance tokens are not tied to any capital flows, and their price may appear to arise purely from hype and speculation.

On the other hand, a format that assesses these tokens as equities is gaining traction. Given that a token grants a vote and effectively control over a project’s development, it can be viewed as a non-dividend stock. Likely, in the future holders will be able to vote for a distribution of fee streams or for token burning.

Some projects have already begun applying traditional investment metrics, such as P/E (price-to-earnings), to compare and assess crypto assets. This approach is evident in Token Terminal and Bankless.

While such an interpretation may be of interest to traditional investors, it comes with regulatory risks.

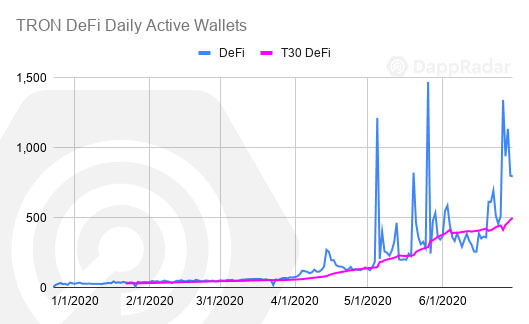

Competitors again seek to catch up with Ethereum

Liquidity mining has notably boosted activity on the Ethereum network, once again exposing the bottleneck in capacity. Competitors sought to seize the moment.

Tron has significantly expanded its DeFi segment. JUST, Zethyr Finance and Oikos.cash have gained traction, and the launch of Tron 4.0 has generated additional excitement around the ecosystem. Tron also announced the launch of its own Uniswap-style platform and showed interest in yield farming.

Source: DappRadar.com

EOS has not seen DeFi activity on the same scale, though similar projects are developing on its platform. Beta testing of Eosfinex points to potential further growth for the platform in this space.

Against the backdrop of Ethereum 2.0 expectations, new infrastructure projects have gained momentum. Notable announcements and launches include: the launch of Shelley at Cardano, SKALE Network and Avalanche.

The BSN — China’s State Information Center infrastructure blockchain platform — has connected with six public networks. While Ethereum is one of them, BSN itself and the other integrated networks could become serious competitors to Ethereum.

Launch of the final Ethereum testnet adds a degree of optimism.

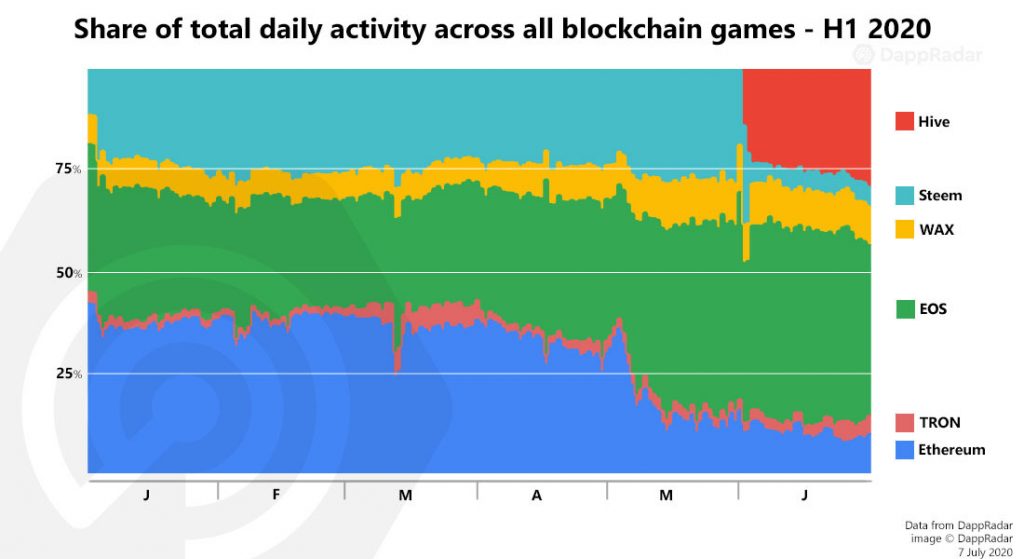

Games cast a gaze at DeFi

One of the industry’s main challenges remains a relatively small user base. The DeFi sector has demonstrated how economic incentives can improve the situation. The gaming industry is beginning to follow suit.

The main streams in this direction are play-to-earn and asset fragmentation. The idea is that in the game, users earn assets that can be sold later.

Axie Infinity has taken centre stage. With Small Love Potion (SLP) having a liquidity pool on Uniswap, players can monetise their playing time. As SLP’s price rises, the topic becomes even more pertinent.

Moreover, Axie Infinity announced the introduction of gold-backed tokens as one of the in-game rewards. Now others are turning to the play-to-earn model. For example, Dissolution will try to implement it.

Axie Infinity has also taken on a central role in asset fragmentation. Niftex allows users to buy slices of rare game heroes. The phenomenon began to gain traction, but Niftex disclosed a vulnerability, and activity was paused for a time.

Non-fungible tokens (NFTs) are attracting increasing attention in general. Notable companies and franchises are turning to NFTs to create digital assets. WAX has given a significant boost to development. Ethereum also remains active. For instance, Dapper Labs announced the launch of licensed Dr. Seuss collectibles.

For Ethereum gaming, summer has proven challenging. As noted in the BGA report for H1 2020, the Ethereum ecosystem faced serious issues due to rising gas costs. Some projects are likely to focus more on layer-2 solutions, as Neon District did with Matic Network. Overall, the main hopes rest on Ethereum 2.0.

Source: DappRadar.com

Some projects have also begun experimenting with governance tokens. Here, the RARI token deserves attention. Implementing this concept could attract additional interest to gaming ecosystems.

How regulators will act

Regulatory intervention in the DeFi ecosystem is not much discussed today, but ignoring the sector’s vulnerabilities in this respect would be a mistake.

Perhaps with sufficient decentralisation, projects could mitigate risks, but at present most projects remain centralised.

It is hard to judge how much Coinbase listing affected COMP’s popularity. Regulators thus have plenty of potential levers of influence.

As the TON case showed, US regulators can influence projects beyond the United States. The recent penalty for Abra also prompts caution.

On the other hand, the stance of SEC commissioner Hester Peirce suggests regulators are not necessarily bent on tight control of the industry. It is possible that in the current climate the growing segment will be allowed to develop.

If we see a repetition of an ICO-style speculative bubble, regulators will have more grounds for intervention.

Subscribe to ForkLog news on Telegram: ForkLog Feed — full news feed, ForkLog — the most important news and polls.