Bitcoin tested $74,000; traders shifted to Hyperliquid to trade oil and gold; miners stepped up coin sales; the community called for a ChatGPT boycott; and other events of the week.

Attempts to consolidate

The past seven days were volatile for crypto, but brought a few brighter signals.

The first cryptocurrency opened Monday around $65,000 and by evening had approached $70,000. It was not the first bid in recent weeks to clear that level, and this time it succeeded.

After a brief pullback on Wednesday, 4 March, digital gold surged to $74,000 for the first time in a month. It did not hold those levels for long.

The next day bitcoin again tested $74,000 before slipping into a correction.

Through the second half of the week the coin gradually lost ground, falling to $67,500 by Sunday.

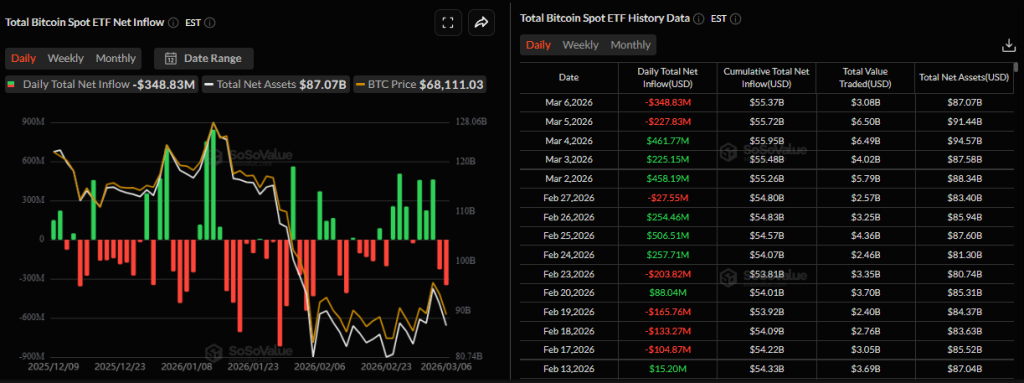

Bitcoin’s rise coincided with a recovery in inflows to spot ETFs backed by the asset. Net inflows for the week totalled $586 million.

On Monday, Tuesday and Wednesday the products recorded positive flows of +$458 million, +$225 million and +$461 million, respectively. On Thursday and Friday they turned negative: -$227 million and -$348 million.

Bitcoin still reacts sharply to global conflicts and macro signals. A statement by U.S. president Donald Trump ruling out any chance of negotiating a settlement to the situation in Iran sparked a jump in oil prices and a stronger dollar index. That pressured risk assets such as big-tech shares and cryptocurrencies.

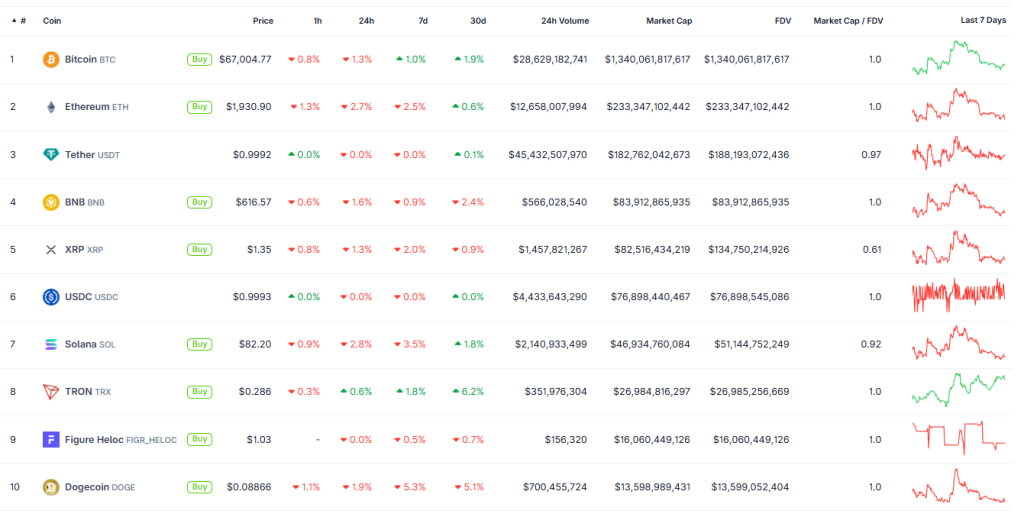

The rest of the digital-asset market duly followed the flag-bearer, though some constituents fared worse.

