Analyst Karim Helmi and the Coin Metrics team developed a new methodology for quantitatively assessing the assets at the disposal of Bitcoin miners. Its distinctive feature is the separation of miner activity and mining pools, enabling a more precise assessment of the coins at their disposal.

ForkLog presents readers with the translation of the second part of the article Following the Flows: When Do Miners Sell?. It discusses the impact of miners on Bitcoin’s price and on the exchanges that receive the largest share of mined coins.

- Contrary to popular belief, selling pressure from miners is modest and has little to no impact on Bitcoin and the broader market.

- Miners interact predominantly with exchanges Binance and Huobi, which have their own pools.

- The correlation between movements in Bitcoin’s price and the inflows to exchanges is virtually non-existent.

Miners are frequently criticised for pressing down the price of Bitcoin, but such claims are often unfounded. Sometimes they rest on imperfect metrics in which pool payouts are mixed with miners’ expenses, which misleads users.

An accurate assessment of the extent of miners’ selling impact is crucial for understanding the market. In the article Following the Flows: A Look at On‑Chain Miner Payments, Coin Metrics introduced a new methodology for evaluating miner activity, in which pool‑related wallets are structured. This approach allows users to distinguish between pool and miner activity.

In this article we refine our estimates using data on the relationships between miners and exchanges. This will help determine when and where miners sell their coins.

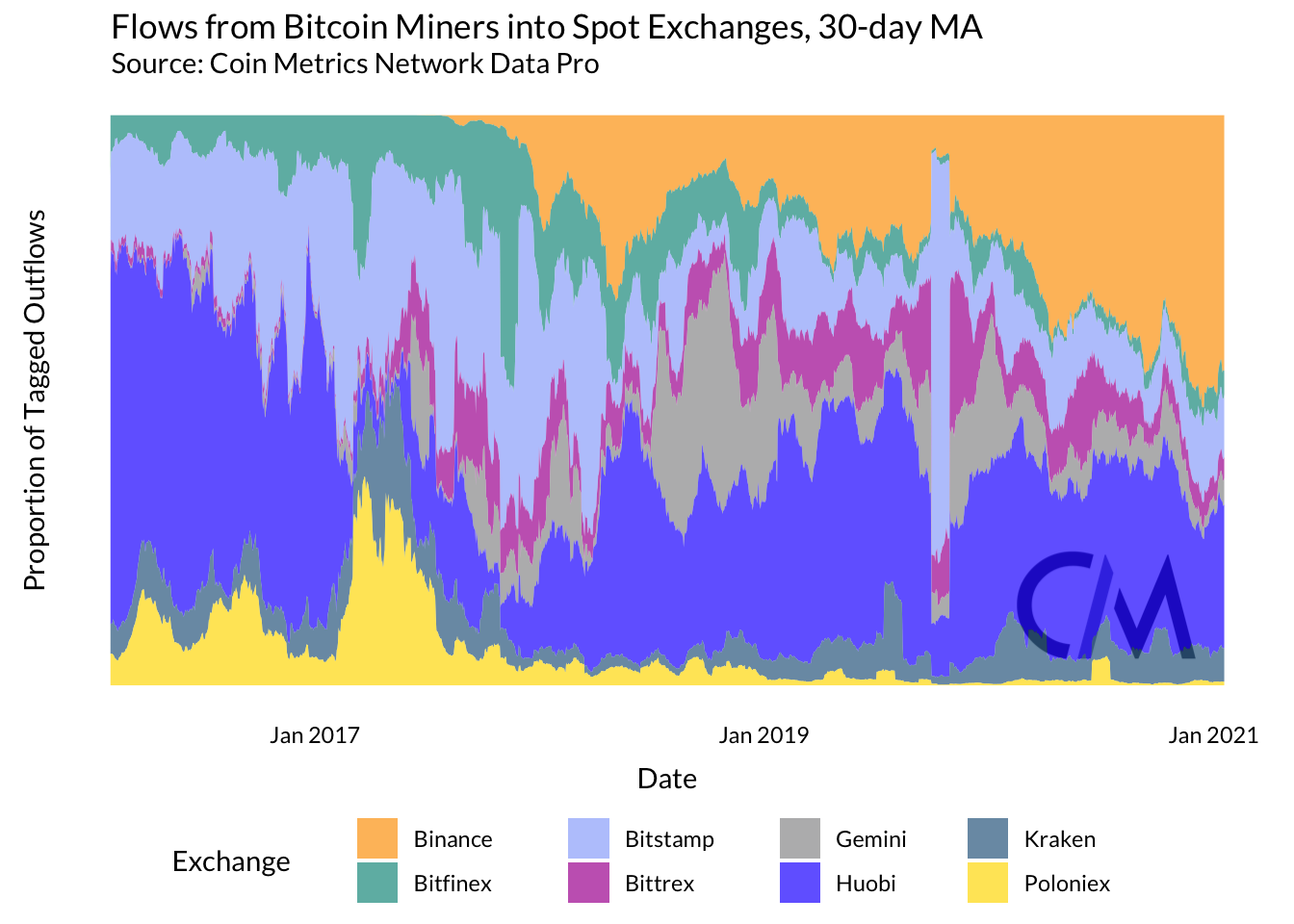

We found that among many exchanges miners predominantly favour Huobi and Binance. It was also found that flows of coins from mining‑related addresses account for a small share of total inflows to trading venues. At the time of writing, this figure stood at 5.5% and is unlikely to be a major source of market volatility.

