In 2021, Bitcoin and Ethereum prices hit new highs, and market capitalization surpassed $3 billion for the first time.

The industry has matured — in the US a Bitcoin futures ETF was launched, Coinbase went public, and publicly traded companies increased their crypto reserves.

Notably, venture investment activity is a key indicator. The volume and structure speak to market participants’ interest in the industry and the prospects for the development of individual segments.

Guided by Galaxy Digital Research and The Block Research, ForkLog studied venture capital activity in 2021.

Key highlights

- In 2021, venture capitalists invested a record $33 billion in the crypto- and blockchain industry.

- Compared with 2020, venture financing volume rose 700%. A similar rise was recorded in the M&A deal flow.

- The total amount of funds raised by startups in Series B rounds and later-stage financing amounted to $13.6 billion.

- In 2021, 40 companies with valuations of $1 billion or more emerged.

Unprecedented harvest

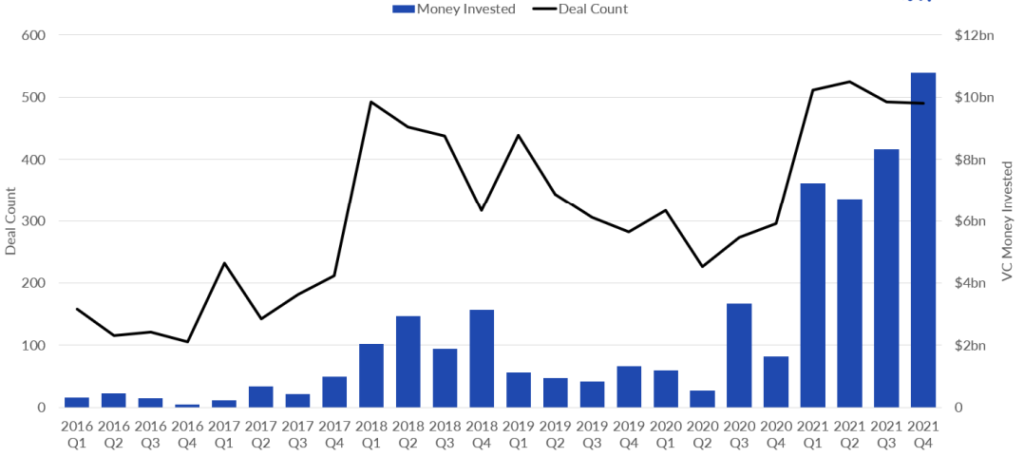

In 2021, the volume of venture investments in crypto- and blockchain-startups surpassed $33 billion, according to Galaxy Digital Research. This is more than the total for all previous years.

As the chart below shows, in the last three months of 2021 alone, new and increasingly mature projects attracted $10.5 billion.

The share of crypto- and blockchain-sectors in global venture investment volume last year stood at 4.7%.

2021 was also a record year for the number of deals — 2018. This was almost twice as high as in 2020 and about 18% higher than in 2019 (1698).

