The mechanisms of the lending DeFi protocol Aave version V3 have prevented the formation of bad debts, though this has resulted in significant losses for borrowers. This conclusion was reached by analysts at the Bank of Canada.

According to a study, from January 27, 2023, to May 6, 2025, Aave V3 did not record a single case of loan default. This was made possible by the model of over-collateralization and automatic liquidations.

Typically, smart contracts close positions before the collateral value falls below the debt amount. This protects lenders from losses.

Risk Shifted to Borrowers

However, this architecture has a downside. Bank analysts noted that the system effectively shifts risks onto borrowers, who bear the brunt of losses during market downturns.

During periods of high volatility, liquidations occur rapidly and often at unfavourable prices. Experts estimate that users in such cases lose an average of 5–10% of the liquidated position amount in fees. Considering the opportunity cost from subsequent price recovery, this figure reaches 10–30%.

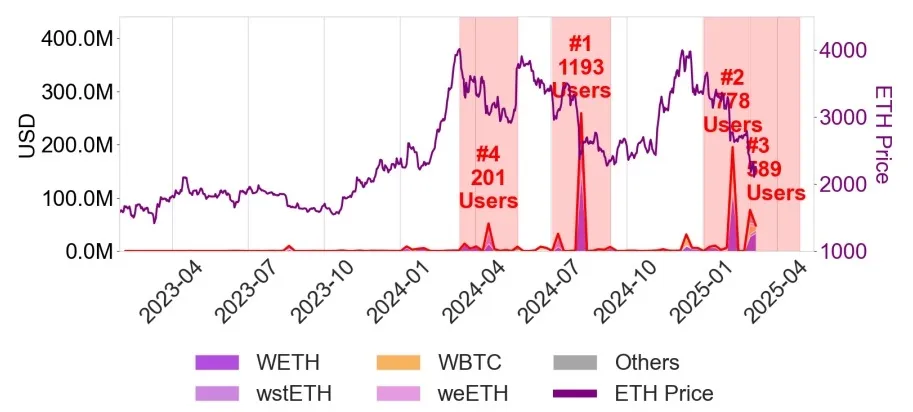

Moreover, liquidations occur unevenly—in waves, increasing market pressure. About 90% of closed positions involve a set of four tokens, which are “wrapped” versions of Ethereum and Bitcoin. This leads to risk concentration and the protocol’s dependence on the dynamics of the two largest crypto-assets.

Role of Leverage

An additional risk factor is the widespread use of so-called recursive lending. This mechanism allows collateral assets to be reused multiple times to increase the loan amount.

This form of leverage accounted for more than 20% of the total borrowing volume in 2024. However, leverage increases users’ vulnerability when collateral prices fall—the model heightens the system’s sensitivity to market shocks and accelerates cascading liquidations.

Potential of DeFi Lending

Following their analysis of Aave V3, Bank of Canada experts noted that DeFi lending is already capable of operating without intermediaries—smart contracts efficiently allocate liquidity and maintain system stability.

“Lending without traditional intermediaries is viable in a technical and operational sense,” they acknowledged.

However, the model has several key limitations. Firstly, some capital remains underutilized due to pool fragmentation, reducing overall efficiency. Secondly, over-collateralization makes loans expensive and limits DeFi’s application outside the crypto market.

The system does not eliminate risks but redistributes them—primarily to borrowers. Analysts consider the lack of clear regulation in the field and traditional lending rules, such as capital requirements, leverage limits, or liquidity thresholds, to be significant issues.

In March, developers launched version V4 of the protocol on the Ethereum mainnet.