For the crypto industry, 2020 was marked by rapid growth in the decentralized finance (DeFi) sector. The number of users, the number of projects, and the total value locked in smart contracts rose by orders of magnitude.

Industry predict continued rapid growth of DeFi in the coming year. In their view, many areas of the sector have yet to realise their potential, and non-custodial exchanges (DEX) will have to win back a significant share of the market from the centralized platforms familiar to most traders.

What makes DeFi attractive and what is its growth potential? Which directions are developing faster than others, and who still has a long road ahead? What hinders the sector’s development and why are institutions watching it with such caution? We answer these questions.

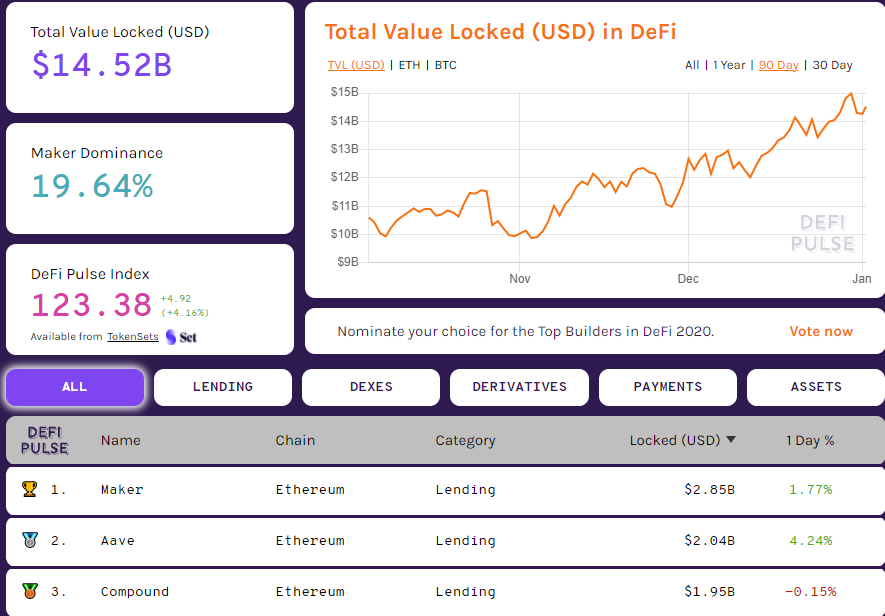

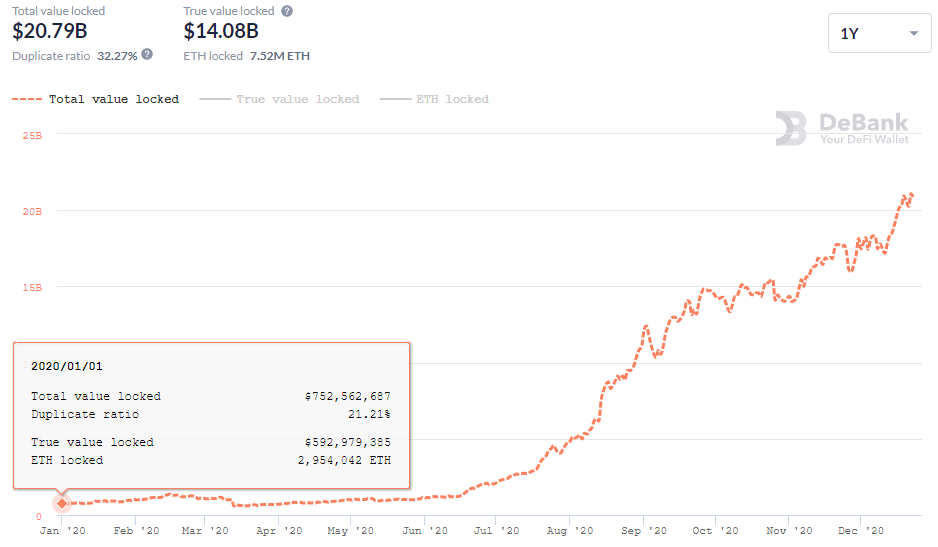

- In 2020, the DeFi sector demonstrated rapid growth. In December the total value locked (TVL) in applications exceeded $20 billion, and the number of users surpassed 1 million.

