Donald Trump is heading to the White House, bitcoin is taking up more space in investors’ portfolios, and altcoins still refuse to rally. We read such headlines both today and exactly eight years ago.

Oleg CashCoin explains why 2024 looks uncannily like 2016, where it differs and what follows.

Waiting for Trump

In 2016 Donald Trump unexpectedly won the US presidential election. Bitcoin traded around $700. He began his first term by trying to push a fiscal agenda that put American business first. His team, as now, worried that the United States could lose the initiative in various areas, including crypto.

“If we do not embrace cryptocurrency and bitcoin technology, China and other countries will. They will dominate, and we cannot allow China to dominate,” — will say Trump in 2024.

Eight years before that statement there was no Department of Government Efficiency (DOGE), no army of crypto supporters in the presidential entourage, no bitcoin ETFs, no large institutions pushing bitcoin. Nor were economic problems and the budget deficit as severe, and the US national debt stood at a “modest” $20trn versus $35trn in 2024.

Business and regulatory expectations at the time about a billionaire’s arrival in the White House are well captured by the minutes of the FOMC meeting on 14 December 2016.

“The effects of [the Trump administration’s] policies on the economy, if implemented, are likely to be partly offset by tighter financial conditions, including higher longer-term interest rates and an appreciation of the dollar,” the document says.

The Fed’s view of Trump’s economic vision is unlikely to have changed over the intervening eight years: as before, the American leader declares cuts to federal spending, a clampdown on illegal migration and higher tariffs on imports.

While power is in transition, no one can predict the scale of the fiscal measures crypto-friendly allies in the White House are preparing. As for the Fed, one can say with confidence only that the process of cutting rates will likely be paused, at least until Trump’s inauguration.

Illiquid alts

New risks and attendant uncertainty have appeared across financial markets of late—paradoxically without visible stress.

Even cryptocurrencies, which have slotted neatly into electoral cycles, are behaving as if nothing exists besides bitcoin and meme tokens. The logic may be that the market sees no clear prospects and so puts altcoins on pause until the first obvious political moves.

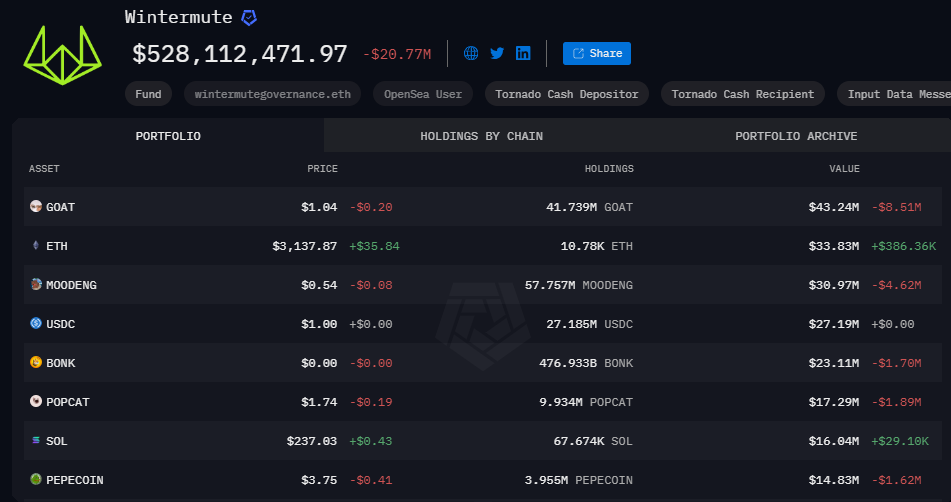

Capital, it seems, finds nothing better than lightweight, illiquid meme coins and reinforced-concrete bitcoin. Just look at a public address of one top market maker, Wintermute, whose portfolio is all but 90% memes.

Altcoins have yet to find a place with big money, unlike bitcoin, which has in effect taken a new form, moving from a risk asset into the bucket of stable investment vehicles—and remarkably attractive ones.

Physical gold’s average annual return is around 6–8% depending on the period, above government bonds. The S&P 500 delivers about 10%. Bitcoin offers roughly 50%, which sets it apart from the rest of the global asset market—let alone altcoins.

