What if, tomorrow, an oil rig split into a thousand tokens were seized by an army or claimed by a state?

With that question in mind, ForkLog peered behind the curtain of tokenisation of real‑world assets and found a chasm between the RWA sector’s soaring valuations and the utility, convenience and guarantees it promises.

A challenge for lawmakers

RWA is undeniably an intriguing, even breakthrough, segment. Tokenising real‑world things makes it possible to track, round the clock, the state of an asset or business; retail investors gain access to previously closed‑off resources, energy projects and on‑chain trading of listed equities.

For TradFi, RWA offers new retail‑driven liquidity, a way to offload pricey illiquids and to acquire more valuable assets. Crypto‑derivatives provide fresh rails for old instruments, and can wrap real‑world assets into perpetual futures—before one even gets to the variety of DeFi mechanisms.

Yet the obvious attractions of tokenising real assets can obscure the flip side.

Amid sharpening global tensions and rising uncertainty among great powers, the risk that owners lose control of RWA is high. History offers plenty of attempts at expropriation and nationalisation:

- the British “enclosures” (15th–19th centuries). Common land was turned into private property as lords fenced off pastures, cutting peasants off from resources. Productivity rose (wool for the manufactories), but an army of impoverished proletarians was created;

- railway mania (1840s). In 1845 Britain saw a boom: hundreds of companies issued shares to build railways. People ploughed their savings into “paper” lines. When the bubble burst, investors were ruined—but the rails remained. Big banks scooped them up for a song and built monopolies that profited for decades;

- post‑Soviet privatisation (1990s). Under socialism in the USSR, material resources were notionally owned by all citizens. A factory mechanic, say, owned a stake in the very enterprise he served. After the Union collapsed, prices of privatised shares crumpled and were deftly bought by businessmen. Some factory bosses even engineered conditions that devalued vouchers, then invested in them via shell firms.

Another hazardous vector of asset loss is war. If a tank knocks down a pillar of a building partly owned by investors—or an invader declares the territory its own—only an insurance payout may help.

Policies do have “political risk” categories, but for crypto innovators they mostly exist in theory.

Crypto and blockchains posed a fresh challenge for lawmakers. Big regimes in the US, EU and Singapore—and popular offshore centres—have proposed corporate‑law frameworks and retail protections, leaning on old statutes. Even so, these systems do not yet eliminate the legal and structural risks inherent in tokenising real assets.

An on‑chain risk map is not enough

Three models are commonly used to paper RWA:

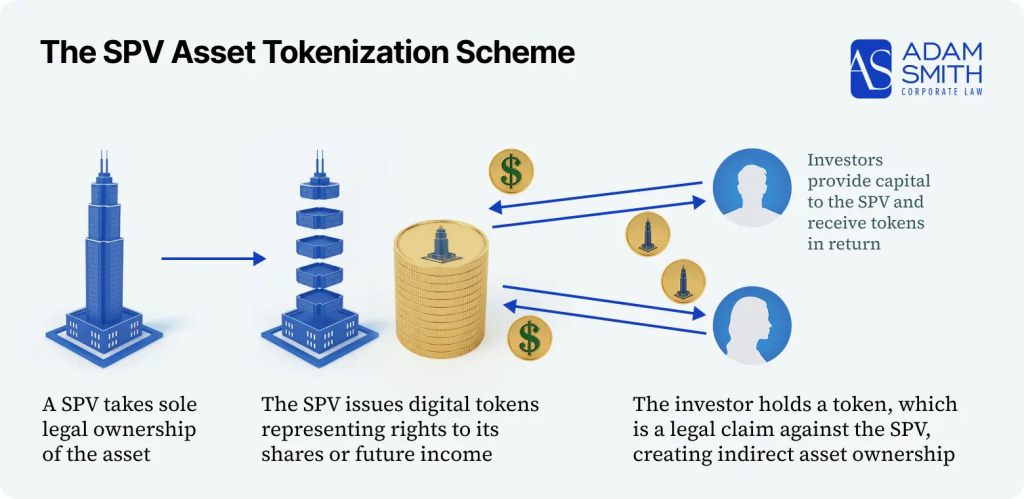

- SPV (equity or debt capital). The real asset is legally transferred so the SPV becomes sole owner. The investor holds a token that grants a claim on the SPV;

- master fund. A central master fund holds and manages the portfolio (eg US Treasuries, corporate loans or property). Smaller feeder funds or SPVs are domiciled in specific jurisdictions (say, one in the EU, one in the US). They issue digital tokens to sell to investors;

- claim‑based tokens. For the asset owner (a property developer or business), this chiefly serves as financing. The asset stays on balance sheet without transferring title to a third party. The owner signs a platform agreement to remit a share of income (rent, revenue or interest) to tokenholders via smart contracts. At maturity or on sale of the asset, the final value is paid and obligations are extinguished.

According to law firm AdamSmith, EU‑regulated tokenised funds typically opt for Luxembourg RAIFs and Irish ICAV/QIAIFs. For global capital outside the US, Cayman SPCs remain the standard. For America‑facing projects, Delaware entities with low taxes are widely used.

