The U.S. Securities and Exchange Commission (SEC) has issued a cease-and-desist order against the blockchain startup ShipChain. As part of the settlement of claims, the company will pay a $2 million fine.

The ShipChain platform was registered in Delaware and promised to increase transparency in shipping. It was part of the BITA transport blockchain alliance alongside FedEx and JD.com.

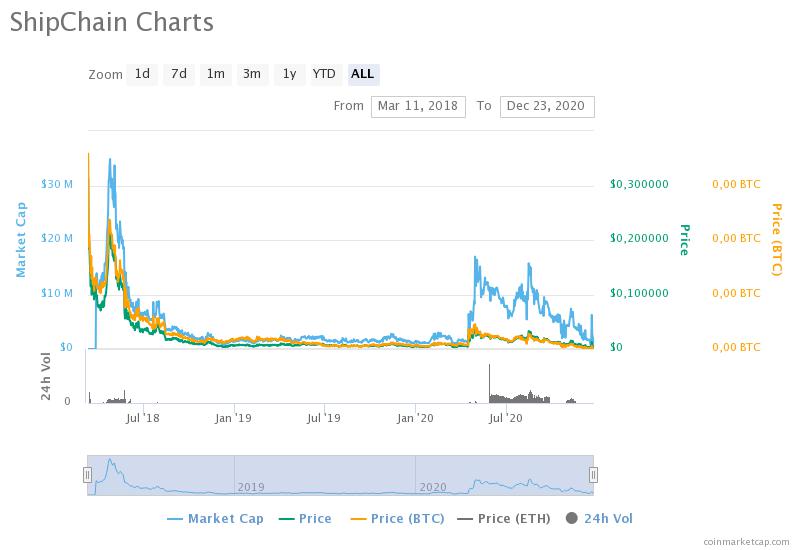

Between 2017 and 2018 the startup raised $27.6 million through an ICO. According to CoinMarketCap, in March 2018 the company’s native token SHIP traded at about $0.20.

In May 2018, South Carolina authorities ordered ShipChain to stop distributing “unregistered investment contracts”. The agency said the company violated securities laws. In the wake of the news, the SHIP token price fell by nearly half—to around $0.06.

ShipChain representatives said the startup was operating within the legal framework and that its token was not a security. In July of that year, the state’s attorney general’s office overturned the order barring the company’s activities, a precedent in the United States.

However, the SEC deemed the ShipChain ICO unregistered. By agreement with the regulator, the startup will pay a $2 million fine, delist SHIP from cryptocurrency exchanges and hand over the tokens to the regulator.

At the time of writing, SHIP traded at $0.001173.

Data: CoinMarketCap.

Earlier, the U.S. District Court for the Southern District of California ordered ICO startup Blockvest LLC and its founder Reginald Buddy Ringold to pay $696,000 per the SEC suit.

Follow ForkLog on Twitter!