The Wisdom of Whales

How prediction markets became corporate barbershops

Marketers have become adept at luring users onto prediction venues like Polymarket or Kalshi with tales of the “wisdom of crowds”, to which anyone might belong. But is that really so?

ForkLog examined just the two recent cases on Polymarket in which whales secured the outcomes they wanted against objective reality and the events on which hefty wagers had been placed.

The wisdom of insider crowds

Backers of prediction markets often point out that such platforms neatly illustrate the “wisdom of crowds”. The notion was popularised by the American journalist James Surowiecki in the eponymous bestseller of 2004, though some version of it has existed for centuries.

In 1906, Francis Galton, an English polymath who founded differential psychology (and, alas, eugenics), ran an experiment novel for its time. At a fair, visitors could pay sixpence to guess the weight of an ox.

Galton hoped to collect the “votes” of a crowd with disparate knowledge and skills to buttress his hunch about the dangers of universal suffrage. Just as a broker cannot eyeball an animal’s weight, he supposed, neither can a farmer judge politicians’ competence.

The results said otherwise. Aggregating 787 entries and taking the median, Galton found, to his surprise, that the “average voter” missed by a single pound—remarkably accurate, given the ox weighed 1,198 pounds.

The claim that, in forecasting, the uninformed majority can outperform individual experts is enticing to democrats—and, as specialists in behavioral economics know, flatters consumers of all political stripes.

But does “wisdom of crowds” apply to modern prediction markets? This was questioned by researchers at London Business School and Yale. Analysing Polymarket transactions from 2023 to 2025, they reached a deflating conclusion for most: 3.14% of participants capture 30% of profits.

“Prediction markets are remarkably accurate, but the source of this accuracy is not the ‘crowd’. […] Information aggregation in prediction markets operates differently from what the conventional crowd wisdom view implies. Rather than many participants each contributing partial information, prices appear to be set by a small number of informed traders who are skilled and whose trades move prices in the direction of final outcomes. The remaining participants provide liquidity and trading volume but contribute little to price formation,” the authors conclude.

They point not only to speculative behaviour by traders, but also to numerous signs of insider dealing.

Such accusations are routinely levelled at Polymarket and Kalshi, for which Donald Trump Jr., the elder son of the sitting US president, serves as a strategic adviser. After a scandal over bets on a military operation in Venezuela, Congress began debating a ban on prediction markets that touch on matters of public importance. Kalshi has already responded to possible regulation and began blocking accounts, for instance those of politicians wagering on their own campaigns.

Incidents of another sort attract far less attention. Seemingly minor, they are increasingly ensnaring ordinary users.

Beirut’s 3D chess

In early March the radical Shia group Hezbollah fired rockets into northern Israel. In response the IDF resumed a ground operation in southern Lebanon while striking Beirut and Tyre from the air.

