The launch of Uniswap v3 marked a milestone in the development of decentralised finance (DeFi). By popularising the automated market maker (AMM) mechanism, the leading Ethereum exchange introduced to the market the concept of concentrated liquidity.

Almost immediately after the platform upgrade, new services emerged, aimed at increasing the profitability of liquidity providers on Uniswap v3 and reducing impermanent losses.

We examined such services, studying their functionality and performance metrics.

- Thanks to the radically new features of Uniswap v3, a new type of service appeared on the market, optimising the profitability of concentrated liquidity positions.

- Despite the apparently compelling concept and relevance, the returns of optimiser services have been modest.

- Concentrated-liquidity managers are exposed to various risks and perform poorly during periods of high market volatility.

Uniswap v3 features

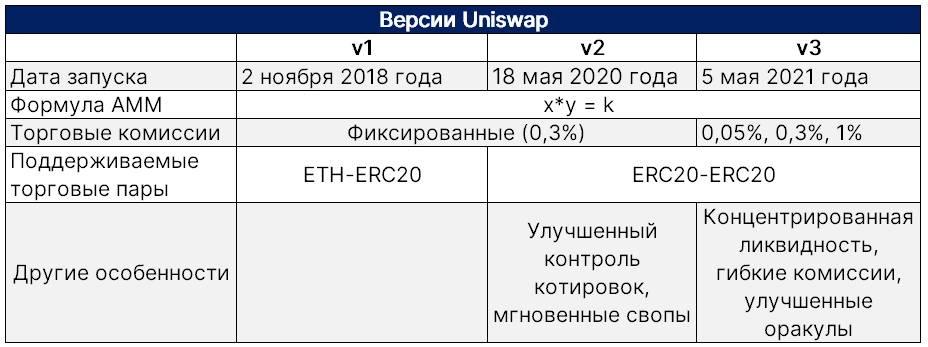

Uniswap is a leading Ethereum-based exchange by trading volume and user count. The first version of the decentralised platform began operating on 2 November 2018. Since then, more exchanges have emerged that use the automated market maker (AMM) mechanism instead of a traditional order book.

In May 2020, Uniswap v2 was launched, whose key feature was the ability to place ERC-20 tokens in pools with any other assets of the same standard.

Key advantages of the first two versions:

- Ease of use — an intuitive interface that opened the possibility for anyone to earn passive income from provided liquidity.

- Compounding of commissions. Accumulated by liquidity providers (LPs), the commissions are returned to the pool, creating a compound interest effect.

- Interchangeability. LP tokens are interchangeable with each other like LEGO pieces. Such assets can be used as collateral in protocols like Aave or MakerDAO, increasing capital efficiency.

On 5 May 2021, Uniswap launched the third version of the protocol with radically new features and capabilities, among which:

- concentrated liquidity;

- range-limit orders;

- multiple positions within a single pool.

In the third version, a three-tier fee structure (0.05%, 0.3% and 1%) also appeared. It is designed to give liquidity providers (LPs) the ability to choose pools in line with their risk appetite. For example, the ETH/DAI pair is more volatile than USDC/DAI, implying higher risk.

Fees of 0.05% are typical for pools with stablecoins. The 0.3% level is common for pools like ETH/DAI, and 1% for far more volatile pairs with low-liquidity assets.