Indicators of Miner–Exchange Interaction

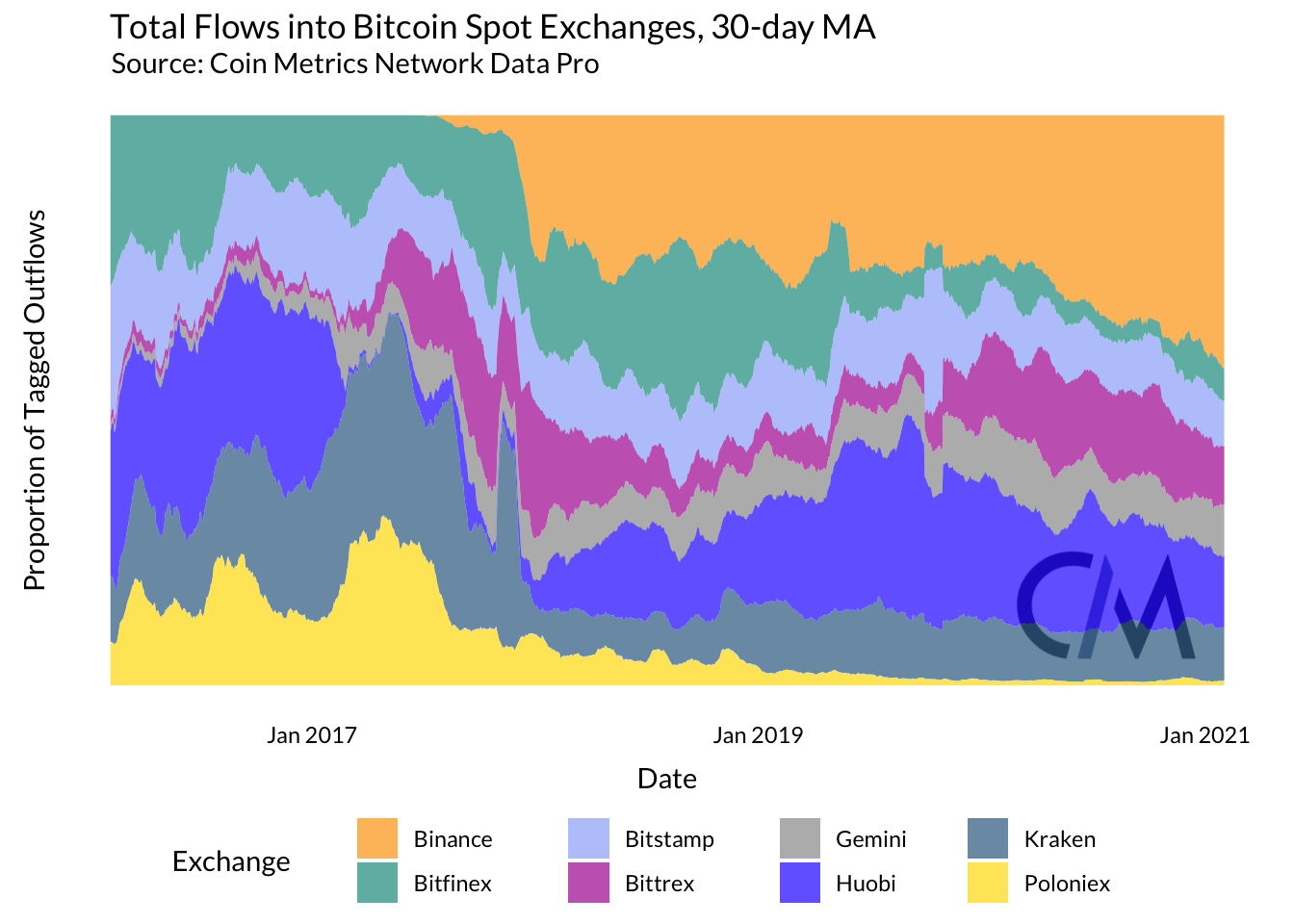

Inflows, outflows and coin-supply indicators provide useful information about market sentiment, the state of the exchange sector and network decentralisation. Because of differences in structure, the flow indicators for exchanges and for miners are built on two distinct clustering methods, each with its drawbacks.

Exchange flows are assessed using the common-input-ownership heuristic. This method is precise but requires at least one initial address from each exchange. It covers only a predefined set of trading venues. The results are also distorted by CoinJoin and [simple_tooltip content=‘Peeling chains are largely processes used by exchanges that involve breaking one large address into smaller addresses, with smaller sums. This fragmentation, or layering (peeling), helps minimise losses in case of hacks and cyberattacks.’]peeling chains[/simple_tooltip].

To begin trading on a centralized platform, users deposit coins that are held in custody by the exchange operator. Mining works in a similar way: participants share resources to increase their chances of finding a block. Coordination occurs through centralized mining pools. The latter receive freshly mined coins at addresses they control, and later distribute the funds among miners.

Flows from miners to exchanges are accounted for by Coin Metrics by clustering addresses according to their distance from coinbase transactions. Addresses that have received coinbase rewards (or 0-hop addresses) are marked as mining pools. Addresses at 1-hop that have received a payment from 0-hop are labeled as miners.

This approach is less precise than the common-input-ownership heuristic. However, it roughly reflects the structure of mining-pool wallets and offers broader coverage.

By combining these two approaches, one can determine where miners deposit their coins. This roughly corresponds to where they sell them.

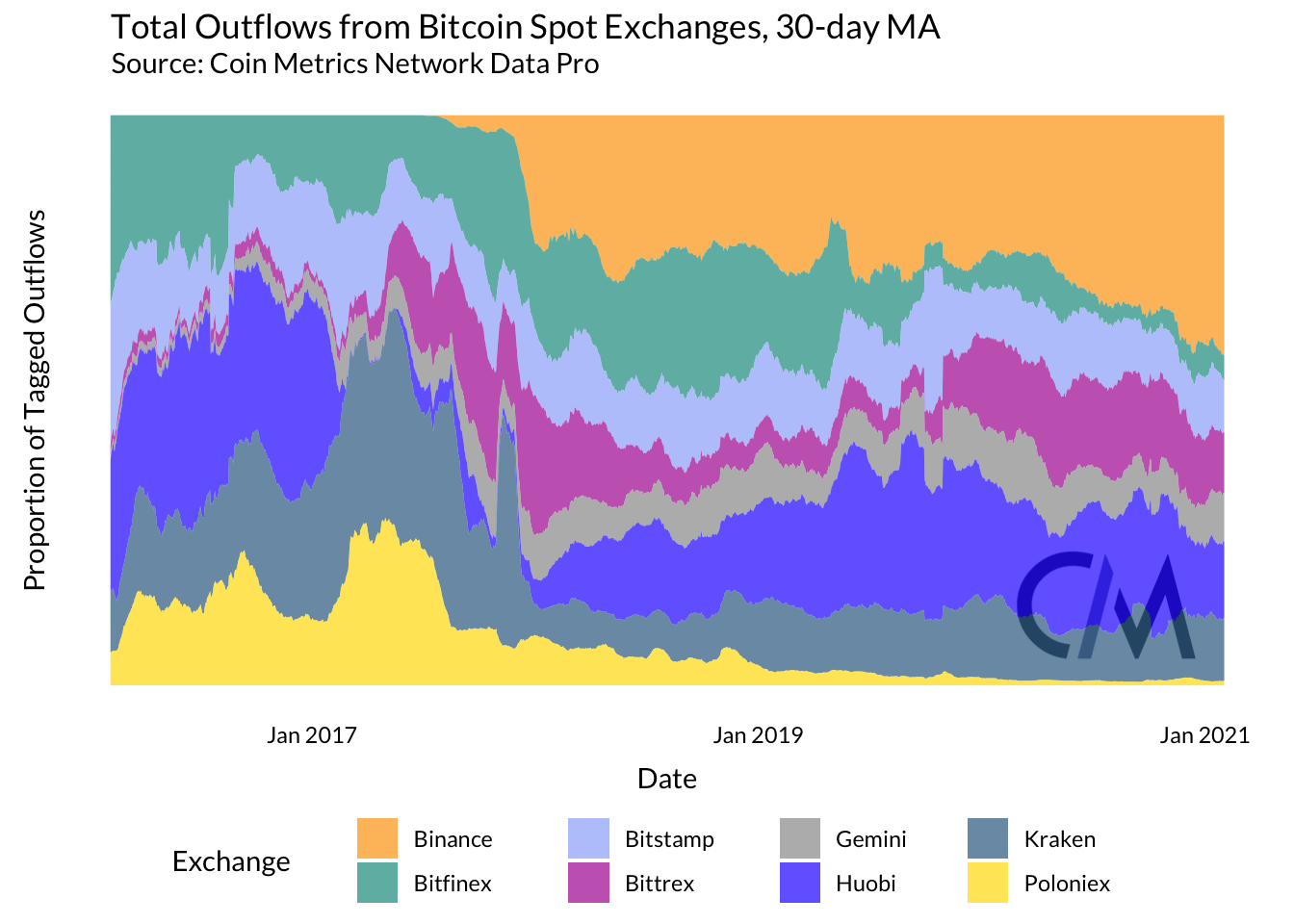

Flows from miners to trading venues largely track aggregated exchange inflows, but there are a few key differences. In this context, Binance and Huobi play the most significant role. The share of the latter is substantial in total inflows.

The results are straightforward: Huobi and Binance are the only exchanges in the sample that also operate mining pools. Both platforms have close ties with miners and a strong presence in Asia, where a large portion of mining capacity is located.

