Capitulation or evolution: why bitcoin miners are betting on AI

Bitcoin miners pivot to AI as margins collapse, selling treasuries and refitting data centres.

Bitcoin mining is undergoing the most radical transformation in its history. What seemed like a forced diversification amid market instability a couple of years ago had, by spring 2026, turned into a wholesale remake of the sector.

Traditional miners, long the guarantors of the network’s stability and security, are swiftly retraining as data centres operators for artificial intelligence. The pivot is accompanied by an unprecedented “sale of the family silver”: companies are liquidating accumulated bitcoin reserves to pay for Nvidia GPUs and to retire hefty debts.

Classic mine-to-hold operations are fading, giving way to hybrid infrastructure models. But what future awaits bitcoin if hashing becomes a low-margin by-product of renting racks to neural networks?

The end of the HODL era for public companies

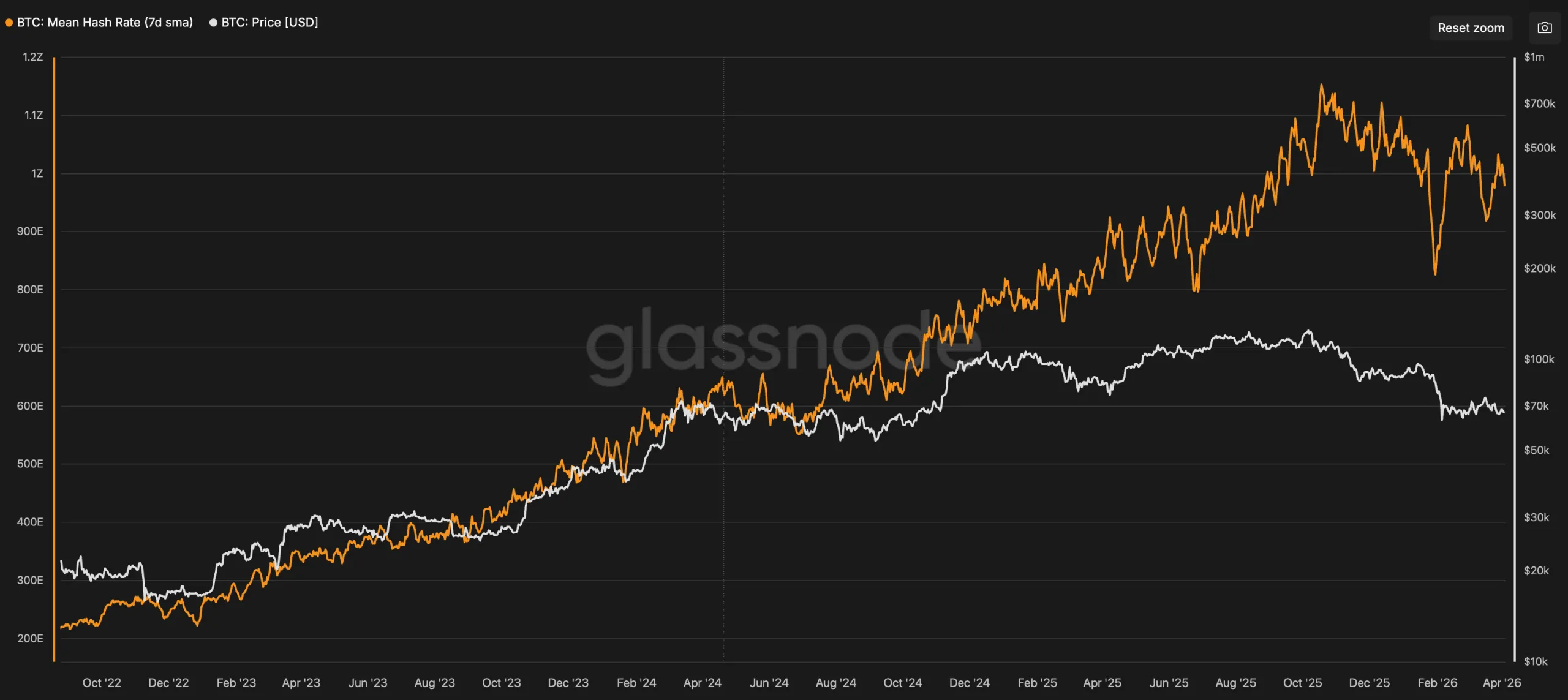

By spring 2026 the mining segment was in a muddle. Late last year the bitcoin network crossed 1 ZH/s. Yet the finances of the companies providing the hashrate had markedly deteriorated.

