The DeFi fever has become a landmark moment for decentralized exchanges. One of the first smart-contract-based DEXs was Uniswap, which implemented the automated market maker (AMM) technology. The platform was created with support from the Ethereum Foundation and Vitalik Buterin.

Until this summer, Uniswap could not boast substantial trading volumes, but in June this figure rose tenfold—from $1.75 million to $17.5 million—and by the end of August had surpassed $425 million, outpaced the American Coinbase.

Forklog has examined how Uniswap managed to mount a serious challenge to centralized exchanges as the first DEX.

From Siemens to Ethereum

The idea behind Uniswap has a specific starting point — Vitalik Buterin’s Reddit post from October 2016. At that time, in his words, the problem with all decentralized exchanges was too wide a spread. He proposed solving it with smart contracts that would manage reserves of different tokens and balance their prices relative to each other according to supply and demand.

Hayden Adams — a young computer engineer from New York — implemented this idea. He came to the crypto industry after being laid off from Siemens in the summer of 2017.

🦄Today its been exactly 1 year since the launch of @UniswapExchange!

To celebrate, I’m publishing V0 of the Uniswap Birthday Blog series.

In it I describe Uniswap’s origin. The the hard work, the chance, and the many people who helped along the wayhttps://t.co/oFFEj2Jvw6

1/

— Hayden Adams 🦄 (@haydenzadams) November 2, 2019

After the layoff, his friend Karl Floersch contacted him and proposed Adams retrain as a programmer and start writing smart contracts on Ethereum. Adams agreed and began work on creating the “automated market maker” (the inventor of the idea is credited to Alan Lu from Gnosis, who described the AMM in 2017).

One of the early Uniswap sites versions with a single liquidity pool. You can notice the UNI token that disappeared from the final version. The “demo version” of Uniswap is still accessible.

Floersch introduced Adams to the Ethereum developer circle and in spring 2018 acquainted him with Vitalik Buterin (he is the one who coined the name “Uniswap” — Adams originally called his project “Unipeg”).

By August 2018 Uniswap received its first funding — a grant from the Ethereum Foundation of $100,000. According to Adams, Uniswap was founded on the “values of Ethereum”.

The official launch took place in November 2018. Presenting the platform, Adams listed its key characteristics:

2/🦄 There is no central token or platform fee. No special treatment is given to early investors, adopters, or developers. Token listing is open and free. All smart contract functions are public and all upgrades are opt-in.

— Hayden Adams 🦄 (@haydenzadams) November 2, 2018

«There is no central token or platform fee. No special treatment is given to early investors, users or developers. Token listing is free. All smart contract functions are public, and their upgrades are opt-in».

How does automated market making work?

In Uniswap, the AMM principle is implemented via liquidity pools, which represent trading pairs and consist of user funds locked in smart contracts. The token ratio in a pair determines the price of the token. The implemented supply and demand for tokens changes the pool’s token balance, and thus the ratio, i.e., the price.

Any user can participate in a pool — they need to contribute both tokens of the pair in the current exchange ratio. Such users become “liquidity providers”, who receive 0.3% of the trades involving the pool’s trading pair. Thus, the fees are earned by the users themselves, not the platform.

“Providing liquidity to protocols mirrors the operation of currency exchangers anywhere in the world. Imagine you could lend $100 and 7,800 rubles to the nearest exchanger in exchange for earning a 0.3% commission on each dollar-to-ruble exchange. At the same time you take on the risks of ruble-dollar volatility. The same amount of dollars and rubles (excluding fees) you would recover only if the rate returns to the level it was when you lent the funds.”

“If the ruble-dollar rate moves sharply, you lose part of your money due to volatility. In the existing financial system, exchangers and banks use their liquidity for such operations, they take on the risks and earn from it. In decentralized finance, anyone with internet access can assume these risks and earn from the fees. To achieve the best exchange rate and reduce volatility risks for banks and a decentralized exchange, there must be as much liquidity as possible. To attract as many people as possible to lend their money, decentralized exchanges Uniswap and Balancer distribute part of their tokens. Banks cannot distribute their shares to every client due to high costs and legal complexity, so effectively they can offer attractive deposit rates. It is worth noting that on decentralized exchanges you trade not ruble for dollar, but one cryptocurrency for another”, — explained the AMM principle by Zerion co-founder Vadim Koleoshkin.

Possible deviations from the spot market are smoothed by arbitrage. Another feature of the platform is that anyone can add a trading pair with a new token.

Rise to the Top

Uniswap did not hold an ICO. The project attracted money from professional investors. More than $1 million was “raised” by Uniswap in 2019 from the Paradigm fund, and in 2020 raised $11 million.

The decision not to conduct an ICO is one reason why Uniswap did not have its own token from the outset.

For a long time, Uniswap lagged behind centralized exchanges, and in DeFi — behind lending protocols like MakerDAO. Everything changed when the market began to flood with DeFi products offering passive income for liquidity provision.

DEX, DAO and tokenized bitcoins: how not to get lost in the DeFi thickets

That same period also popularised yield farming. By that time, Uniswap was already the most authoritative project in the DEX space.

