Experts note rising centralisation in the DeFi sector

In most areas of DeFi, the core capital is concentrated in a few large projects. The Gauntlet report notes this, according to Bloomberg.

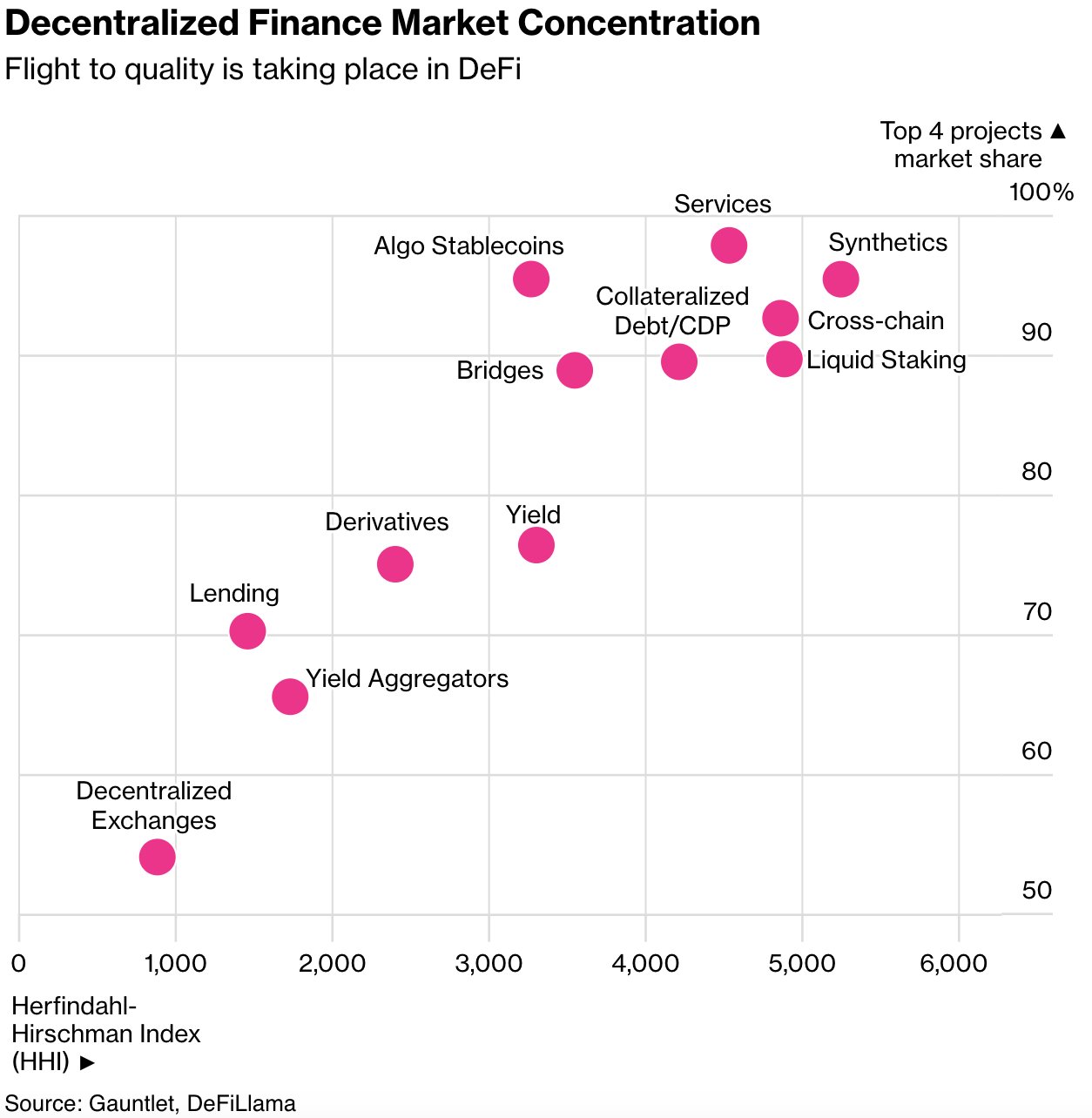

In total, analysts highlighted 12 sectors:

- decentralised exchanges (DEX);

- lending protocols;

- yield farms;

- yield aggregators;

- derivatives;

- cross-chain;

- bridges;

- algorithmic stablecoins;

- infrastructure services;

- liquid staking;

- synthetic assets;

- other services.

In its calculations the firm used data from DeFi Llama and the market concentration and competition metric—the Herfindahl–Hirschman Index (HHI)—a high score indicates a less decentralised market.

The strongest competition is observed in DEX: the four largest platforms control only 54% of the market.

Other sectors show less decentralisation. For instance, the total assets across the four liquid-staking projects account for about 90% of assets in the category.

“This has largely occurred due to security failures and risks in some new protocols, which has led to a ‘flight to quality’,” said Tarun Chitra, Gauntlet’s chief executive.

Yet a number of newcomers have managed to break into the leadership. According to the tracker Token Terminal, the total trading volume on Vertex Protocol—launched earlier this year—reached $69.5 billion.

The founder of one of the oldest and most profitable DeFi projects—MakerDAO—Rune Christensen expressed concern about the potential side effects of market growth:

“If the bear market really is over and there is a big upturn, I think it will be somewhat problematic for the industry. There are still many companies that could be wiped out, and that is a healthy process. That is the reality of startups. Most of them fail.”

Earlier, Chainlink’s head Sergey Nazarov expressed concern about the current state of protocol governance. In his view, there are only three “significantly” decentralised blockchains — Bitcoin, Ethereum and Chainlink itself.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!