In crypto circles, digital assets are often cast as a lifeline for people in developing economies. At first glance, that looks like a victory for financial freedom. On closer inspection, however, the euphoria around bitcoin tends to obscure inconvenient truths.

ForkLog examines whether cryptocurrencies can truly deliver economic independence—or whether they amount to a new form of digital colonialism.

What is the problem?

The popularity of cryptocurrencies in developing countries stems from economic instability, high inflation and limited access to banking. People turn to digital assets as a store of value and for everyday or cross-border transactions. The appeal lies in relatively easy account opening, lower fees than in traditional finance and fast transfers.

That freedom has a flip side. In a new monthly digest, the ForkLog editorial team highlighted a problem that grows with each adoption cycle: in pursuit of the mass user, the industry is drifting from its core principle—decentralisation. Many products and parts of the infrastructure are becoming more centralised, enabling large market players not only to regulate access to services but also to change the rules of the game.

For developing countries this raises the risk of a digital-colonialism trap, where reliance on external solutions and the inability to build domestic infrastructure threaten a new form of dependence.

Digital colonialism manifests as dependence on global financial institutions, international organisations and centralised platforms, where decisions about access, pricing and the rules of the game are made by large corporations. As a result, states and users lose sovereignty over their data, financial flows and digital economies.

Independence within others’ rules

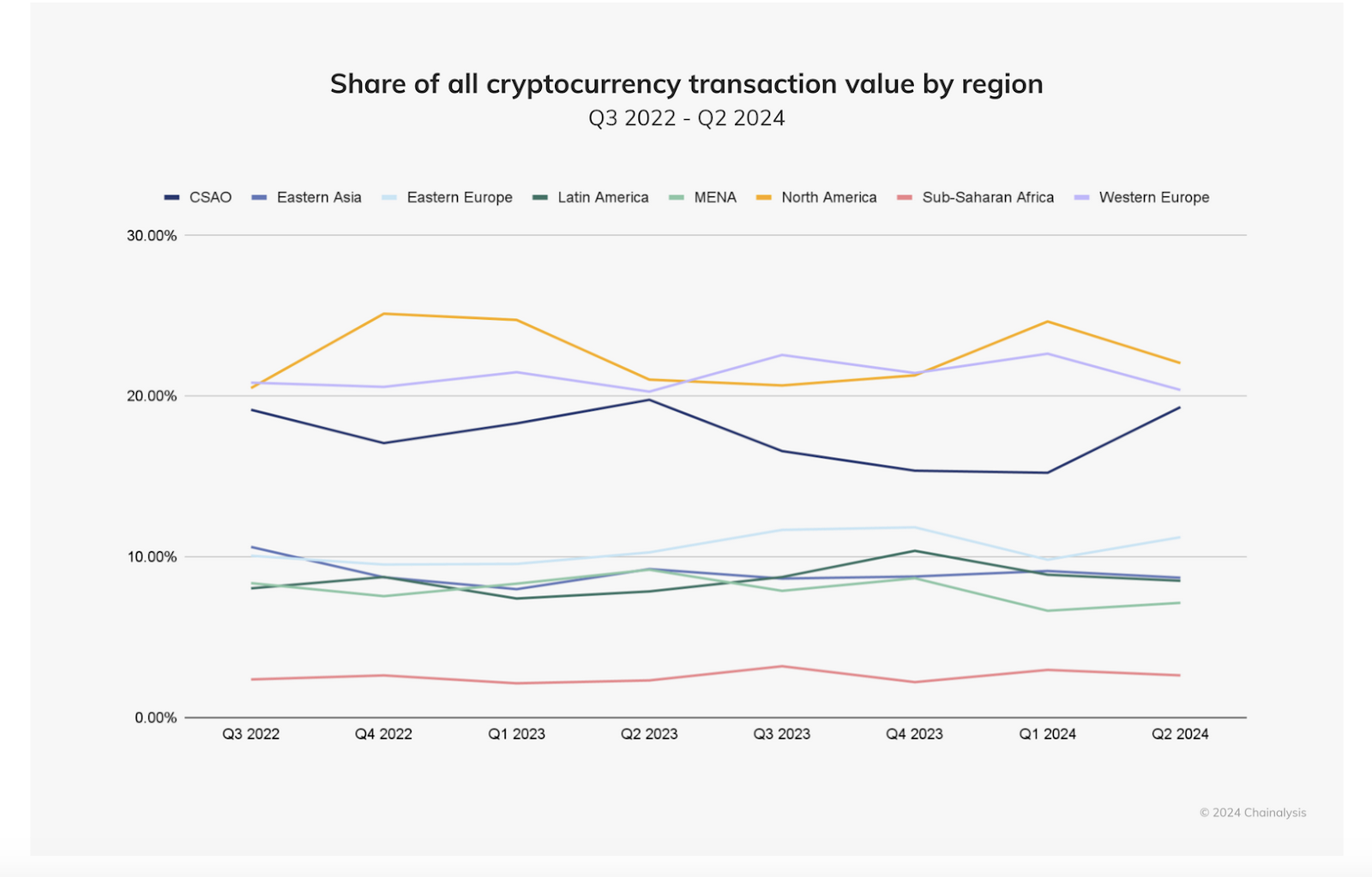

Latin America is among the regions where cryptocurrencies have spread widely: it accounts for 9.1% of the total value received in crypto, according to Chainalysis.

The most conspicuous example of bitcoin at the state level—and of dependence on a financial organisation representing rich countries—is El Salvador. In 2021 the government made bitcoin legal tender, a move the IMF did not appreciate (IMF). As leverage, the organisation used money—the country needed a loan to address liquidity problems and repay sovereign bonds.

In the end, El Salvador agreed to revisit its bitcoin strategy in exchange for $1.4bn in financing. Including regional programmes, the package exceeds $3.5bn.

A similar problem confronted the authorities of the Central African Republic (CAR). They legalised bitcoin in April 2022, prompting an almost immediate response from the IMF. Representatives warned of possible problems for the country and the region as a whole. Later they even suggested that all African countries tighten oversight of digital assets. A year later, the CAR abandoned bitcoin.

Pressure on developing countries is not exerted by the IMF alone. In March 2024 Vietnam’s finance ministry raised the prospect of prohibiting or regulating digital assets by May the following year as part of efforts to step up anti-money-laundering measures. The plan aims to remove the country from the FATF grey list.

Yet the threat does not come only from international organisations that end up telling governments how to treat new asset classes. In countries where crypto is widely adopted, the risks of centralisation and dependence on decisions by major market players are growing.