The industry ran into a “paradox of efficiency”: aggregate compute kept rising while hashprice sank to record lows of $28–30 per PH/s.

For comparison: in the third quarter of 2025 the figure hovered around $55; at the peaks of prior bull cycles it ran into the hundreds of dollars.

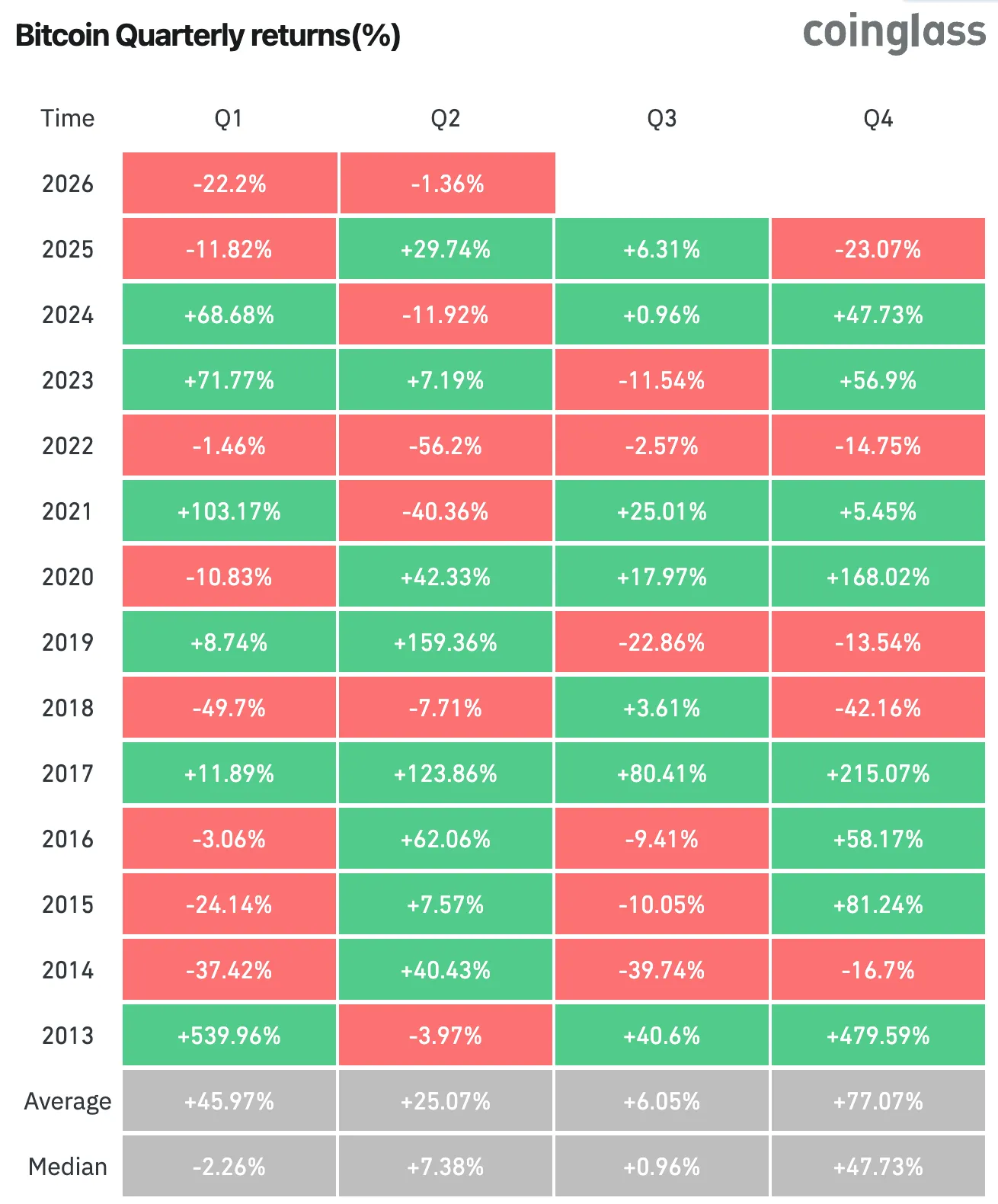

The first quarter of 2026 was bitcoin’s worst start in eight years. A 22.2% slide — from about $87,500 in January to below $70,000 by the end of March — upended the economics of most large miners.