- DeFi platforms are far from perfect — centralisation risks and smart-contract bugs are common. Some services lack a compelling value proposition altogether.

- The sector continues to grow rapidly, with scaling solutions and other innovations being actively implemented.

- Experts forecast that, alongside Bitcoin and Ethereum, institutions will soon embrace DeFi.

What is DeFi and why is there so much buzz around it?

Decentralised finance (DeFi) is a direction of crypto-industry development aimed at creating a new financial system, open to everyone and not requiring trust in intermediaries such as banks.

DeFi projects rely on cryptography, blockchain technology and smart contracts. At present, the vast majority of DeFi services run on Ethereum.

Among all smart-contract platforms, Ethereum has the most developed ecosystem, bringing together thousands of developers. The activity of the latter, the growth of the user base and the volume of funds locked on smart contracts (Total Value Locked, TVL) create a significant [simple_tooltip content=’The network effect, a phenomenon whereby the value of a good or service to one user depends on the number of other consumers of that good (or service).’]network effect[/simple_tooltip]. Many attempts to “kill” Ethereum by faster protocols have not yet succeeded — at least, this is how Coinbase views it.

One of the DeFi pioneers is MakerDAO, founded in 2014 by now a familiar name. It opened users’ ability to lock collateral in Ethereum to generate DAI — an algorithmic stablecoin. The latter has over time become one of the main components of the new financial system — the decentralized credit market.

In 2020, the market capitalisation of DAI grew more than 20-fold thanks to the DeFi craze.

«By the end of 2021, this figure will double, reaching $2 billion. Other synthetic stablecoins will enter the competitive race», — shared by Messari analysts.

Over time, the number of DeFi components expanded. Beyond lending, the sector now includes non-custodial exchanges, decentralized derivatives and margin trading, insurance and other directions.

DeFi is also tightly linked to stablecoins, including centralised ones like USDT or USDC. They are actively used in lending and other directions.

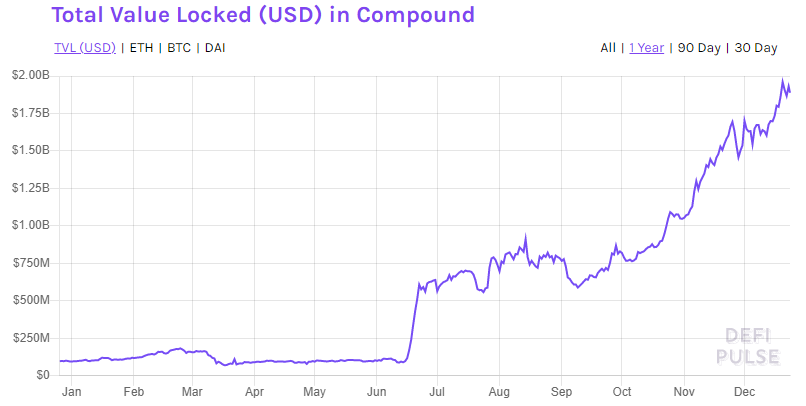

Besides MakerDAO, a key project is the lending DeFi protocol Compound. As of 01.01.2020, funds locked on its smart contracts stood at $1.95 billion.

Compound is a decentralised lending protocol with algorithmic adjustment of interest rates. Its users can deposit Ethereum, BAT, 0x, DAI, USDC, WBTC and other coins to earn interest. Deposited funds can serve as collateral for borrowing.

Another popular lending DeFi project is Aave. Its TVL recently surpassed that of Compound.

