After a blowout 2024, the decentralised physical infrastructure (DePIN) sector failed to replicate its success. Stagnation deepened from the second half of 2025, in step with the broader industry.

Despite a pullback in market capitalisation, notable structural shifts unfolded within the sector. Investors began favouring more mature teams capable of scaling products and generating revenue. The niche also drew impetus from more frequent outages at centralised providers such as Cloudflare, demand for training AI models and robots, and greater regulatory clarity.

In a new report, ForkLog examined how companies are reshaping to lift profits and which DePIN lines could strengthen in 2026.

Revenue is king

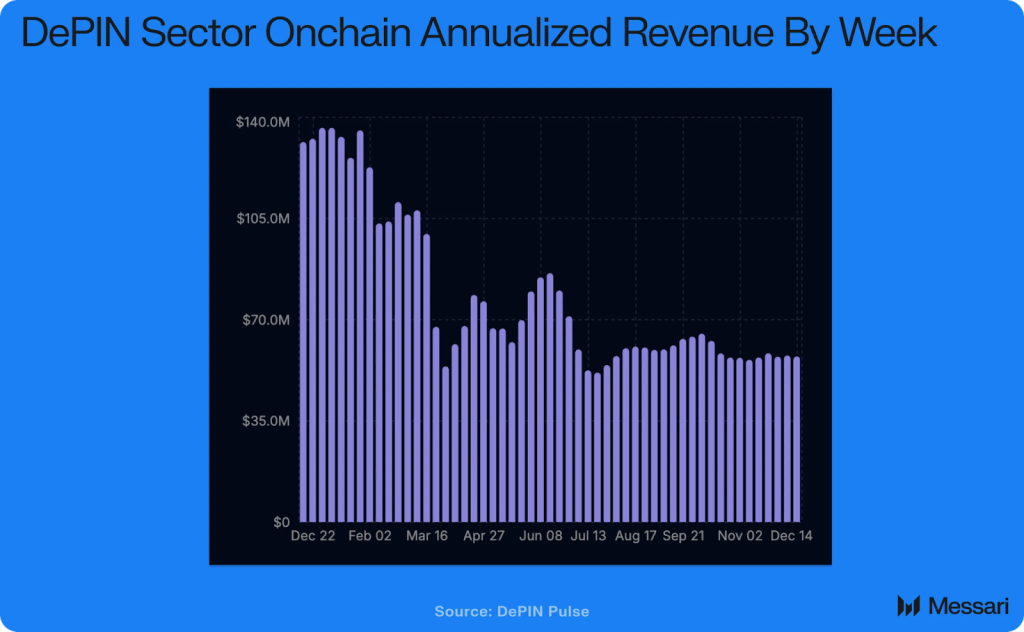

In 2024 the frenzy around DePIN stemmed from early successes, user-base growth and rising project-token prices. The sector also owed its popularity to AI, for which DePIN became an alternative source of capacity, offering GPU compute and data generation. However, according to a report by Messari, in 2025 the segment lost about 56% of its value.

The correction exposed weak spots in infrastructure firms and the shortcomings of valuing the industry using technical analysis and market capitalisation alone.

Analytics anchored in speculative assets obscured fundamental changes in the sector. At the end of a good run, analysts boldly projected growth to $150m in 2025. In their words, “so, probably, it did”, but verifying the outcome is nearly impossible given business specifics and accounting sleights. Much of the revenue is tallied off-chain and bundled with services only tangentially related to DePIN.

The downturn forced a more professional approach to valuing the niche, cutting through noise around token prices and teams’ grand claims. On-chain revenue has become one of the cornerstones of DePIN’s transformation in 2025.

Even as tokens of stronger projects such as cloud-compute platform Akash, mobile operator Helium and geodetic sensor network Geodnet fell over the year, their teams delivered robust revenue growth. Such conditions create a more attractive entry point for investors, with scope to improve 2026 outcomes, Messari reckons.