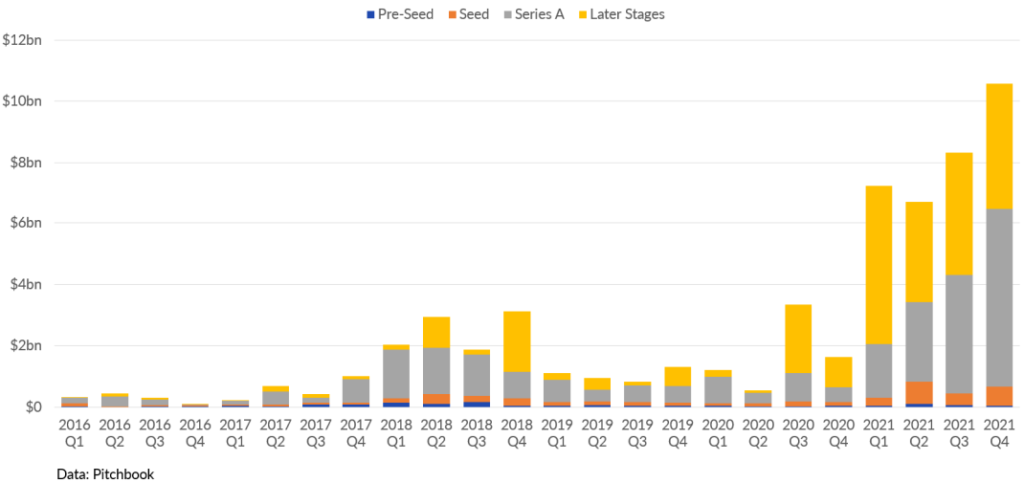

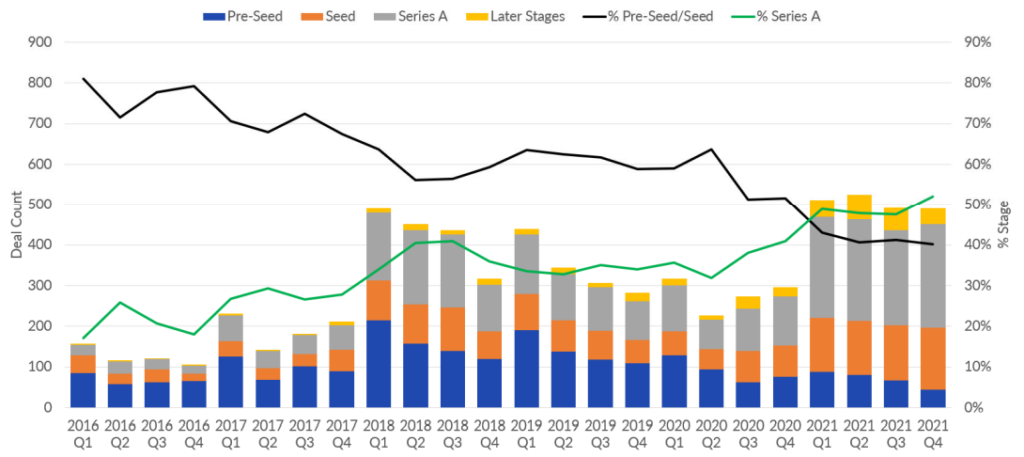

In Q4, the largest share of venture capital (more than 60%) went to Series A rounds. This indicates that relatively recently created projects have matured and developments attract investors willing to put substantial sums into promising technologies.

In 2021, significant capital was also invested in later-stage projects, reflecting industry maturation and the growing number of companies generating steady revenues.

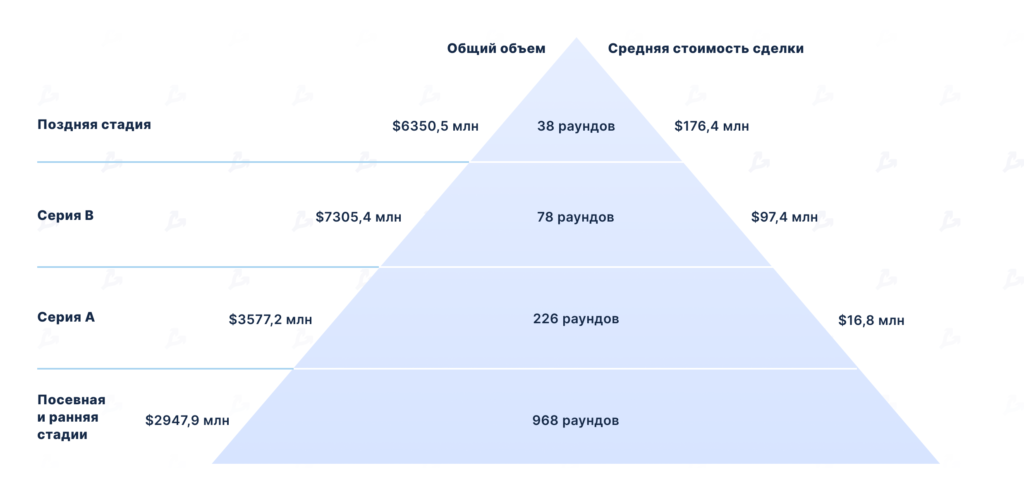

The largest financing volume was raised in Series B rounds: after 78 deals, companies raised more than $7.3 billion — the average round size was $97.4 million. The corresponding figures for later rounds stood at $6.35 billion and $176.4 million, according to The Block Research.

