Anchor — the largest protocol of the Terra ecosystem — continues to grow TVL amid persistent demand for the stablecoin UST. The latter has already overtaken Binance USD in market capitalization, taking the third place in the ranking of stablecoins by this metric.

Clearly, the popularity of the algorithmic stablecoin is largely linked to the nearly 20% annual yield offered by the Anchor protocol. In this context a number of questions arise:

- how long can such a high rate be sustained?

- how resilient is the Terra economy?

- would a potential decline in Anchor’s rate lead to capital outflows to other protocols and divert UST from its $1 peg?

- will the stablecoin Bitcoin reserve from LFG help?

ForkLog has looked into these and other questions.

Astounding success

In just a year, Anchor’s TVL rose almost 25-fold—from $0.6 billion to $16 billion. The platform now ranks third in the overall ranking of the sector, behind only Curve and Lido. The latter supports a wider range of networks.

Given the rapid growth, Anchor is likely to become a leader among DeFi ecosystems soon.

Recently the protocol added support for Avalanche. However, this network’s share of total TVL is small—only $158 million.

The figures underscore Anchor’s critical importance to the Terra ecosystem. The TVL of the latter stands at $29.29 billion (as of 24.04.2022). The Anchor dominance index is 54.45%.

In other words, a large portion of activity in the Terra ecosystem is tied to Anchor, which accounts for 72% of the total UST supply.

Всего пользователи депонировали в Anchor 13 млрд UST. Согласно CoinGecko, общее рыночное предложение стейблкоина составляет 18,1 млрд.

Устойчивый спрос на UST обусловлен высокой доходностью на Anchor. И это положительно отражается на курсе LUNA, поскольку для выпуска UST необходимо изымать из обращения соответствующее количество нативной криптовалюты Terra. Механизм, во многом опирающийся на арбитражеров, помогает поддерживать паритет с американским долларом.

Другими словами, чем больше выпускается UST и заходит в Anchor, тем больше сжигается LUNA и тем сильнее растет ее цена.

As a result, UST’s market capitalization and LUNA’s price are closely correlated.

In early November, the total market value of the stablecoin stood at less than $3 billion; now the figure exceeds $18 billion. Over the same period, LUNA’s market value roughly doubled.

Not for long

Digging deeper, the Terra ecosystem’s prospects are not cloudless. Anchor Dashboard shows that total deposits exceed the value of borrowings in circulation by more than three times.

The project is experiencing a sharp asset shortage needed to sustain interest accrual for lenders. The distribution of the native token ANC among borrowers is not particularly effective and does not smooth out the imbalances.

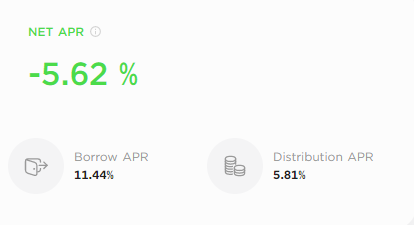

As of 24.04.2022, the actual borrowing rate on Anchor stands at -5.62% (UST loans issued at 11.44%, and the annual ANC yield is 5.81%).

In March, the project community voted for a proposal, according to which the yield rate on deposits can change by up to 1.5% per month depending on the reserve volume on Anchor.

The current crypto-market climate is not characterised by high activity. In an environment where fear dominates greed, many investors favour stablecoins, borrowing reluctantly against crypto collateral due to liquidation risk.

Low business activity, often punctuated by panicky mood, will only favour deposits over borrows and further shrink reserves. Consequently, the yield rate is likely to fall to 1.5% soon.

Critics argue that a decline in the attractiveness of UST deposits would push funds out of Anchor into other protocols, increasing demand for alternative stablecoins.

This, in turn, could dampen arbitrageurs’ incentives to maintain the peg to the US dollar. As a result, its volatility would rise, potentially triggering a larger outflow of funds and, possibly, catastrophic consequences for the entire ecosystem due to an irreversible loss of the peg at $1.

«Could reserves of $2 billion really defend a $17 billion stablecoin from collapse? No, of course not,» emphasised Hartmann.

Researcher Ryan Clement(s) is convinced that the backbone for algorithmic stablecoins should be a sustained demand for ecosystem products. The latter determines the efficiency of the arbitrage mechanism.

The parity to the dollar could be broken if the traders backing the peg lose confidence in the system. This risks a “death spiral.”

Clements also questions whether UST can be considered a decentralised asset.

“The fact that Terraform Labs needs a centralised structure (LFG) to inject capital, buy reserve assets and continually take steps to strengthen Terra’s ecosystem (and create more use cases for UST) calls into question Terra’s decentralised nature,” said Clements.

Messari analyst Dustin Teander, on the contrary, argues that UST remains decentralised despite the above processes.

“BTC is effectively considered only after Jump Crypto’s proposal is implemented. And when that happens, Bitcoin would be used in a decentralised protocol, not a centralised organisation,” he emphasised.

Conclusions

Terra’s success has spurred various projects to create similar stablecoins and reserve crypto funds. However, potential issues with Anchor, including a decline in yields and capital outflows, could lead to serious consequences for the ecosystem, the DeFi sector, and the entire crypto economy.

The leading Terra platform and the stablecoin UST require tokenomics revisions aimed at a long-term horizon. Otherwise, mounting dislocations could drive capital toward other projects, coins and ecosystems.

This is likely to shake the UST price and trigger a “death spiral,” as it would deprive arbitrageurs of the incentive to sustain the peg with the US dollar.

Subscribe to ForkLog news on Telegram: ForkLog Feed — all the news stream, ForkLog — the most important news, infographics and opinions.