Over the past six months the asset fell by more than 40%. In such conditions, the “mine and hold” strategy (or HODL) ceased to be effective and now threatens many companies with bankruptcy.

According to CoinShares and TheEnergyMag, the industry is in the throes of a broad capitulation — one masked, for now, by the inertia of large infrastructure projects and long-term power contracts that prevent firms from simply pulling the plug.

The numbers are unforgiving

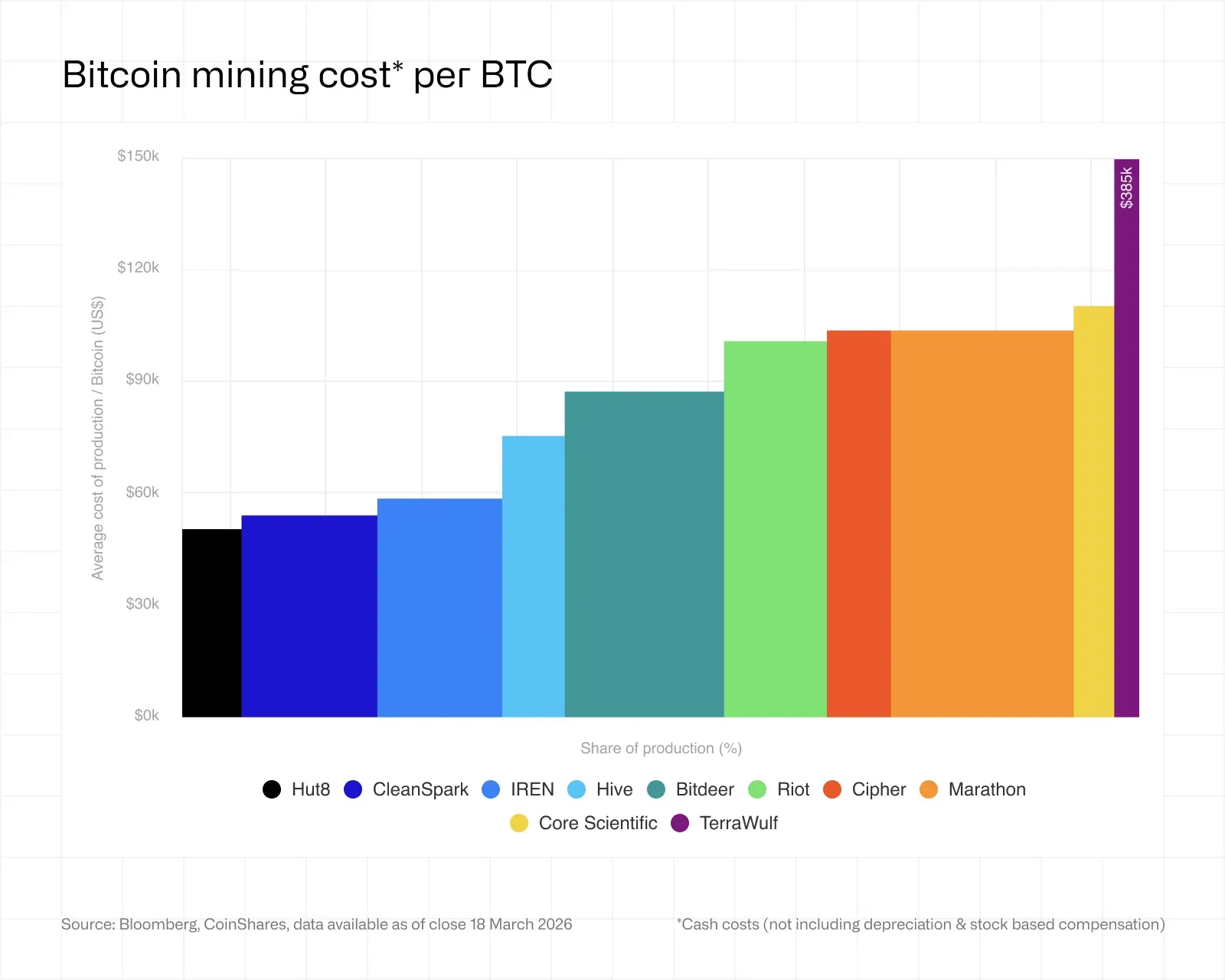

For most publicly listed miners, bitcoin production has turned loss-making.

