What is survivorship bias?

Survivorship bias is a fallacy that distorts analysis by relying on a skewed sample. The term is often used when assessing business or investment performance. The distortion arises when conclusions are drawn from the “survivors” while excluding the “dead”.

For instance, the story of one company’s success can be misread as a universal recipe for achieving a goal. Cases with the opposite outcome—projects that failed and “died” despite following the same principles as the “survivors”—are ignored.

Where did the idea originate?

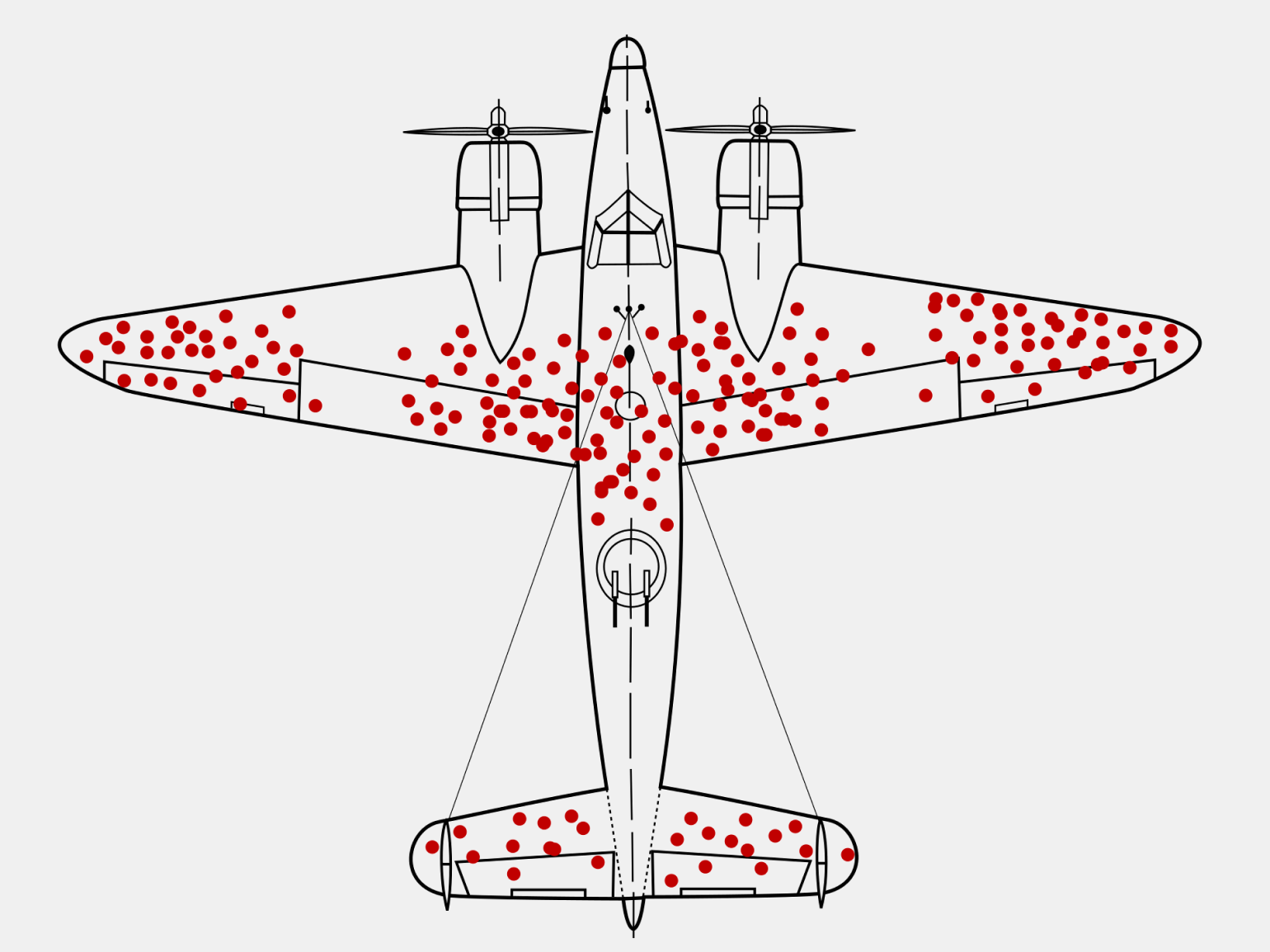

During the second world war, the mathematician Abraham Wald worked in the Statistical Research Group organised by the US military. He was tasked with reducing bomber losses using data on aircraft damage.

The initial plan was to reinforce the most damaged parts of the fuselage. The military’s logic ran: protect the areas with the most bullet holes.

Abraham Wald offered a radically different view. He observed that if a plane made it back to base, the damage it sustained was non‑critical. Reinforcement was needed where there were no holes—those were likely the hits that kept other bombers from returning.

This is the classic example of survivorship bias: drawing conclusions from incomplete data on aircraft that survived rather than those that were shot down.

A standard case of this distortion in traditional markets is the S&P 500, which comprises shares of the 500 largest US public companies.

Many assume the index’s moves reflect the broader American equity market. Yet just seven firms (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia and Tesla) account for about 30% of the index’s total market value. That means the index’s price is heavily swayed by a handful of companies versus the other 493.

How does survivorship bias apply to cryptocurrencies?

The crypto market, like traditional finance, is prone to the same cognitive traps. Consider data from CoinGecko.

Its analysts say that more than 50% of all cryptocurrencies listed on the platform have ceased to exist. From 2014 to 2023, 14,039 out of more than 24,000 projects “died”, even as total market capitalisation rose to $1.8trn over the same period.

Thus the claim that crypto as a whole is a safe place to invest is a survivorship‑bias error. Few account for the vanished companies, projects, coins and users who went broke over the same years.

Memecoins offer another illustration. According to CoinGecko, which tracks around 600 such tokens, the category’s capitalisation as of May 2024 exceeded $51bn. Yet few pay attention to “dead” or untracked tokens.

In early May 2024 alone, the Solana network saw a record number of native SPL tokens created in a single day: the daily figure approached 15,000.

Following such examples, some investors will always believe crypto teems with lucrative opportunities; others will deem the industry too risky. Both can be right and wrong at once if they rely on only part of the available evidence.

Consider, too, tales of standout crypto traders. In early April 2024 a user nicknamed Larp Von Trier increased his stake 23,770‑fold on tokens with market caps below $5,000 on Base, turning $353 into $8.39m in six days.

Reading such stories can prompt the mistaken belief that illiquid assets are excellent vehicles for investment. Few disclose how much money is lost in these markets.