The Bitcoin mining industry is attracting the attention of traditional and venture investors. With the advent of synthetic assets and hash-rate-based financial instruments, there are more options for investing in mining.

This signals the sector’s maturity, but investors still lack the knowledge and experience to build a sound investment strategy.

Researchers at Anicca Research told about the options available to those looking to invest in mining beyond purchasing and plugging in equipment.

They classified all hash-rate-related assets and financial instruments and examined their merits and drawbacks.

- Investing in mining is possible not only through buying and operating equipment, but also through financial instruments (cloud mining contracts, machine tokens, hash-rate forwards and others).

- Markets for such synthetic instruments are small and immature; there is a risk of fraud.

- Another way to invest in mining is to work with specialised companies (SPVs).

Equipment Markets

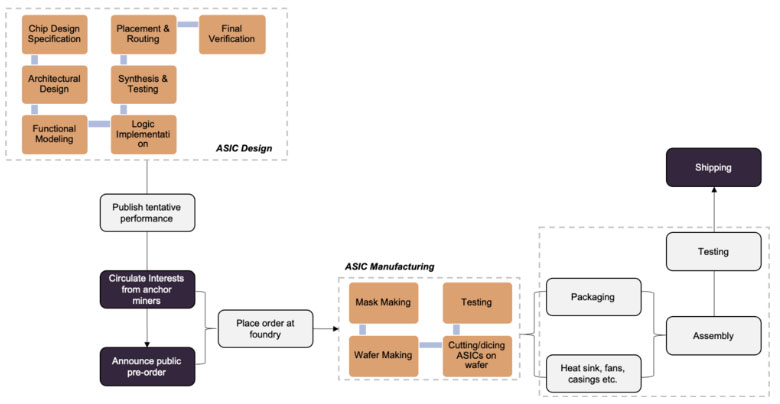

Several factors influence mining, including the quality characteristics of the equipment, the location of the farm, and electricity supply conditions. The production of ASIC miners involves many stages, including chip design, actual manufacturing, supply chain, and maintenance.

Manufacturers typically plan the release of new equipment for the rainy season in Sichuan province in May to maximise demand from miners. Most of the latest models are snapped up instantly. Only a small fraction goes to retail. Most devices are supplied to large miners and distributors on pre-orders. A new generation of ASIC miners is usually available about six months after the announcement.

Purchasing new devices from manufacturers resembles buying oil supply contracts dating back to the 1980s. The seller under the contract agreed to deliver the specified amount of oil in the planned timeframe, but the price was determined unilaterally by the oil company.

Since 2018, miners manufacturers have become more cautious in inventory management. They assemble devices only after orders are confirmed and aggregated. Buyers typically expect delivery in 2-3 months.

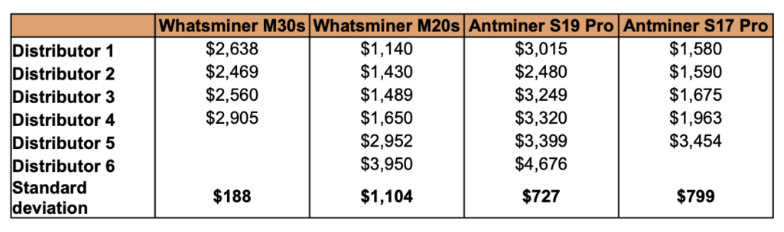

Many are forced to purchase new equipment at a premium from distributors. The price can vary significantly depending on distributor location and stock availability.

There is a sizeable secondary market for mining equipment. Purchases on it require substantial experience. Deals are usually without intermediaries, and sellers understand device quality better than buyers. Typically, used ASIC miners carry no warranty and often do not disclose promised performance characteristics.

In the secondary market it is even more important to choose reliable distributors and sign contracts that provide compensation in case of delivery delays or substandard equipment.

It is well known that the mining equipment market is illiquid. Some devices are easier to acquire on the secondary market because they were produced longer ago and in greater quantities.

Mining devices are commodities. Machines with the same efficiency can fetch the same price from different manufacturers. But once they reach the secondary market, everything depends on supply and demand. This is why, although over the last two years MicroBT and Canaan have pushed Bitmain aside, Bitmain’s devices still dominate the secondary market.