Experts reckon Switzerland, Germany and Liechtenstein are leading RWA hubs.

By 2026 tokenisation had grown up, but lawyers still tackle political‑risk protection with intricate legal structures and contractual plumbing. Some platforms rely not only on smart contracts, but also on guarantees from agencies that insure complex risks.

The RWA leader Ondo Finance is backed by US government debt and BlackRock ETFs. In that case, aggressive “seizure” or nationalisation of the real asset is unlikely—tantamount to a US default. In 2026 Ondo expanded into equities, using custodians like BNY Mellon, which have protection mechanisms of their own.

Centrifuge, one of the oldest protocols, uses an SPV structure. In the event of physical seizure of an asset, its legal setup lets investors sue in the SPV’s jurisdiction (typically Luxembourg or Delaware). Some lending pools in emerging markets (via partners such as Credix) may be insured by private PRI firms.

The insurer Goldfinch operates in riskier regions—across emerging markets in Africa and Latin America. Its borrowers (local finance companies) are often required to insure their portfolios against political risks with traditional carriers.

The leader in decentralised on‑chain insurance, Nexus Mutual, has a strong track record. It is governed by a DAO that decides which policies to underwrite. Members allocate capital to pools to provide cover and earn interest from clients’ premiums.

Its cases span on‑chain risks from smart‑contract hacks to DeFi technical failures and stablecoin stablecoins losing their peg.

These products are well thought through, but their coverage is confined to the digital plane—insufficient for RWA. They do not reach crucial physical‑world contingencies such as isolation or loss of the tokenised object.

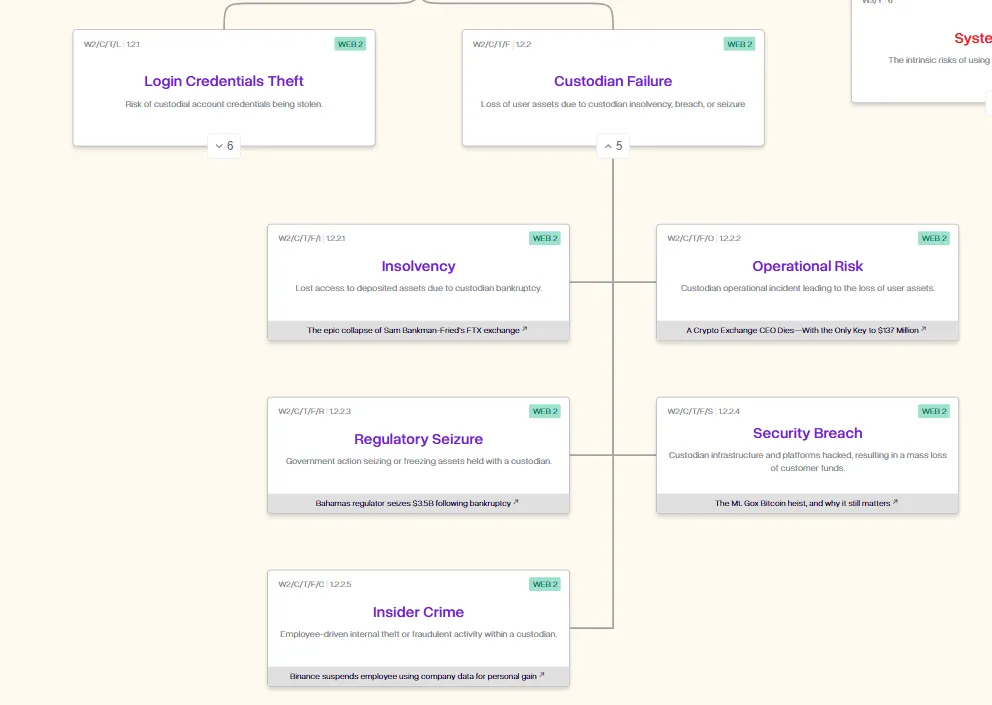

In February 2026 Nexus Mutual, in partnership with the crypto insurer OpenCover, introduced the “On‑chain Risk Map”. Intended as an interactive guide to hazards across crypto and adjacent sectors, it proved incomplete.

Loss of the underlying is tucked under custodian risk, but only in the form of regulatory seizure—evidence that leading insurers are not yet ready to offer full PRI cover.

Influential backers, cloud cities and bans

A sudden change of regulatory course in any country can upend an RWA project overnight. So it was with Satoshi Island, an island NFT “state” in Vanuatu.

Despite promises to welcome first residents in 2023, at the time of writing not a single modular home has been built. The lone resident was a project lead, Denis Troyak.

For years he nurtured an investor community and touted the virtues of life far from civilisation.

It turned out investors could not own the land directly. The island belongs to local landholders and is leased to the project. Buyers of the NFTs thus receive sub‑lease rights rather than full title.

Vanuatu’s regulators warned in 2024 that Satoshi Island Limited had no licence to arrange residency or citizenship, though the project used that as a marketing pitch.

In July 2025 the team officially halted all digital‑asset sales and purchases, effectively paralysing the NFT secondary market.

As a result, Satoshi Island Coin (STC) collapsed. As of February 24th 2026, it was down by more than 99.9% from its all‑time high (from $48 to about $0.004).

