Key Highlights

- Trading volume on centralized exchanges fell 25%, marking a low not seen since late 2020.

- Dogecoin surged after Elon Musk’s Twitter purchase.

- Over the month, MEV-Boost relays censored 90% of Ethereum blocks passing through them.

- In October, the total TVL of the liquid staking segment rose by 39%.

- Many on-chain metrics signalled a market-cycle bottom.

- The Foundry USA pool’s share of Bitcoin’s hashrate reached 25.9%.

- Since the start of the year, Bitcoin mining difficulty rose by more than 50%, placing miners on the brink of unprofitability.

- Stablecoin market capitalization fell to $145 billion, a level not seen since late 2021.

Performance of Leading Assets

- In October Bitcoin managed to break out of a prolonged consolidation and test the $21,000 level. The Ethereum price exceeded $1,650, significantly outpacing Bitcoin’s momentum.

- For the month, Bitcoin rose 5.56%, while Ethereum climbed 18.4%.

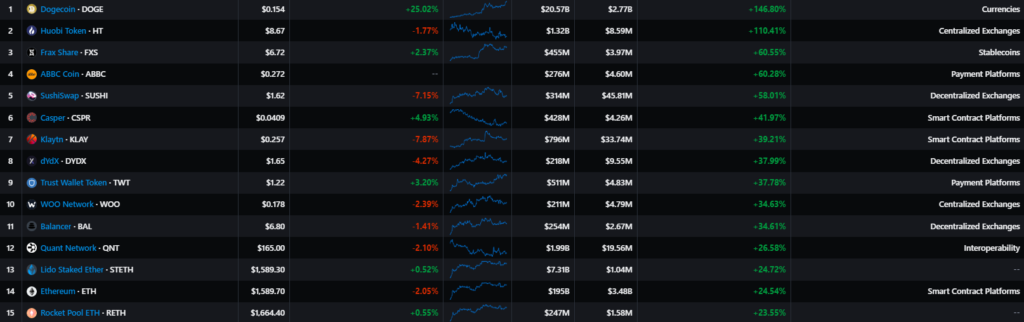

- The best performers among mid-cap assets were meme crypto Dogecoin (DOGE) and exchange token Huobi Token (HT). DOGE rose by more than 140%, helped by Elon Musk’s Twitter purchase. Investors seem to expect future crypto integrations into the social network, while Musk continues to raise the audience. HT surged 110% after leadership changes at Huobi — in October Justin Sun, founder of TRON, joined the advisory council and immediately foreshadowed activities with HT, partnerships and a rebrand.

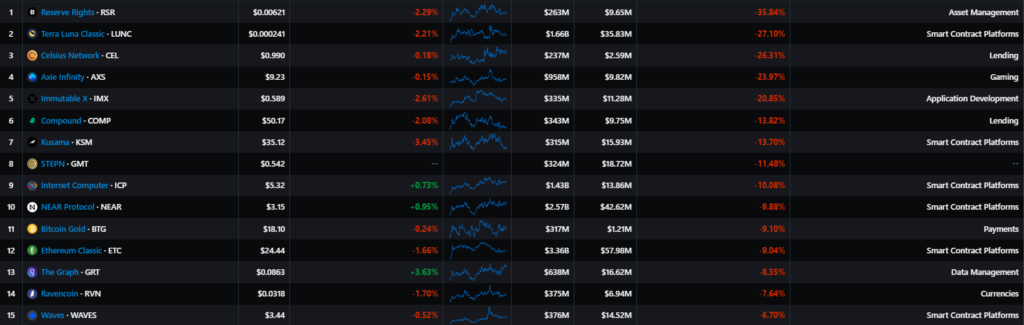

- Luna Classic (LUNC), Celsius Network (CEL) and Axie Infinity (AXS) were among the month’s laggards. In October, Binance launched a burn of 1.2% of fees in LUNC/BUSD and LUNC/USDT, but the effect was modest in scale and did not impact LUNC prices. The exchange later reduced the burn to 0.2%.

- Another underperformer was Celsius Network’s CEL token. The main trigger was clarity on the timing of the auction for selling bankrupt assets. The drop in Axie Infinity (AXS) quotes was driven by the unlocking of more than 21 million tokens among early investors and project advisers.

Crypto-Linked Stocks

Mining Stocks

Stocks linked to crypto performed broadly mixed. Some market-positive signs supported MicroStrategy due to the large reserve of cryptocurrency on the balance sheet. At the same time miners faced difficulties amid a stagnant market, higher energy costs and a fall in hashrate. Core Scientific’s cash reserves and equivalents are likely to run out by the end of 2022.

Macroeconomic Backdrop

- The new government under Rishi Sunak announced a plan to cut the budget deficit, discarding the initiatives of former prime minister Liz Truss. Yields on 10-year UK gilts fell to 3.5%, easing pressure on risk assets.

- Senate Banking Committee Chair Sherrod Brown urged Fed Chair the Fed to avoid a sharp rise in unemployment amid tighter policy. The head of the San Francisco Fed, Mary Daly, said debates on lowering the pace of rate hikes were warranted.

- US consumer price growth in September slowed from 8.3% to 8.2%, but the core rate rose against expectations—from 6.3% to 6.6%.

- According to the CME FedWatch tool, at the upcoming November 2 meeting the Fed is priced in to raise by 75 bps (88.7%), with December expectations split between 50 bps (52.5%) or another 75 bps (46.8%).

- Despite disappointing reports from some tech giants, equities and the crypto market have turned positive in anticipation of signals from the Fed regarding the peak of rate hikes.