In 2020 there were only 4 deals above $100 million. In 2021 there were 69 such deals. A similar rise was recorded for deals in the $50–$100 million range: 4 in 2020 and 56 in 2021.

The aggregate capital raised through deals over $100 million totaled $22 billion, representing 67% of the total crypto- and blockchain-startup investments for the year.

In the next chart, the number of Series A deals rose sharply in 2021, while pre-seed rounds declined. Seed rounds, by contrast, rose markedly.

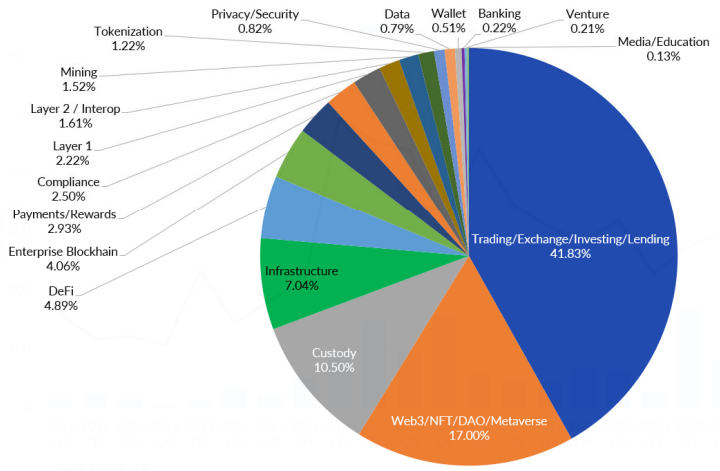

Despite a boom in NFT, Web3 and metaverse sectors, the largest share of capital (41.83% or $13.8 billion) went into more traditional, time-tested sectors — trading and investment platforms, and crypto-lending services.

Notable deals include:

- Circle — $440 million from FTX, Digital Currency Group, Fidelity Management, Valor Capital Group and other venture firms;

- MoonPay — $555 million following a Series A round;

- Crypto-lending startup Eco — $60 million.

The past year also marked rising institutionalization — crypto-finance firms attracted multi-million-dollar investments to build solutions for large market participants.

For example:

- Fireblocks — $310 million with a $2 billion valuation;

- Paxos — $300 million with a $2.4 billion valuation;

- NYDIG — $100 million, and later — $200 million;

- Amber Group — $100 million with a $1 billion valuation;

- Bitwise — $70 million with a $500 million valuation;

- Custodian Copper — $50 million.

Despite heightened regulator scrutiny of crypto lending, investors continued to fund this segment.

In March, centralized crypto-lending platform BlockFi closed a Series D round of $350 million. The company filed with the SEC to launch a spot Bitcoin ETF and announced plans to roll out institutional crypto products in partnership with Neuberger Berman.

Celsius Network raised $750 million in a Series B round. The firm was valued at $3.25 billion.

The round followed allegations in the United States that the platform sold unregistered securities. The company faced inquiries from state regulators in Texas, New Jersey, Alabama and Kentucky.

The Canadian crypto-lending platform Ledn raised $70 million in a Series B at a $540 million valuation.

Significant investments also flowed into trading and brokerage platforms — 118 companies raised a total of $4.5 billion, according to The Block Research.

In July, the crypto-derivatives exchange FTX raised a record at the time $900 million in a Series B. Investors valued the company at $18 billion. In October, FTX closed a Series B-1 round for $420.69 million, after which the company’s market valuation reached $25 billion.

The institution-focused New York Digital Investment Group (NYDIG) outpaced FTX. In December, the company attracted $1 billion at a $7 billion valuation.

In November, the U.S. exchange Gemini attracted $400 million at a $7.1 billion valuation.

Considerable investments also went to projects in developing regions, including Africa, Latin America, Southeast Asia and the Middle East.

