Proceeds from cryptocurrency sales are enabling low-income households to secure larger mortgage loans, thereby introducing financial risks. This conclusion was shared by researchers from the OFR in a recent report.

A new OFR Brief examines the relationship between crypto exposure and the increase in household debt since the COVID-19 pandemic.https://t.co/0h1aCfqhFh

— Office of Financial Research (OFR) (@OFRgov) November 26, 2024

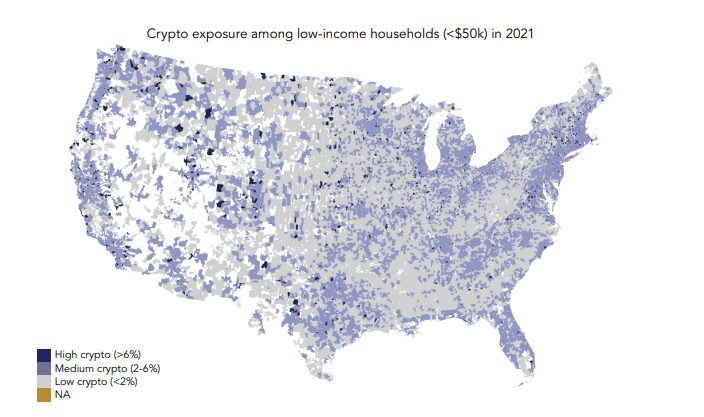

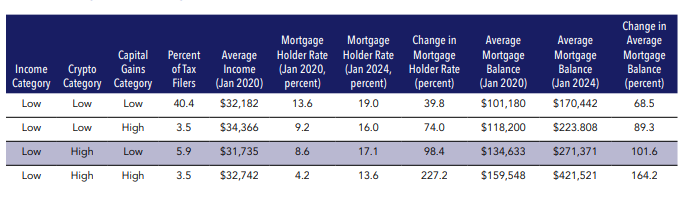

The researchers analyzed credit and taxation data in the US from 2020 to 2024. Taxpayers were categorized by annual income: low income was considered $50,000 or less, middle income $50,000–100,000, and high income over $100,000.

Regions were grouped by postal codes and classified by the degree of cryptocurrency usage: regions with low usage were those where less than 2% of households mentioned cryptocurrencies in tax returns; medium usage was 2–6%; high usage was more than 6%.

According to the researchers’ findings, cryptocurrencies are prompting less affluent Americans to take on more loans—in regions with high cryptocurrency popularity, the number of low-income households taking out mortgages or car loans increased by 250% compared to 2020. The average loan balance rose by 150%.

The debt-to-income ratio in such households, according to the report, significantly exceeds recommended levels.

“[Cryptocurrency usage] may be associated with behaviors that contribute to financial instability,” the researchers noted.

Although during the period under review, the number of payment delinquencies in this group did not exceed the norm, the researchers emphasized that under stress, the number of loans could become a vulnerability:

“Increasing stress in this group could trigger future financial stress, especially if the exposure of such consumers […] is concentrated in systemically important institutions.”

As reported in the Crypto Wealth Report 2024, since August 2023, the number of crypto millionaires increased by 95%.