Market Sentiment, Correlations and Volatility

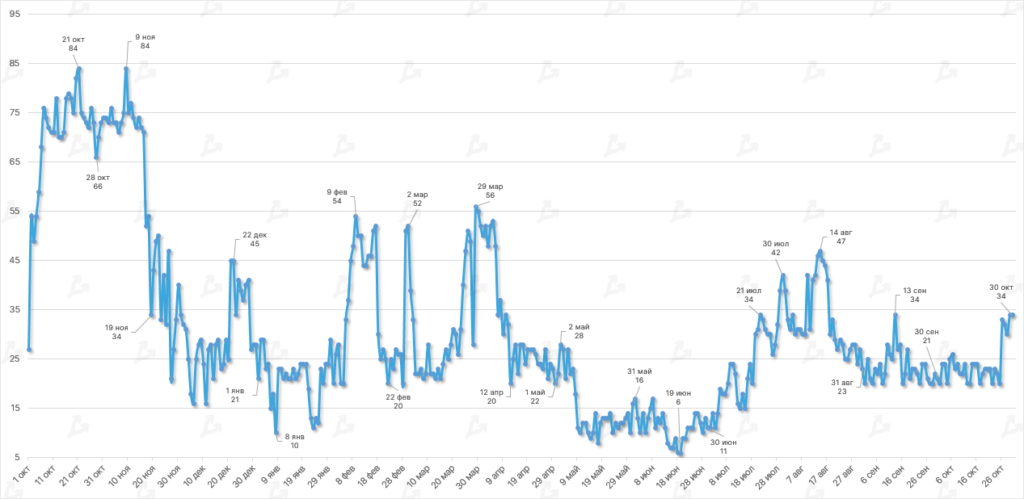

- Nearly the entire October was spent in the “extreme fear” zone for the Fear & Greed Index; only at month end did it edge out of that range. The average reading was 24.4 (23.2 in September).

- The unstable macroeconomic and geopolitical backdrop continues to weigh on investors, who fear putting money into high-risk assets.

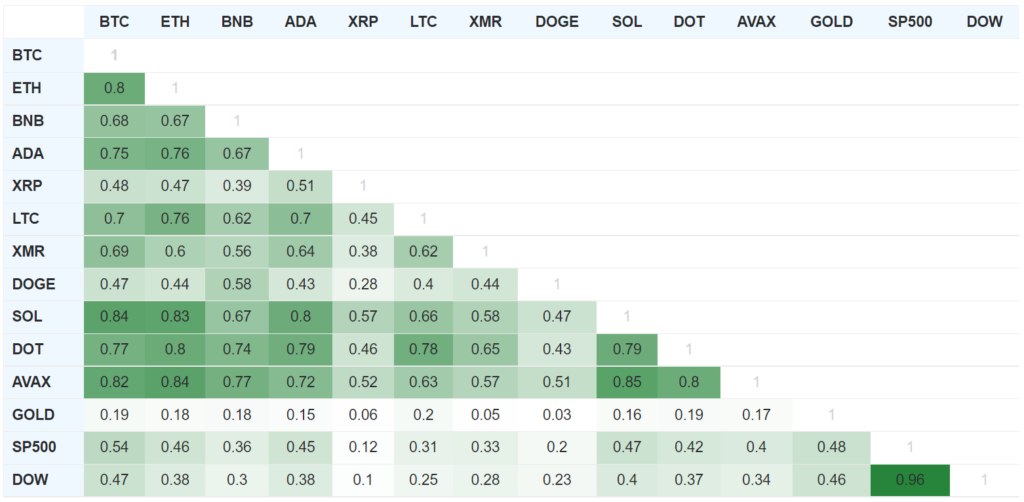

- In October, Bitcoin’s correlation with the US stock market weakened. The 90-day moving average stood at 0.54 for the S&P 500 and 0.47 for the Dow (0.61 and 0.59 in September respectively).

- Some analysts believe that Bitcoin will eventually break its link to traditional risk assets.

- Bitcoin’s correlation with gold also weakened after a three-month run (0.19 versus 0.27 in September). In Q3 2022 the asset posted the best performance versus precious metals.

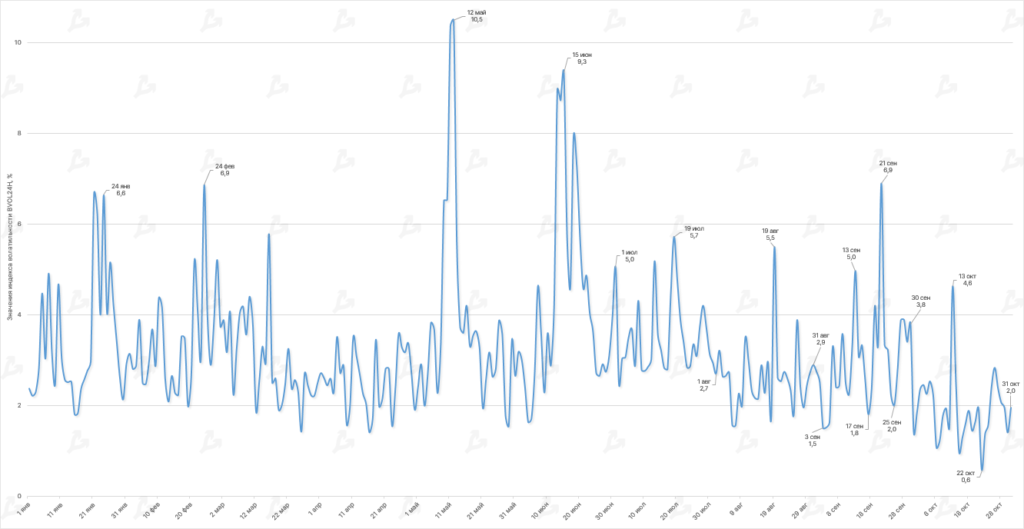

- In October, the average BVOL24H reading was 1.9%, below September’s 3%.

- The maximum reading was 4.6% — the extreme occurred on October 13, when, amid US inflation data, Bitcoin prices dropped below $18,200.