For example, the Bitcoin exchange CoinDCX raised 6.7 billion rupees (about $90 million), becoming India’s first cryptocurrency unicorn.

The largest crypto exchange in Latin America, Bitso, raised $250 million in a Series C at a $2.2 billion valuation. BitOasis in the UAE raised $30 million in a Series B round.

Web3 and NFT gaining momentum

The share of projects in NFT, DAO, GameFi and metaverses in annual venture investment totalled 17% ($5.61 billion).

The share of the above segments in seed and pre-seed rounds in 2021 stood at 63%.

Investors are showing growing interest in Web3. Products in this area relate to digital identity, data governance, content monetization, data storage, etc.

In 2021, substantial investments also went to projects developing decentralized social networks. For example, the blockchain project DeSo (Decentralized Social) by BitClout creator Nadér Al-Naji raised $200 million. The funds came from Andreessen Horowitz (a16z), Sequoia, Coinbase Ventures, Winklevoss Capital, Polychain Capital, Pantera Capital, Blockchain.com Ventures, Reddit co-founder Alexis Ohanian and other notable investors.

Play-to-Earn games, also known as GameFi, gained substantial popularity. This was largely driven by the success of Axie Infinity from Sky Mavis.

For GameFi blockchain foundations, high throughput and low transaction costs are essential, often at the expense of decentralization. Axie Infinity initially ran on Ethereum’s mainnet, but due to scalability issues developers used the Ronin sidechain. The latter is characterized by near-instant and inexpensive transactions. In addition to layer-2 solutions, many GameFi projects rely on alternative L1s such as Binance Smart Chain and WAX, which also offer high throughput at much lower costs than Ethereum.

DeFi and multi-chain solutions

Decentralized finance was one of the main investment trends in 2020. Investor interest in the segment persisted — roughly a quarter of all rounds in 2021 related to this “financial lego.”

In 428 deals, DeFi projects raised a total of $1.9 billion. The average and median deal sizes were $5.4 million and $2.7 million respectively, according to The Block Research.

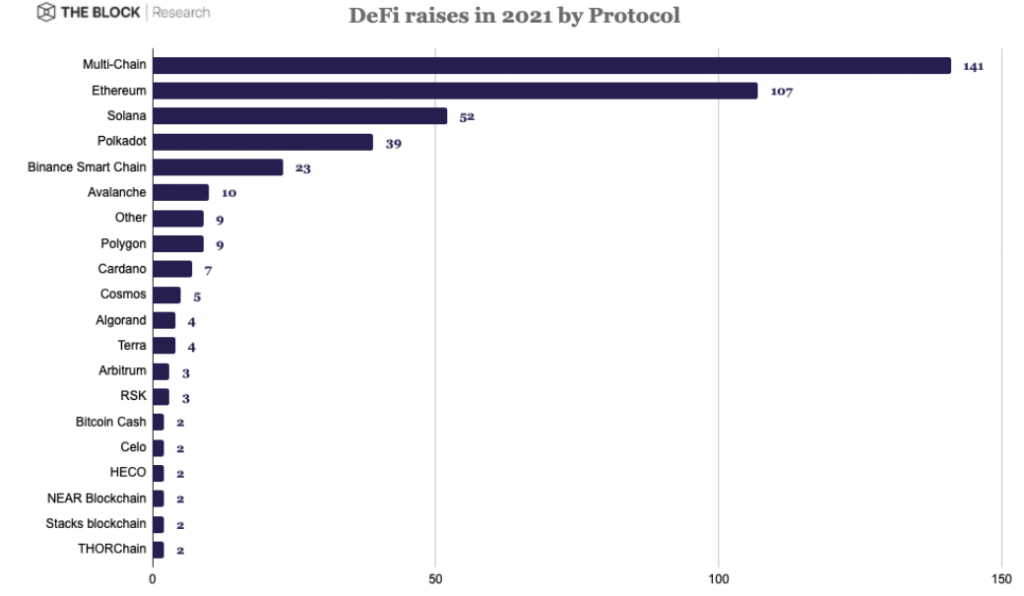

Investors most actively funded projects supporting various networks.

