- Trump Media & Technology Group will raise $2.5bn via an issuance of common stock and convertible notes to acquire digital gold.

- The execution of the bitcoin strategy resembles a pyramid propped up by a premium of the securities over the value of the coins.

- An analyst drew parallels between MSTR and Grayscale’s GBTC.

Trump Media & Technology Group (TMTG), the parent of U.S. president Donald Trump’s social network Truth Social, on May 29 will place roughly $1.5bn of common stock and $1bn of secured convertible notes.

Around 50 institutional investors, with whom agreements have been reached, will purchase the securities.

Proceeds will fund a bitcoin treasury.

“We view digital gold as the culmination of financial freedom. […] The investments will create synergies with subscription payments, utility tokens and other planned transactions in Truth Social and Truth+,” the statement said.

The offering will expand the company’s balance sheet 4.3 times; it stood at $759m at the end of the first quarter.

Cantor Fitzgerald & Co. acted as financial adviser to the deal. Earlier, Brandon Lutnick became the firm’s chairman and CEO, the son of former head Howard Lutnick, who this year took office as U.S. commerce secretary.

Crypto.com and Anchorage Digital will serve as custodians of the coins.

On May 26 the Financial Times, citing informed sources, reported that TMTG planned to raise $3bn via a securities offering. Trump Media denied this.

TMTG will join the roster of companies that have adopted a bitcoin strategy. According to BitcoinTreasuries, there are 114 such organisations, holding a combined 807,853 BTC (3.85% of supply). The leader is Strategy with 580,250 BTC ($63.2bn).

Signs of a pyramid?

A user going by Lowstrife shared concerns in a thread about how such large-scale buying of digital gold could ultimately “blow up” the whole structure.

Bitcoin treasury companies are all the rage this week. MSTR, Metaplanet, Twenty One, Nakamoto.

I think they're toxic leverage and the worst thing which has ever happened to bitcoin & what bitcoin stands for. In the right conditions, here's the mechanism of how this blows up

1/n pic.twitter.com/3I4NNAs0Le

— lowstrife (@lowstrife) May 23, 2025

The specialist pointed to rising leverage at Strategy and firms copying it, fuelled by a constant wave of securities issuance that dilutes existing shareholders.

“[This method] works great if mNAV > 1. The problem is that the leverage relies on ATM to fund mandatory payments. If MSTR trades below 1 mNAV as it did in 2022, there’s a problem,” Lowstrife noted.

He highlighted a management habit of pushing securities payments into the future, which ultimately creates side effects.

For the common stock, bitcoin’s price appreciation may not offset lower returns from fresh issuance. For the convertible debt, refinancing or selling some coins may be required.

With preferreds comes the need to pay dividends. Issuance of such securities and their cash flows would be financed by diluting common shareholders.

“STRF is a perpetual 10% security. Strategy will constantly tap the ATM to fund every dollar issued. Forever. Purchases made today at the expense of future shareholders. What does this look like?” the analyst asked.

Lowstrife stressed the dependence on market conditions. He noted there is an option to suspend dividend payments, but deemed activation unlikely, as it would be seen as a sign of potential insolvency.

“How does this end? It all starts with mNAV. mNAV is everything. […] If it breaks, the company’s ability to raise capital weakens. Conversion hurts mNAV. The company loses the ability to make financial payments on its debt,” he forecast.

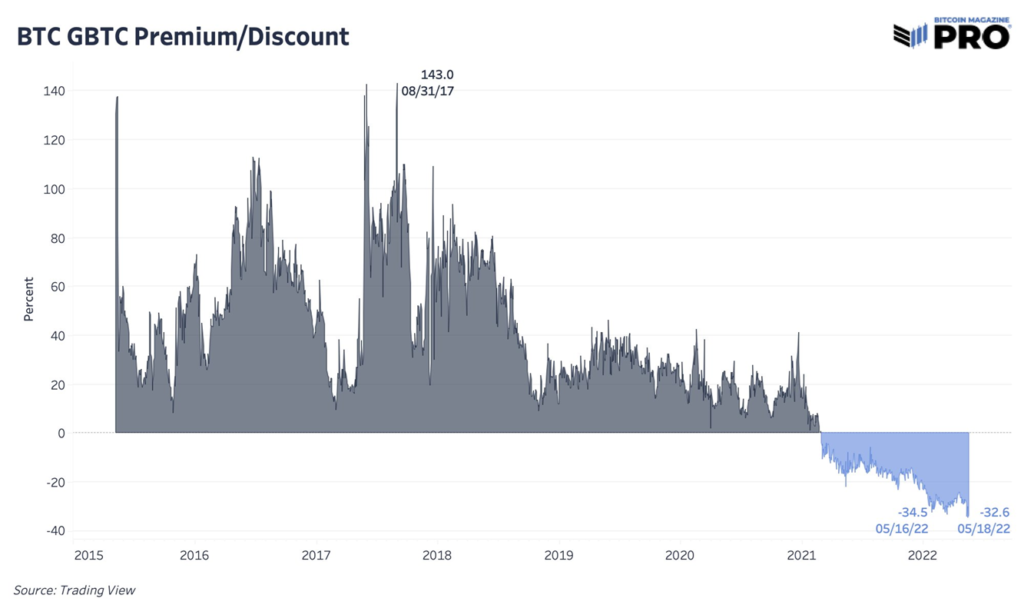

Lowstrife flagged risks for Strategy from the rising number of corporates adopting a bitcoin strategy. He drew parallels with Grayscale’s GBTC, which lost its uniqueness after spot ETFs launched. The share premium vanished, as did demand, along with a drubbing for mNAV.

The expert reiterated that mNAV is entirely sentiment-driven. There is no mechanism or reason forcing it to match asset value.

He noted the risk of the metric compressing below 1, shrinking scope for capital raising and new coin purchases. The need to pay dividends in adverse markets could make matters worse.

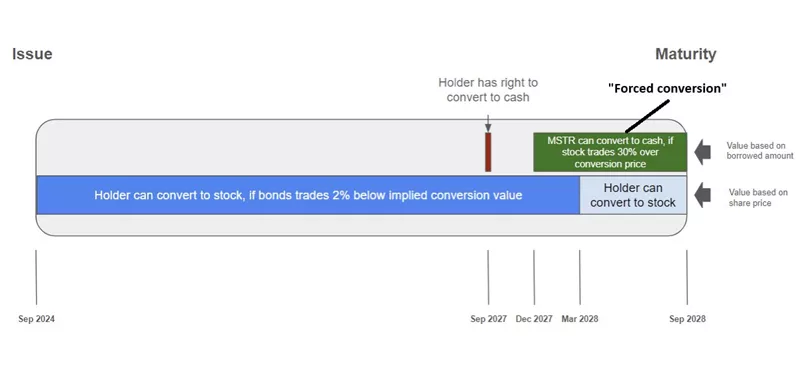

The picture is complicated by $8.2bn of convertible bonds maturing in 2028–2032. If the common stock price fails to reach conversion levels, Strategy will have to refinance or repay by selling coins.

“This is not a revolution. It’s financial pyramids chasing leverage. I’m a HODLer. It makes me really sad to see [Michael Saylor] recycling the financial engineering of 2008 which led to the creation of digital gold,” Lowstrife concluded.

Jess Myers of Moon has forecast that the share of bitcoin on public companies’ balance sheets could rise to 50% by 2045.

According to Bitwise, by end-2026 institutional holders, including governments and corporates, will control 20% of total supply (~4.2m BTC).

Earlier, Bernstein predicted corporate bitcoin reserves would climb to $330bn by 2029.