ETH fell 2.5% over seven days to $1,930. SOL slipped 3.5% to $82. TRX added 1.8%.

The analyst Darkfost noted that about 38% of altcoins are nearing all-time lows. Conditions in the sector are worse than after the FTX collapse.

Investors, he said, are shunning risk. Liquidity is rotating from crypto into equities and commodities. Alternative coins are bearing the brunt and losing market share.

As of 8 March the total crypto market capitalisation stands at $2.36 trillion. Bitcoin’s dominance is 56%, Ethereum’s 9.9%.

The Crypto Fear and Greed Index hovered around 12.

Oil and gold on-chain

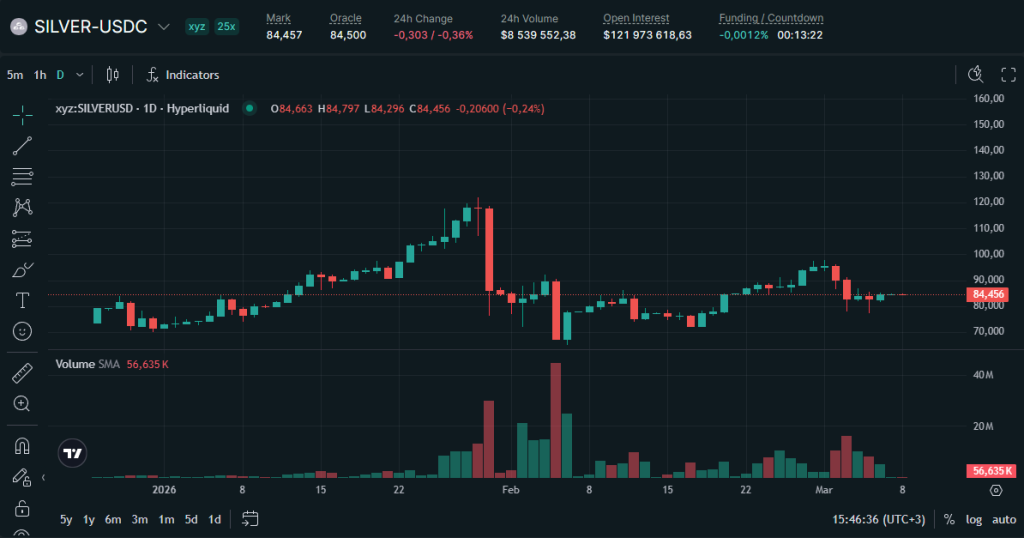

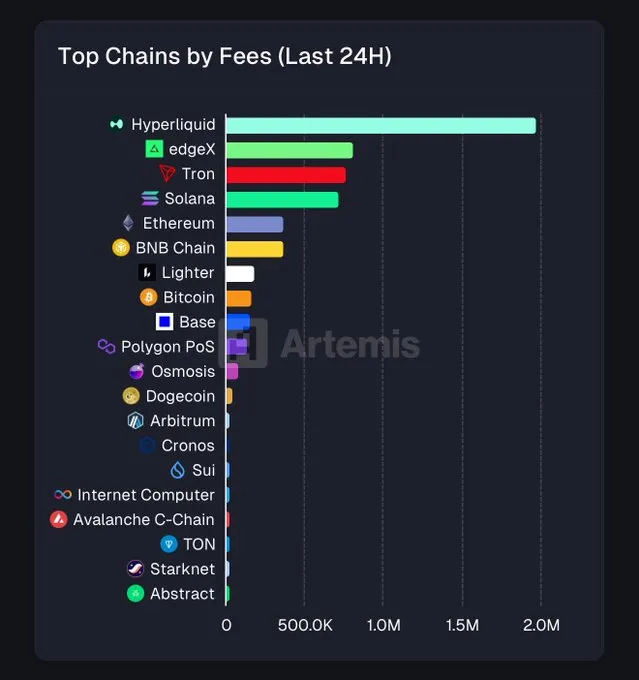

Escalation in the Middle East prompted a mass move by crypto traders to the decentralised exchange Hyperliquid to trade perpetuals on oil and gold.