Valuing an ASIC Miner

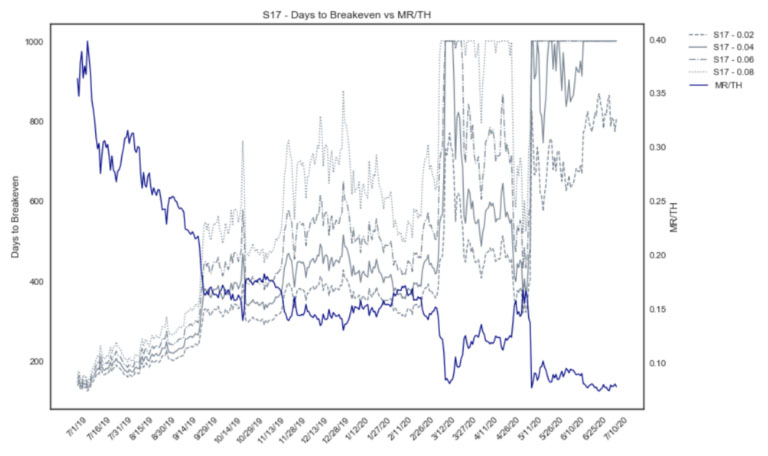

A multitude of factors influence the price of mining devices, but the primary driver is profitability. Today, the most commonly used valuation metric for machines, especially in China, is the number of days to break even. This metric is easy to calculate and intuitively straightforward.

Where:

D — static days to break even.

C — upfront capital expenditures.

P — current Bitcoin price.

S — hashrate produced by the purchased equipment.

H — network hashrate.

m — the block reward (currently 6.25 BTC).

n — current average transaction fee per block.

k — efficiency (J/TH) of the equipment.

r — total electricity cost ($/kWh).

However, this is a static metric that cannot capture all components of a device’s cost. Its two main components are revenue and price.

Before investing in mining, one must understand the structure of one’s costs and lock in per-unit expenses over the machines’ lifetimes. Revenue is determined by the Bitcoin price, network hashrate and the block reward size.

Synthetic Hashrate

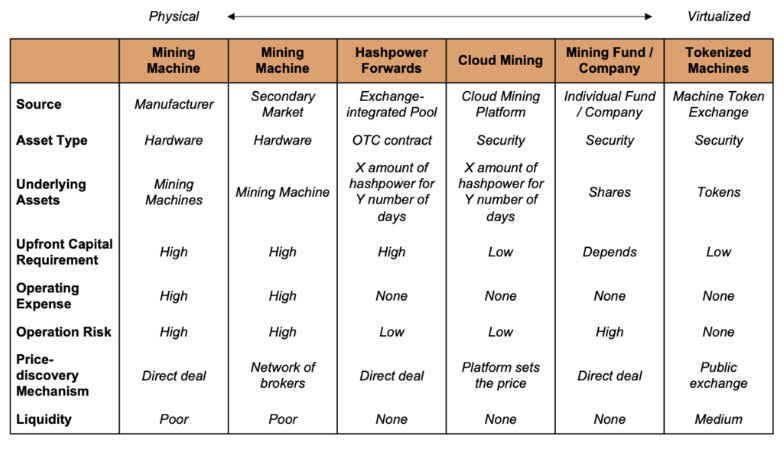

In addition to the complexity of financial valuation, buying and operating mining devices involves many operational risks. For retail buyers, the process can be daunting. A simpler way to invest in cryptocurrency mining is through synthetic hash-rate-based assets.

Some of these are cloud mining contracts. This is a primitive form of a financial derivative that separates hashrate from the physical location of the equipment.

Over the years, countless cloud mining projects have appeared and disappeared. The dilemma is that they are clearly aimed at retail investors, as large players prefer to work with hardware. But evaluating such contracts requires knowledge of the mining industry and experience with financial derivatives. This is the main reason that, although cloud mining in theory is the natural next step in the development of capital markets in the sector, most such projects are seen as scams. Often, that is indeed the case.

