Against a backdrop of market growth in 2020-2021, the sector of cryptocurrency options strengthened, with the main activity concentrated on the centralised Deribit exchange.

DeFi — one of the main drivers of the crypto industry’s development. Not surprisingly, as the boom in this segment grows, decentralized options—which are publicly accessible and do not require KYC procedures—are gaining popularity. Projects such as Hegic and Opyn have demonstrated that there is demand for even these sophisticated financial instruments.

ForkLog has examined the features of decentralized options, identified the reasons for their rising popularity, and learned about the pitfalls of these complex but interesting and promising financial instruments.

- Against the rapid growth of DeFi, fairly advanced financial instruments — decentralized options — are gaining popularity.

- The segment is still small, but developing rapidly. Hegic, Opyn and other projects are gradually increasing TVL, improving user interfaces.

- Liquidity for DeFi options is boosted by integrations with various projects, liquidity mining programmes, the development of Layer 2 solutions, and tightening regulation of centralised equivalents.

Why DeFi Options Matter

Options have long been one of the main pillars of the traditional financial system. These derivative instruments provide investors with the ability to bet on the future dynamics of assets and hedge price risks, effectively using capital.

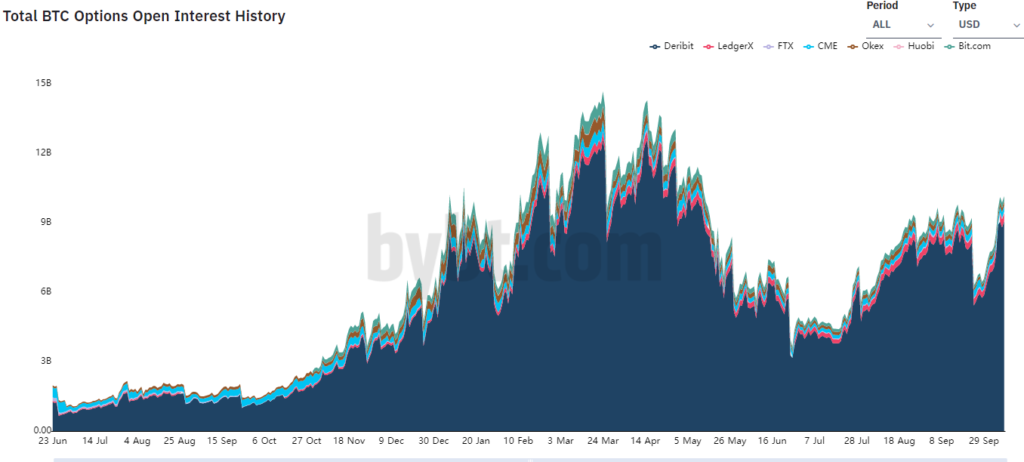

The chart below shows the meteoric rise of open interest in options, peaking in spring 2021. This was followed by a decline in activity and a gradual recovery from late June.

There is also a clear dominance of Deribit, with LedgerX, FTX and CME lagging significantly.

Due to a global trend toward tighter regulation, Deribit was forced in May 2020 to restrict access to the platform for users from certain countries, including Japan. Later the exchange introduced mandatory client verification.

Probably, as a result of these measures, traders turned to DeFi options. These on-chain protocols offer similar capabilities to traditional counterparts, while being permissionless and non-custodial.

There are two types of option contracts: put and call. Put contracts give holders the right to sell the underlying asset at a fixed price in the future. Conversely, calls allow buying the asset at a set price.

An example of a simple on-chain option contract: a user creates a call to buy 1 ETH for 4000 Dai on January 1, 2023. The process involves three steps:

- The user deposits 1 ETH into the smart contract;

- The smart contract issues 1 call option;

- At expiry — January 1, 2023 — the token holder can send 4000 Dai to the smart contract and withdraw 1 ETH.

Even such a straightforward scheme may seem complex to many, especially compared with more user-friendly liquidity pools and lending services. The latter, thanks to their ease of use, can attract substantial sums. Bright examples: Uniswap and Aave, whose TVLs are measured in the billions.

Creating effective option protocols with intuitive interfaces is no easy task for developers. The architectural complexity of such platforms carries significant risks for market participants.

In May, the Opyn platform lost $371,000 due to a vulnerability in the project’s internal token. Attackers conducted a double-spend on Ethereum put options, gaining access to collateral posted by users. To avoid further losses, the Opyn developers withdrew 572,165 USDC from their own smart contract, and removed the ability to buy oTokens.

Recently, venture-capital analyst Bridget Harris took advantage of the Ribbon project’s May airdrop exploit, receiving more than $2.4 million in RBN tokens.

That the segment is still in its early stages is evidenced by figures. For example, Hegic’s TVL is about $21 million, and Opyn’s is about $127 million (per DeFi Pulse data as of 10.10.2021). These sums are minuscule compared with leaders in AMM platforms or lending protocols. Turnover relative to centralised equivalents is also modest.