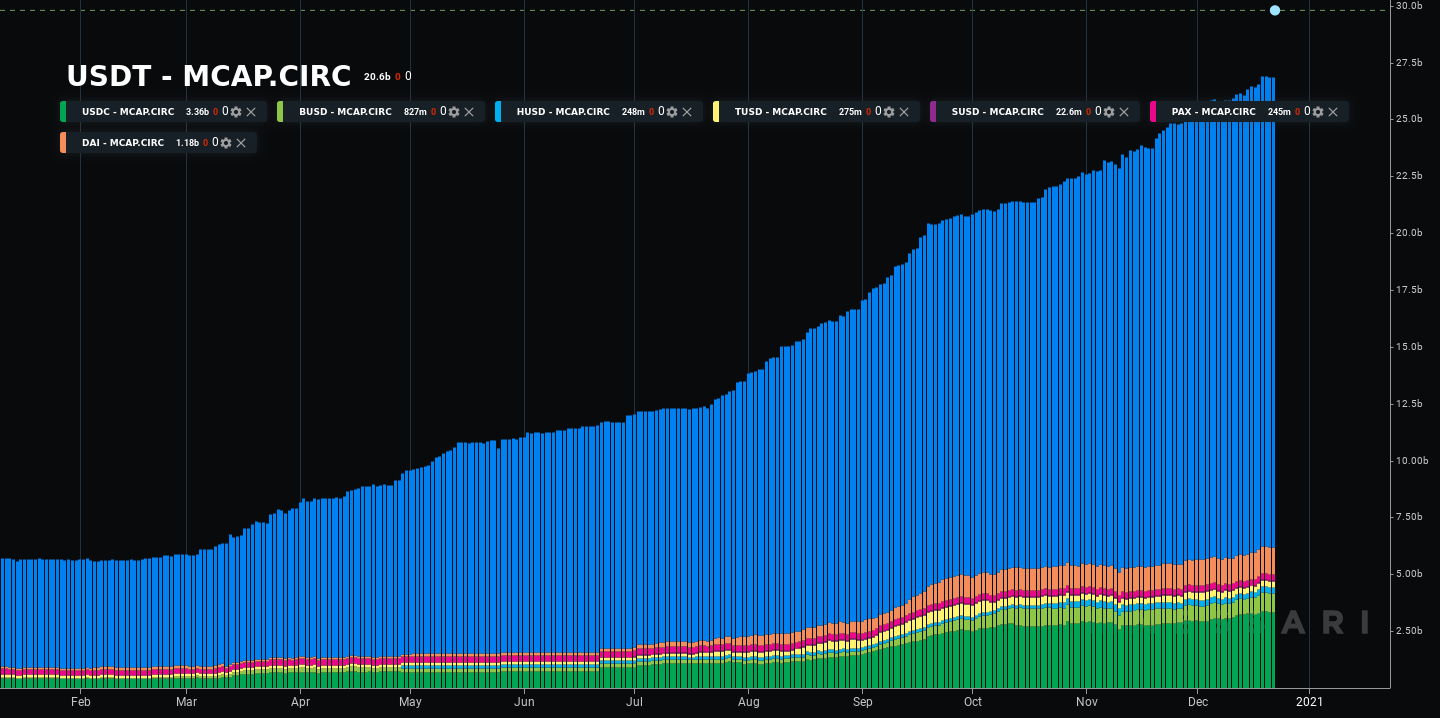

Stablecoins — another important component of the DeFi ecosystem, actively employed in the vast majority of applications. Besides DAI, there exist centralised assets USDT, USDC and PAX. They are not only pegged to the fiat dollar on a 1:1 basis, but are backed by fiat reserves, roughly equivalent to the circulating supply of the coins (or close to it, as with Tether (USDT)).

The stablecoin sector, closely linked to DeFi, is growing rapidly — its market capitalisation exceeds $27 billion (as of 1 Jan 2021). At the start of 2020 this figure stood at just over $5 billion.

First mover in the segment — Tether (USDT). With a market capitalisation of $21 billion, this stablecoin accounts for 75% of the market share.

USDC and DAI are also fairly popular. Their market capitalisations stand at $4.04 billion and $1.18 billion respectively (as of 1 Jan 2021).

Decentralised exchanges — another important and rapidly growing component of the DeFi ecosystem. DEXes operate on a distributed ledger and do not store users’ personal data. Such platforms are also called non-custodial, since market participants control their private keys themselves.

There are two kinds of DEX:

— liquidity-pool-based with an automated market maker (AMM);

— order-book-based platforms.

The most popular are the first type. They include Uniswap, Kyber, Balancer and Bancor.

Examples of order-book-based DEX include Loopring, IDEX and dYdX. The latter combines an off-chain order book with on-chain settlements. In the medium term, dYdX plans to implement layer-2 solutions for perpetual contracts.

DEX can also be categorised as platforms with a native token and those without one (yet).