On-Chain Data

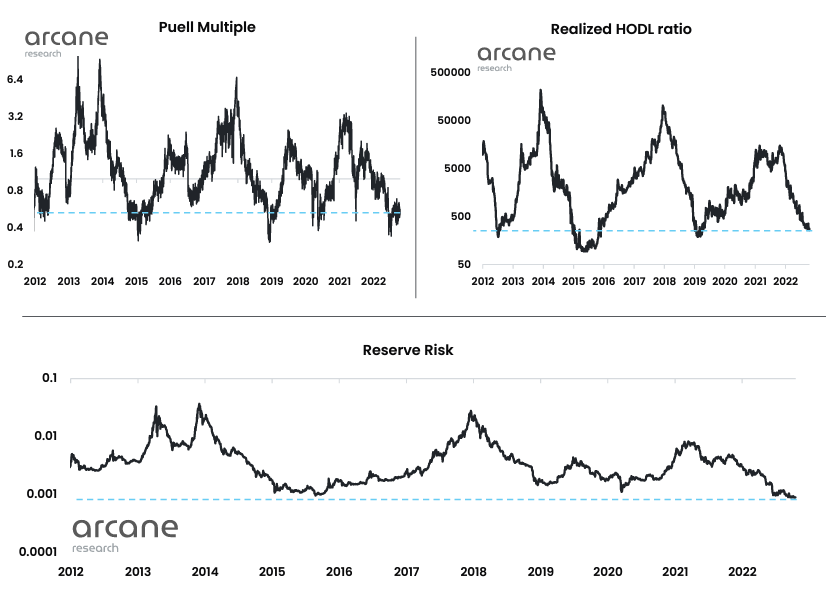

- Most on-chain metrics, including Puell’s multiplier, RHODL Ratio and Reserve Risk, signal deep Bitcoin oversold conditions and a likely bottom in the bear market. However some indicators suggest a risk of a renewed redistribution wave and price consolidation in the $16,500–$21,100 range.

- MVRV indicates that Bitcoin’s realized cap is higher than its market cap. Earlier, similarly low readings coincided with bear-market lows.

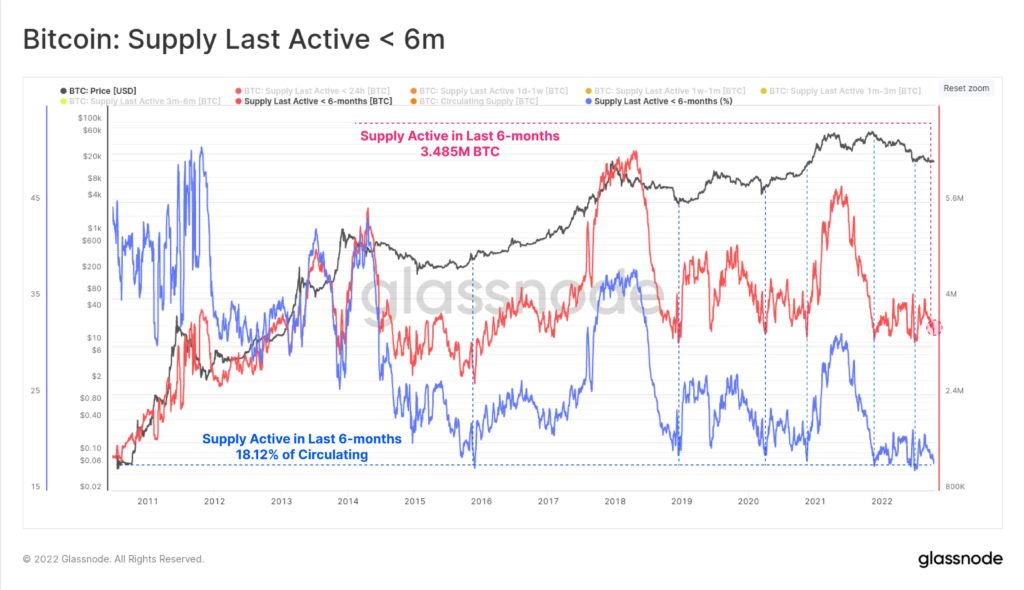

- Total lost Bitcoins and hodlers’ coins on long-term wallets reached a five-year high. This implies dwindling active supply and could bode well for price if demand remains firm or rises.

- Unspent supply of Bitcoin on idle addresses touched a record threshold around 18%. Glassnode analysts highlighted that such low numbers tend to occur after long bear markets.

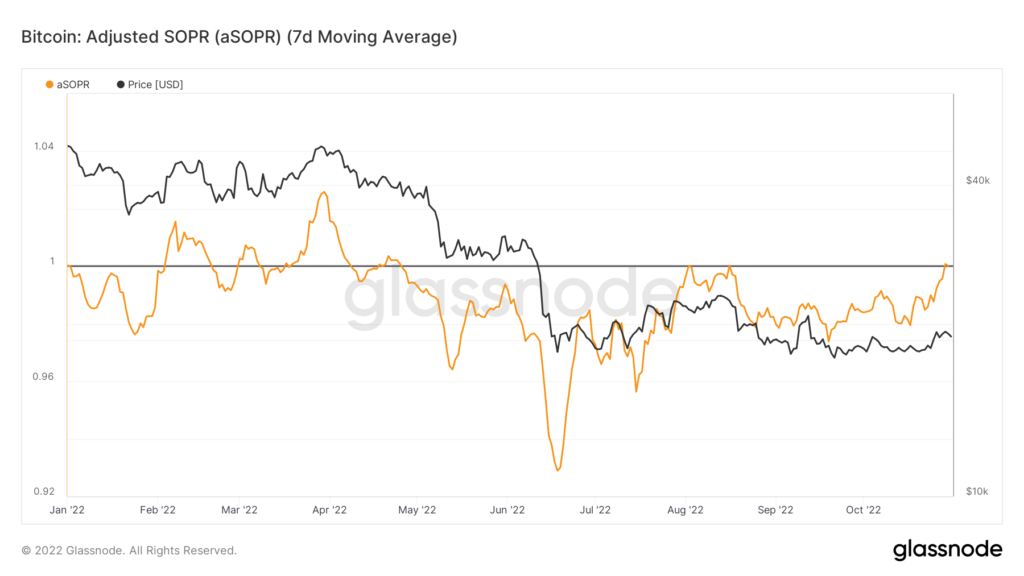

- aSOPR rose above 1 for the first time since August amid market revival and increased volatility. Previously, price declines diverged from rising indicator values, suggesting seller exhaustion.