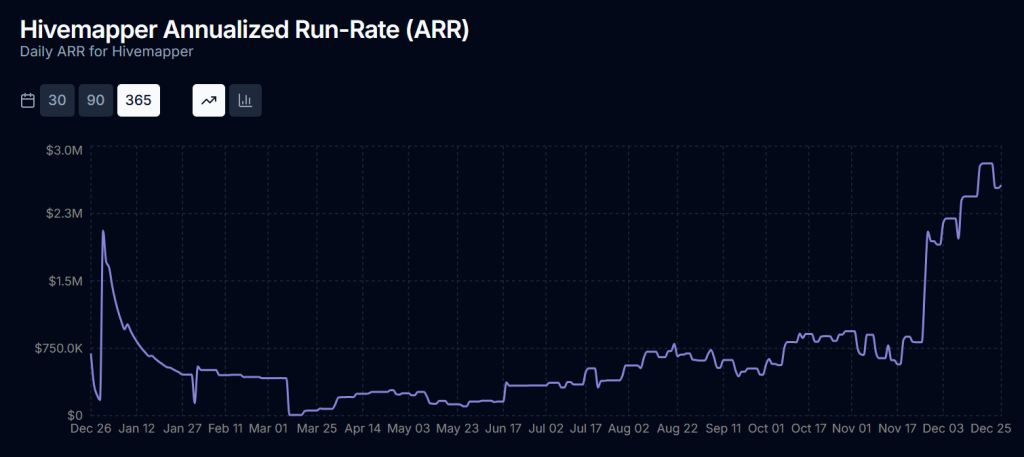

According to DePIN Pulse, from August to November 2025 the ARR of Hivemapper, a decentralised analogue to Google Maps, rose from $500,000 to about $3m. On 29 December the project’s 30-day ARR exceeded $1.3m.

Hivemapper’s active reorganisation, begun in 2024, allowed it to adopt the Map Improvement Proposal (MIP). It introduced a customer-centric approach to meeting demand for mapping data and increased map-refresh speeds required by some buyer categories.

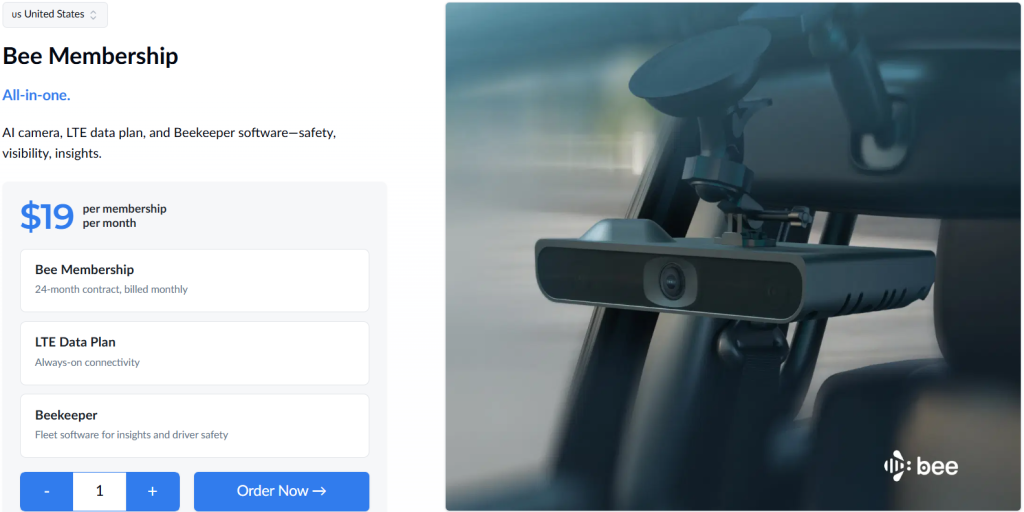

The startup also lowered the entry barrier for data suppliers—drivers who film roads using Bee devices. Renting the required hardware, software and membership cost $19 per month.

Investors backed the changes. In the same month Bee Maps raised $32m in a funding round led by Pantera Capital, LDA Capital, Borderless Capital and Ajna Capital.

Messari estimates DePIN’s projected annual revenue could double in 2026, topping $100m.

Main drivers:

- new TGE events for projects such as DAWN, BitRobot and Daylight may account for revenue on-chain in a timely manner while improving transparency;

- expansion of proven, profitable networks.