Interest centred on tokenised commodities based on HIP-3.

On 8 March the USOIL token’s price in its pair with the USDH stablecoin hit a local peak of $125 before correcting to $115. Intraday, 24-hour volume reached $17 million.

Gold has also been in high demand. Peak daily turnover exceeded $159 million.

Traders were most active in perpetuals linked to silver, where 24-hour volume reached $398 million.

On 2 March, as trader interest swelled, the Hyperliquid network ranked first by fees generated, nearly hitting $2 million.

“This is proof of the power of tokenised assets and perpetual contracts built on cryptocurrency infrastructure,” said Kenny Chan, head of the stablecoin ecosystem at Coinbase.

Previously, during serious geopolitical events at weekends, traders had no choice—only bitcoin. That has changed thanks to blockchain, he added.

What to discuss with friends?

- The Economist forecast an era of space-based data centres.

- “The worst is behind us.” K33 flagged the end of bitcoin’s sell-off.

- Bitwise predicted a rapid Wall Street migration into DeFi.

- AI models preferred bitcoin over stablecoins and fiat.

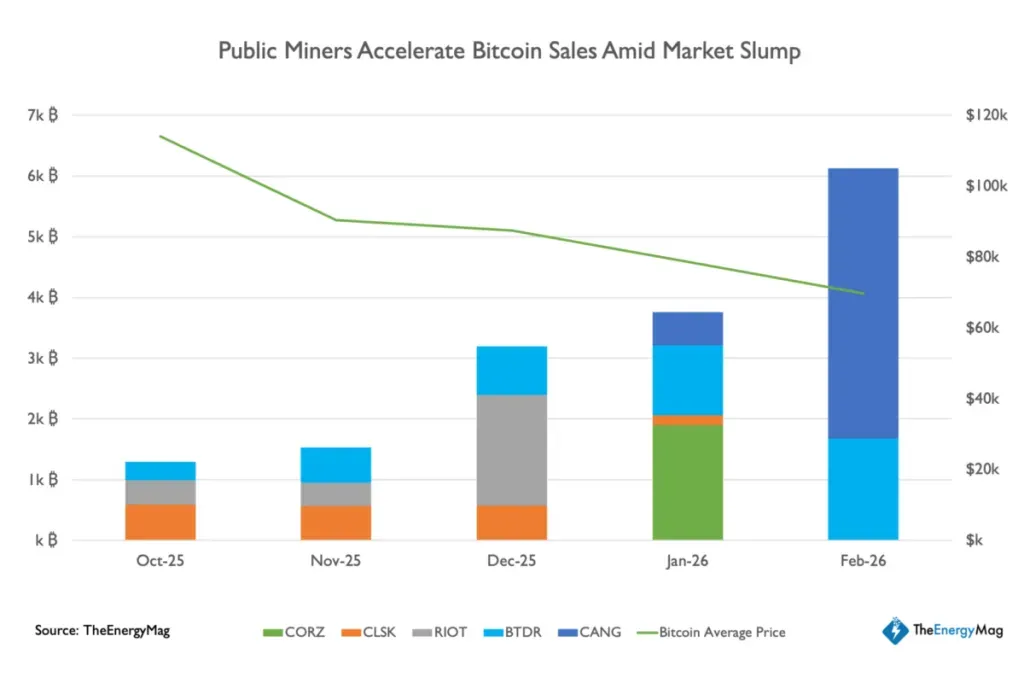

Miners sell

Reports of bitcoin miners’ capitulation are appearing more frequently. TheEnergyMag writes that recent disclosures by major players suggest the trend may be intensifying.

In recent months, the following sold down their treasuries:

- Riot — in December it sold four times more coins than it mined in 30 days;

- Cango — in February it liquidated 4,451 BTC (60% of reserves);

- Bitdeer — in the same month it fully sold its bitcoin holdings (about 943.1 BTC);

- Core Scientific — it reported plans to sell most of its coins by the end of the first quarter.

Analysts estimate that over five months public miners sold more than 15,000 BTC in aggregate.

