In recent years, stablecoins have become a central plank of the crypto economy—their combined market capitalisation has exceeded $301bn, and the largest tokens have cemented themselves in the top ten crypto assets. For many users, these “stable coins” are a convenient way to store funds, circumvent restrictions and make cross-border payments.

Growth has invited scrutiny—especially from American regulators, since most stablecoins are dollar-based. In 2025 Washington passed the first federal law setting a regulatory perimeter for the sector. Against the backdrop of a swelling public debt and economic challenges, a question follows: might the White House one day go further and nationalise stablecoin issuers?

A juicy prize

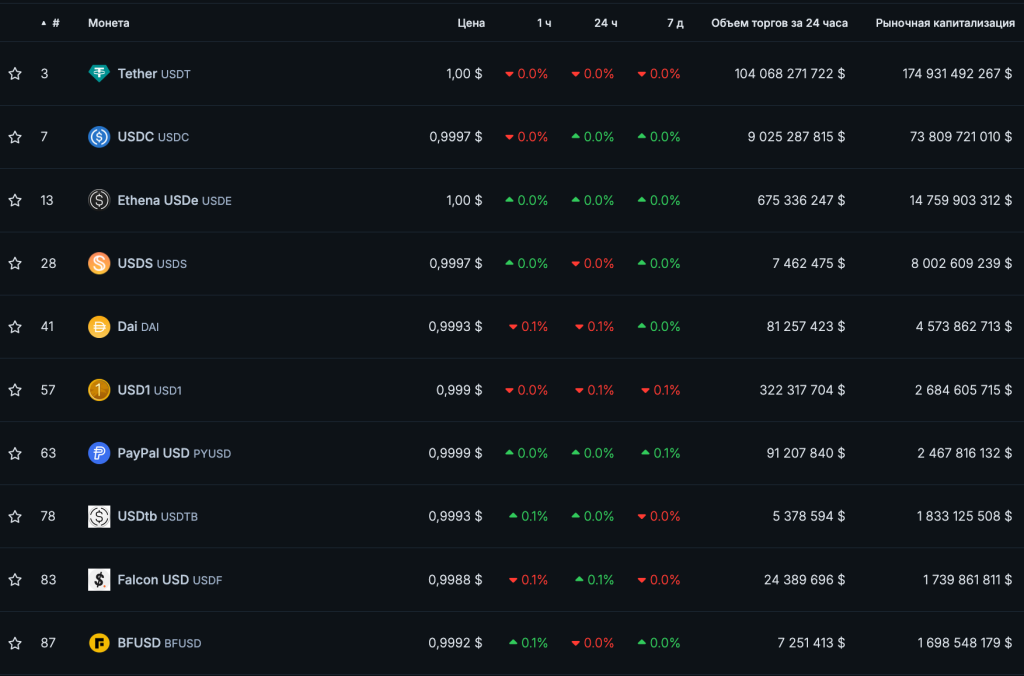

As of October 1st, the market capitalisation of the sector’s biggest player—Tether’s USDT—was nearly $175bn, according to CoinGecko. Trading volume stood at $104bn, while its nearest rival—Circle’s USDC—saw about $9bn.

In the second quarter, Tether International Ltd.’s net profit amounted to $4.9bn. From April to June the USDT issuer minted $13.4bn of tokens, and $20bn since the start of the year. Total circulating supply exceeded 157bn USDT. The firm has also become one of the largest holders of US Treasuries with $127bn (around $105.5bn directly and ~$21.3bn indirectly via funds/instruments).

Circle, issuer of the second-largest stablecoin, is following a similar path. According to ARK Invest data for May 2025, Tether and its closest competitor would rank as the 18th-largest holder of US debt, behind South Korea but ahead of Germany. And in 2024 the USDT issuer was the seventh-largest buyer of US Treasuries, after Britain and Singapore.