In the fourth quarter of 2025, the sector’s weighted-average all-in cost to mine one bitcoin rose to $79,995. With the market price near $70,000, each coin minted was generating almost $10,000 in net losses.

The industry faces a systemic crisis driven by several forces at once.

Fee income is meagre

Last autumn, difficulty hit an all-time high, yet miners’ fee income dropped below 0.7% of the block reward. Bitcoin is used mainly for large-value settlement, and on-chain activity remains subdued.

The fee bump from the Runes protocol proved short-lived.

Regulatory pressure and energy costs

Power tariffs are creeping up in many countries. In the first quarter of 2026, average global household electricity prices rose 9.8% year on year.

There were added headaches in Texas, the biggest mining hub. Senate Bill 6 stripped miners of “priority customer” status.

They must now allow the grid operator ERCOT to curtail equipment remotely during peak loads and emergencies — a constraint that cuts uptime and heightens operational risk.

Heavy debt loads

To scale aggressively and survive the bear market, companies issued convertible bonds apace. In a year, aggregate debt of public miners swelled sixfold — from $2.1bn to $12.7bn. As revenues fell in 2026, servicing those obligations became a critical line item.

Cost structures and company health lay bare the scale of the problem:

| Company | All-in cost ($/BTC) | Electricity cost ($/BTC) | Debt and status notes |

|---|---|---|---|

| MARA Holdings | $153,040 | $64,703 | Significant equipment depreciation; debt secured by 53,000 BTC. |

| IREN (Iris Energy) | $140,441 | $34,325 | Low power costs, but a large volume of shares issued. |

| Riot Platforms | $170,366 | $49,196 | High spending due to a 1 GW build in Corsicana. |

| Core Scientific | $168,693 | $66,720 | Poor equipment energy efficiency; undergoing restructuring. |

| TeraWulf (WULF) | $471,841 | ~$50,000 | Metrics skewed by debt and high AI-related capex. |

| Cipher Digital | $231,980 | $41,047 | Tenfold increase in quarterly interest expense. |

| CleanSpark | $118,932 | $52,463 | Tight financial discipline; relatively modest debt. |

Cipher Digital is telling. After issuing $1.7bn of secured notes at 7.125% per annum, the firm’s quarterly interest bill leapt from $3.2m to $33.4m.

That looks more like the gamble of an infrastructure giant, betting that AI-compute revenues will cover obligations before default beckons.

A technological cul-de-sac and the limits of Moore’s law

Beyond finances, the industry has hit a technological ceiling. Progress in ASIC miners is slowing, reflecting the physical limits of Moore’s law.

From 2020 to 2025, flagship devices’ energy efficiency improved by 65% (from 31 to 11–13.5 J/TH). Now transitions to 3nm and 5nm chips cost far more, for gains of only 20–30% — and demand colossal investment.

Older rigs, including popular Antminer S19s, are unprofitable at today’s prices if power tops $0.05/kWh. Smaller operators without access to wholesale rates (retail averages $0.12–0.15/kWh) are being forced out.

New infrastructure standards, higher barriers to entry

Baseline requirements have shifted: conventional air cooling is giving way to liquid and immersion cooling.

Hydro setups add $500–1,000 to each machine, while immersion tanks require $2,000–5,000 of upfront capex per unit.

Prospective models such as S23 Hydro (claimed 9.5 J/TH) or Bitdeer’s SEALMINER (target 5 J/TH) could shore up margins. But money once earmarked for refreshing ASIC fleets is now flowing elsewhere.