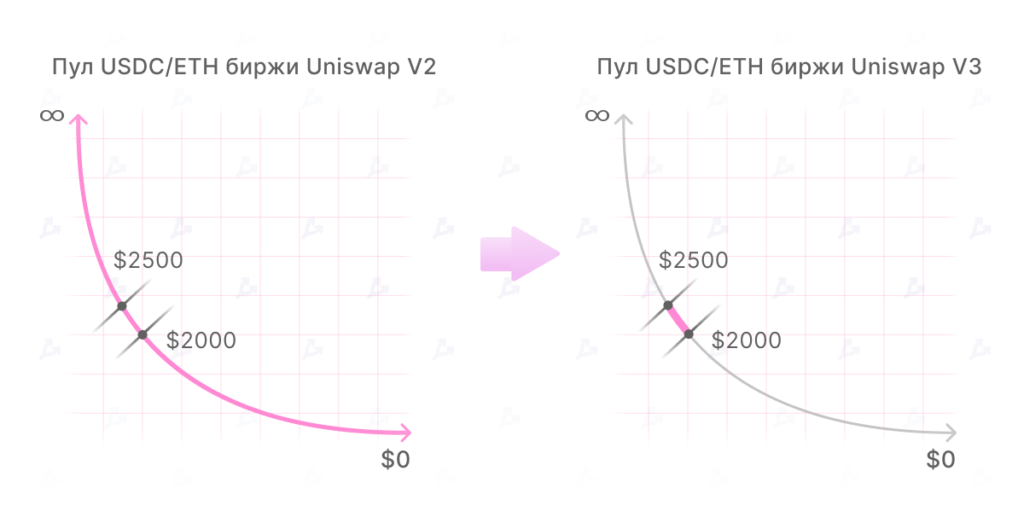

Thanks to the now-popular DeFi concept of concentrated liquidity, LPs can choose specific price ranges within which their funds are placed in the pool. For example, a participant could place 30% of assets in the USDC/ETH pool for the $2000–$3000 range, allocating the remaining 70% to a narrower range — $1500–$1700. There are countless options.

In the first two Uniswap versions, liquidity was distributed evenly along the price curve. This means users did not need to select price ranges, merely load assets into pools.

The downside of this simple approach is that only a portion of liquidity is effectively employed. The price of even highly volatile assets cannot move from zero to infinity; it largely remains within a limited portion of the price curve.

This means liquidity scattered in regions irrelevant to current market conditions simply sits unused. As a result, capital is not used as efficiently as it could be.

Uniswap v3 liquidity providers can use capital far more efficiently by selecting individual price curves. To illustrate how this mechanism works, imagine Alice and Bob provide liquidity to the USDC/ETH pool. Each has $10,000, and the current Ethereum price is $2,700.

Alice deposited 5,000 USDC and 1.85 ETH into the v2 pools, effectively splitting her capital evenly between the two assets.

Bob chose not to put all funds into a single pool. By selecting a price range between $2,200 and $3,200, he deposited only 600 USDC and 0.22 ETH. The remaining $8,800 was deployed elsewhere.

Despite the large difference in invested amounts, Alice and Bob would earn the same commission income while ETH remains in the $2,200–$3,200 range. By upgrading to the new Uniswap version and selecting an optimal range, Bob made his capital work many times more efficiently.

Moreover, he significantly reduced risk. If the ETH price suddenly falls to $0, Bob would lose 12% of his capital, while Alice would lose all of hers.

To implement the concentrated-liquidity concept, Uniswap’s developers had to make some compromises. For example, third-version liquidity providers receive NFTs instead of interchangeable ERC-20 tokens representing their funds in the pool.

“However, positions can be made interchangeable through the use of third-party contracts and partner protocols. In addition, trading fees are no longer automatically reinvested back into the pool on behalf of the LP,” explained in Uniswap’s blog.

By choosing narrow price ranges, providers expose themselves to the impermanent loss risks inherent in AMMs. Given the volatile nature of most crypto assets, selecting an optimal range can be challenging. Capital efficiency is not easily achieved—there is always a risk that the price will move out of the user-set range.

For example, a user provides liquidity to the USDC/ETH pool, setting the concentrated-liquidity range at $2,500–$4,000. If the price falls below $2,500, all liquidity provided by the provider is converted into ETH. If the second-largest crypto climbs above $4,000, the user ends up with USDC. In both cases the LP stops earning fees, exposing themselves to the opportunity costs.