- Inactive Bitcoin supply on idle addresses remained at historically low levels around 18%. Glassnode analysts highlighted that such lows tend to coincide with bear market bottoms.

- aSOPR rose above 1 for the first time since August amid market revival and rising volatility. Previously, price declines diverged from rising indicator values, suggesting seller exhaustion.

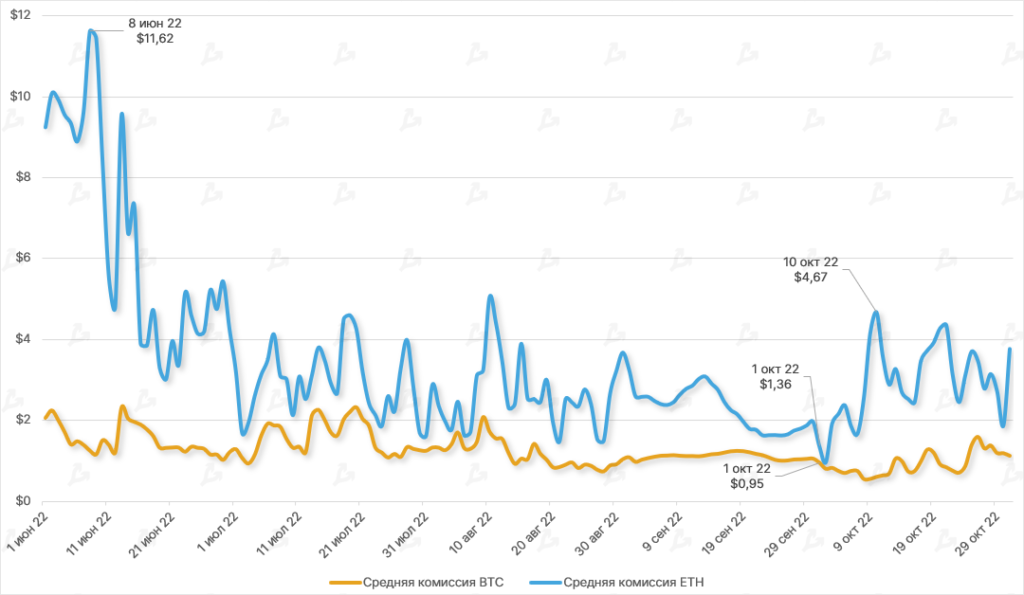

- In October, the average BTC transaction fee mostly stayed below $1; in the second half of the month it rose, reaching $1.59 as on-chain activity picked up with Bitcoin breaking above $20,000.

- The average Ethereum transaction fee at the start of the month reached $4.67, matching August levels. It later declined. The relatively low fees on Ethereum signal subdued DeFi activity and a downturn in the NFT space.

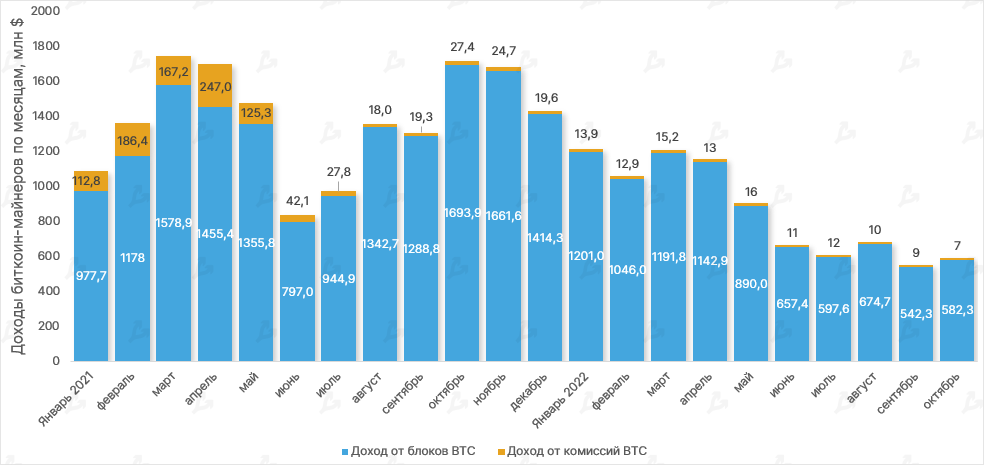

- Total Bitcoin miner revenue for the month rose 7% to $589.7 million. The share of fees in revenue fell to 1.28%, amounting to just $7 million.