“De”centralisation

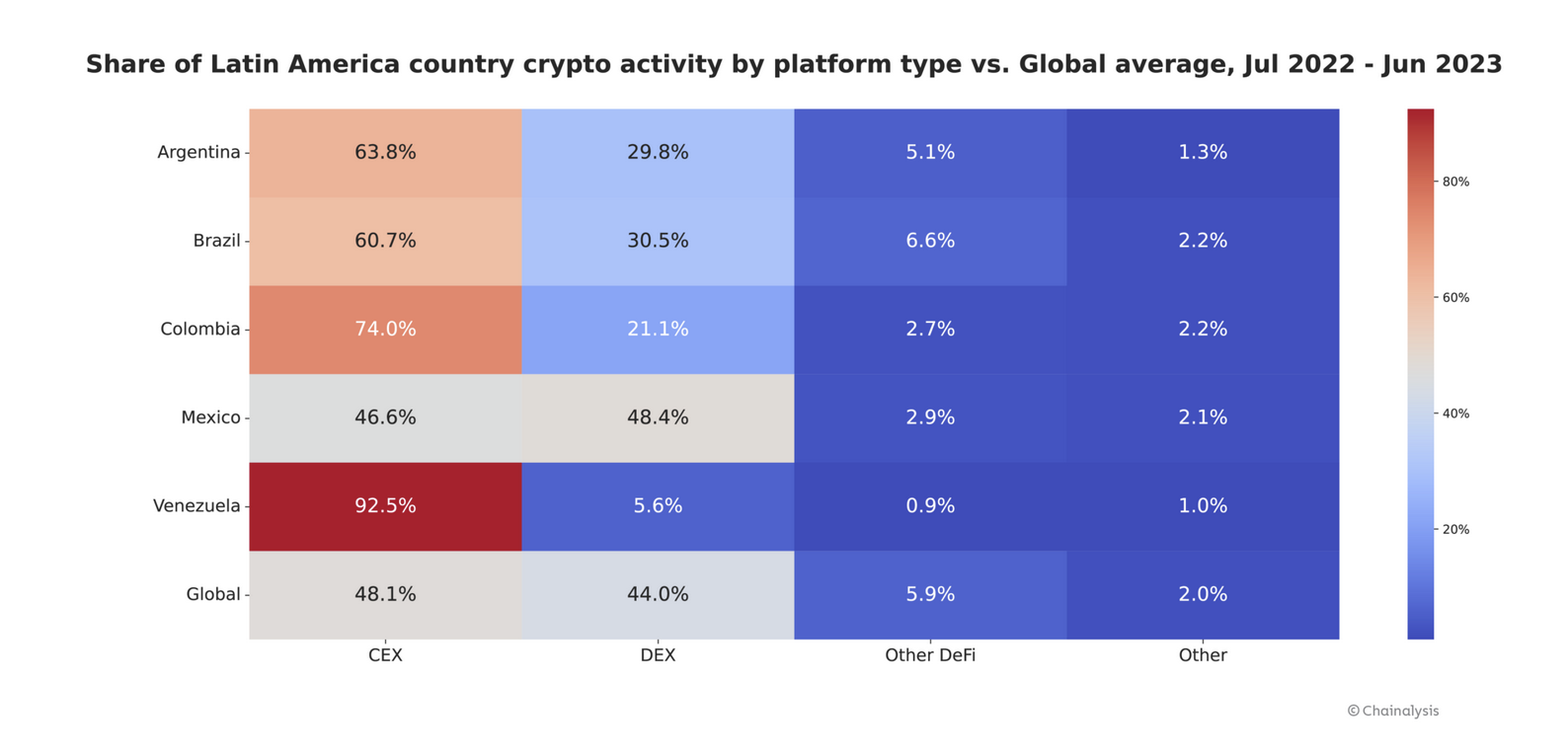

According to Chainalysis, people in Latin America mostly prefer CEX (68.7%). As of 2023, centralised platforms accounted for 92.5% of transactions in Venezuela, 74% in Colombia and 63% in Argentina. Only in Mexico was usage of CEX and DEX almost equal.

Mexico is the world’s second-largest recipient of remittances: by estimate, $61bn flows into the country each year, mostly from the United States. Bitso CEO Daniel Vogel told Chainalysis analysts that his exchange processed more than $3.3bn in crypto remittances sent from the US to Mexico in 2022 (5.4% of the total market).

This tilt toward centralised platforms reflects the mass user’s demand for simplicity. Unlike DEXs, many CEXs are straightforward and, in a sense, safe. Much the same goes for stablecoins.

They have become the dominant form of digital asset across Latin America thanks to their tight peg to the US dollar (USDT, USDC). In Argentina at least a third of the population relies on digital assets for everyday transactions. This helps locals avoid the effects of peso devaluation and preserve savings. The country’s share of transactions involving stablecoins is 61.8%, slightly ahead of Brazil (59.8%) and far above the global average (44.7%).

Obvious dependence on centralised platforms and products makes users in developing countries vulnerable to external circumstances and to decisions by major players.

For example, after problems arising for Binance in Nigeria, local clients lost the ability to interact with the platform. In March 2022 MetaMask users in Venezuela, Lebanon and Iran reported difficulties accessing the non-custodial wallet due to the team’s decision to “comply with legislation.”

In December 2023 Tether announced a new policy of freezing wallets whose owners are under OFAC sanctions. Given how unpredictable geopolitics can be, any country could, in theory, face economic restrictions.