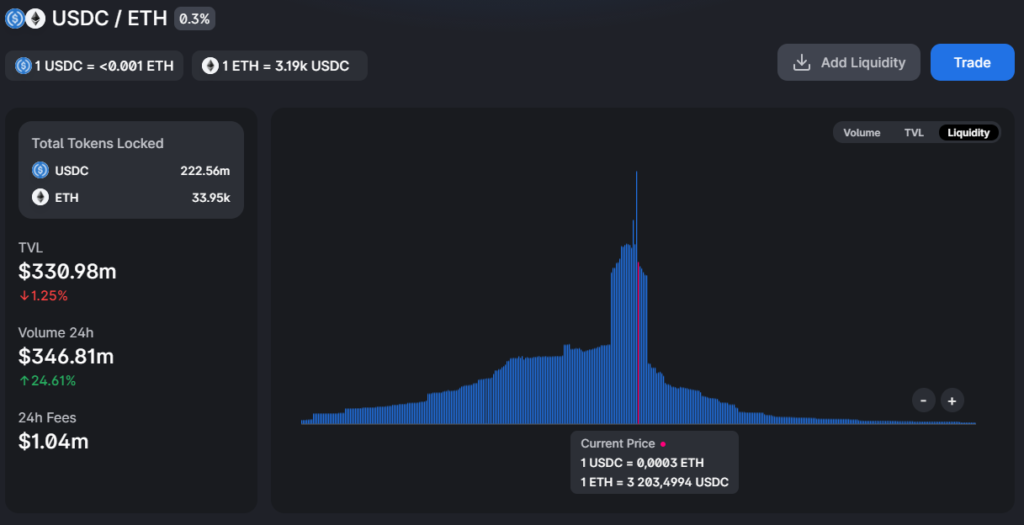

Despite these drawbacks, the turnover of the new version of the exchange is several times higher than Uniswap v2. The difference is also visible when looking at individual pools, including USDC/ETH — $332 million versus $305 million (as of 9 Aug 2021).

According to Nansen’s July study on the market-making landscape of Uniswap v3, the majority of Uniswap v3 users (58%) hold only a single concentrated-liquidity position. More than five such positions are held by fewer than 10% of addresses.

“In total we identified 22,684 unique addresses that hold/held Uniswap v3 positions. A significant portion (77%) of such users are passive liquidity providers. This means they rarely adjust their position parameters,” researchers noted.

Fourteen percent of users held between one and five positions and changed them more than twice. Only 1% of providers held more than 25 positions.

Thus, only a small share of users adopts a proactive approach to liquidity management. In response to market conditions, various services have emerged to manage concentrated Uniswap v3 positions with minimal user involvement.

Key approaches to managing LP positions

The process of withdrawing liquidity after price exits the target price corridor and reallocating funds to another range is called rebalancing. The aim of recently emerged liquidity-management services for Uniswap v3 is to automate rebalancing of LP positions. In addition, such services may reinvest the liquidity providers’ commission income.

Native tokens of such platforms are typically ERC-20 standard. This means they can be used as collateral on lending services, as well as participate in programs liquidity mining.

According to the Charm Finance Alpha Vaults documentation, Charm Finance’s Alpha Vaults has two approaches to managing concentrated liquidity:

- Active rebalancing, involving token swaps to subsequently place funds in a new range and, accordingly, a certain commission for each such operation.

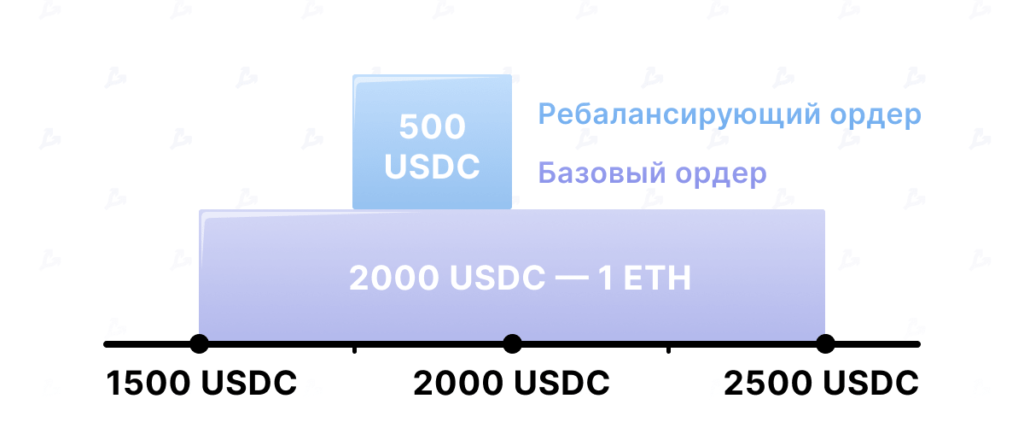

- Passive rebalancing — does not involve token swaps to move the position to another range. Instead, two types of orders are used — a base order and a rebalancing or “single-sided” order. Base orders are placed symmetrically around the current price. The second order type occupies a narrower range, close to the current price and aligned with the base. Order parameters change every 12 hours.