Ethereum remains the backbone of DeFi, but competition is tightening. Alternative chains such as Solana, Polkadot, Binance Smart Chain and Avalanche are becoming more popular.

There are more unicorns

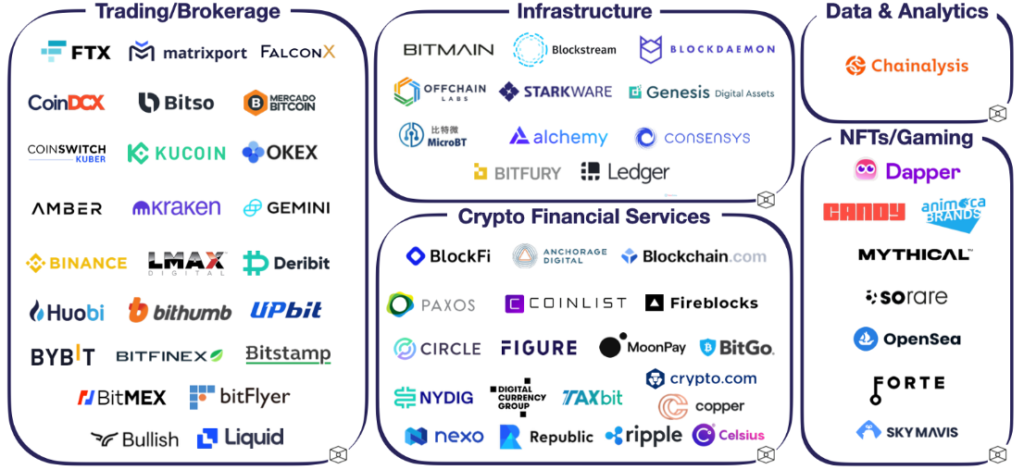

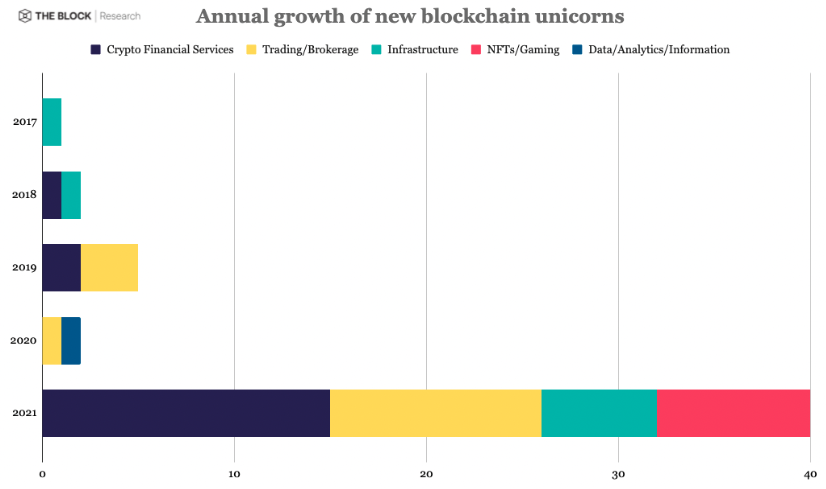

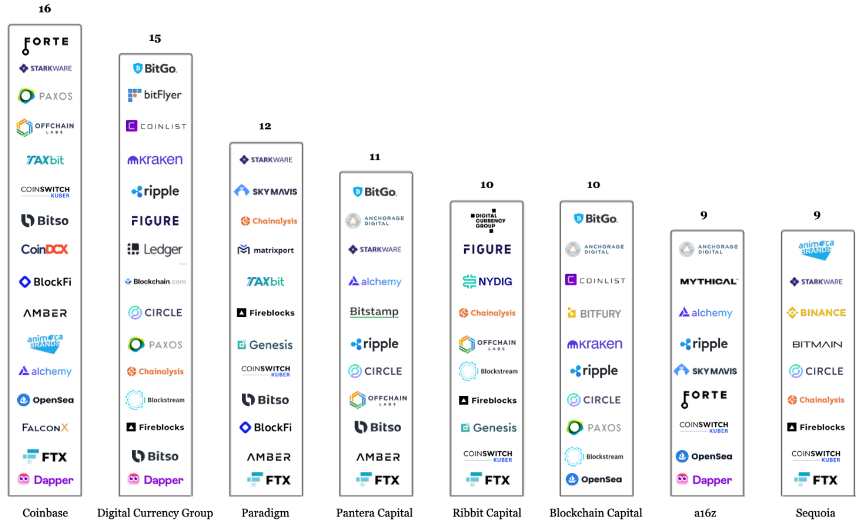

The increase in late-stage rounds has meant that at least 65 crypto- and blockchain-industry companies have unicorn status.

The image below features unicorns from various sectors with valuations of $1 billion or more.

In October 2019, Hurun counted only 11 unicorns in the crypto- and blockchain-industry. In the past two years, this figure has grown nearly sixfold — in 2021 alone, 40 companies achieved unicorn status.

Most unicorns lie in portfolios of Coinbase, Digital Currency Group and Paradigm.

Fourteen of the fifteen largest venture rounds occurred in 2021. The largest share of investments went to crypto-financial services (35.7%). The shares for the categories “Trading/Brokerage,” “Infrastructure,” and “NFT/Gaming” stand at 21.4% each.

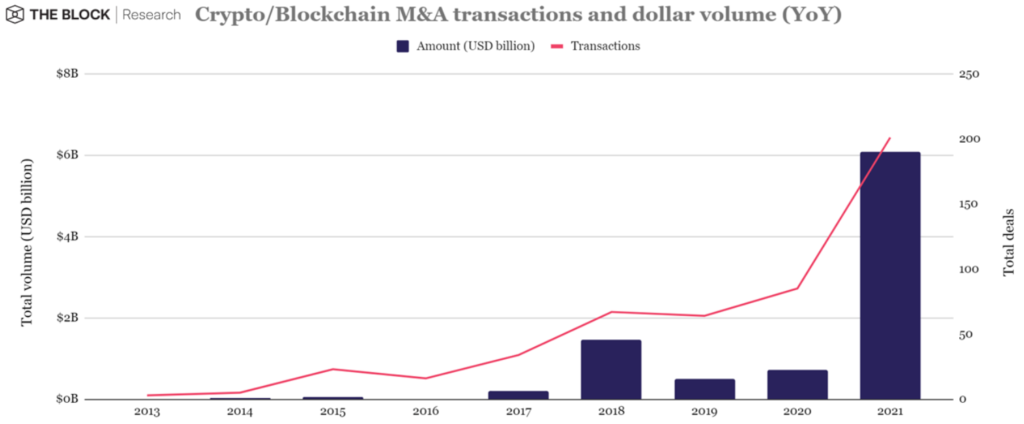

M&A activity surges

Compared with 2020, industry venture funding rose by 700%. A similar rise is observed in M&A deals.

Total M&A deal value last year exceeded $6 billion — more than in all previous eight years.

Deal count across M&A rose 131% year over year. Of the 15 largest M&A operations, 80% occurred last year.

The record-setting deal was Galaxy Digital’s purchase of BitGo, a crypto custodian, for $1.2 billion.

The second-largest operation of the year was Riot Blockchain’s acquisition of Whinstone US, a Bitcoin-mining infrastructure provider, for $651 million.

Coinbase led M&A activity. Last year the U.S. company acquired:

- RouteFire — an institutional-focused startup;

- Bison Trails — a provider of infrastructural blockchain solutions;

- Skew — an analytics platform;

- Zabo — an API provider for the digital-asset market;

- Agara — an AI startup;

- BRD — a Bitcoin-wallet operator.

Coinbase also announced the purchase of Israeli Unbound Security, a company specializing in secure storage for cryptocurrencies.

The portfolio suggests a focus on large players and the active building of related infrastructure.