Just like in traditional finance, cryptocurrency derivatives are contracts whose value is determined by the prices of underlying assets. The largest DeFi derivatives platform is Synthetix. As of 01.01.2020 its TVL stood at $1.27 billion.

There are also platforms for margin trading, where lending is available. Among the popular ones are dYdX and Fulcrum.

Insurance — a key area of the traditional market, actively developing in DeFi as well. The most popular decentralised insurance platforms are Nexus Mutual and Opyn.

Oracles play a crucial role in the sector, supplying reliable data from off-chain sources to smart contracts. The best-known player in this space is Chainlink. Such services are not exclusive to DeFi, and their importance in DeFi is hard to overstate.

«Chainlink, the popular decentralized oracle, is an important component of the information infrastructure. Yet this is more a [simple_tooltip content=’Layer or set of software to enable interaction between different applications, systems, components.’]linkage software[/simple_tooltip] than a part of the financial system. Likewise, smart-contract platforms provide the baseline tools for DeFi, but are not solely focused on financial applications», — Messari’s report “Crypto Theses for 2021.”

These categories outlined above are the core components of the DeFi ecosystem. Various platforms combine these components almost like building with Lego, yielding complex products such as TokenSets that implement sophisticated crypto-asset management strategies.

In the table below, the main differences between DeFi and centralised services (CeFi) are listed.

One important distinguishing feature of DeFi services is their permissionless nature, whereas CeFi platforms are permissioned.

Users of decentralised platforms are attracted by relatively high yields on deposited assets and accessible borrowings that do not require visiting a financial institution or bureaucratic red tape.

To access these services, a wallet is required — one of the most popular is MetaMask.

Chronicles of the DeFi Mania

In 2017, during the ICO boom, various projects competed to call their creation the “best cryptocurrency.” By 2020 almost every project positioned its tokens as “DeFi.”

Against the backdrop of the coronavirus crisis and the radical government measures to address its economic fallout, the DeFi sector took off.