“The term ‘single-sided liquidity’ isn’t entirely clear, but in essence it behaves like a limit order placed close to the current price. Thus, if the price moves in that direction, the second position becomes active and starts collecting LP fees,” explained in his article by the DeFi expert going by the nickname Vividot.

In the example above, liquidity is illustrated as 1 ETH and 2000 USDC in the base range of $1,500–$2,500. When the price fluctuates between $1,750 and $2,000, a rebalancing order is triggered, converting excess USDC into ETH.

According to Vividot, with passive rebalancing, fees are not charged. On the other hand, LP position profitability declines during strong and prolonged price movements in a given direction. In such periods, the passive rebalancing strategy does not work, making a proactive approach to position management more attractive.

“Choosing the rebalancing range is even more important than choosing the method of rebalancing,” the expert stressed.

A dilemma is looming:

- The most capital-efficient range is as narrow as possible and best aligned with future prices (which are unknown);

- Choosing a narrow range risks lower returns during periods of heightened market volatility.

If a user aims to minimise impermanent loss (IL), they should choose the broadest possible stretch of the price curve.

Each Uniswap v3 liquidity manager has its own approach to selecting a range and managing the position. These services charge a performance fee, sourced from Uniswap v3 fees. The returned remuneration is used to cover gas costs for rebalancings, token buybacks, and other purposes.

To illustrate the importance of such fees when choosing liquidity-management strategies, Vividot provided the following example:

“Suppose Manager 1 uses a wide-range strategy (low LP fees, small IL risk). Manager 2 uses narrow ranges (high LP fees, high IL). In this case, the performance reward is the same (10%), as is the outcome in the form of LP fees and the magnitude of IL. However, Manager 2 will pay more rebalancing fees, which is undesirable from the user’s perspective.”

According to the expert, the rebalancing period is also crucial, as it determines the compounding of LP fees and IL realization.

Overview of Uniswap v3 liquidity managers

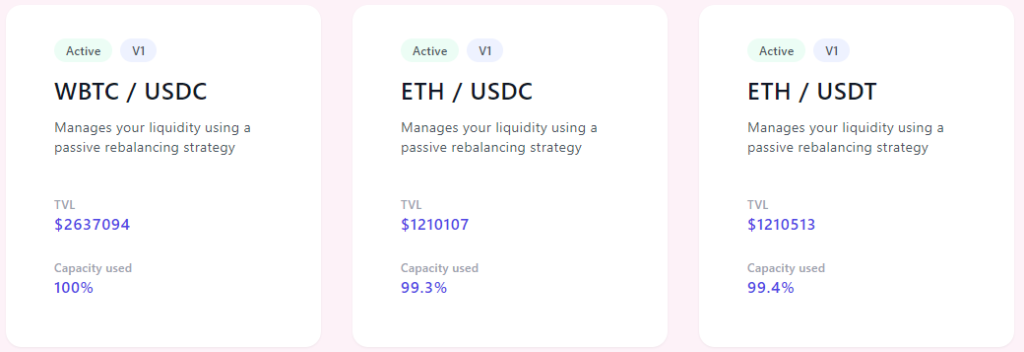

Alpha Vault. This is the first service of its kind, launched on May 7 — two days after the third version of Uniswap began operating. As of writing (10.08.2021) there are three automated liquidity pools:

- WBTC/USDC;

- ETH/USDC;

- ETH/USDT.

The TVL of the first pool surpassed $2.6 million, with the second and third at $1.2 million. The project periodically raises caps on the total assets in the vaults.

Alpha Vault uses a passive rebalancing method and ranges that depend on time-weighted average price (TWAP). The performance fee is 5%, with funds flowing into Charm’s treasury.