Data from BitcoinTreasuries also indicate that bitcoin-mining firms are selling reserves en masse. Proceeds are being funnelled into building infrastructure for artificial intelligence.

A long-term hoarding strategy is losing appeal as mining revenues decline. If in 2021 bitcoin mining margins reached 90%, the figure has now fallen sharply owing to intense competition, high electricity tariffs and price corrections.

Meanwhile, the hashprice fell below $30 per PH/s per day. In such conditions, most public players operate at or below break-even.

Many miners are also now forced to service debts. The industry tapped credit lines, bitcoin-backed loans and secured bonds to finance operating expenses and large-scale build-outs of AI data centres.

The drop in bitcoin compelled many firms to top up collateral by selling part of their coins.

ChatGPT boycott

Relations between major AI startups and the U.S. military have been a lively topic of late.

In late February OpenAI chief Sam Altman announced a partnership with the Pentagon. The company agreed to deploy its AI models on classified military networks.

Anthropic’s chief executive, Dario Amodei, by contrast, publicly refused such contracts. He barred the government from using the project’s neural networks for mass surveillance and for creating autonomous weapons.

Although Anthropic was criticised by U.S. authorities—including negative remarks from President Trump—OpenAI faced stiffer blowback from the user community.

After securing the military contract, a Reddit post calling for a boycott of the ChatGPT chatbot drew 30,000 likes, and the quitGPT account on Instagram gained 78,000 followers.

More than 700 employees of Google and OpenAI also signed an open letter. The document urged rejecting the use of AI in surveillance systems or for combat tasks without direct human oversight.

After the backlash Altman moved to clarify matters, promising to amend the Pentagon deal. In the new version OpenAI added a clause banning “the intentional use of artificial intelligence” to spy on U.S. citizens.

“One thing I did wrong: we should not have rushed to do the deal. The issues are very complex and require clear communication. We sincerely tried to de-escalate and to avoid a much worse outcome, but I think it looked opportunistic and sloppy,” the chief executive said.

The tweaks did little to change the mood. Amid the boycott, Anthropic’s Claude overtook ChatGPT by downloads in the U.S. App Store.

Also on ForkLog:

- Solana Mobile opened its software to Android device-makers.

- A five-year DCA strategy delivered bitcoin investors a 72% net return.

- An app appeared that detects smart glasses.

- U.S. authorities arrested a suspect in the $46 million theft from a government wallet.

Banking intervention

The week also brought crypto moves by big financial players. Investment bank Morgan Stanley, with $1.9 trillion in assets, filed with the SEC to launch a spot bitcoin ETF.

For custody the organisation plans to use Coinbase’s service and BNY Mellon. Most of the bitcoins backing the fund will be held in cold wallets to minimise hacking risk.

Over the past five years Morgan Stanley has steadily expanded its crypto footprint.

In 2021 the bank was the first major U.S. financial institution to offer its wealthy clients access to NYDIG’s bitcoin fund. In 2024 the company allowed advisers to recommend exchange-traded vehicles based on the first cryptocurrency from BlackRock and Fidelity. In autumn 2025 Morgan Stanley analysts advised allocating up to 4% of portfolios to cryptocurrencies.

Another notable development was Western Union’s stablecoin announcement. The USD-pegged USDPT is planned to be issued on Solana, in partnership with the Web3 platform Crossmint.

USDPT’s main feature is direct conversion into national currencies. Users will be able to cash out digital dollars at 360,000 Western Union locations in more than 200 countries. The solution will let third-party fintech apps settle instantly via Solana and send funds straight to cash-out points.

Other stablecoin and cryptobanking initiatives last week included:

- Visa and Stripe will roll out stablecoin cards in more than 100 countries;

- Japan’s central bank launched a blockchain sandbox for domestic transfers;

- Tether backed a project to integrate USDT into the bitcoin blockchain;

- the Sui network launched the native stablecoin USDsui;

- Florida passed the first state-level “stablecoins” bill in the U.S.

What else to read?

In new ForkLog cards we explain what tokenised gold is, how tokenisation works and why billions are flowing in.

How street-level surveillance is built in big cities—and why governments rushed to roll it out everywhere.