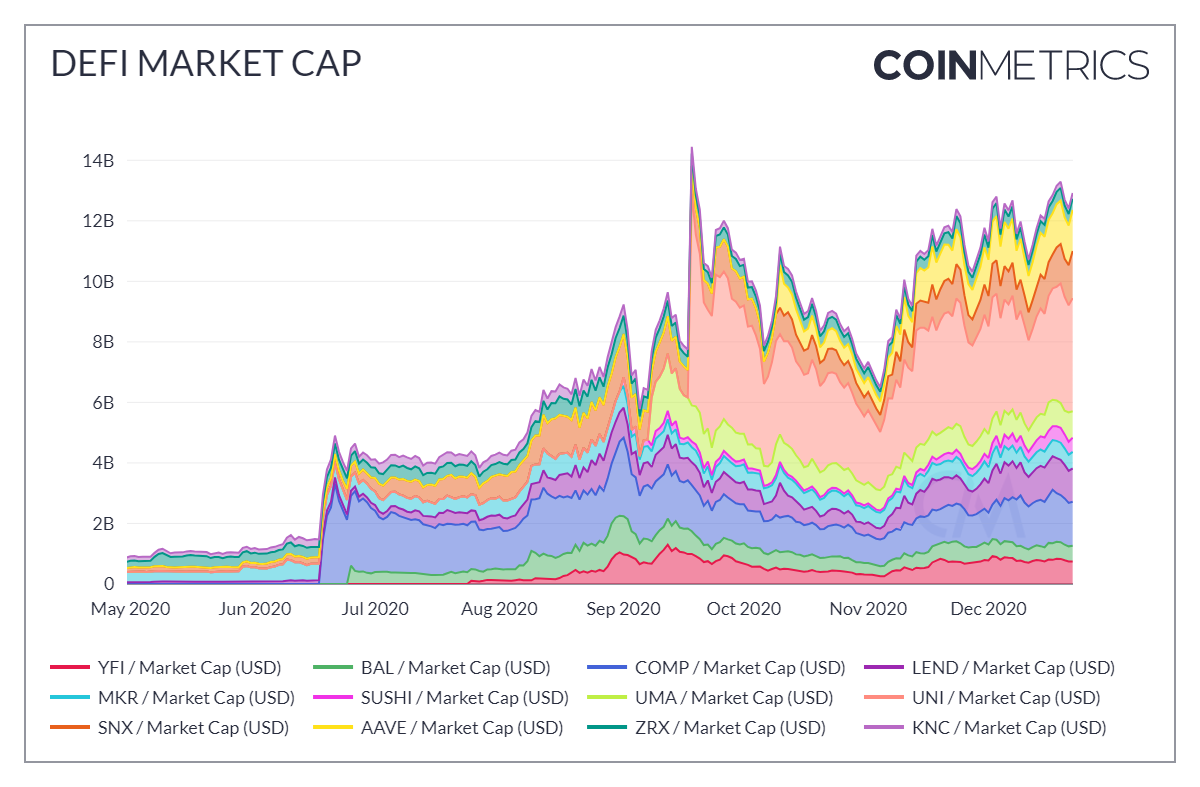

On 1 January the aggregate TVL was around $600 million, and by the end of December it had surpassed $15 billion, according to DeBank. In less than a year, the figure had grown twentyfold.

Growth accelerated notably in June when Compound launched its governance token COMP.

A week after COMP’s distribution began, the value locked in Compound rose from below $100 million to over $600 million. The token’s launch created a hype around “yield farming” and signalled the start of a race for high returns on DeFi locked funds.

«Soon after, many DeFi projects began to imitate the COMP distribution model, pushing Ethereum’s price to price levels not seen for several years», — in a Coin Metrics report.

Another powerful growth driver was Ethereum-based Uniswap, which popularised the automated market maker mechanism (AMM). In June, Uniswap’s daily trading volume stood at around $1 million, and by early September it approached $1 billion. For the first time in the industry’s history, a DEX surpassed Coinbase by turnover.

Uniswap’s rally led to a sharp uptick in on-chain activity, pushing Ethereum network fees to new highs.

In September, Uniswap unexpectedly released its own governance token, which almost immediately found listings on Binance and several other major CEXs. In the largest DeFi airdrop in history, 113 million UNI were distributed among 184 thousand DEX users, including liquidity providers and SOCKS token holders.

The sudden appearance and distribution of UNI pushed TVL and the DeFi segment’s market capitalisation to new highs. Yet the hype soon waned as recipients sold the token en masse. As a result, UNI’s price retraced from $7 to below $2.

Success from Uniswap has been attempted by other projects. One of the latest examples is the large airdrop from leading DEX-aggregator 1inch.

After a significant fall in October–November, the sector’s market capitalisation recovered, returning to September levels.

As of the end of December, Uniswap counts more than 24,000 different trading pairs. Each week, around 100,000 users interact with the platform. Uniswap’s turnover exceeded $50 billion since its inception.

The total DEX turnover for 2019 was $2.98 billion. The 2020 figure surpassed $100 billion, according to Dune Analytics.

Market share of AMM-based DEXs is almost 90%. Among liquidity aggregators, 1Inch leads, with the Matcha platform from the 0x developers gaining popularity.

By the end of December, the number of DeFi users surpassed 1 million. The figure continues to grow steadily.

The market for tokenised Bitcoin is rising as well, with Wrapped Bitcoin (WBTC) standing out. As of 24.12.2020, more than 140,000 WBTC had been issued worth $3.26 billion (according to BTC on Ethereum). Wrapped Bitcoin’s share of its segment exceeds 80%.

Protocols such as WBTC, renBTC and HBTC give holders of digital gold access to a DeFi-rich sector. Demand for Bitcoin-backed Ethereum assets limits the supply of the first cryptocurrency and thus supports its growth.

Among other developments, the second half of 2020 saw elevated activity in DeFi acquisitions. The startup yEarn.Finance made notable progress, quickly integrating with lending protocol Cream, project Pickle Finance and the Argent wallet, the Akropolis platform, the decentralised insurance market Cover Protocol, and with Uniswap’s fiercest competitor — non-custodial exchange SushiSwap.