Trading Volume

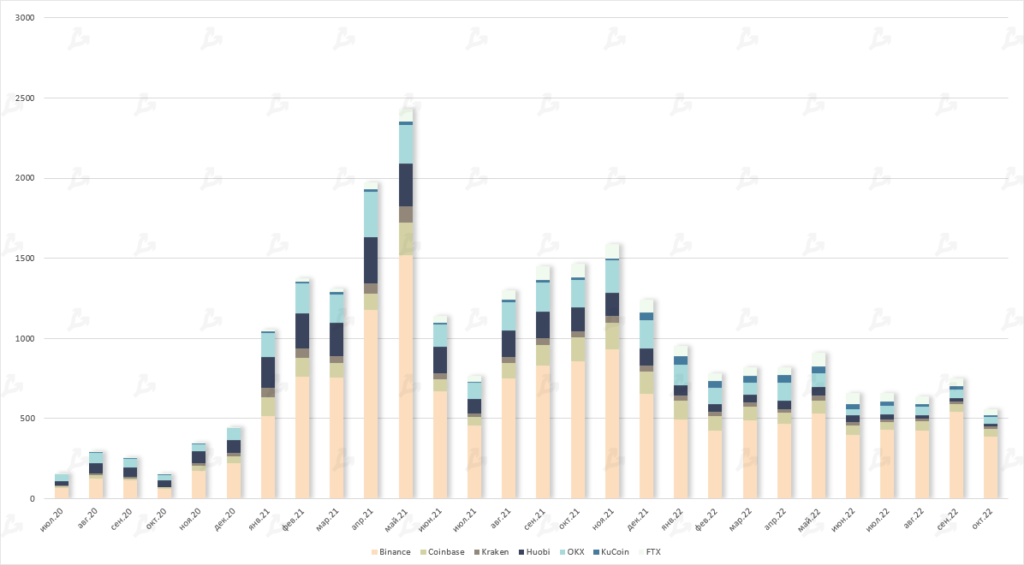

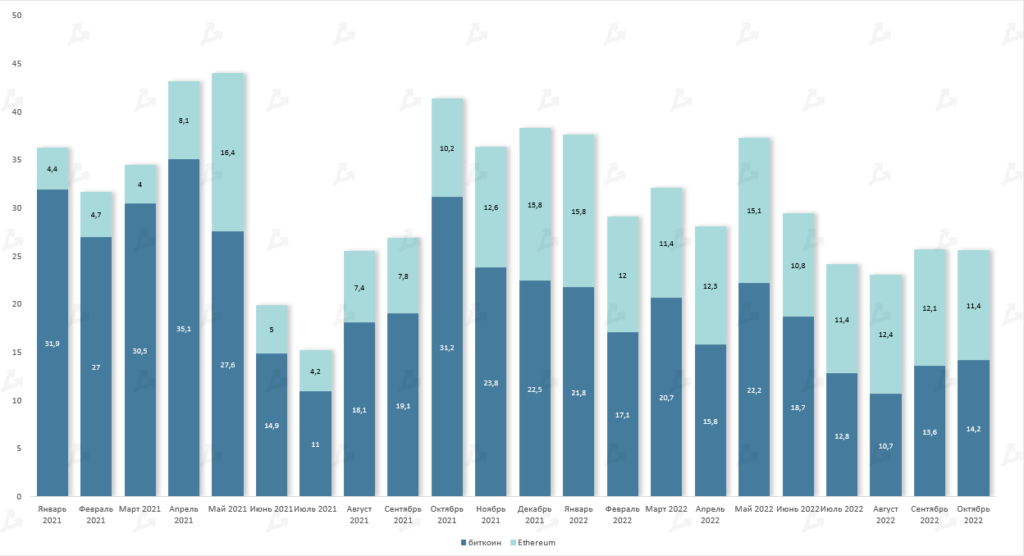

- October spot trading volume on ForkLog-tracked platforms fell 25% to $558 billion.

- All platforms posted lower volumes, but Coinbase saw only a modest decline — from $47 billion to $48 billion in September. Binance volumes dropped from $541 billion to $390 billion, FTX from $52 billion to $36 billion.

- As a result, overall trading volume on crypto exchanges reached a multi-year low not seen since December 2020.

Futures and Options

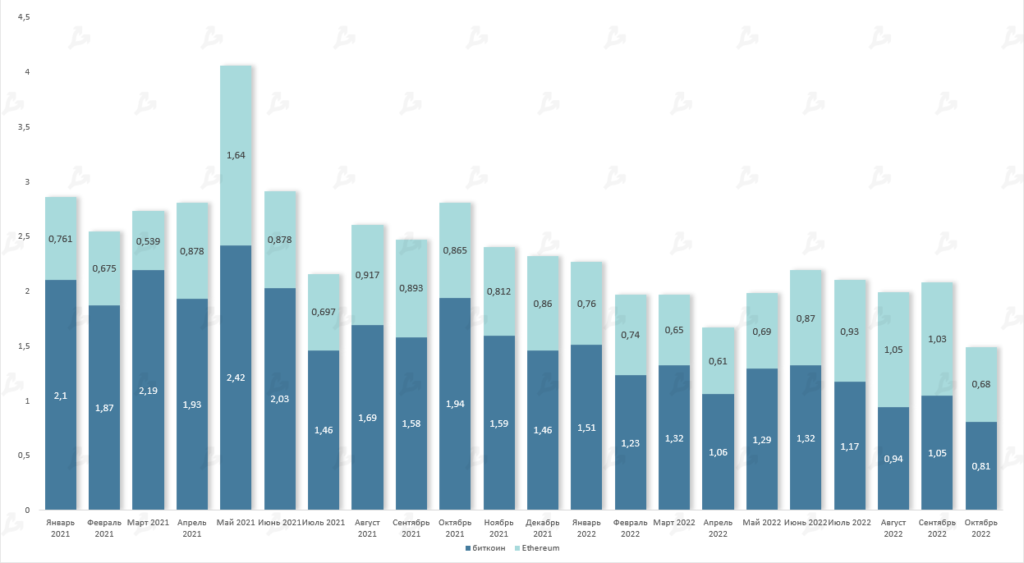

- October saw a clear contraction in futures trading volumes on Bitcoin and Ethereum—total platform activity was the lowest since November 2020 ($810 billion and $680 billion, respectively).

- Options volumes held relatively steadier.