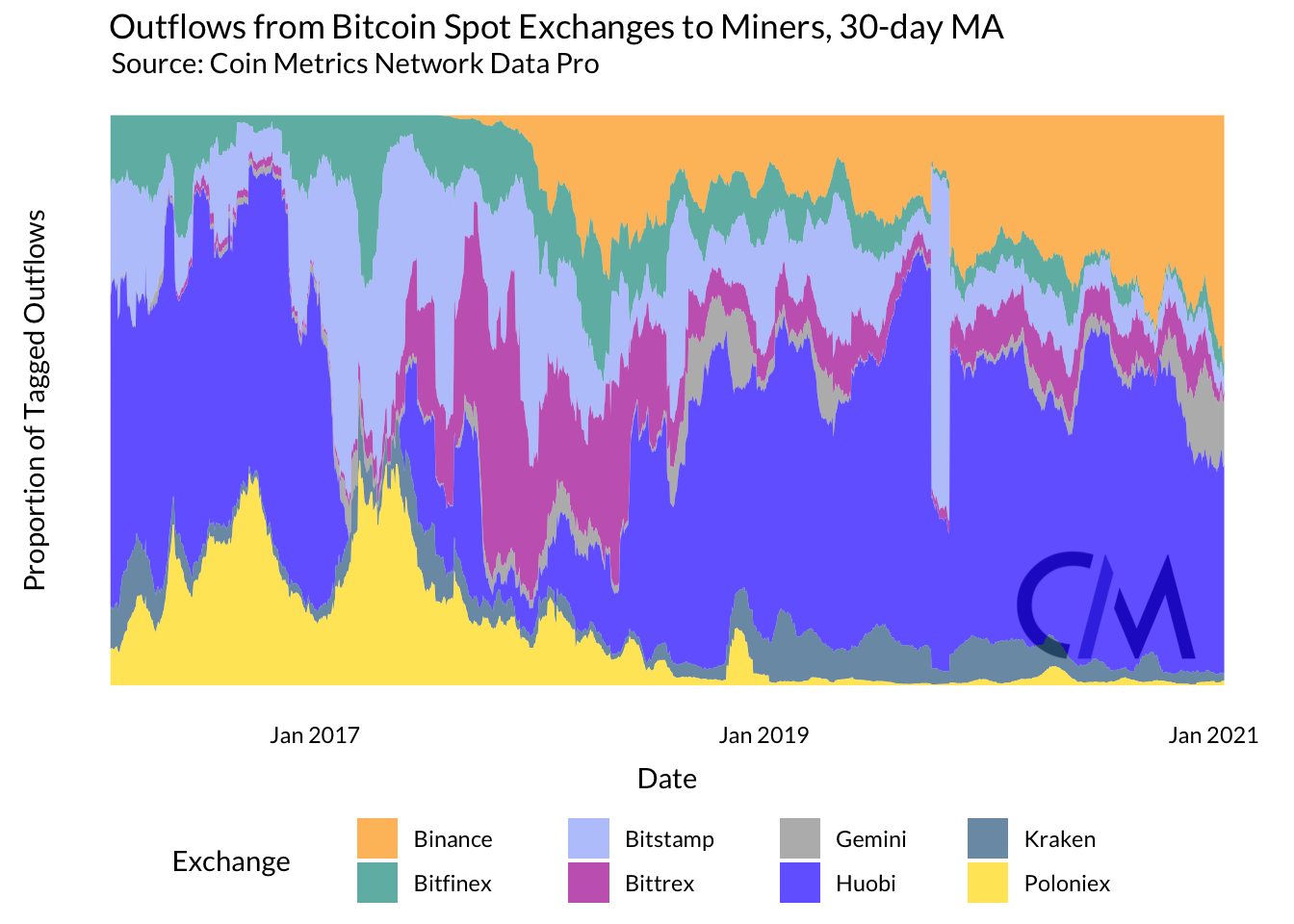

Binance and Huobi also dominate in the context of outflows from exchanges. This suggests miners also buy on these platforms.

As with inflows, Huobi dominates outflows relative to other exchanges that do not operate mining pools. Binance’s share in both cases is roughly comparable.

Looking ahead, flows between miners and trading platforms could serve as an indicator of the approximate geographic distribution of hash power. This metric would be based on the assumption that miners use exchanges in their region. To provide a complete picture, broader exchange coverage will be required.