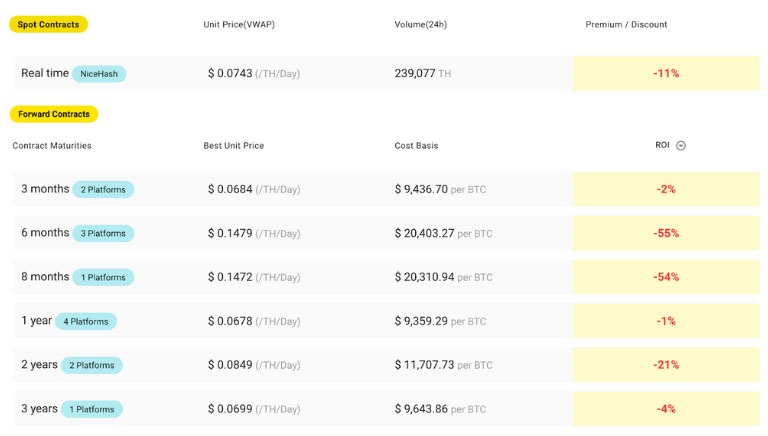

Being immature and still relatively small, cloud mining suffers from a complete lack of market standards. Using data from the HoneyLemon Market aggregator, one can see that contract terms and prices vary markedly across platforms:

By mid-July the majority of contracts were unprofitable. Because of an additional cost markup to the generation of hashrate, specific market conditions are required for cloud mining to be profitable. As a rule, after a prolonged price decline the trend often moves into a rally (for example, April–May 2019). Demand for hashrate then increases. Acquiring and installing ASICs takes time, and purchasing cloud mining contracts is a faster way to invest in mining.

Another synthetic asset based on hashrate are “machine tokens” (machine tokens). These are liquid tokens that virtually represent a part of a mining device. Traders speculate on the volatility of the secondary market for machines rather than the coins produced by the equipment. The concept has existed for some time, but the volumes of this market do not show meaningful growth. The main reason is that the multi-dimensional nature of mining income prevents speculation on pricing of these assets from converging.

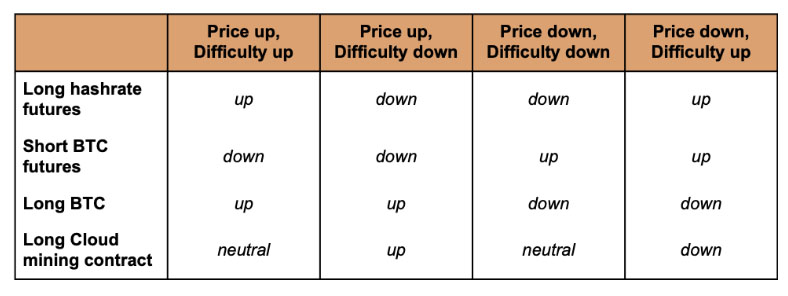

Experienced traders can structure portfolios of synthetic assets based on hashrate. For example, buy a long contract for cloud mining simultaneously with a long position in hashrate futures and add a short BTC futures position. There are many creative ways to structure portfolios using financial instruments. For funds and trading firms that do not wish to operate hardware, this is another way to invest in mining.

In practice, building a balanced portfolio is a task with many nuances. The hedging coefficients for each instrument must continuously be updated. Management requires careful oversight and frequent adjustments. There are many constraints, such as low liquidity and opaque pricing. Traders must precisely understand the risks they need to account for.

For miners a new hedging method has become forward contracts on hashrate. Similar to renting computing power on cloud mining platforms, forward contracts allow a miner to sell a fixed amount of hashrate over a defined period at the initial price. Unlike cloud mining, they typically offer more flexible terms. But without a widely accepted benchmark, the forward market lacks a settled pricing system. Each deal becomes a negotiation, and the counterparty who executes it bears certain risks.

The number of such deals will grow as more exchanges and financial services integrate with mining pools.

Many are interested in BTC flows from miners, but the high liquidity of exchanges allows offering creative and potentially risky deal types to win this race.

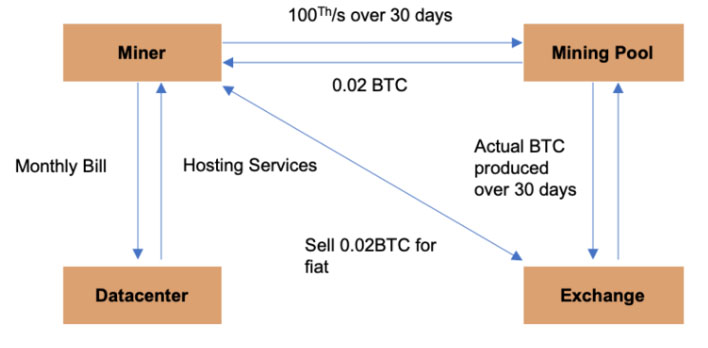

Miners can set terms to always sell a percentage of their hashrate to cover operating costs. The counterparty then receives a stream of coins produced by that hashrate from the pool. For example, a miner might pre-sell 100 TH/s for 30 days at the start of the month. Based on projected difficulty growth and fees, the pool offers to pay upfront 0.02 BTC. The miner commits 100 TH/s to production for the month, transferring production risk to the pool.