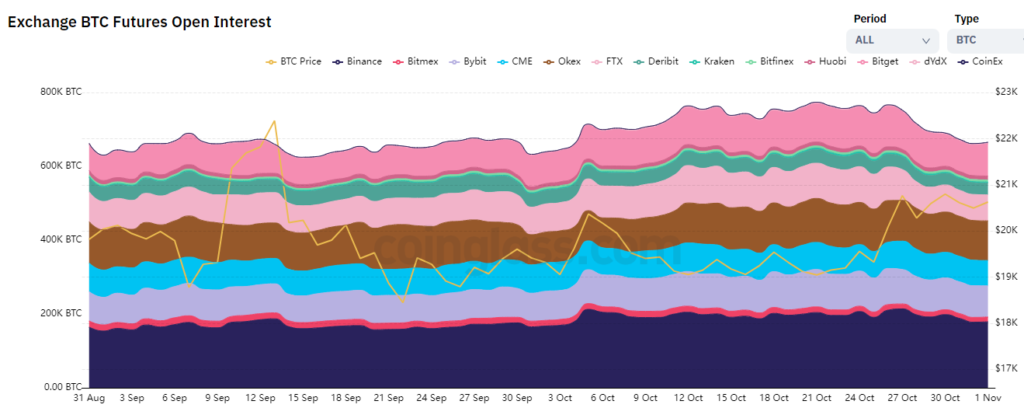

- After hitting a peak in September, open interest on futures began to retreat. Throughout October, total open positions fell by around 100,000 BTC.

DeFi

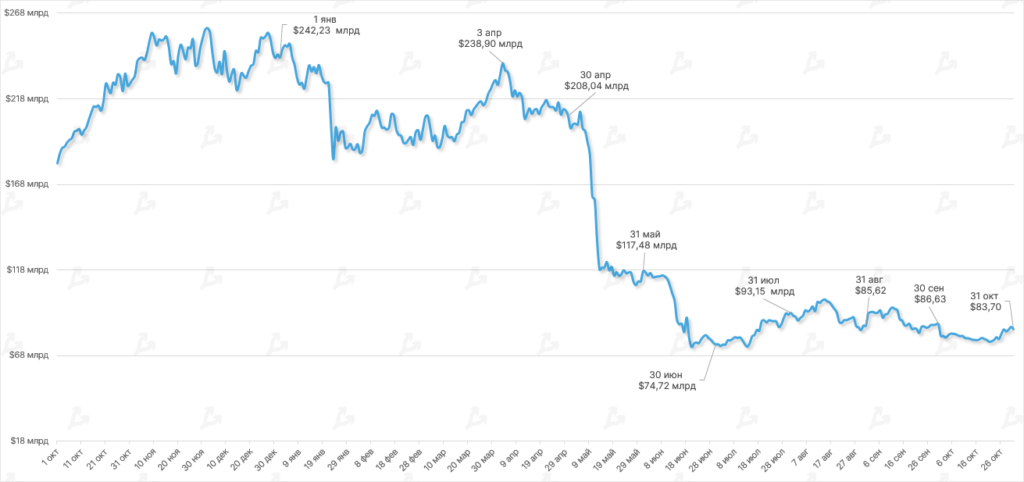

- In October, the TVL of DeFi apps fell 3%, to $83.70 billion.

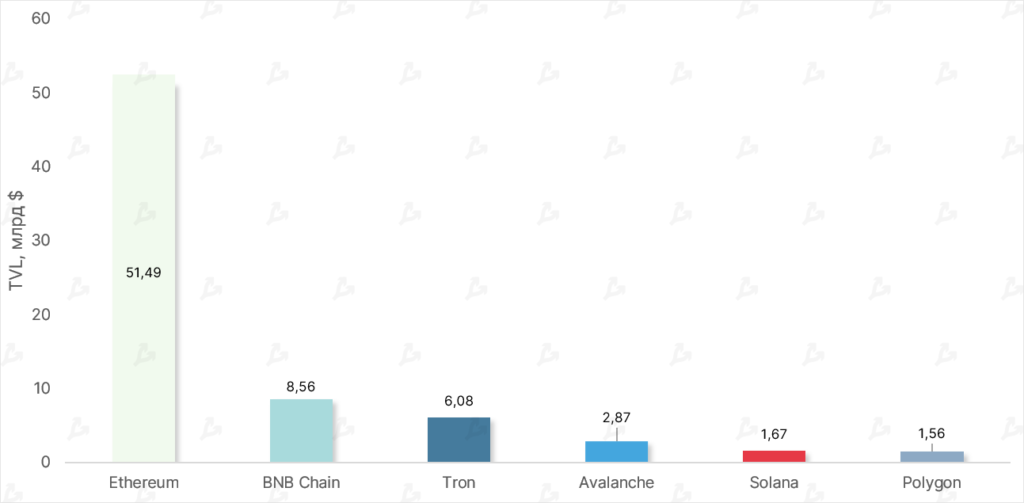

- The leading ecosystem by blocked funds remained Ethereum, up $3.76 billion. Ethereum accounted for more than 61% of total TVL ($51.49 billion). The move was driven by a rise in ETH prices and growing interest in staking.