It is worth highlighting other inherent characteristics of options, which bring many challenges and risks. First, these contracts are not perpetual — they must be continually created and executed.

Options entail asymmetric terms and, accordingly, risks for buyer and seller. For example, a holder of a call option risks only the premium paid for the contract. The risk to the seller of a short call is unlimited, while potential profits are limited to the premium from selling the contract.

Many on-chain option platforms (Hedget, Opyn v2) rely on an order book. It is a well-understood model, but for effective operation it requires market makers to provide sufficient liquidity.

There are also option platforms built on liquidity pools — for example, Hegic and Finnexus. The advantages of this model:

- the ability to easily attract liquidity to underpin the platform’s operation;

- flexibility: option buyers can set strike prices and expiration dates themselves;

- providing liquidity on an ongoing basis (meaning LPs do not need to close positions and move to another pool at expiry).

However, pricing on these platforms is not conducted via AMMs as on Uniswap, but algorithmically — using the Black–Scholes model. In this context, the option price is determined by the value of the underlying asset, the strike price, the contract duration (expiry dates) and the implied volatility. Data for the latter can be sourced from centralised exchanges like Deribit via oracles, which can be the targets of attacks and manipulation.

Hegic

Hegic is an on-chain protocol that allows buying American-style call and put options on ETH and WBTC. Users can also sell contracts, acting as liquidity providers.

Created by developer Molly Wintermute, the non-custodial platform does not require KYC. The service began operating in February 2020.

In September that year, the HEGIC token was issued. It became the central element of the new protocol version — Hegic v888, which began operating a month later. The token can be staked in lots, used to collect fees, and for on-chain governance of the platform.

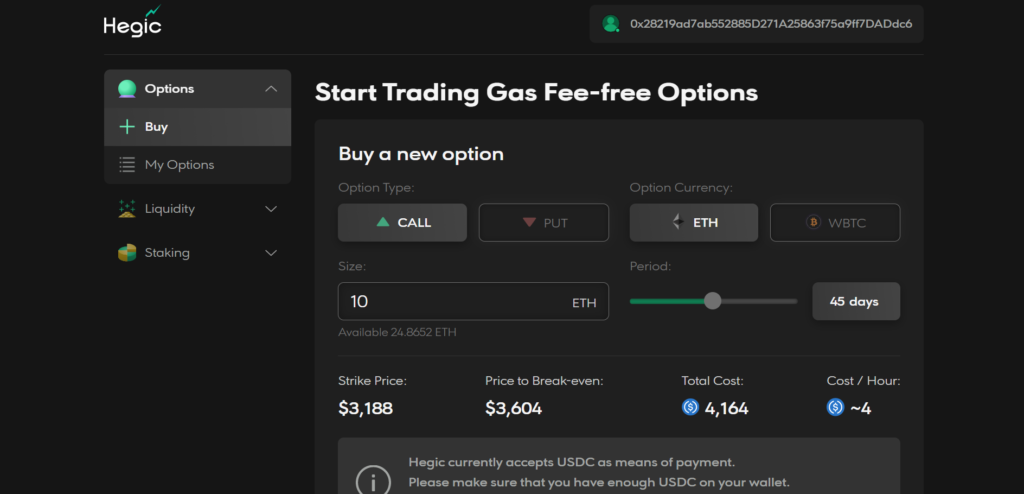

Participants of this AMM platform can customise option parameters, setting strike price and expiration date. Option prices are calculated automatically immediately after configuring their parameters.

After this, you need to connect to the platform via a Web3 wallet such as MetaMask.

Then you can choose the option type — call or put — based on ETH or WBTC. There is also the option to set the option period (Period). The Strike Price points to the current market price, and the calculation is performed in the stablecoin USDC. The Price to Break-even is the break-even price for the given option parameters.

Below is a calculator that shows the net profit if the ETH or WBTC price reaches a certain level during the hold period.

In the project’s Medium blog, it indicates that as little as a single on-chain transaction is enough to start “gas-less” trading on the platform. However, to do this, the minimum order size must be 10 ETH or 1 WBTC.

After confirming the transaction, the user will receive an ERC-721 token linked to the option they created.

Execution fee is 1% of the contract size. It goes to HEGIC stakers, while other fees go to liquidity providers.

External price data are obtained via Chainlink oracles.

From October 10 to January 10, total trading volume on Hegic reached $168 million. The protocol issued 3,530 contracts for 1,094 unique addresses. The average contract size was $47,700.

Hegic’s success in the DeFi segment has attracted attention from developers of external protocols. For example, a staking service zLOT has emerged. It lowers the entry threshold for staking HEGIC by pooling the assets of small investors into lots.

Users can deposit HEGIC into zLOT. After that, zHEGIC tokens are issued to them. During withdrawal of native assets, zHEGIC tokens are burned.

The project also provides a governance token, ZLOT, which can be locked for staking, and used to vote on changes to various protocol parameters.