Moreover, the developers prepped technically for the hype — in May there was a major protocol upgrade. It addressed the main weak points — notably, enabling direct exchange between ERC-20 tokens (previously all exchanges went through ETH), instant swaps for trading, and improved control over quotes.

From early July to the end of August, the volume of funds locked in Uniswap pools grew almost fivefold — from $47 million (July 2) to $831 million (August 31).

However, the record inflow to the protocol was aided by the success of the SushiSwap fork, launched at the end of August. Forklog detailed this at the link:

Fledgling ‘Chef’, DeFi fever and whale gambits: how SushiSwap attracted $1B in two weeks

SushiSwap offered record yields by distributing its own governance token to all participants in its pools. As a result, $1.4 billion flowed into pools originally launched on Uniswap in just a few days. It became clear that such a token incentive was precisely what decentralized exchanges lacked to spur growth.

Initially, SushiSwap rapidly lured a lion’s share of Uniswap’s user funds, but after the SUSHI airdrop was trimmed, it likewise quickly lost them. They returned to Uniswap with the launch of the governance token UNI, which was announced on 16 September.

Liquidity on Uniswap, September 26. Data: Uniswap.

Liquidity on SushiSwap, September 26. Data: SushiSwap.vision.

What UNI Changed

Uniswap learned the lessons of its fork.

First, the issuance of new tokens was turned into a large promotional campaign: 15% of all tokens were given away for free to all platform users, including those who had not used Uniswap for a long time. The minimum payout was 400 UNI.

This substantial airdrop instantly drew the attention of a large audience.

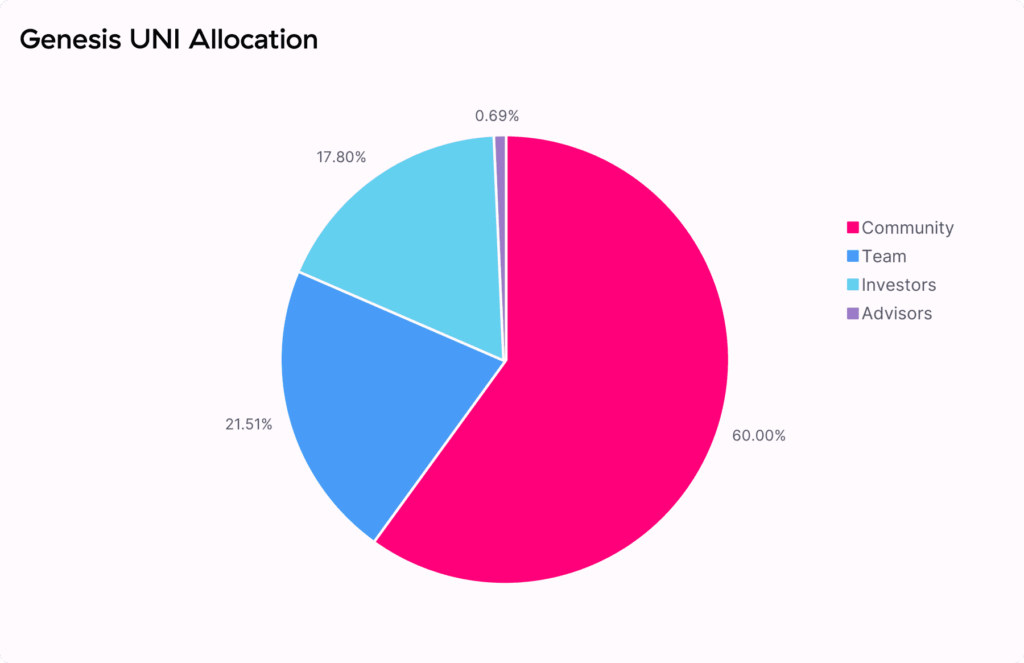

UNI issuance breakdown: 60% — community (airdrops and treasury), 21.51% — team, 17.8% — investors, 0.69% — advisers.

Second, developers altered the inflation approach. In SushiSwap the first two weeks of SUSHI issuance were increased tenfold compared with the standard, and the surplus of new coins pushed the price down. In UNI, the inflation mechanism (2% annually) will kick in only after four years.

Third, the governance approach was changed. SushiSwap includes a developers’ fund, into which 10% of all issued SUSHI are directed. Uniswap also has a fund — the so-called “community treasury”. Over the next four years it will receive 43% of all coins (430 million UNI). The fund is intended for grants, incentivising community initiatives, liquidity mining and other directions.

A month after the UNI release, on 18 October, the Uniswap community will gain control of the fund. In the meantime, UNI holders must select a council of “protocol delegates”. In six months, the community will take control of Uniswap’s main lever — the governance.

The creators urged the community to pick a diverse and high-quality list of protocol delegates from among its ranks, and to start discussions and engagement on concrete decisions to be taken. And the community responded.

Thus, a union had already formed, drawing in smaller UNI holders. Its aim is to unite small coin stakes to defend the interests of small users and secure a voice in votes comparable to whales.