Binance, OKex and Huobi are actively expanding their pools. It is expected that other exchanges will follow suit or become partners of existing pool operators. Some financial and trading firms are also moving in this direction: Babel Finance intends to launch an Ethereum mining pool, Three Arrows Capital — to offer structured products via Poolin.

Specialized Companies for Hashrate Investing

Because most traditional investors and venture capitalists do not possess the skills and experience to manage equipment or structure complex hash-rate-based asset portfolios, they often invest in mining through specialized companies (SPVs). SPV managers use investor capital to buy and operate machines, taking a share of the revenue in return.

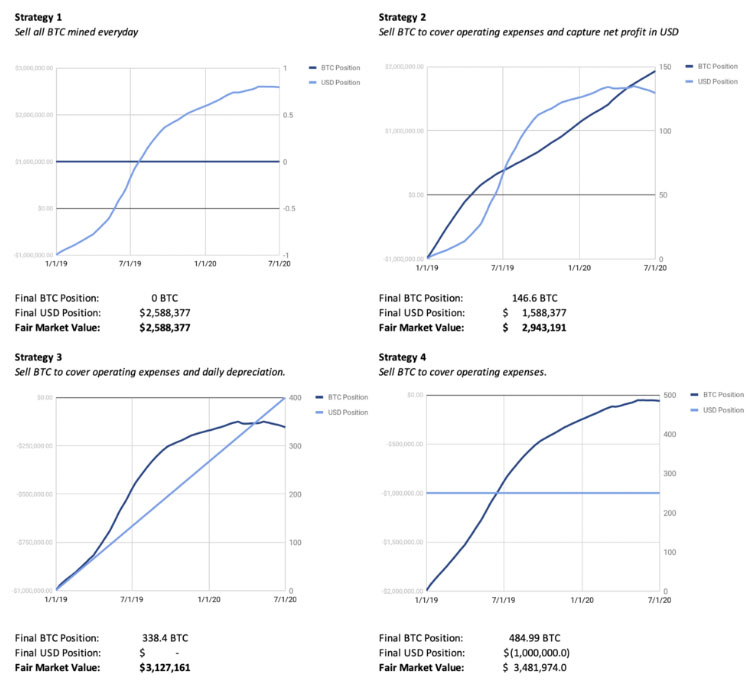

Crucially, how SPV managers manage cash flow is central to financial success. The development of a prudent sales strategy to counter market shifts is of decisive importance.

There are four typical strategies to consider under assumed conditions:

- Start date: 01.07.2009.

- Valuation date: 01.07.2020.

- Initial investments: $1 million.

- Number of devices: 4840 S9 units, acquired at $206.6 per unit. Depreciation is charged linear over 18 months.

- Total hashrate: 67 761 TH/s.

- Total power consumption: 6 389 kW.

- Total electricity price: $0.04 per kWh.

Options:

- Sell all mined BTC daily.

- Sell BTC to cover operating costs and lock in net profit in USD.

- Sell BTC to cover operating costs and depreciation of equipment.

- Sell BTC to cover all operating costs.

The strategies outlined represent different risk preferences for BTC and USD positions. The most profitable among them may not deliver maximum returns in another market environment. Depending on the manager’s objective (accumulating BTC or returning USD), the strategy can be tweaked accordingly.

Mining entities with seasoned traders on staff may also sell rewards and buy back coins when the price dips below the cost of production, use financial instruments (secured lending, BTC futures, etc.) to hedge price risk.

There have been many well-capitalised mining projects that failed due to mismanagement of trading positions. The infamous example is Gigawatt in 2018. According to court documents, the company’s assets were valued at less than $50,000 against liabilities of $10–50 million at the time of the bankruptcy filing.

Subscribe to ForkLog news on Telegram: ForkLog Feed — the full news feed, ForkLog — the most important news and polls.