Estimating the Magnitude of Miner Flows to Exchanges

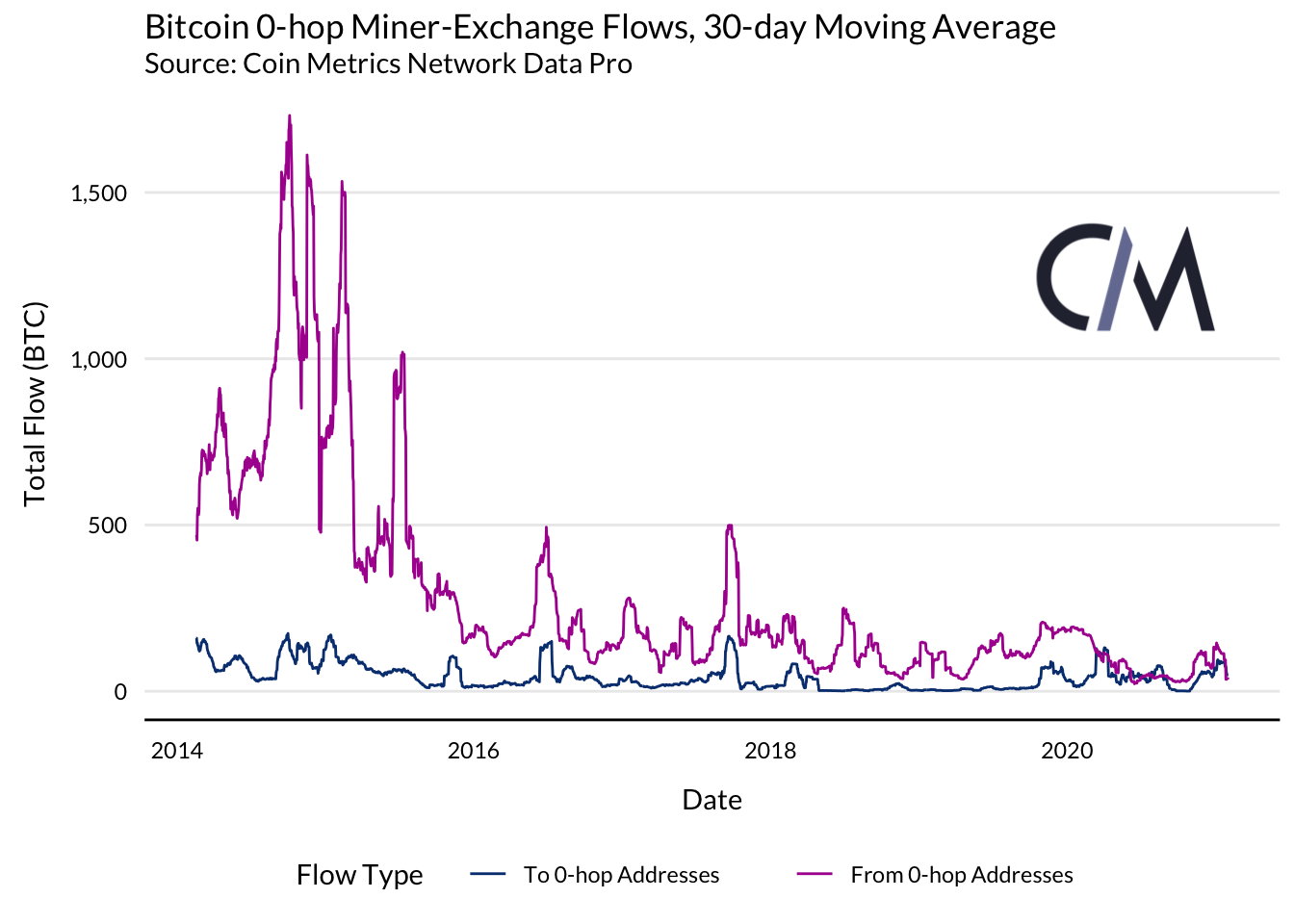

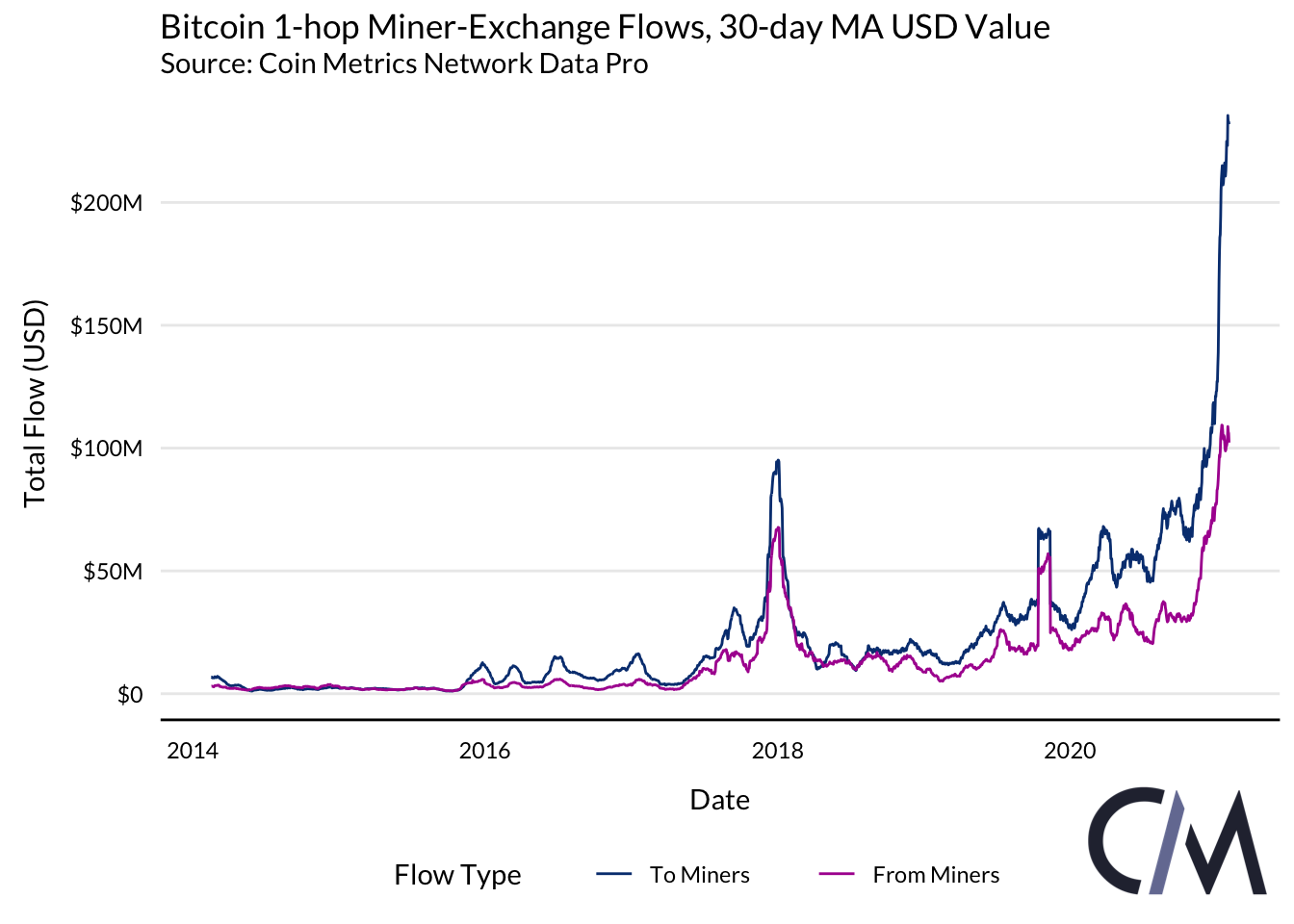

Our methodology can be used both to determine the structure of flows between miners and exchanges and to gauge their overall scale. In general, mining pools act as net depositors of funds on exchanges, though the amount they transfer daily is small.