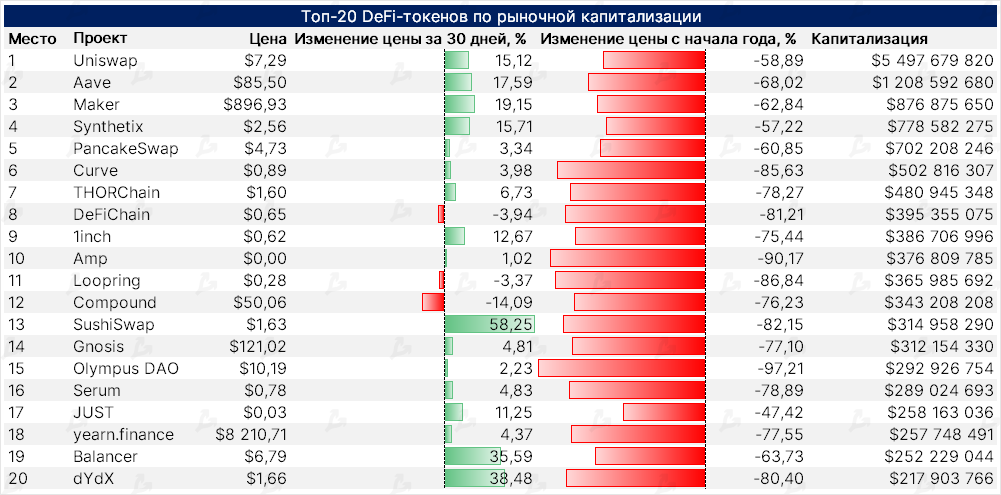

- By October, almost all top-20 DeFi tokens by market cap were green. Exceptions: COMP (-14.09%), DeFiChain (-3.94%), Loopring (-3.37%).

- The price decline for COMP may be linked to the community’s decision to delist low-liquidity assets.

- The strongest performer was SushiSwap’s governance token — up 58.25%. The rally was aided by news that GoldenTree Asset Management bought SUSHI; GoldenTree manages assets worth about $47 billion.

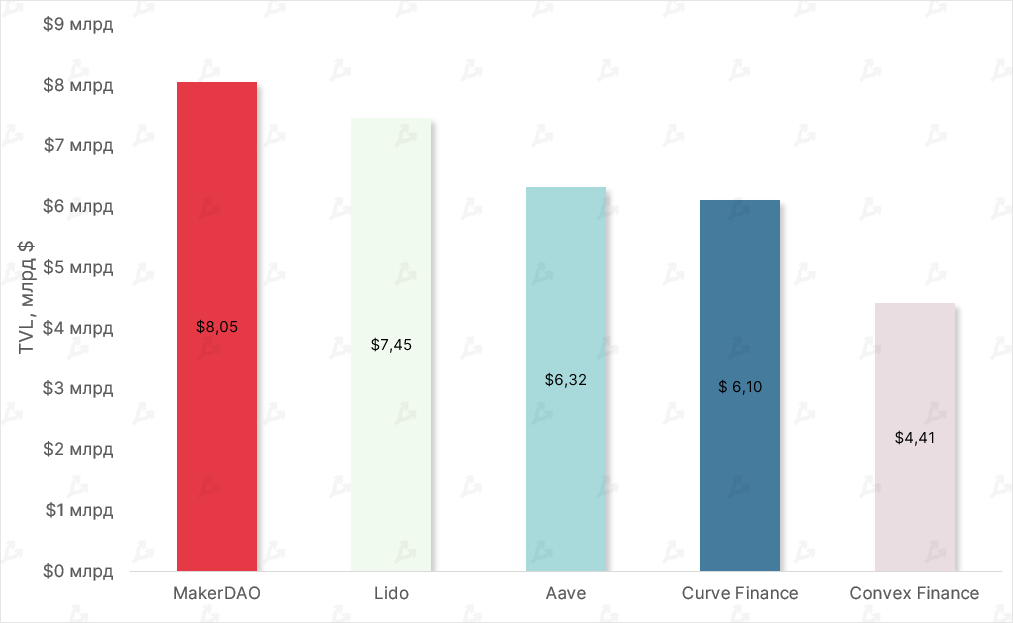

- Within Ethereum projects, MakerDAO led TVL at $8.05 billion, with Lido second at $7.45 billion. Since The Merge, demand for applications in this segment has risen.

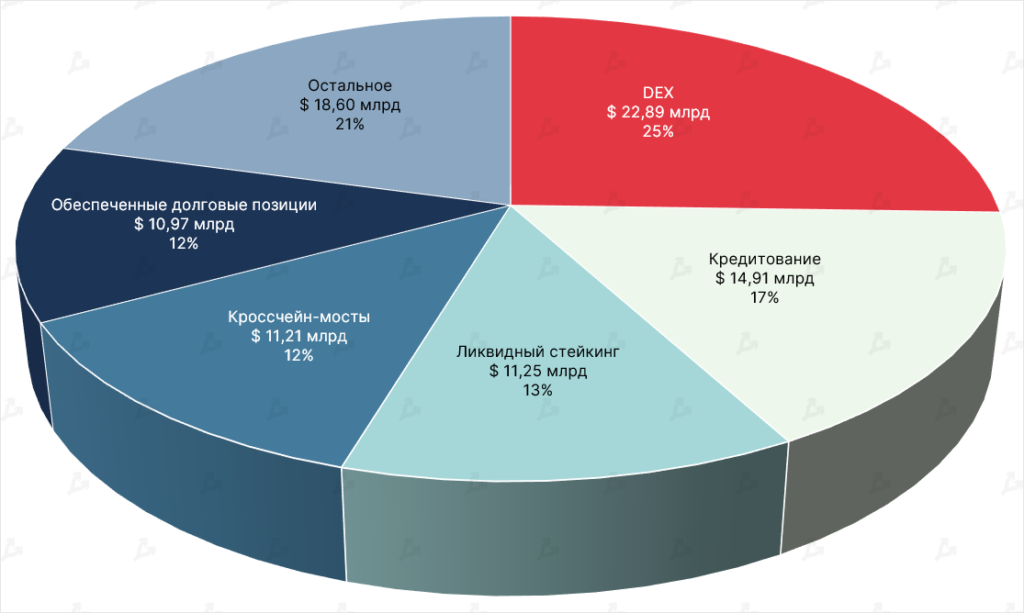

- Decoded decentralized exchanges remain dominant within DeFi TVL — they account for more than 27% of the sector or $22.83 billion.

- Second place goes to lending protocols ($14.91 billion), followed by liquid staking services. Over October, TVL for the latter rose by 39%.