The great pivot: AI as a lifeline

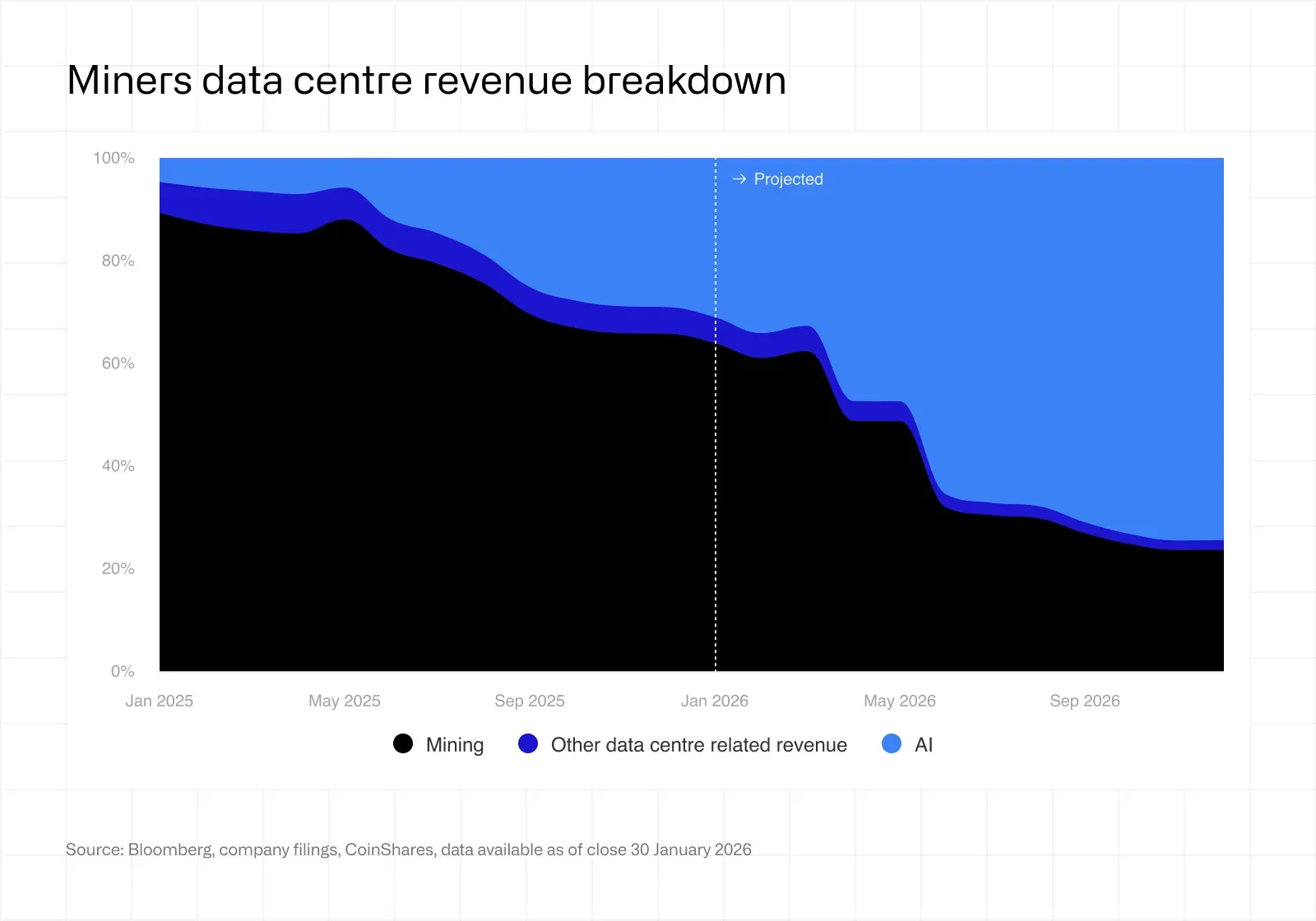

Miners’ turn to AI compute is a forced response to shrinking profitability. Wall Street analysts dub it “infrastructure cannibalisation”: firms dismantle ASIC racks to free power for GPU clusters.

The logic is simple: AI workloads yield 2–5 times more revenue per kilowatt-hour than securing the bitcoin network. Tech giants crave infrastructure, while miners command access to large blocks of cheap power and industrial-grade cooling.

Public markets have noticed. Shares of firms with high-performance computing contracts trade at 12.3x forward revenue; pure-play miners command just 5.9x.

Contract backlogs in this new line of business have already topped $70bn, says CoinShares.