Scaling up and solving the demand problem

Pioneers assumed that surplus, community-provided hardware would let networks compete primarily on price for GPU compute, bandwidth and storage, while offering performance perks such as low latency. In practice, revenue proved modest.

Most DePIN networks effectively produce commodities for which building a durable sales channel has been hard. Messari believes the most profitable models will integrate the output into a full-cycle solution sold directly to the end customer—changing the business approach, as Hivemapper did.

In 2022–2023, leaders of several DePIN projects assumed the issue was a lack of sales and marketing support to place resources. Some protocols created subsidiaries and funds. The approach delivered only initial profits.

Analysts argue part of the problem lies in the nature of commodity businesses. Low margins and intense competition demand the lowest possible price and depend heavily on scale, which the DePIN sector has not reached.

In their view, the fix could be to:

- move into higher-margin products that can command premium pricing;

- expand the customer base to secure direct access to end users;

- remove the need for aggressive price dumping;

- strengthen long-term token value by linking it to multiple, higher-value economic activities;

- create a tight feedback loop between users and the network to match demand more nimbly.

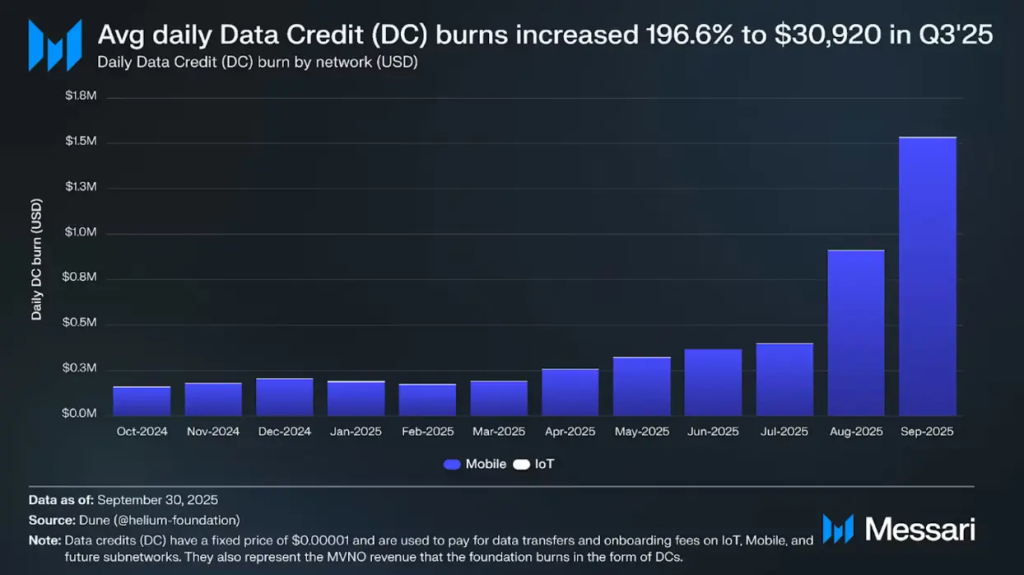

According to DePIN Pulse, the unchallenged 2025 revenue leader in the sector was Helium Mobile. Its 30-day ARR in December neared $21m; the daily figure on 29 December was $60,666.

Experts attribute the startup’s success in wireless primarily to vertical integration.

Rather than selling bandwidth as a generic commodity, Helium Mobile delivered a full consumer product, combining hotspots into mobile coverage. The company took on every stage of customer work—from device activation and billing to SIM cards and support.

This reshaped Helium’s economics. Messari estimates the mobile unit accounts for 53% of the burn of HNT and the internal currency used to pay for services, Data Credits (DC).

To maintain a deflationary economy, Helium Mobile burns 100% of its subscription revenue from the $15 and $30 monthly plans. Although offloading via Helium Mobile Offload burns far less HNT in dollar terms than a similar operation at centralised competitors, the “virtual operator” generates more revenue on a B2C model.

On 8 December, Helium Mobile Offload burned HNT worth $6,700 compared with $201,377 from operators’ offload. Instead of competing to sell bandwidth to corporate carriers, Helium earns higher margins by serving end users.