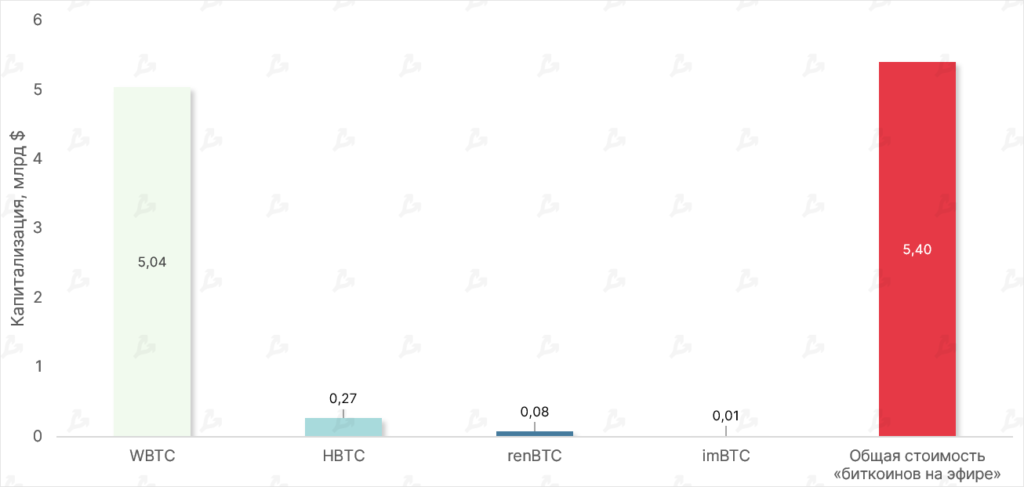

- By month’s end, the combined market cap of “Bitcoin on Ethereum” assets fell to $5.4 billion. The WBTC dominance index rose to 93%.

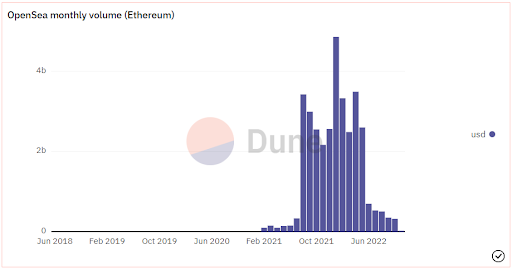

- In October, OpenSea’s NFT market trading volume fell for five straight months, totaling $319.25 million (232,985 ETH).

- Meanwhile, some projects gained traction. NFT collections Art Blocks (+101%), Azuki (+76%) and Gods Unchained (+50%) posted notable gains.

- Reddit’s NFT sell-through exceeded $9 million.

- There was a marked rise in NFT sales volume on Immutable X and Polygon networks.

Activity of Major Players

- Tesla, in its Q3 report, said it continues to hold Bitcoin on its balance sheet valued at $218 million. Market participants saw this as a positive signal given Tesla’s stance on cash crypto hoards).

- Marathon Digital Holdings, for September, mined 616 BTC and increased its crypto reserves to 10,670 BTC. Bitcoin Treasuries shows Marathon’s holdings at 10,055 BTC, up 3.44% versus Tesla.

- Other miners’ digital reserves have remained steady, underscoring confidence in Bitcoin’s mid- to long-term prospects.

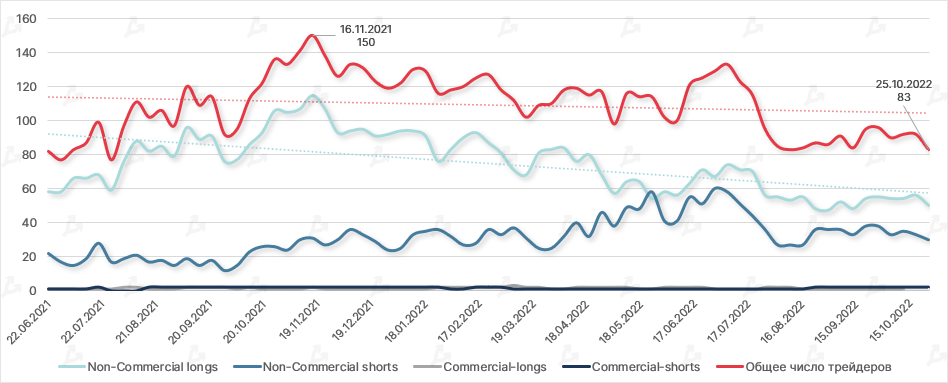

- Open interest (OI) on Bitcoin futures rose modestly for the month—by 4%. Overall, the metric shows an upward trend and a gradual return to year-ago levels.

- Longs vs. shorts among hedge funds and other big players (Non-Commercial) were roughly balanced. Among smaller traders (Nonreportable) long positions slightly prevailed.

- Among institutional players (Commercial), shorts were dominant, but the gap with longs is narrowing.

- OI in microfutures on Bitcoin remained broadly unchanged since March, currently below its peak at the end of October 2021 by about 63%.

- Over the year, the number of traders in these relatively new instruments declined sharply — down 45%. With a market revival, the indicators above may resume growth.

- In terms of long vs. short positions among market participants, the picture is broadly similar to Bitcoin futures. The notable difference is that among institutional players longs are still heavily outweighed by shorts.

$165m

Uniswap, a decentralised exchange, in a Series B round led by Polychain Capital.

$150m

BlockTower Capital for a Web3-focused venture fund.

$55m

Celestia Foundation backing the development of modular blockchains. Funds will support launches and partnerships.

$41.5m

Tatum, a platform for building blockchain apps. Round led by Evolution Equity Partners.

$40m

Golden, a Web3 data transfer protocol, with Andreessen Horowitz as lead investor.

$40m

Horizon Blockchain Games, behind Skyweaver, following Series A.

Regulation