A Spoonful of Bitterness

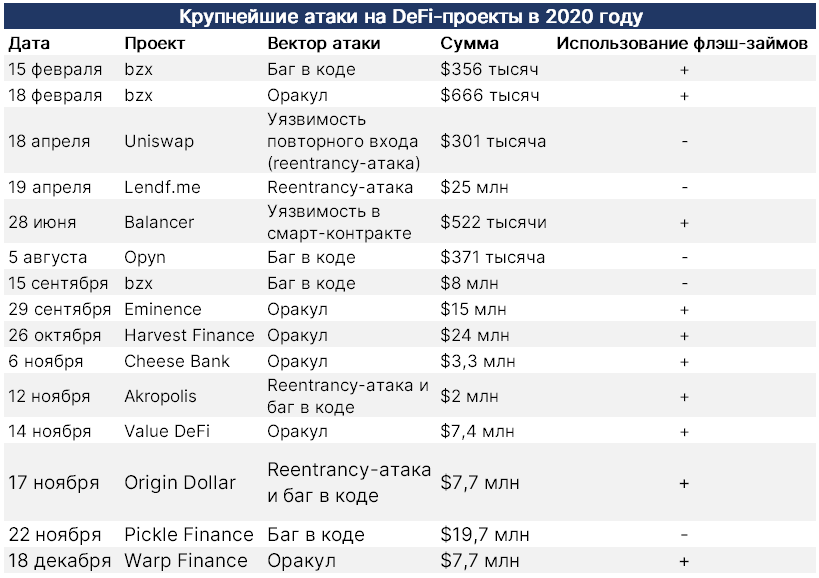

Like any sector, DeFi carries multiple risks. The fate of users’ funds in any project can be threatened by a bug in a smart contract or a hacker attack.

In August, YAM’s token collapsed by 99% due to a discovered bug. The Yam Finance developers announced they could not fix the vulnerability and disclosed the second version of the protocol.

Before depositing funds, users should carefully assess not only yields but also how decentralised the project is and whether the governance levers really lie in the hands of the community.

In early September, the SushiSwap administrator sold part of the developer fund with assets worth $27 million, sending SUSHI prices down. However, he soon returned the funds, apologising to the community.

There are also systemic risks capable of affecting a number of projects. For instance, in November a temporary rise in the DAI price on Coinbase led to the liquidation of multi-million-dollar positions on Compound.

Recently, MakerDAO found a loophole, according to B Protocol founder Yaron Velner, allowing users to evade liquidations. He cautioned that some vulnerabilities’ potential consequences are hard to predict.

The March market crash yielded a class-action suit against MakerDAO for $28 million. Against a backdrop of global panic and extreme load on the Ethereum network, attackers managed to drain more than $8 million from the system.

Algorithmic stablecoins are not without flaws. For example, DAI is backed by centralised assets — USDC, WBTC, TUSD and PAX — to a degree of about 40%.

Indices of DeFi tokens are also imperfect. Messari analyst Roberto Talamas called them not sufficiently diversified and overly dependent on the “blue chips” included in their baskets. This means their ability to reduce investment risk is questionable.

Excessive on-chain activity, as seen during the UNI airdrop, leads to network congestion on Ethereum. During such periods, users face high transaction costs. Some participants lose the opportunity to top up collateral to avoid liquidations in time.

Amid the hype of H2 2020, there was a rise in hacks targeting DeFi protocols, often using flash loans. Warp Finance was a victim, losing $7.7 million. The incident occurred a week after the project’s launch.

In November, the Value DeFi project was harmed after developers disclosed a “complex attack” that enabled the attacker to drain $6 million in DAI and USDC stablecoins.

Shortly before, an unknown hacker carried out a flash loan attack on the Akropolis DeFi protocol, emptied the YCurve and sUSD pools in DAI for $2 million.

Sometimes hackers target the founders’ personal addresses, as in the Nexus Mutual incident.

Against the backdrop of DeFi mania, shady projects mushroomed. Their organisers’ main aim was to misappropriate user funds, cover their tracks and vanish. This included Compounder Finance, Yfdexf.Finance, LV Finance, EMD and DistX.

Such incidents often occur during market bubbles — exit scams became commonplace around 2017–2018 during the ICO frenzy.

Numerous bugs, hacks and exit scams — a serious obstacle to the sector’s development. It is no accident that a third of ForkLog readers refused to invest in DeFi.

Further prospects for DeFi

There is a high probability that 2021 will see continued growth in the sector. That means more attacks, including those involving flash loans.