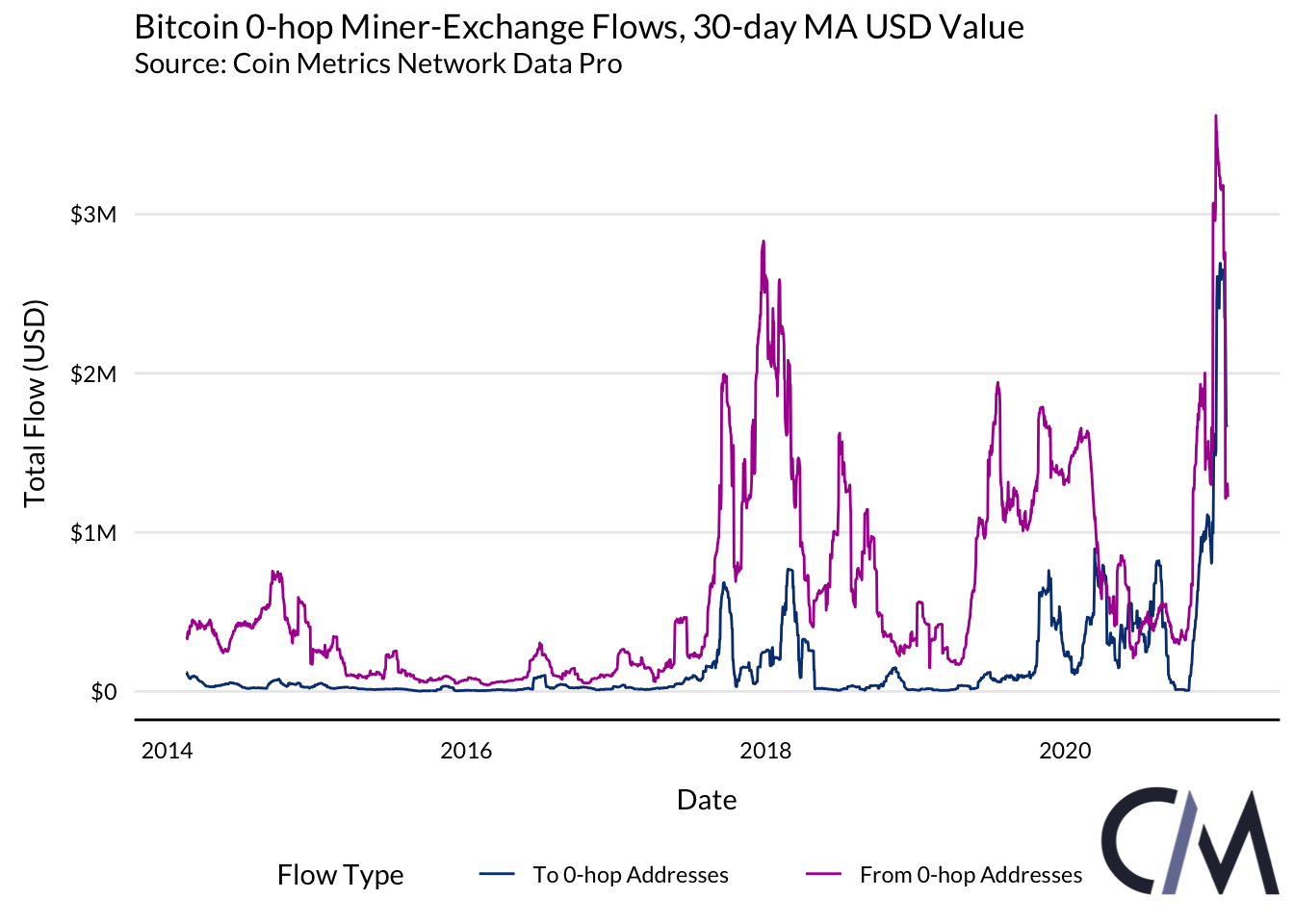

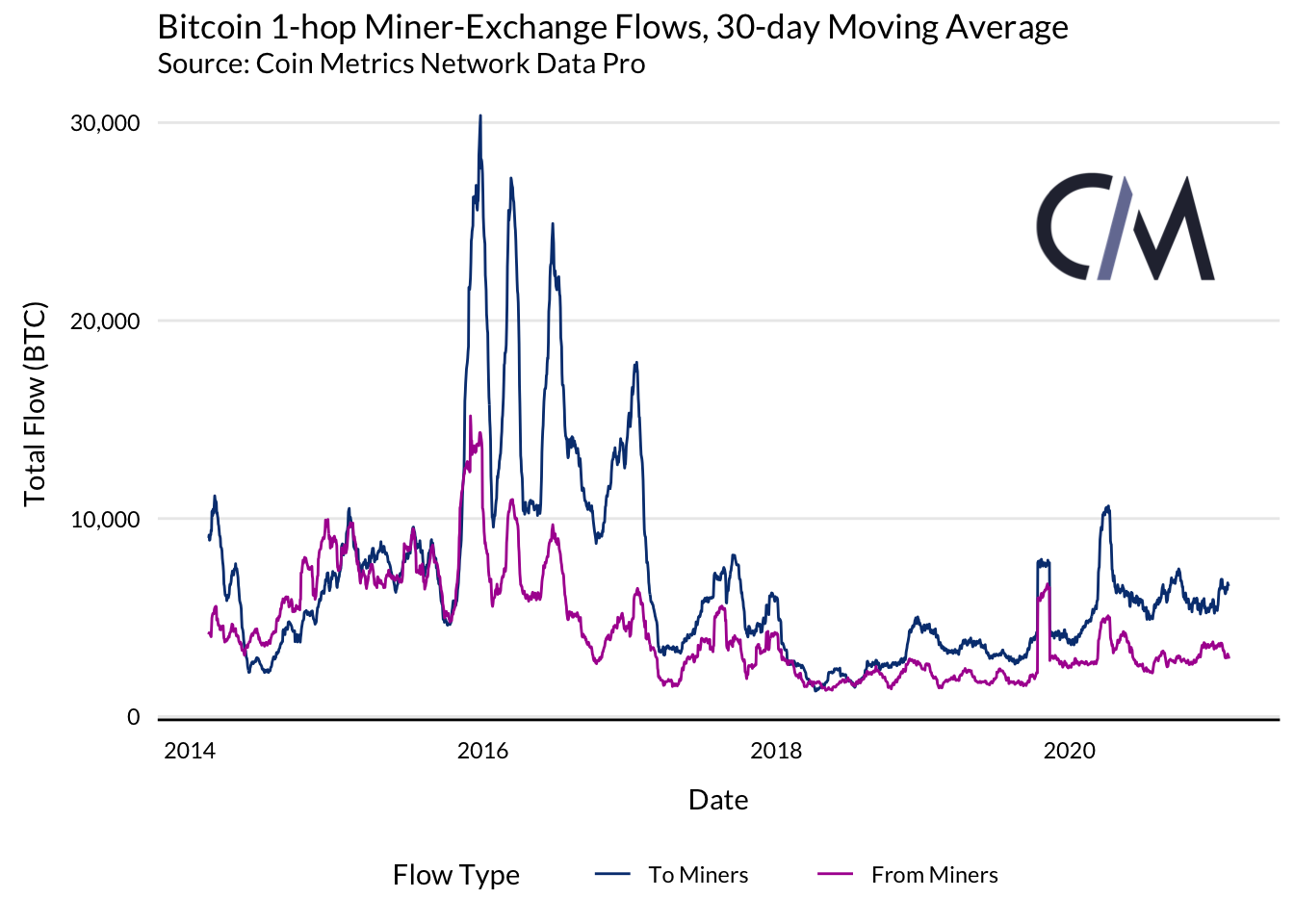

As with overall flows, movement between 1-hop addresses and exchanges is far more vigorous than between 0-hop. And though these flows declined since their peak in 2016, they have gradually increased since 2018. By contrast, USD-denominated flows have surpassed previous highs, reflecting Bitcoin’s price rise.

Strangely, our calculations indicate that miners appear to be net buyers. This is likely a methodological artifact arising from a variety of factors. For example, miners tend to sell coins mainly on over-the-counter (OTC) desks, which means funds are not sent to exchanges immediately.

Another possible factor is the concentration of funds among early miners. The issue can be addressed by excluding from the sample those who have not recently received funds from 0-hop addresses.

Finally, payments from mining pools affiliated with exchanges may be bundled with withdrawals from trading venues.

Features of Flows

Flows between exchanges and miners are clearer when viewed in terms of their components. Comparing them with aggregated miner flows and total exchange flows will help gauge their scale.