How business models are changing

There is no shortage of telling examples:

- Core Scientific. A twelve-year contract with AI provider CoreWeave helped the firm recover from recent bankruptcy. AI-infrastructure revenue already accounts for 39%;

- Keel Infrastructure (formerly Bitfarms). In spring 2026 the firm completed a rebrand, changed its ticker and moved its headquarters to New York — a clear shift from bitcoin mining to serving traditional finance;

- TeraWulf (WULF). Buoyed by investment from Google, the company pivoted to AI. Mining now merely monetises surplus or idle capacity.

Breaking into the AI-provider market is capital intensive. A standard mining site costs $0.7–1m per megawatt, whereas a Tier 3 data centre for neural networks runs $8–15m per MW.

With borrowing costs high, companies are turning to their main reserves to finance such projects.

Selling down the treasure chests

Public miners, historically among bitcoin’s biggest corporate holders, are now exerting notable downward pressure on the price as they sell reserves.

The long-standing HODL playbook is losing relevance. Riot Platforms was among the first to abandoned it, routinely selling mined coins in 2025 to cover operating costs and fund a large build in Corsicana. According to vice-president Josh Kane, mining is no longer the end goal and now serves only as a tool to “maximize the value of megawatts”.

Others followed. Bitdeer fully liquidated its bitcoin holdings, redirecting capital to chip R&D and manufacturing. Notably, the company took the lead among public miners by installed hashrate.

Credit risks and market pressure

MARA Holdings, the largest corporate bitcoin holder among miners, is instructive. Confronted with heavy leverage and the need to fund AI infrastructure, management opted to liquidate part of its collateral.

In March alone MARA Holdings sold 15,133 BTC for roughly $1.1bn, using the proceeds to retire its convertible notes early.