«To counter such attacks, DeFi platforms must significantly expand the range of price data they obtain. Then price manipulation would only be possible by distorting the asset’s global value», — emphasised by Chainlink co-founder Sergey Nazarov.

DappRadar researchers are confident about the bright prospects of projects like Nexus Mutual and Opyn. The firm’s experts counted more than $120 million in user losses from 12 hacks involving bugs in smart contracts.

«Insurance will become the next important subcategory of the DeFi ecosystem», — researchers预测.

In light of this, some projects expand platform functionality. For example, Opium Protocol, a crypto-derivatives platform supported by Galaxy Digital and Alameda Research, announced the launch of a risk-hedging service in the sector.

Also, DappRadar experts believe that DeFi projects will be the main driver of the crypto economy in 2021. They expect increased use of Bitcoin and Bitcoin-backed assets, including WBTC and sBTC from Synthetix.

The founder of Uniswap, Hayden Adams, is confident that in eight years the platform’s total trading volume will reach $1 trillion, provided that the current monthly turnover of $10 billion is maintained.

DEXes are increasingly competing with mainstream CEXs on spot trading volume. The Block analysts believe that the new rivals to traditional financial products will be decentralised derivatives — perpetual swaps, futures and options.

«Synthetic assets are especially interesting. They open up permissionless trading not only of tokens but also of futures on equities and commodities», — researchers noted.

The vast majority of DeFi applications are built on Ethereum, and the scalability problem remains relevant. However, various projects are implementing innovative solutions to improve performance and speed up applications, as well as reduce transaction costs for users.

For example, the Polymarket prediction market uses the Matic second layer technology, Loopring employs zk-Rollups scaling solutions, the dYdX platform plans to use StarkEx from StarkWare for scaling, and Curve is integrating zkSync from Matter Labs.

On Optimistic Rollups, Uniswap and Synthetix are working. Recently, the Perpetual Protocol launched a sidechain xDai. The Graph project will use scalable state channels.

A reasonable question arises: if DeFi is so attractive, why hasn’t institutional money poured in as with Bitcoin? The Block researchers say the sector still lacks risk-management tools and institutional-grade custody integrations.

«Participation in DeFi requires understanding a number of risks that differ from traditional finance», — researchers stressed.

Among the risks are:

— smart-contract vulnerabilities;

— hacker attacks;

— failures in economic incentive mechanisms and other protocol flaws (for example, non-execution of liquidations);

— custody risks, often tied to insufficient decentralisation of a project, etc.

To address these issues, various tools are being developed. Gauntlet, a platform specialising in financial models for blockchain projects, is developing a risk-assessment tool for DeFi services.

Fireblocks launched a cloud platform to protect crypto transactions from a range of risks — from private key theft to spoofing. The firm provides institutional access to DeFi products on the Compound platform. In November Fireblocks raised $30 million in a Series B round.

MetaMask is working on a new version of its Web3 wallet. The product is aimed at trading firms and custodians, who will be offered “institutional-grade features.”

«Tools for institutional participation in DeFi are improving, but regulatory questions remain. When trading on decentralised exchanges there is no clear counterparties, which is challenging under KYC/AML requirements. Still, growth in the number of large participants is expected», — The Block researchers noted.

According to experts, the DeFi ecosystem needs robust multi-signature solutions. Popular browser-based Web3 wallets do not provide security guarantees adequate for institutional players.

Conclusions

Products from the traditional finance world are still built on legacy infrastructure and are not accessible to everyone. They require strict KYC/AML compliance (хоть и не для всех) and carry high transaction costs.

In contrast, the DeFi ecosystem offers more open and transparent permissionless solutions. These include not just non-custodial asset exchanges and collateralised loans, but crypto-native constructs such as decentralised autonomous organisations (DAOs), AMMs, liquidity mining, yield farming and much more.

The majority of DeFi services are built on Ethereum, but future competition from other platforms and greater interoperability with various protocols remains possible.

Institutional players are showing interest in decentralized finance. This is evidenced by the positive trajectory of venture investments in the sector and the acceleration of developments aimed at large players.

DeFi is a rapidly evolving field with wide opportunities. Users should remember that the sector is still in its infancy, and attractive returns from new projects usually come with substantial risks.

Subscribe to ForkLog’s channel on YouTube!