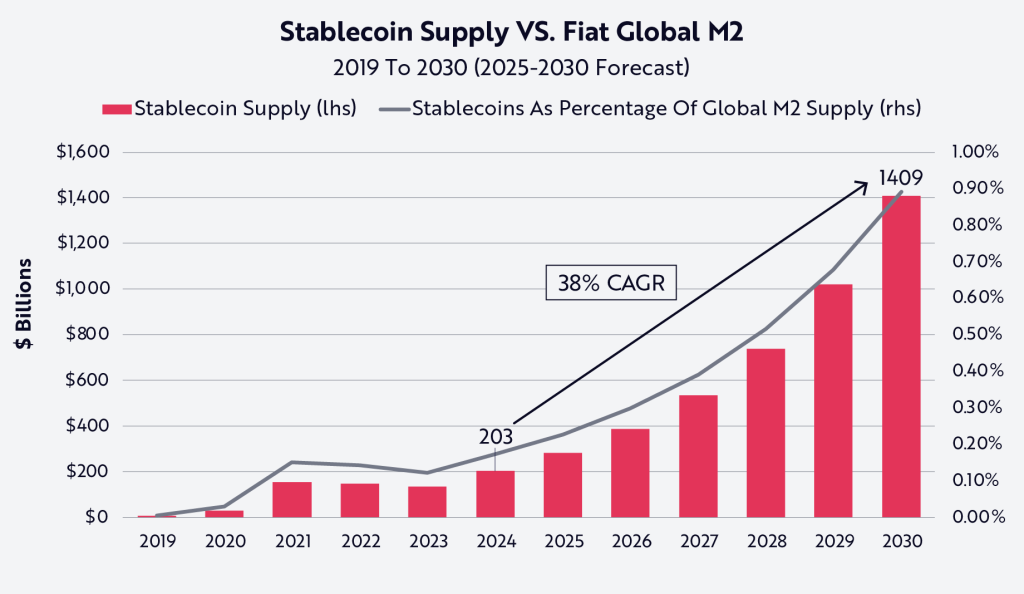

ARK’s analysts project that by 2030 the total supply of stablecoins could reach $1.4trn.

“If Tether and Circle maintained their current market shares and their allocations to US Treasury securities, together they could own more than $660bn of US Treasuries […]. It is clear that Tether, Circle, and the broader stablecoin industry could become one of the largest sources of demand for US Treasuries in the coming years, potentially replacing China and Japan as leading holders by 2030,” the report says.

By trading volume and market cap Circle trails the leader, but it has made significant strides in the US. On June 5th Circle’s shares were listed on the NYSE under the ticker CRCL. On day one the stock jumped 168%—from $31 to $82. As of October 1st, the shares were trading much higher in pre-market.

In July Circle filed a request with the US Office of the Comptroller of the Currency for a national trust bank licence, while Tether only plans to obtain foreign stablecoin-issuer status in America. The USDT issuer has also been actively assisting American law enforcement in freezing suspect addresses: over the past year the company blocked a total of $2.9bn in USDT.

These two dominant issuers backed the GENIUS Act, a bill that sets out rules for the sector and marks the first significant crypto statute in the US.

What the GENIUS Act does

On July 19th US president Donald Trump signed the GENIUS Act. The ceremony was attended by industry figures including Gemini co-founders Cameron and Tyler Winklevoss, Circle CEO Jeremy Allaire, Tether chief Paolo Ardoino and Robinhood CEO Vladimir Tenev.

The law requires full backing of stablecoins by liquid assets and annual audits for issuers with a market capitalisation above $50bn. It bans paying interest or other income to stablecoin holders and sets guiding rules for foreign firms in the segment.

In addition, issuers may not claim that their assets are “backed by the US government, insured at the federal level or have legal-tender status”. The GENIUS Act will come into force six months after signing or 120 days after regulators issue implementing rules.

Earlier, in comments to ForkLog, Bitget Research’s chief analyst Ryan Lee noted that the bill “kick-starts the creation of a regulatory framework for stablecoins pegged to the US dollar”. For Circle this could mean increased trust, while Tether faces pressure from tougher disclosure, greater transparency and audits.

Trader and Coen+ Telegram-channel author Vladimir Coen attributed Democratic backing for the bill to lobbying by giants such as Coinbase, Circle and Gemini, traditional sponsors of the party.

“Gemini, for example, has its own stablecoin. It is in their direct interest to pass and implement this law, which strengthens the position of stablecoins issued by US companies while simultaneously weakening their main competitor—USDT,” Coen added.

According to the expert, crypto-friendly legislation in the US “will only strengthen its position and the role of the dollar in the digital-asset economy”.

This matters amid growing chatter about de-dollarisation, a risk also flagged by ARK Invest. Citing Oilprice data, they note that by the end of 2023 some 20% of global oil transactions were settled in other currencies.

“Stablecoins occupy a unique position in the changing global financial landscape. They serve as the most liquid, efficient, and convenient wrapper for short-term US debt, effectively eliminating both obstacles associated with de-dollarization: preserving US dollar dominance in global transactions while ensuring sustained demand for Treasuries,” the report says.

In ARK Invest’s view, dollar-pegged stablecoins “could become one of the most dependable and resilient financial allies of the US government”. Their role is most visible where the greenback is in greatest demand.

USDC and USDT are widely used in countries with troubled economies: they give people swift access to dollars, lower remittance costs and protect savings from inflation. Such steady demand for dollars forges a direct link between the global market and America’s public finances.

Each new dollar token is backed by reserves; for both Circle and Tether, the main instrument is short-dated US Treasuries (T-bills). The greater the issuance of stablecoins, the more US government debt issuers must buy. Washington thus gains a new, steady source of demand for its bonds—one less reliant on traditional investors—that can even smooth market swings.

Against this backdrop, a logical question arises: if stablecoins are becoming a global channel for dollarisation while shaping demand for US debt, might American authorities seek complete control over them?

Nationalisation or regulation?

In public discourse, the idea that the US government might nationalise stablecoins is hardly heard. A similar notion was floated by a commentator writing as The Unhedged Capitalist in September 2022, albeit mainly in the context of Ethereum.

In his blog he mused about plans by some countries to create CBDCs, pointing to privacy issues for users and officials’ shaky grasp of the technology.