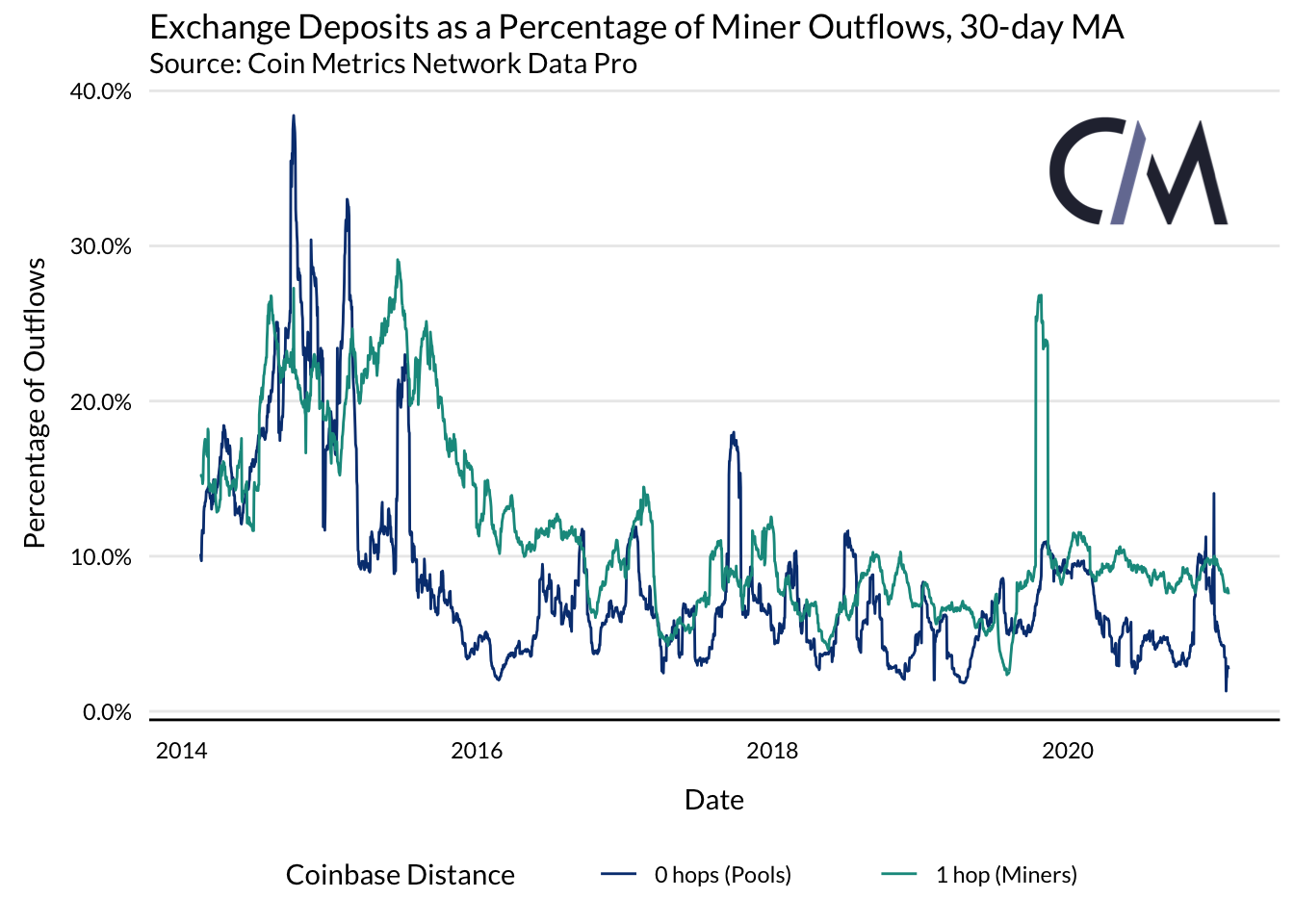

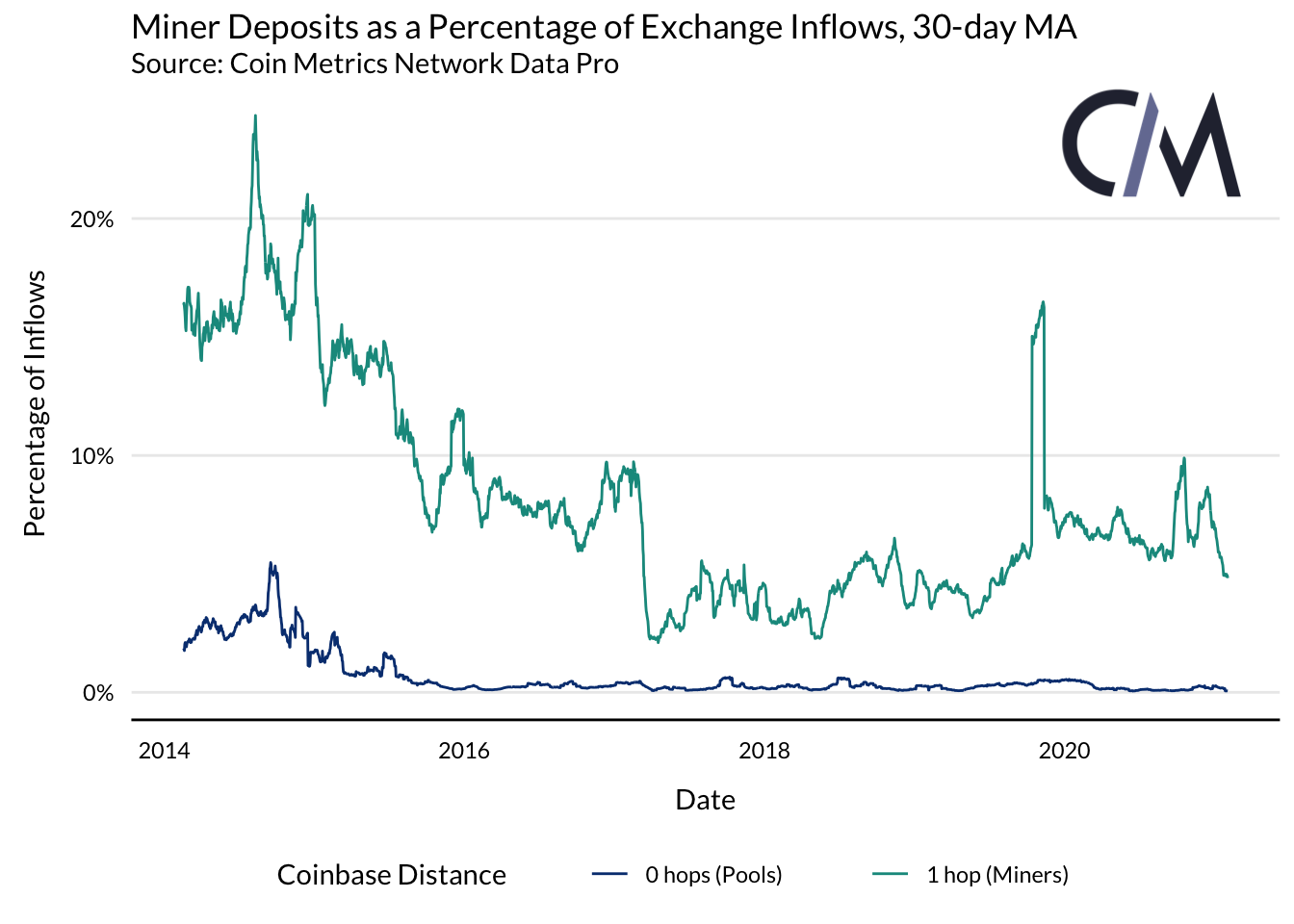

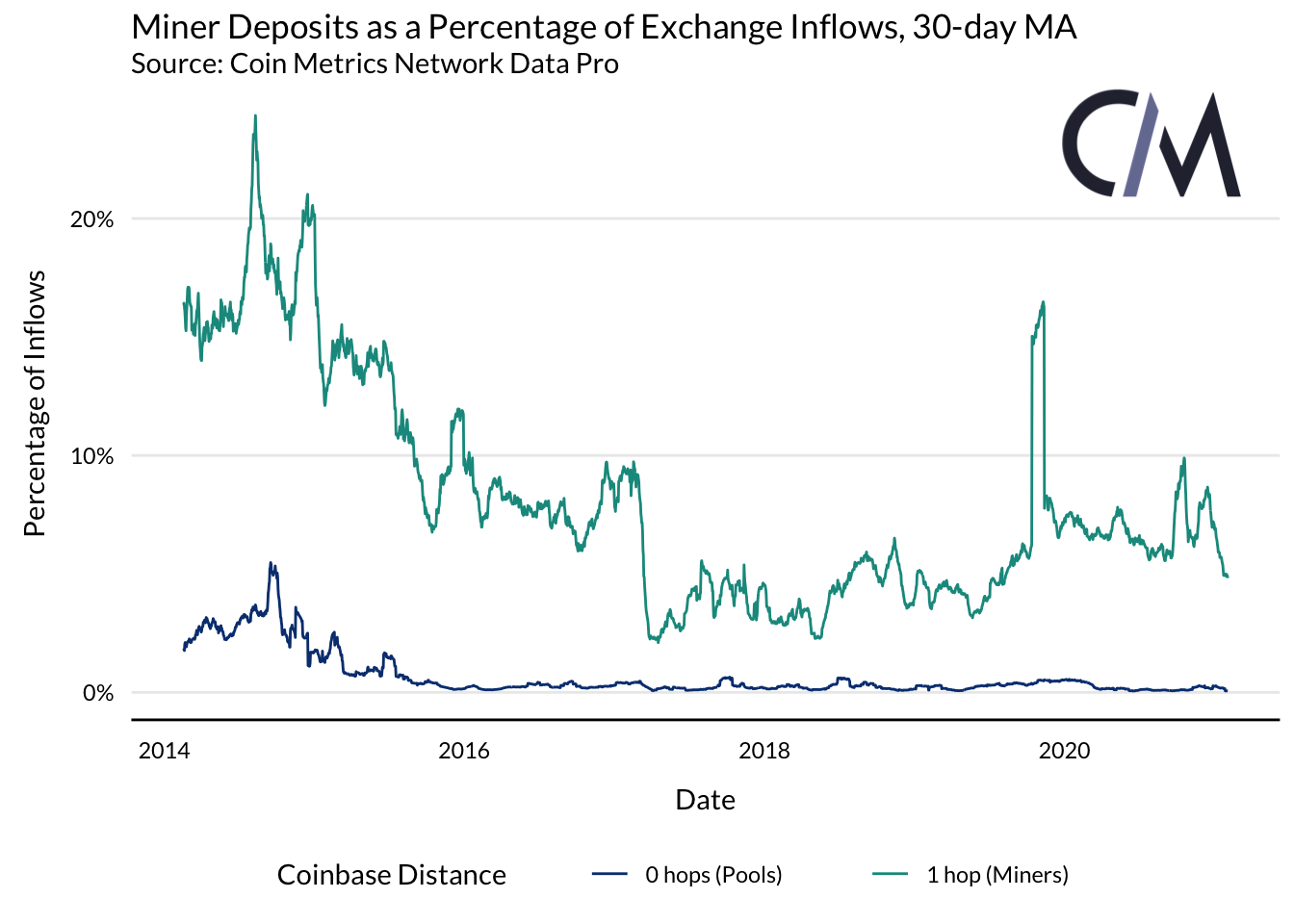

Transfers to exchanges typically amount to no more than about 10% of the total miner flows, although this metric has historically fluctuated. Deposits to exchanges also constitute a small share of pool flows.

Miner deposits to exchanges, which in theory should correlate with sales, have historically hovered around a single percentage over the past five years.

At the time of writing, the figure stands at about 5.5% of total inflows to exchanges. Since a large portion of mining output is sold OTC, this figure may be somewhat overstated.

Although flows between miners and exchanges are volatile, their fluctuations are not substantial in the context of total exchange flows. Movements between 0-hop addresses are also small, so there is no basis to link Bitcoin’s price volatility with miners’ selling pressure.