In search of resources

Environmental concerns, local opposition and high electricity tariffs are pushing miners to seek new locations for their data centres, ideally where natural resources are plentiful. The choice often falls on developing countries.

In 2023 MARA announced the launch of a bitcoin-mining facility in Paraguay. The company chose Itaipu—the world’s second-largest hydroelectric power plant. Representatives pitched the news as a way to help the country avoid losses and monetise excess electricity.

Later, MARA made global expansion part of its strategy and did not rule out entering Africa. The region also attracted Chinese miners—Bloomberg reported a relocation to Ethiopia thanks to a favourable climate and low-cost electricity.

As of December 2024 the state utility Ethiopian Electric Power had signed contracts with 25 mining companies. The country’s share of bitcoin hashrate reached 2.5% in the same month.

Viewed one way, developing countries have offered major industry players their natural resources and labour, receiving financial benefits in return. Viewed another, they have constrained opportunities for home-grown development (it is hard to compete with a large player that entered the market with ease) and made themselves dependent on external circumstances. Moreover, much of the profit leaves the local economy.

Conclusion

Cryptocurrencies have opened access to alternative financial tools for users in developing countries, offering protection against hyperinflation and economic shocks. Yet the absence of domestic infrastructure and genuine decentralisation gives rise to a new form of colonialism.

Digital independence begins where control over data and technology is local. That is a challenge not just for developing countries, but for the entire industry.