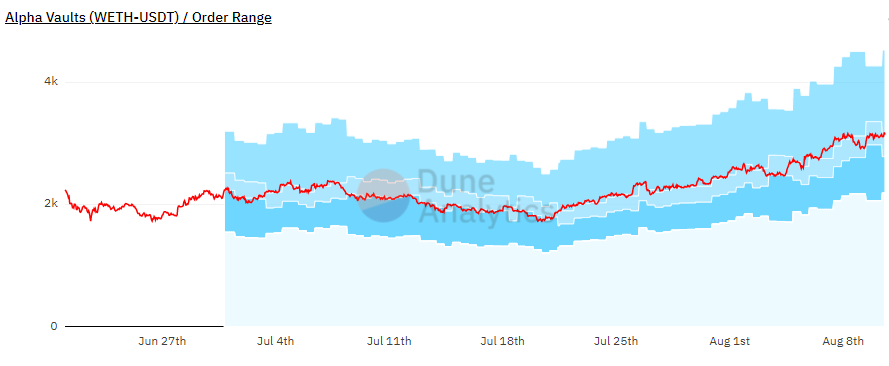

The chart below shows the range dynamics for the WETH/USDT pair. Light blue and blue indicate rebalancing and base orders.

As can be seen, the ranges are fairly wide. This approach aims to reduce losses during sharp price movements.

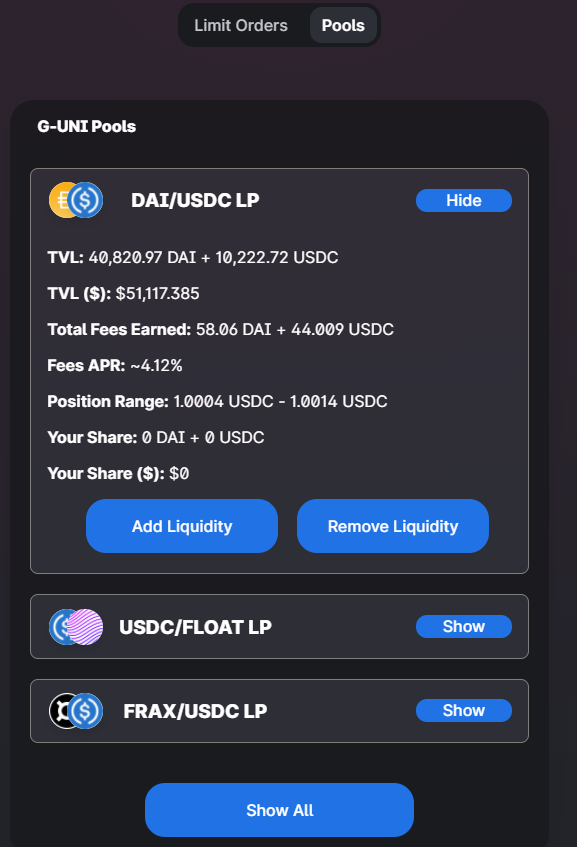

Gelato Network. The project has its own ERC-20 token — G-UNI. It is used in a liquidity mining program developed with the DeFi platform InstaDapp.

Liquidity management is carried out on Sorbet Finance by Gelato Network developers.

The platform markets itself as a network of bots using smart contracts for active rebalancing. The price range is set by the developers. The performance fee is 10%.

Visor Finance. The beta version of the service began on 18 May. The project uses Bollinger bands to determine price ranges.