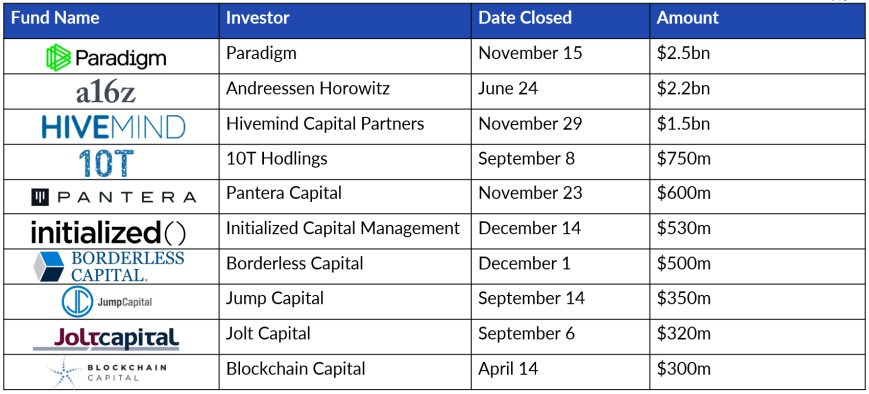

Funds have grown larger

The boom in the industry has also led to bigger funds focused on crypto- and blockchain development.

Last year, 49 such funds were created, with an average assets under management of about $300 million (a level nearly double that of 2020). According to Galaxy Digital Research, the number of venture firms reached 500 in 2021.

In November, Paradigm launched the largest venture fund. Its size was $2.5 billion, surpassing media expectations.

The size of Andreessen Horowitz’s (a16z) third fund reached $2.2 billion.

In November, Hivemind Capital Partners launched a $1.5 billion fund. The firm, led by former City executive Matt Zhang, will invest in crypto companies and will trade digital assets and pursue Play-to-Earn opportunities.

In September, the total assets under management at 10T Holdings for investing in rapidly growing crypto companies reached $750 million. In early December, led by Dan Tapiero, the firm filed with the SEC for a third fund of $500 million, focused on crypto startups at mid- to late-stage development.

Early 2022 was marked by the launch of FTX’s venture fund at $2 billion.

A broader picture

As noted, 2021 was a record year for the venture-capital sector.