Another instructive case is not strictly about tokenised assets, but lays bare conflict between crypto and dated laws.

Investors in the city of Próspera—an economic zone on the Honduran island of Roatán—were sideswiped by a change in political leadership. The project was founded on ZEDE law (“Zones for Employment and Economic Development”), which gave investors unprecedented autonomy.

The government of President Xiomara Castro, campaigning against “corporate colonialism”, repealed the law. In September 2024 Honduras’s Supreme Court struck it down as unconstitutional.

In response, developer Honduras Próspera Inc. filed a $10.7bn claim at the World Bank’s ICSID. The firm sought compensation equal to a third of Honduras’s GDP, arguing its agreement guaranteed a stable legal regime for 50 years.

In 2024–2025 the republic began withdrawing from ICSID in protest, to avoid paying any award to Próspera.

For investors, taking on a state would likely have been impossible without heavyweight backers. Among early participants in Pronomos Capital were billionaire Naval Ravikant, Network State theorist Balaji Srinivasan, and activist Patri Friedman, who works closely with Peter Thiel’s fund.

Thanks perhaps to Palantir’s founder, the dispute drew attention in the US Congress, lending it international heft and pressure on Honduras’s authorities.

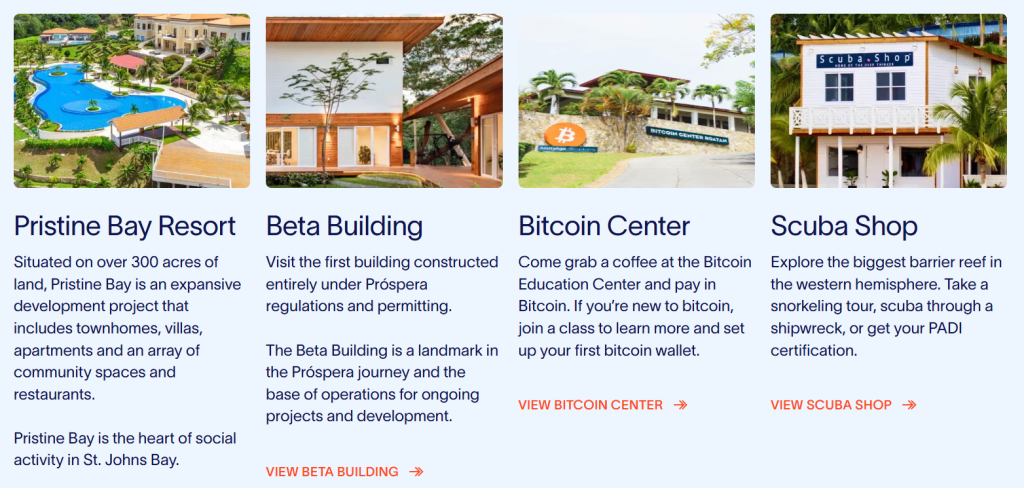

Despite the lawsuits, Próspera continues. Investor money has funded the island’s tallest building—Duna Residences—plus office and medical centres.

More than 200 companies are active and about 1,000 jobs have been created. Digital nomads, crypto founders and scientists live there. Próspera has become known for biohacking and medical tourism. Liberal rules allow cutting‑edge gene‑therapy and longevity methods to be tested that are not yet approved in the US.

Srinivasan proposes ways to reduce political risk for RWA—an integral part of his vision for “network states”.

The thrust of his theory is decentralisation and the primacy of code over law, though he concedes the legal layer is the weakest part of building “digital archipelagos”.

In his view, RWA protection in a “network state” should come from distributing assets across multiple jurisdictions. If one country’s authorities try to seize a building, they cannot wipe out the structure as a whole.

If, in time, an insurance payout is received for a destroyed or expropriated asset in one place, the community can build two new ones elsewhere.

In a July 2025 post, “All property becomes cryptography”, Srinivasan set out simple technical points that complicate attempts to grab assets.

For him, RWA is a fundamental shift in the nature of ownership. Traditional property rights, he argues, have always rested on force (police and armies); cryptographic rights rest on mathematics.

“The ultimate goal is to make any kind of property as hard to confiscate as bitcoin. We are moving from a world where title is attested by the state to a world where it is attested by knowledge of a private key,” the entrepreneur believes.

Srinivasan is sure the future lies with assets that cannot be “switched off” by a bureaucrat’s order. That leads to the idea of cryptographic locks not only for data, but for physical things.

In short, RWA today sits in a grey zone of its evolution. Convenience and liquidity on one side; the unresolved “last mile” on the other—where blockchains meet drone strikes and nationalisation.

Traditional legal contraptions like SPVs and Luxembourg funds remain useful crutches, but the Satoshi Island and Próspera cases show even grand projects can become hostages to political regimes. RWA investors must weigh not only smart‑contract audits but the macro landscape of the region.

The gap between sectoral growth and real guarantees remains wide. If Srinivasan is right, though, the day may come when “seizing an oil rig” is pointless—without the cryptographic key it is just a heap of illiquid metal, impossible to sell or use lawfully in the global digital economy.