Opyn

No less popular among DeFi supporters is the Opyn project. It was founded by UC Berkeley alumni Aparna Krishnan, Zubin Koticha and Alexis Gauba.

The Convexity Protocol-based platform attracted $2.16m in seed investments from Dragonfly Capital in the summer of 2020.

Despite losses from a hack, in the following year the project raised $6.7m in a Series A round from Paradigm, Synthetix co-founder Kane Warwick and DeFi project Aave’s head Stani Kulechov.

In 2019 Opyn was among the first to offer decentralized options. The first version of the protocol enables the creation of American options in the form of oTokens, fully collateralised by the underlying asset.

The second version of the protocol includes a number of innovations, including auto-execution and flash minting. The latter is based on the concept of flash loans.

Launched in late 2020, Opyn v2 is based on an order book using the 0x protocol. The platform supports European-style options (as on Deribit) with a narrow range of strike prices and expiration dates. Base assets: USDC, ETH, WBTC.

Oracles are used to determine the strike price. Each contract is issued as a token of the ERC-20 standard and, consequently, becomes tradable on any DEX.

Opyn v2 features enable spread strategies, where one option position can collateralise another. For example, buying a put option with a relatively high strike price and using it as collateral to sell a cheaper put with a lower strike.

Support for flash minting and spread strategies is aimed at increasing capital efficiency for trading operations. In June, the developers introduced the possibility of partially collateralised contracts.

Prices data and liquidations are provided by Chainlink oracles.

Gamma Protocol, used in Opyn v2, has undergone an OpenZeppelin audit, and its formal verification was performed by Certora.

According to information on the project’s website, Opyn’s turnover since inception has exceeded $1.95bn, and a total of 38,779 trades have been executed. Such impressive figures have largely been achieved through integrations with Ribbon Finance, Opeth, Gamma Portal, Fontis Finance, Optional Finance, Ziku Finance and other projects.

Other Projects

Primitive — a platform for decentralised American options, using tokenised long and short positions. Calls settle in the underlying asset (wrapped ETH or SUSHI), puts — in the stablecoin Dai.

Siren Protocol — originally launched as an AMM platform with bTokens and wTokens. When a trader buys an option from a pool, its collateral is used to mint the asset pair. In this process, bTokens are issued to the buyer, while wTokens remain in the pool.

This approach is similar to Hegic and FinNexus. The difference is that the options are tokenised, while the pools are “one-sided”. For example, for a WBTC-based call, the collateral asset could be “Bitcoin on Ethereum.”

Subsequently the platform underwent significant changes. In the August version of the protocol, there was a shift to European-style options, settlement in a stablecoin, and Polygon support. The user interface was substantially redesigned.

Auctus — a DeFi protocol supporting flash execution, launched also on Arbitrum and Binance Smart Chain. Users have access to trading options in both basic and advanced interface modes, creating contracts with different strike prices and durations, and the possibility to act as a liquidity provider.

On Auctus, market participants have access to fairly sophisticated automated strategies. For example:

- The user deposits USDC into a Vault.

- USDC is issued as a loan on the Curve platform. The user receives CRV tokens, which are sold to automatically purchase ETH-based call contracts.

- If the call finishes in-the-money on expiry, the contract is executed automatically — the trader earns a profit.

This year the project plans to launch an on-chain governance system, with the AUC token as its central element.

Premia — a decentralised marketplace enabling the issuance of contracts with varying parameters and staking of the native token. A second version of the protocol with a completely redesigned interface is planned.

Antimatter — a project positioning itself as the “Uniswap for options”, offering perpetual financial instruments across multiple networks — Ethereum, Binance Smart Chain, Arbitrum, Avalanche, Fantom, Near and Solana. The site mentions the ability to issue NFTs backed by various underlying assets.

Conclusion

Decentralised options are — while quite complex — fascinating instruments. For sophisticated investors they unlock new strategies, and for projects they offer broad opportunities for integration.

The landscape of this still-young and relatively small segment is changing rapidly. Developers are actively working to improve platforms and to create projects with new capabilities.

The founder of DeFi project yEarn Finance, Andre Cronje, described Hegic as “a really excellent technology.” The praise culminated in a partnership to create binary options using yEarn vaults. (link)

Developer Molly Wintermute is working on the on-chain hedging protocol Whiteheart based on Hegic. The solution is designed to automatically buy put options on-the-money on behalf of users when they acquire assets on decentralised exchanges.

Interfaces on some projects are not exactly user-friendly yet. It is also clear that many services lack liquidity.

Decentralised options mark a natural phase in the evolution of the crypto industry and DeFi. The adoption of Layer 2 solutions and support for new ecosystems such as Polygon, Avalanche and Solana could act as powerful drivers for the development of option protocols, boosting their liquidity and enabling further integration with other “financial Lego” projects.

Subscribe to ForkLog’s YouTube channel at YouTube!