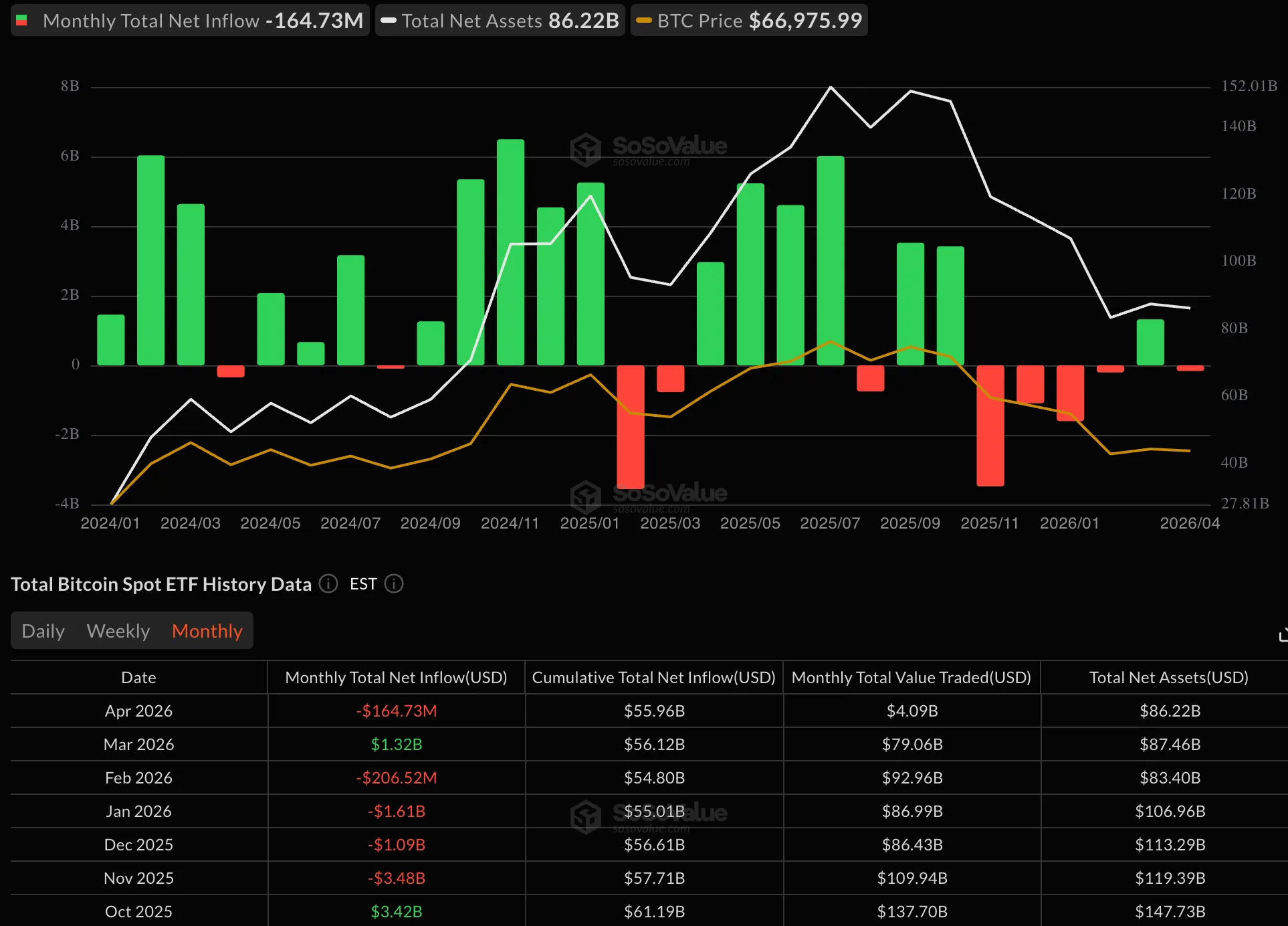

Buyer appetite is flagging as well. Spot bitcoin ETFs have seen net outflows in recent months, and the Coinbase Premium Index has turned negative.

By selling bitcoin to fund AI buildouts, miners are pressuring the price further — and making their core business even less profitable.

Geopolitics, the network’s pulse and creeping centralisation

Network metrics lay bare the industry’s woes. The hashrate’s drop from a record 1.16 ZH/s to 920 EH/s in spring 2026 is hard to dismiss as seasonal. The network logged three consecutive downward difficulty adjustments — last seen during the ‘great Chinese ban’.

Under regulatory pressure and shrinking margins, miners are shifting capacity to developing countries. Tough inspections in China’s Xinjiang and tighter rules in Texas have triggered a new migration wave. Firms such as HIVE Digital and Bitdeer seek inexpensive, stable hydro generation in Paraguay and Ethiopia.

Many in the market see this not as an exploration of new frontiers but as an effort to preserve traditional mining in isolated zones.

At the same time, the best, power-rich sites in the US and Europe are steadily moving under the control of tech giants — a looming risk.

The combined share of the US, China and Russia in global hashrate exceeds 60%. Concentrating rigs in the hands of a few corporations, whose business now hinges on AI-contract profitability, jeopardises bitcoin’s resistance to censorship.

Were a Microsoft, say, to offer corporate miners double the mining yield to retool remaining data centres for training language models, bitcoin’s hashrate could tumble within days.

$100,000 or oblivion

With the halving of 2028 approaching — when the block subsidy drops to 1.5625 BTC — mining’s future depends squarely on price. CoinShares reckons bitcoin needs to hold above $100,000 by year-end to restore acceptable profitability.

Failing that, several risks loom:

- Industry takeovers. Should prices stagnate at $60,000–75,000, firms that fail to diversify into AI risk hostile bids. Their infrastructure could be bought on the cheap purely for grid access.

- Cascading bankruptcies. Bitcoin’s realised price (the average purchase price of all circulating coins) is about $54,100. Deep drawdowns often test this level. A slide that far would be fatal for many leveraged players, triggering a chain of equipment fire-sales and treasury liquidations.

- Technological transformation. An alternative path lies in a broader on-chain economy. Widespread use of payments via Lightning Network, progress in layer-two solutions and BTCFi protocols could support miners — but adoption is lagging the revenue decline.

A paradigm shifts

The era of classical mining, insulated from the broader tech sector, is ending. Amid a new gold rush, the industry is transforming: a niche business is becoming a backbone for high-performance computing.

Abandoning HODL and selling down treasuries is the price of adaptation. To manage leverage and meet new realities, firms are tapping accumulated capital. Their future will depend on how well they balance bitcoin’s security needs with richer compute contracts.

Despite thinner margins and the risk of hashrate concentration, the pivot opens new opportunities. Tying into AI could make miners more resilient to crypto bear markets.

The line between bitcoin mining and servicing neural networks is blurring — irreversibly. The question now is which incumbents can secure their place in the new order.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!