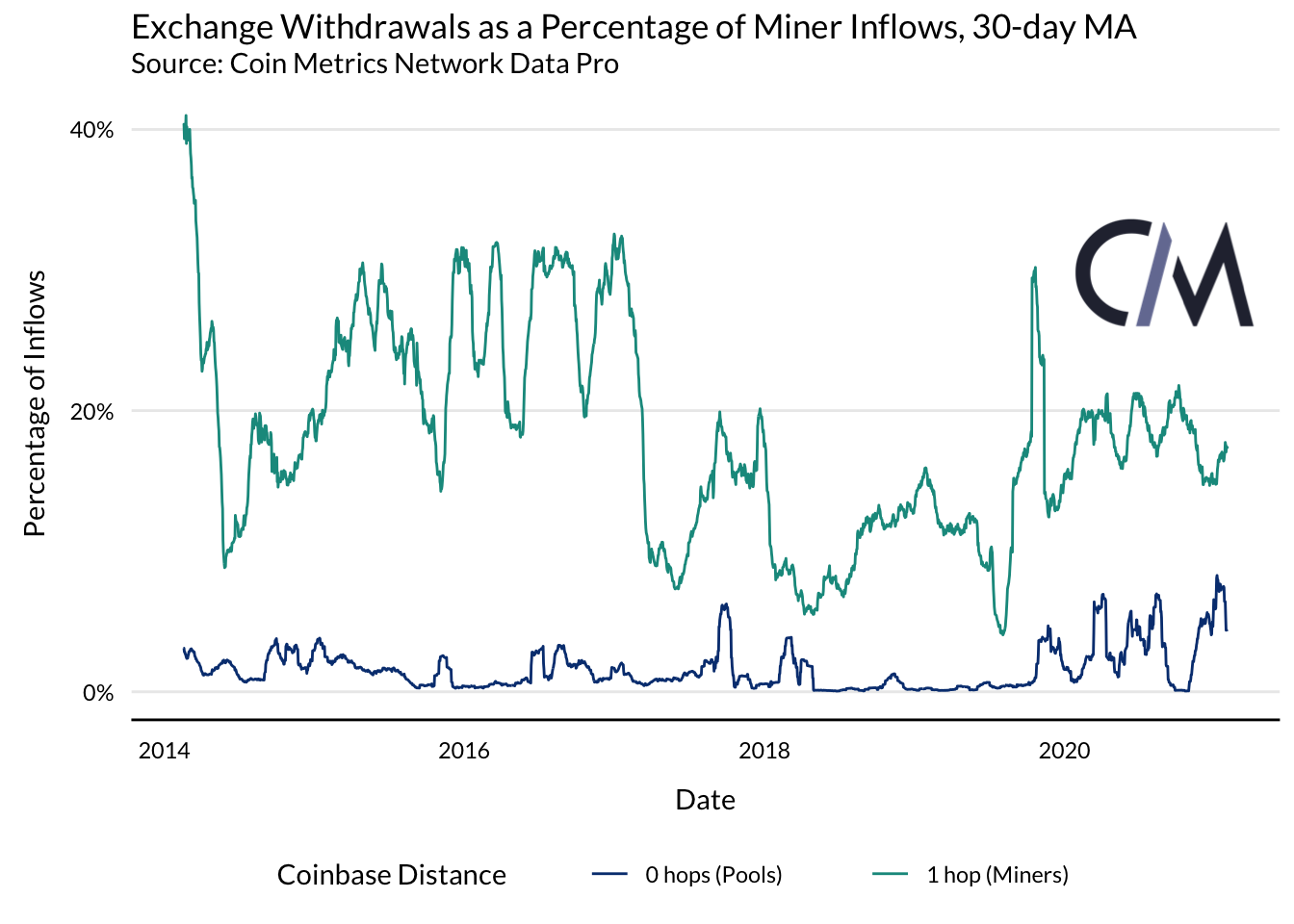

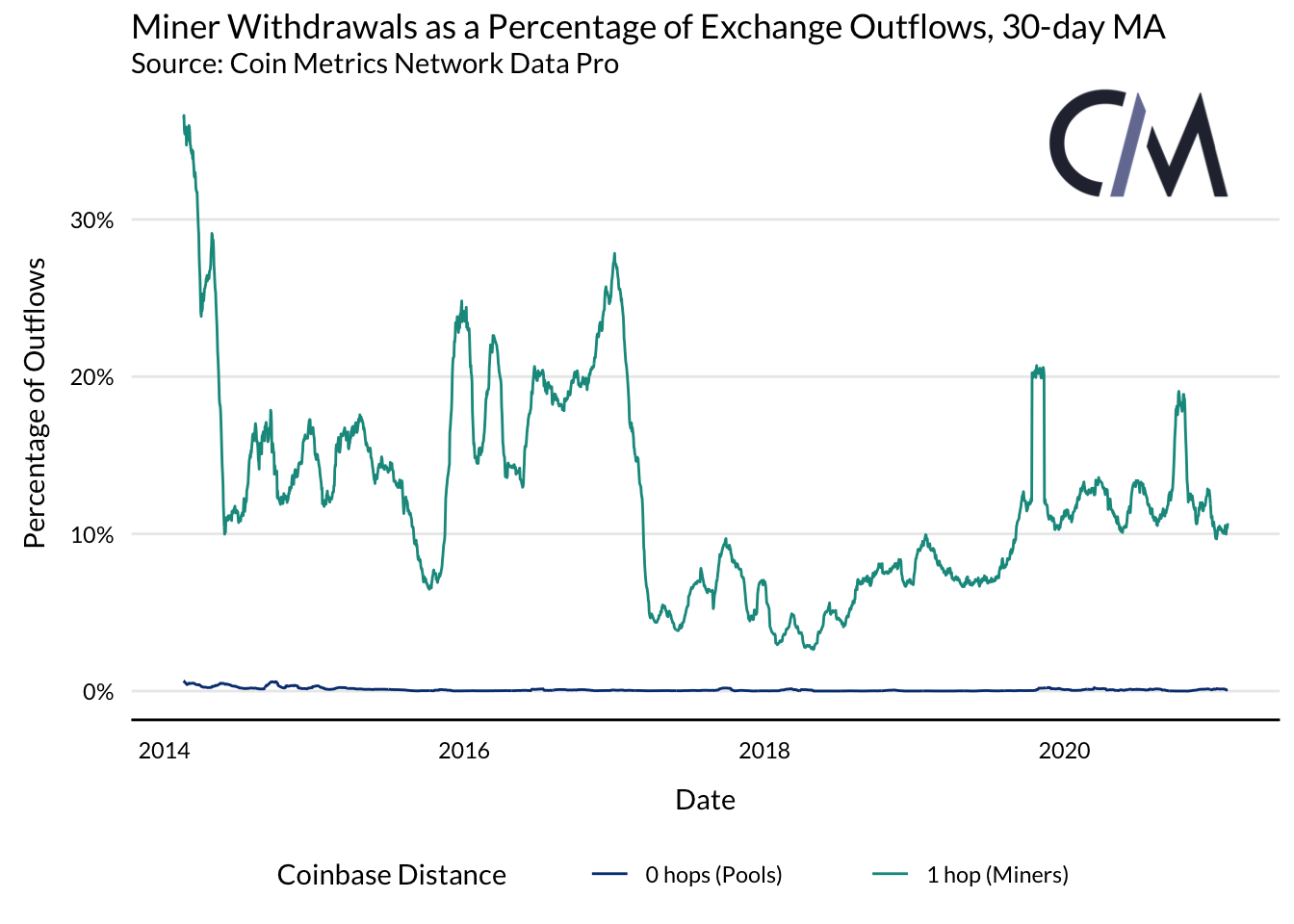

Miner withdrawals represent a more significant portion of total exchange outflows. Last year the figure remained above 10%. The discrepancy between this figure and the miners’ deposits share in inflows may be attributable to exchange‑affiliated pools, which may be closely linked to the parent company and make payments from overlapping addresses.

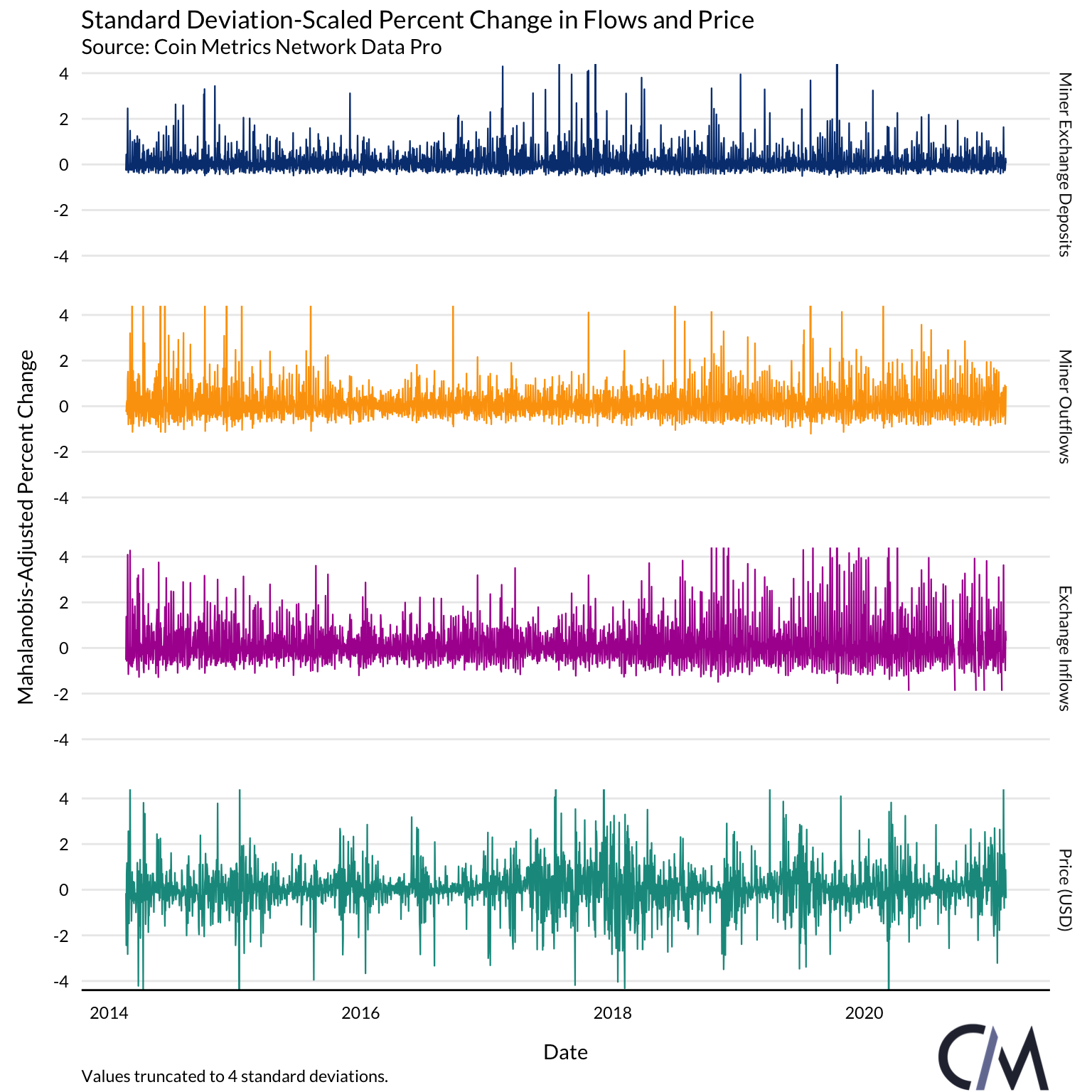

The absence of a link between Bitcoin’s market price and miner activity is reinforced by the low correlation between price and deposits. The weak correlation persists even during price declines.

The absence of a relationship between price and miners’ outflows is also visible visually when comparing price movements with miner deposits. These values rarely move in tandem, indicating a low correlation.

Conclusion

The influence of Bitcoin miners on the market remains underexplored. Yet, as methods for gauging the scale of miner activity improve, we can begin to understand their role more clearly.

Given the relatively small share of miner deposits in inflows compared with aggregate exchange flows, and the lack of a clear correlation between flows and price, there is little reason to believe these market participants are driving Bitcoin’s price decline.

There remain opportunities to improve metrics, including expanding exchange coverage and filtering addresses that have not recently participated in mining. However, at the exchange level, flows align with the widely held view that Binance and Huobi are miners’ preferred exchanges.

Subscribe to ForkLog news on Telegram: ForkLog FEED — the full news stream, ForkLog — the most important news and polls.