Will Uniswap Become More Decentralised?

The development team, responsible for 21.5% of the UNI supply, will continue to improve the protocol’s code and conduct audits. At the same time, team members will not directly participate in governance, though “they may delegate their votes, without the intention of influencing future decisions”.

Another nearly 18% of the tokens were allotted to investors. Therefore, the likelihood of whales holding large sums of UNI is real.

The creators of Uniswap aim to push for further decentralisation by handing governance levers to the community. But it is not that simple.

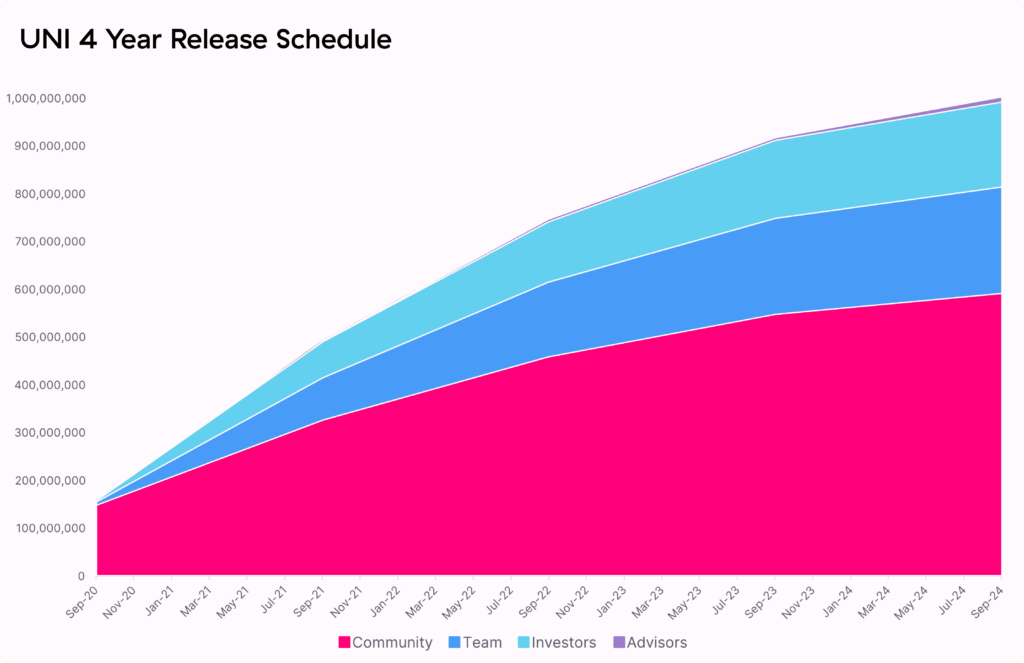

Investors, advisers and team members are allocated 40% of the total token supply, to be distributed via vesting. This procedure involves locking that number of tokens in smart contracts and releasing small amounts over a defined schedule.

A four-year release schedule for UNI tokens. While the team talks of vesting, its exact timetable and payout sizes remain undisclosed.

However, as highlighted in a Glassnode study, these funds currently sit on ordinary Ethereum addresses (just 43 in total), whereas the community treasury coins are distributed in a dedicated smart contract with a specific unlock schedule. In other words, technically the team’s and investors’ funds could be used already.

“It remains unknown who controls the keys to these addresses, but until an explanation emerges, these tokens are likely not locked. It appears the Uniswap team interprets the term ‘vesting’ very broadly, perhaps to persuade the community that team and investor tokens will not be accessible until vesting ends”, says Liesl Eichholz, the report’s author.

Although on Twitter she clarified that the risk of using tokens before vesting ends, “given the reputation of the team and its investors”, is very small.

6/ To be clear, I think we can trust @UniswapProtocol and @haydenzadams. The risk of a rug-pull is pretty low given the reputation of the team & its investors.

Even though the tokens are liquid now, I rate the chances of them being used before they «vest» as extremely low.

— Liesl Eichholz (@liesleichholz) September 24, 2020

UNI has already been listed on Binance, Coinbase Pro, Bitfinex and other top exchanges. As of writing, 131.6 million tokens have been distributed.

Industry participants fear that the success of UNI and SUSHI could lead to other platforms without viable business models issuing useless governance tokens, potentially triggering a fresh ICO boom:

You’d have to be a fool not to start using DeFi protocols or DeFi infra apps that don’t have tokens just to gamble on the chance they do something similar to Uniswap

— Larry Cermak (@lawmaster) September 19, 2020

In either case, the UNI introduction helped TVL on Uniswap not only to recover but to exceed previous levels, standing at about $1.92 billion at the time of writing.

The ForkUniswap project has already presented the payments company Crypto.com, and Binance launched two DeFi projects. This suggests centralized exchanges are prepared to challenge Uniswap’s leadership in DeFi, and with their resources this is more than feasible. Whether the project can keep the crown remains an open question.

Subscribe to ForkLog news on Telegram: ForkLog Feed — the full news stream, ForkLog — the most important news and polls.