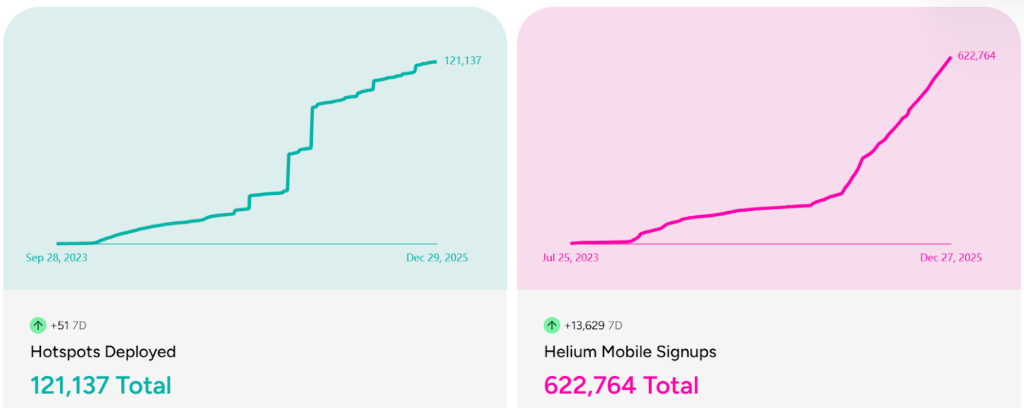

Data showing exponential growth in new users alongside the steady increase of installed nodes confirms the DePIN company’s success.

According to Helium, as of 29 December 2025 sign-ups reached 622,000 with 121,000 hotspots.

Optimism rose after claims by the SEC were resolved. In April the regulator closed its investigation into Helium developer Nova Labs.

In December the platform announced a partnership with Mambo WiFi to improve internet access across Brazil. Mambo WiFi’s network of more than 40,000 hotspots will significantly expand Helium’s reach in a country with uneven connectivity.

The quest to build distinctive products that increase value is becoming the new DePIN narrative.

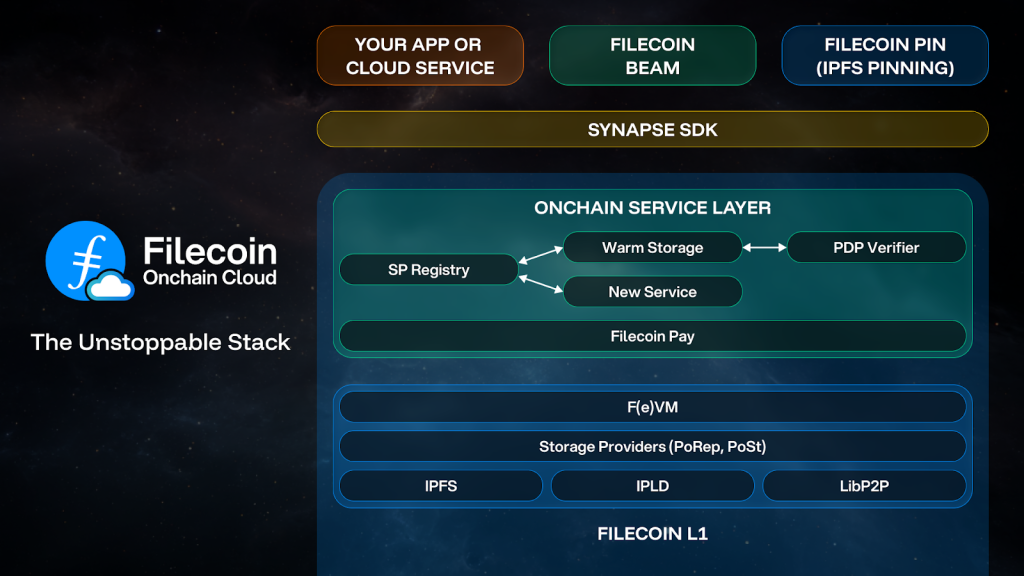

One of the sector’s pioneers—and the market-cap leader at about $1bn at the time of writing—is Filecoin. The project began as a decentralised alternative to cloud storage. In November 2025 the team announced Filecoin Onchain Cloud, taking on giants such as Cloudflare and AWS.