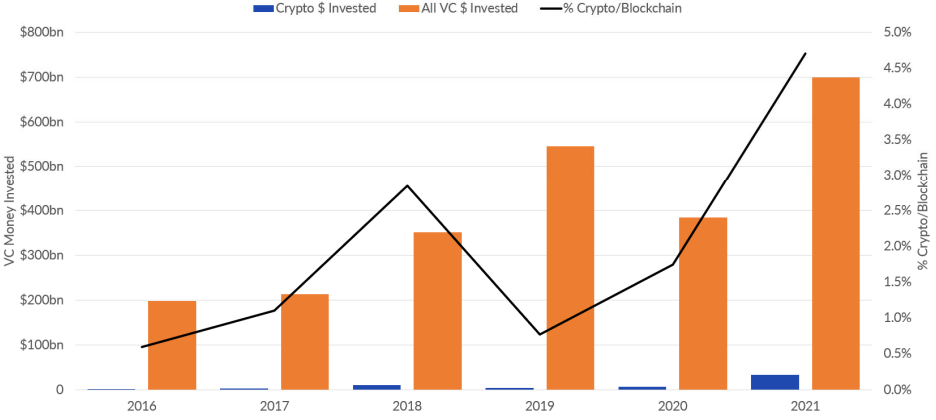

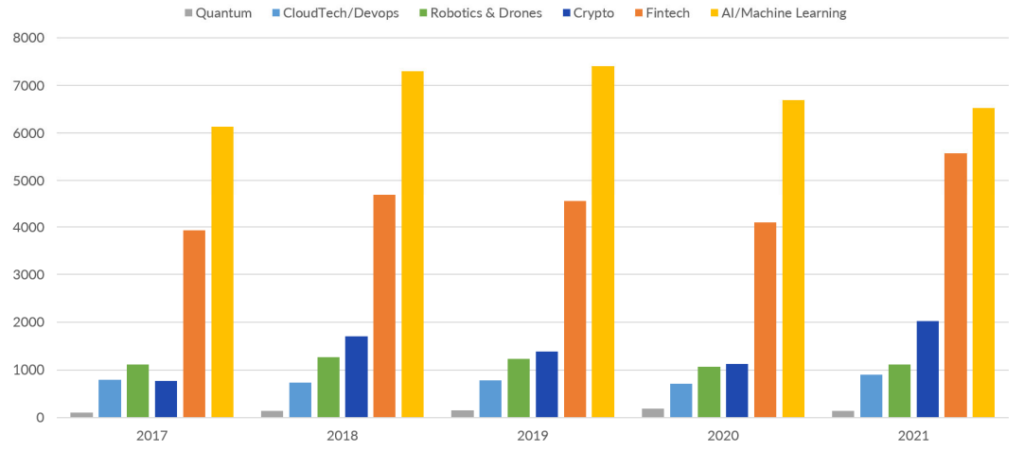

The share of investments in crypto- and blockchain-startups relative to AI, machine learning and traditional fintech remains small, but the figure is gradually rising.

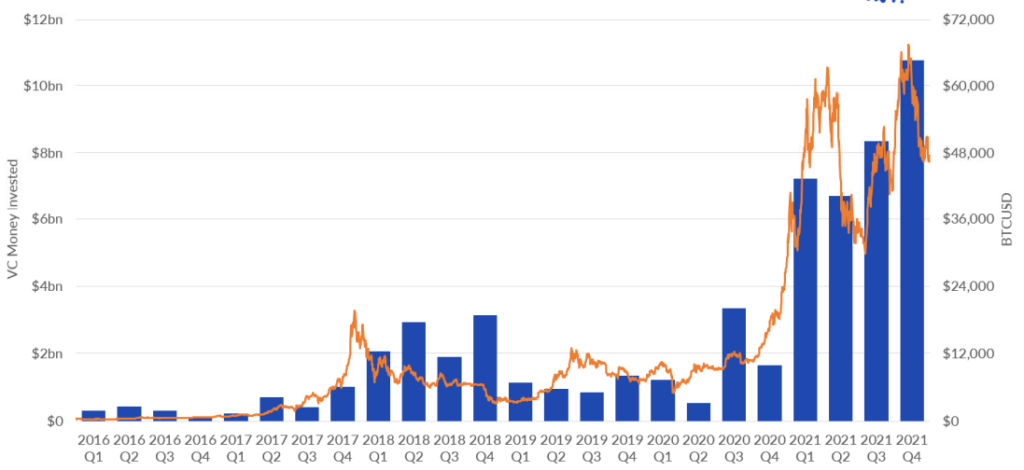

The chart below shows that Bitcoin’s price has closely tracked venture investment dynamics in the crypto- and blockchain industry.

In 2017 and 2018, there was a lag between price and venture investment volume. In subsequent years, this divergence subsided.

In 2021, a fairly tight linkage between the metrics was already evident. The correlation is likely to persist in the future.

Conclusions

In 2021, global venture investment reached a record $700 billion. Of this, more than $33 billion went to the crypto- and blockchain-industry — up 700% from the previous year.

The main catalysts for investor activity were rising valuations and market maturation.

Many projects born during the 2018–2019 bear market survived and attracted funding in new rounds. At least 69 companies secured funds above $100 million. In 2021 alone, 40 projects achieved unicorn status.

Other indicators of the industry’s maturation and rising appeal include:

- high valuations of crypto companies;

- emergence of new funds with multi-billion-dollar assets;

- growth in late-stage deal share;

- companies going public (Coinbase, Argo Group, Riot Blockchain, Marathon Digital Holdings);

- rising interest from crypto-friendly firms like Robinhood and PayPal;

- the trend of holding reserves in digital gold (MicroStrategy, Tesla, Square, El Salvador’s Bitcoin fund).

Venture investments are, in a sense, the fuel for the development of projects and the market as a whole. Given recent momentum, Web3, DAOs, metaverses and other directions are likely to be powerful growth drivers in the near term.

Subscribe to ForkLog news on Telegram: ForkLog Feed — the full news stream, ForkLog — the most important news, infographics and opinions.