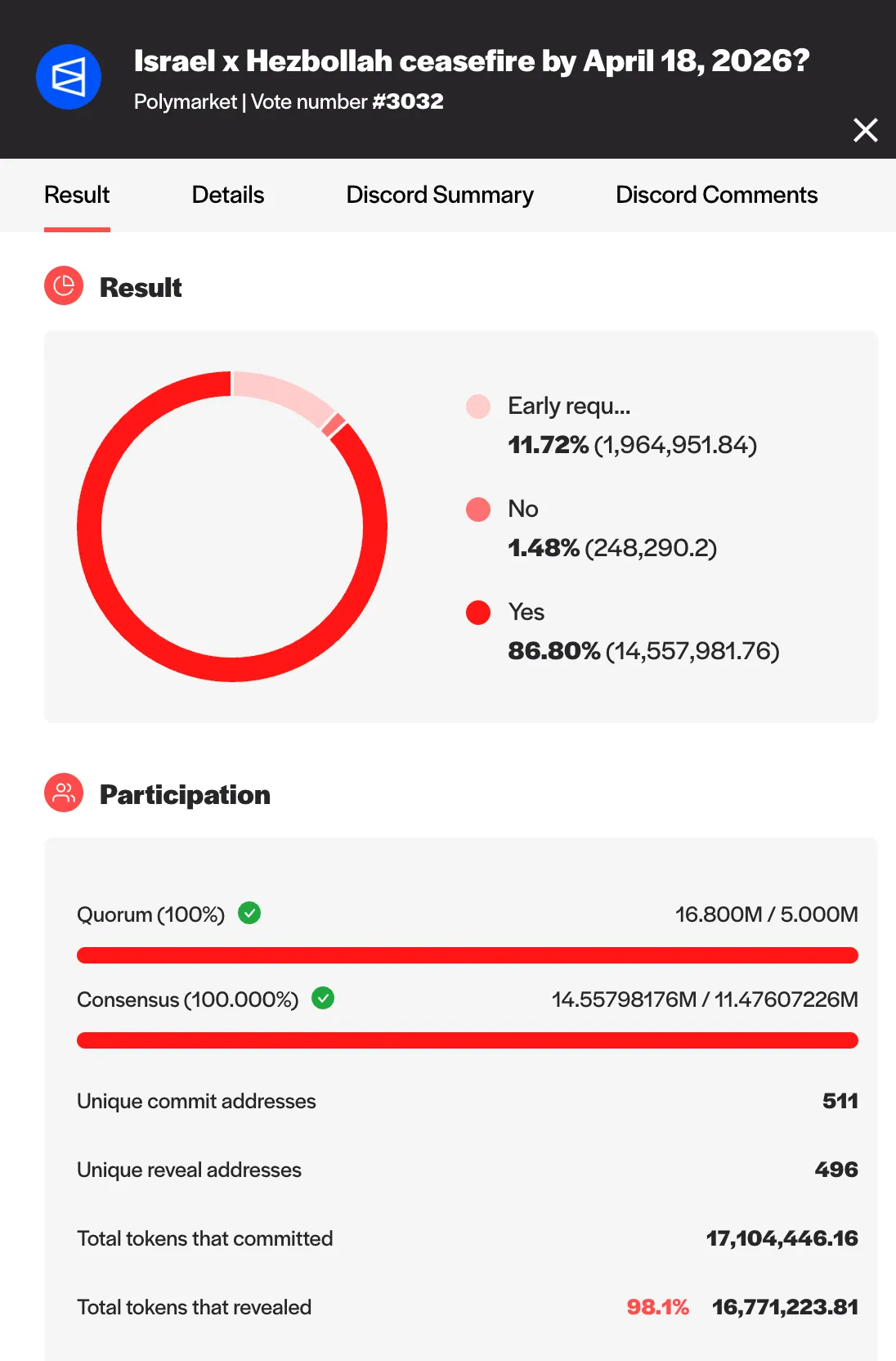

As American diplomacy joined efforts to calm the conflict, Polymarket opened a prediction market inviting users to bet on the date of an officially declared ceasefire between Israel and Hezbollah.

On 16 April US President Donald Trump announced a truce to take effect at midnight on 17 April. Soon after, the market—having amassed more than $112m—was closed early at the request of a user who had bet on “Yes” before 18 April.

The decision angered those who had forecast that no ceasefire would be reached by the stated date. First, the ceasefire was largely formal: within hours of its supposed start, official Beirut accused the IDF of new strikes on its territory. Second, Lebanon is not an active party to the current conflict, and Hezbollah said it would not join talks until Israel withdrew its troops and freed the group’s imprisoned supporters.

Those unhappy with the closure, as the rules allow, tried to contest it via UMA’s oracle platform. They failed there, too: 86.6% of votes, weighted by delegates’ token holdings, backed Polymarket’s decision and just 1.48% opposed it. “Yes” amassed ~14.5m tokens. On 16–17 April UMA traded around $0.45.

That sparked another wave of comments on the closed market. Angry users accuse Polymarket and UMA of collusion, criticise the oracle’s model for letting whales sway outcomes, complain about the admins’ silence and demand compensation.

“If Polymarket cannot reverse a final on-chain result, it should still consider refunds or compensation in cases where a disputed market failed to provide adequate protection against contested rule interpretation. This is a matter of market integrity, not just trader displeasure,” one user notes.

A $50m “crime”

At the same time, a similar incident unfolded, also tied to the Middle East. Yuri Yatsenko, co-founder of a Web3 start-up, posted on X: “A $50m crime is happening on Polymarket right now.”

The trigger was a market on a ceasefire between the US–Israeli coalition and Iran. Under the rules, a positive resolution would be counted if the parties observed a ceasefire for 14 days, or 336 hours. Polymarket’s admins held that they had. Yet, Yatsenko notes, on 7 April—the day the market was resolved in favour of “Yes”—rocket attacks continued for 20 of the 24 hours.

“Disputed resolutions sent to the UMA voting; 50 new wallets opening large ‘Yes’ positions before the announcement; one wallet turning roughly $72,000 into roughly $200,000 within hours,” Yatsenko concludes.

Experience suggests such disputes rarely end well for prediction-market punters who feel cheated. In March 2025 Polymarket refused to compensate users harmed by the premature, incorrect resolution of a market on a US–Ukraine minerals deal.

Researchers found that three large UMA tokenholders, accounting for 25% of votes, pushed through the unjust outcome. Polymarket acknowledged a governance attack, calling it “unprecedented”.

“This is not part of the future we want to build. We will create systems, monitoring and more to ensure it does not happen again,” the platform said at the time.

Back in August 2024 Vitalik Buterin wrote that “to classify Polymarket as gambling is to misunderstand what prediction markets are.” In that, the Ethereum co-founder—himself well-versed in how such venues work—was quite right.

By 2026, prediction markets had indeed shifted from advanced bookmakers into yet another piece of infrastructure in which ordinary users are merely liquidity for big players.

ForkLog contacted Polymarket on April 23 and 28 to request a comment on these developments. We have yet to receive a reply.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!