The launch aims to extend Filecoin’s capabilities, including in AI: integrating storage, data retrieval and on-chain payments for Filecoin Beam and Filecoin Pay.

Everyone wants energy—and AI

Amid more frequent outages at internet-infrastructure providers such as AWS, changes in DePIN are likely to catch the eye of users and investors.

On 18 November 2025, during the latest incident at Cloudflare, trading volumes in the DePIN category on exchanges rose by 25–40% on average. Activity was evident in FIL/USDT, AR/USDT and GRASS/USDT pairs on Binance and Bybit.

The volatility was brief but sent an important signal: markets understand the value of decentralised solutions.

A tilt towards business clients is under way in other subsectors. Decentralised energy supply and distribution solutions such as Daylight and Fuse are building their own vertical integrations.

Daylight focuses on renewables, installing solar panels and batteries. It encourages users to connect assets to the network with forthcoming token rewards.

The DePIN startup connects distributed energy resources, accesses energy and data through the network, and sells a differentiated product to energy buyers.

In October Daylight reported raising a total of $75m in a funding round led by Framework Ventures.

Another important player in the DePIN energy subsector—Fuse Energy—manages a broader stack. The company handles generation, retail and virtual-power-plant operations within a single system. Instead of selling capacity and data to independent participants, Fuse runs its own ENERGY network to attract supply.

The company uses token incentives to markedly increase the flexible capacity it can access while lowering acquisition costs. The savings then fund customer discounts and rewards across Fuse’s energy ecosystem.

Per DePINscan, Fuse also secured capital in December. In a Series B round led by Lowercarbon Capital and Balderton Capital, it raised $70m, lifting the company’s valuation to $5bn.

According to Messari’s experts, a vast seam of opportunity for DePIN lies in AI, specifically in the adjacent stack of decentralised infrastructure for artificial intelligence—DePAI.

The core is represented by a wide range of solutions, most of which are several years from large-scale enterprise adoption. Analysts think collecting real-world data to train robots already carries economic heft.

Many AI firms are already willing to pay for:

- navigation data;

- video streams;

- 3D maps;

- sensor logs;

- telematics;

- geospatial signals.

DePAI data-collection protocols can plug specific gaps in these areas, creating opportunities for near-term monetisation.

Several existing DePINs already generate real revenue from selling data, showing demand from AI is real:

- DIMO — vehicle telematics data;

- Geodnet — geodetic-sensor data;

- ROVR — drone imagery and aerial photography.

These networks sell data directly into industries that intersect with physical-AI training: mapping, navigation, geolocation, autonomous driving, simulation and world-model grounding. They already serve DePAI use cases—just not as specialised robotics data engines.

The next stage of evolution is DePAI networks built specifically for robot-grade data capture and training embodied AI.

Three in-development projects stand out as the first specialised DePAI data collectors:

- BitRobot. A decentralised platform for embodied-AI research and robotics data built on Solana. It unites robots, compute, datasets and contributors into modular subnets that generate real-world data, models and benchmarks to accelerate AI progress;

- PrismaX. The protocol aggregates high-quality multimodal interaction data, robot sensors and human-in-the-loop teleoperation to power the LLM;

- Poseidon. A full-stack data network focused on creating high-quality, IP-clean datasets for AI, with built-in consent, licensing and provenance. It targets humanoid robotics, autonomous driving and multimodal learning.

According to Messari’s analysts, in 2025 DePIN sat in an awkward middle ground for investors. Traders chasing dominant narratives disliked market conditions, while fundamental investors deemed the P/S multiple excessively rich.

Even so, the push for transparent accounting, sector development, liberalisation of regulatory oversight and token sell-offs could attract investors in 2026.

In this new environment DePIN is well placed for its next phase. Its defining traits—real-world utility, observable demand and rising revenue—align with the market’s direction. Execution remains the open question: whether DePIN networks can keep scaling revenue and grow into large, durable businesses.