The robustness of Strategy’s balance sheet and the company’s ability to avoid selling the first cryptocurrency matter more for the asset’s short-term price than miner pressure, JPMorgan analysts conclude, reports The Block.

Nikolaos Panigirtzoglou highlighted two main sources of pressure on bitcoin’s price:

- a drop in hashrate and mining difficulty in the digital-gold network due to tightening bans in China after a surge in private mining and the exit of inefficient players from the country;

- market jitters following statements by Strategy’s chief executive, Phong Le.

A falling hashrate typically boosts miners’ revenues in the short term—until the next difficulty adjustment. At the time of writing, the leading cryptocurrency is trading near the cost of production—$92,000.

«As profitability shrinks, some high-cost miners in recent weeks have been forced to sell bitcoins,» the experts noted.

However, their actions are not the decisive factor for the cryptocurrency’s next move. The company’s financial health carries far more weight, the analysts say.

A margin of safety

JPMorgan named the mNAV ratio as the key indicator of the resilience of Michael Saylor’s company. The multiple reflects the firm’s market value relative to its bitcoin reserves. Despite a sharp decline in the second half of the year, it remains at 1.13.

«If the value stays above 1 and Strategy avoids selling bitcoins, that will reassure the market, and the worst for the cryptocurrency’s price is likely behind it,» the analysts believe.

Another sign of stability is the creation of a $1.44bn reserve. The bank estimates these funds can cover two years of dividend and interest obligations to shareholders, eliminating the risk of forced sales of digital assets “in the foreseeable future”.

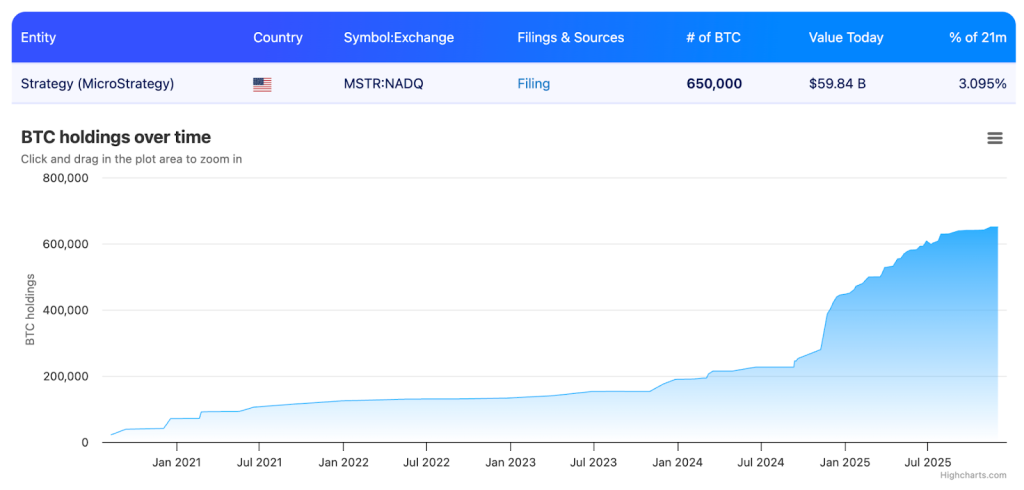

Strategy has slowed the pace of purchases but continued to add to its bitcoin position. From 17 to 30 November the company acquired 130 BTC for about $11.7m at an average price of $89,960.

The firm’s total holdings reached 650,000 BTC, valued at $59.8bn.

Risk of exclusion from the MSCI index

The market awaits MSCI’s decision on the status of Strategy’s shares and other crypto-treasury companies in global indices. It is due on 15 January.

JPMorgan’s analysts reckon the impact would be asymmetric: potential losses from exclusion are limited, while the benefit of remaining in the index is substantial.

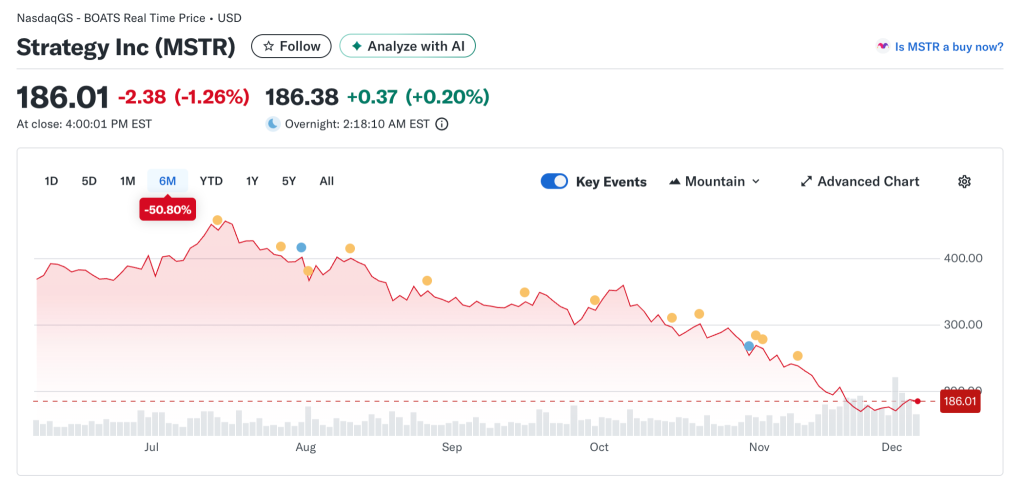

In their view, the risks are already “more than priced in”. Since 10 October, when MSCI announced a review of its classifications, Strategy’s shares have slumped 40%. Such a deep correction suggests the market has factored in not only removal from the provider’s indices but also potential exclusion from other major benchmarks.

Earlier, JPMorgan estimated potential capital outflows at $2.8bn. If other index providers take similar steps, losses could reach $8.8bn.

The company’s founder, Michael Saylor, said:

«Index classification does not define us. Our strategy is long-term; confidence in bitcoin is unshakable».

Analysts say that keeping Strategy in the MSCI index would be a powerful positive signal. In that case, the company’s shares and bitcoin’s price have every chance to “rebound strongly” to levels seen before the October plunge.

The analysts confirmed that the cost of production ($90,000) has historically served as a “soft floor”. A prolonged spell below that level, as in 2018, could intensify pressure on miners and push the support threshold lower.

Over the longer term, JPMorgan remains optimistic. Its model comparing bitcoin with gold (adjusted for volatility) still points to a fair value of about $170,000. That implies considerable upside over the next 6–12 months, assuming the market stabilises.

Strategy does not need to sell bitcoins

Bitwise’s chief investment officer, Matt Hougan, rejected concerns that Strategy would be forced to sell its digital assets because of exclusion from the MSCI index or market pressure. He called this scenario mistaken.

He acknowledged that a delisting would have an effect, but one weaker than expected. Hougan recalled that inclusion in the Nasdaq-100 triggered $2.1bn of fund purchases of MSTR shares, yet the price barely moved.

Like JPMorgan’s analysts, Hougan is confident that a negative MSCI decision is already priced in.

The Bitwise executive deems unfounded the forecasts that the company’s market value will fall below the worth of its bitcoin reserves. Even if the shares trade at a discount to NAV, the firm would not have to sell cryptocurrency.

The company’s main obligations — annual debt service of $800m and bond redemptions — will not create immediate pressure on the treasury, Hougan concluded.

Earlier, CryptoQuant analysts viewed Strategy’s creation of a dollar reserve as preparation for a prolonged bear market.