Your transaction @#$%. Why censorship is spreading in crypto

Few crypto projects can afford to operate in conditions of full decentralisation, one of whose key hallmarks is resistance to censorship. Any community is compelled to follow its own rules and principles—and the laws of the state.

Attempts are under way to remove the human factor from blockchains, but experiments combining cryptocurrencies and artificial intelligence are still in their infancy. Social consensus and the personal choices of network participants will therefore retain priority for a long time yet.

ForkLog examined the arguments advanced by both supporters of censoring crypto transactions and their opponents.

Censorship at the blockchain layer

A striking instance of blockchain censorship is the behaviour of Ethereum validators. When, in 2022, America’s Treasury put ETH addresses linked to the Tornado Cash protocol on its sanctions list, some network participants refused to process transactions associated with the mixer.

Such decisions are their personal choice, unrelated to the Ethereum protocol itself, but for this very reason researchers at the Federal Reserve Bank of New York concluded that Vitalik Buterin’s project is surprisingly susceptible to censorship.

Although a blockchain can operate impartially, some of its participants choose to follow sanctions. Validators use intermediary services that propose profitable transaction ordering, skimming a small fee for the “approval” of a block.

This practice is known as maximal extractable value (MEV).

The social contract

The ecosystem of any major crypto project consists of many groups of users, sometimes with opposing aims and values. Yet all of them operate within the same blockchain, protocol and smart contracts.

As with Ethereum, we see that some infrastructure participants chose to censor, even though the network itself does not mandate it. In essence, this amounts to a social consensus on sanctions.

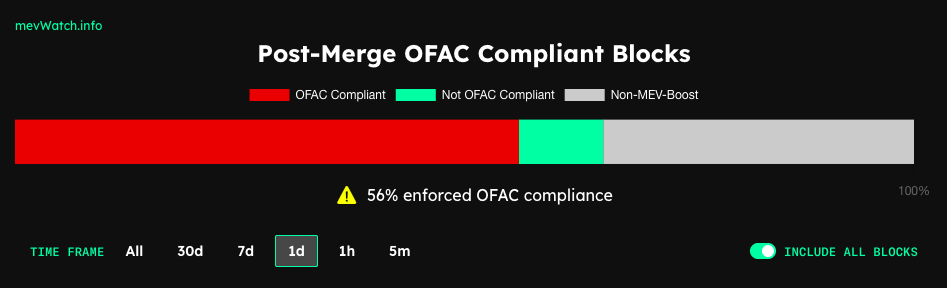

As of the evening of 17 September 2024, 56% of Ethereum transaction blocks over the preceding 24 hours were censored.

Every wallet holder, trader, exchange, project, investor, miner, validator and liquidity provider in decentralised-finance applications operates in the same place. How a project is built matters less than the social contract.

If the community were to decide that censorship on Ethereum warranted a move to another blockchain, validators would be expected to react. Deprived of income, many would likely agree to skirt sanctions to keep users.

Some still believe developers, large investors, miners and validators wield more influence than ordinary users and can decide unilaterally which changes to make. This is not always so. In essence, the rules are determined solely by what buyers and sellers accept as a legitimate asset worthy of their time and money.

According to experts at Mixer.Money, the use of cryptocurrencies to circumvent sanctions demonstrates states’ inability to adapt to new technological and economic realities.

“Even the staunchest opponents and skeptics are forced to acknowledge the power of cryptocurrencies, their resilience and reality. Accordingly, this sphere, like all others, simply must be regulated. The problem, however, is that this phenomenon is nothing like classical financial instruments, and so the regulatory legislation must differ as well. For now, though, the movement follows the well-trodden path—control, censorship, and, when those are impossible, total bans,” the service’s analysts believe.

The MakerDAO case

A current example of a community willing to accept censorship at the expense of decentralisation is MakerDAO, issuer of the largest algorithmic stablecoin, DAI.

In late August 2024 the company announced a rebrand and the issuance of new coins to replace the old. From 18 September one DAI can be exchanged for one USDS, and one MKR (the protocol’s governance token) for 24,000 SKY.

The new “stablecoin” is slated to include address-freezing functions, as in the centralised USDT and USDC.

The public announcement did not mention this, yet the topic surfaced anyway, and MakerDAO founder Rune Christensen had to disclose the plan’s details.

He noted that stablecoins face their own trilemma: simultaneously achieving a dollar peg, decentralisation and large-scale adoption is impractical. For the last of these, a mechanism for regulatory compliance is needed. Hence the freeze function in USDS tokens.

This suggests it is extremely difficult to scale projects without meeting regulatory requirements. Moreover, in Christensen’s view, such an approach enables new products based on passive income generated by buying government bonds.

Put simply, to gain additional earning options one must enter the US government-debt market—with all that entails. “Classical” stablecoins such as USDT have reached the same model, acquiring American government securities in exchange for loyalty.

In the end the plan envisages DAI giving up its dollar peg in exchange for decentralisation, and USDS giving up decentralisation in exchange for a dollar peg.

Experts at Mixer.Money believe this trend in the global market will only strengthen.

“So long as countries’ laws can be interpreted, as in the case of Pavel Durov, in favour of the state, any large-scale decentralised business immediately enters the risk zone,” the company’s representatives conclude.

Conclusions

Crypto’s growth has shown that decentralisation can be achieved only by the largest projects by capitalisation and number of active participants.

A small network is inherently vulnerable: a limited community is easier to influence from outside, however elegant the technology.

Yet scaling a project to serious size invites regulatory pushback—something not every project or community is ready to face. And for many, decentralisation is not especially important, or not needed at all.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!