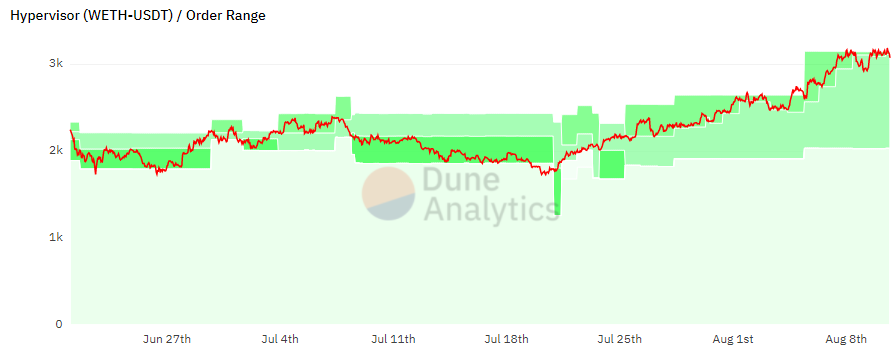

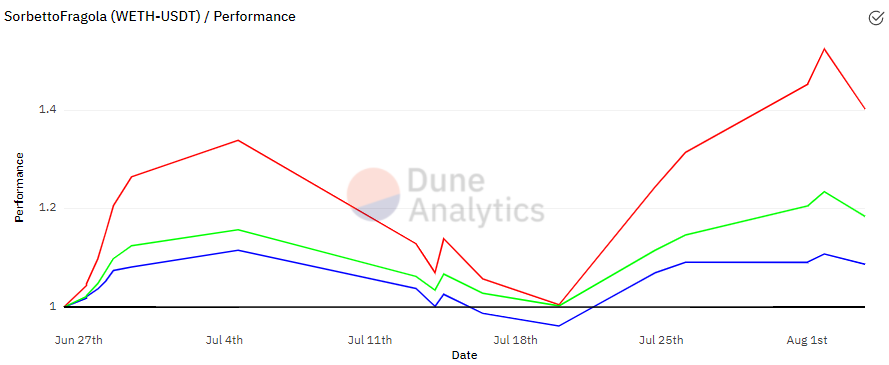

WETH-USDT metrics lag even more behind alternatives amid Ethereum’s price rise. A notable advantage is the relatively shallow drawdown of the LP position during the July market correction.

Not encouraging either is the yield from Sorbetto Fragola by Popsicle Finance.

By the charts, the traditional v2 pools perform better than v3-optimisers. In a bull market, investors find it easier and more profitable to hold assets in a wallet (HODL).

“Currently, LPs that stay within a broad price range show good performance,” noted Vividot. “If the ETH price falls sharply or rises, moving outside the range, the metrics can become terrible.”

A Twitter user with the handle revert shared an example of the ETH/USDC position in a wide range — $1,665–$3,334.

1/ ETH/USDC position on a range from $1655 — $3334 has a 94% apr vs HODL. It has stayed within range 100% of the time for its 42 day life, has had no capital reallocation or fee collection. https://t.co/2Zk2BoVGO1 https://t.co/ta11tAIyaz pic.twitter.com/86HER3uFPS

— revert 🦇🔊 (@revertfinance) July 3, 2021

According to his observations, the position yielded a return nearly on par with HODL. Throughout all 42 days of observation, the position remained within the defined range.

As with any DeFi service, concentrated-liquidity managers are not immune to hacks and bugs. The aforementioned Popsicle Finance protocol recently suffered a hack, resulting in the loss of $20.7 million.

The flaw was found in Sorbetto Fragola’s product. The attacker drained 85% of the pools.

“The hacker forced the contract to believe that he had earned as many fees as the total value locked in the pool and, based on that, had a claim to the $20.7 million held in the pool,” the project said.

Subsequently, the attacker swapped the obtained coins for ETH on Uniswap and then moved the funds to the Tornado.Cash mixer to launder them.

Popsicle Finance later said that 439 addresses were affected. 146 of them had active positions in at least one pool. 62% of addresses had losses under $10,000, and 86% under $60,000.

The developers assured users that the bug has been found and plans for compensation and a restart of Sorbetto Fragola have been drawn up.

Conclusions

The profitability of most LP optimisers remains unimpressive. It is substantially lower than standard HODL returns and the performance of Uniswap v2 liquidity pools. On the other hand, this sub-segment is nascent and it is early to draw strict conclusions about the effectiveness of such services.

The Aloe Capital approach, integrating with prediction markets, looks most interesting. However, forecasting future prices of volatile crypto assets remains challenging, so the project’s tokenomics still has to prove itself.

The potential of Uniswap v3 is far from exhausted. The concentrated-liquidity concept opens broad possibilities for creating automated asset-management strategies. The success of developers of new solutions could broaden crypto investors’ options, democratise market making in DeFi, and strengthen Uniswap’s market position amid rising competition.

Subscribe to ForkLog’s channel on YouTube!