“USDC, regardless of whether it’s backed by reserves or unicorn dust, is battle-tested technology. Why would the government spend years building its own CBDC and another year or two testing it (indeed, if they are even technically capable of building such a thing) when they could just nationalize what already exists?” the author asked.

He also posited that the target would be the entire Ethereum ecosystem. In his view, the US Treasury could brand Vitalik Buterin’s project, together with the stablecoins that run on it, “a systemic threat to the United States and the sovereignty of the dollar”. Such claims do surface in one form or another: for example, Tether are called “a money launderer’s dream”. In January 2024 UN experts stated that USDT had become one of the popular tools among fraudsters.

“When the Treasury seizes Ethereum, it will take control not only of staking providers but will bring stablecoin issuers to heel. They will force USDC, USDT, PAX USD, BUSD and everyone else to allow redemption only on ‘Treasury Ethereum’. […] The craziest thing about my theory is that just imagine how damn easy it would be for the Treasury to pull this off,” noted The Unhedged Capitalist.

Such hypotheses have not gained broad support. Experts polled by ForkLog tend to think the state will opt (and is opting) for regulation rather than outright seizure.

Andrey Tugarin, founder of the law firm GMT Legal, observed that current requirements for stablecoin issuers are being designed so that independent firms channel funds into US government debt through their reserves.

“On that basis, the practicality of nationalisation should be assessed as low,” the expert added.

Ignat Likhunov, founder of the legal agency Cartesius, also sees such a scenario as unlikely. The US government, he argues, has chosen a different strategy—tight regulatory constraints that achieve key goals without buying out private companies.

He noted that the GENIUS Act contains no provisions for nationalisation. On the contrary, it establishes clear federal operating rules for issuers.

“Moreover, Congress, by a separate law, prohibited the Fed from issuing a state digital currency, which confirms the focus on a private-sector model under government oversight,” the speaker noted.

Tugarin and Likhunov agree that given current rules there is no sense in nationalising the industry. If authorities wanted to centralise control, says GMT Legal’s founder, the conversation would be about a CBDC.

“In this case the state is handing the technology to corporations while obliging them, in turn, to support public debt by mandating that part of reserves be held in short-dated Treasuries,” Tugarin noted.

In Likhunov’s view, measures in the GENIUS Act effectively turn private firms into conduits of monetary and debt policy without changing ownership. Tether and Circle’s future, he said, looks like further adaptation to regulatory demands.

“Both companies will remain independent players, but their core business model will be tightly regulated to serve national interests, making them de facto ‘semi-state’ structures by function. As for structural demand for government debt, stablecoins have already become a significant source. […] By the end of the decade the stablecoin market is expected to reach $3.7trn, creating trillions of dollars of additional demand for US Treasuries and helping to reduce debt-servicing costs,” the expert stressed.

Ani Aslanyan, founder of the Telegram channel “Everything about blockchain, the brain and WEB 3.0 in Russia and the world”, takes a firmer line. In her view, outright nationalisation of issuers is highly unrealistic. In America, such moves are used only in emergencies tied to national security or systemic risk and require a specific statute.

“The GENIUS Act allows issuers to operate under the supervision of the OCC or state regulators, with a focus on transparency and stability, without the need for state intervention in ownership. […] This preserves innovation in the private sector, minimises risks to the budget and avoids legal disputes,” Aslanyan noted.

She expects Tether and Circle to remain independent, but under tighter oversight—more “regulated” and closer to financial institutions.

For his part, Web3 researcher Vladimir Menaskop called nationalisation of stablecoin issuers a realistic scenario. In comments to ForkLog, however, he added that its implementation would mean Washington “had definitively lost the economic war to China”:

“Nationalisation has happened in US history, but each time it was a rejection of the basic principles on which this state rests. In fact, the ‘iron wars’, ‘trade wars’ and other conflicts are pushing the States towards this scenario, although for now it is likely but not inevitable,” Menaskop stressed.

He argues there is logic to nationalising issuers of “stable coins”:

“First, the issuers, to hedge, buy government bonds—which are literally debt—and then that debt is zeroed out through nationalisation. The US gets liquidity without repaying its debt: a double saving.”

Even so, Menaskop questioned whether Tether and Circle can be called non-state today. He pointed to the large share of dollars in their assets and their holdings of Treasuries as a form of indirect control. And the USDC issuer is directly tied to the jurisdiction, he noted.

Nationalisation still looks a poor choice. For the industry and the TradFi players already intertwined with it, a state grab of major issuers would provoke a backlash. “Domestication” through regulation is the more realistic route—one consistent with the new administration’s agenda and its contrast with the previous one.

The emerging framework has effectively integrated stablecoins into America’s legal and financial system. The companies remain private, but their key decisions—whether to serve citizens of various countries, to freeze addresses, to structure reserves—will be governed entirely by Washington’s rules.

The result: a steady source of demand for US Treasuries and a way to entrench the dollar’s global leadership in the digital age. For the rest of the world, stablecoins will remain a handy settlement tool—but one that increasingly embeds a new form of dependence on US financial policy. So the question is less whether Tether or Circle will be nationalised than how deeply America will control this infrastructure—and what that will mean for the world economy.

Text: Alisa Ditz