For comparison, the Bitwise 10 Crypto Index Fund, launched at the end of 2020, outpaced digital gold only once, in the 2021 bull market. Over the past four years, the first cryptocurrency has beaten the index’s constituents by more than 2.5 times.

This is just one of many statistical illustrations of why altcoins typically have short lives: over long stretches they simply make less money while carrying higher risks. No one has yet matched the returns of digital gold.

Notably, if you take the 2021 peaks across markets, around March, you get a vivid picture of identical behaviour in gold, the S&P 500 and bitcoin. The Bitwise crypto index, by contrast, remains deep underwater.

From an economic standpoint, it is physical gold that would somehow have to lose investment appeal for conditions to emerge that favour risk assets, including altcoins.

The key difference

Returning to Trump in 2016, who tried to refocus efforts on the home market, many expect the 2024 cycle to reprise an investment script aimed at the technology and manufacturing sectors.

The macro backdrop differs by just one variable: the Fed’s policy rate. US inflation is roughly where it was eight years ago—just above 2%—leaving the central bank room to manoeuvre. Unemployment is about 20% lower than in late 2016, at 4.1%, which also provides a cushion for stress.

The only material difference is that the Fed’s rate sits above 4%, whereas in 2016 it was below 1%. Yet Trump arrived just as a multi-year hiking cycle was beginning. If you recall the FOMC’s words from that time, today the Fed need do nothing more than keep things where they are.

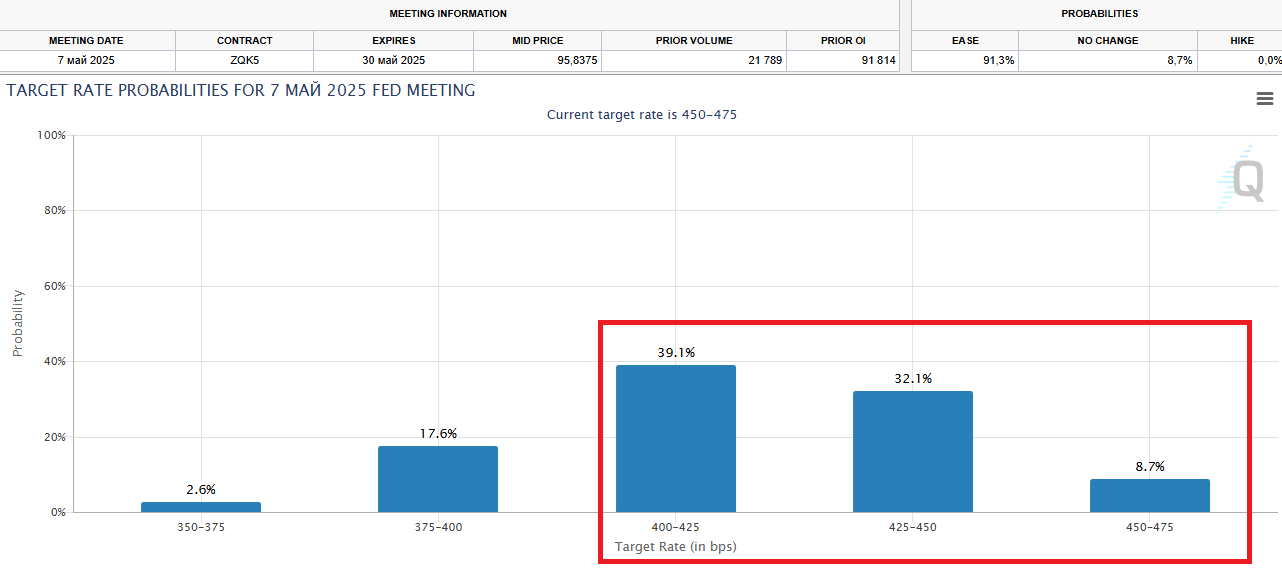

This is visible in CME rate futures, where by May 2025 expectations have shifted towards halting the process of rate cuts. Hence the so-called Fed pivot is postponed indefinitely.

Given the theory behind rate hikes and cuts—when the Federal Reserve pours liquidity into markets or drains it, as in 2016—today we are, in effect, deprived of that tailwind. That weakens the case for liquidity spilling into risk assets, which could have propelled altcoins.

Thus, while global political uncertainty persists and gold stays firm, it is logical that liquidity concentrates in bitcoin—and altcoins have to wait.