Key

- Bitcoin and Ethereum hit all‑time highs above $67,000 and $4,400 respectively. One of the market drivers was the launch of the first US bitcoin futures ETF.

- October saw a trend toward meme tokens, as well as native metaverse and GameFi coins.

- Inflation expectations prompted investors to turn their attention to cryptocurrency company equities.

- Trading volume on leading spot exchanges approached $1.5 trillion, behind only the April–May highs this year. A similar pattern was seen on DEXs.

- The US rose to the lead in Bitcoin’s hash rate share. The metric is recovering strongly after the Chinese ban.

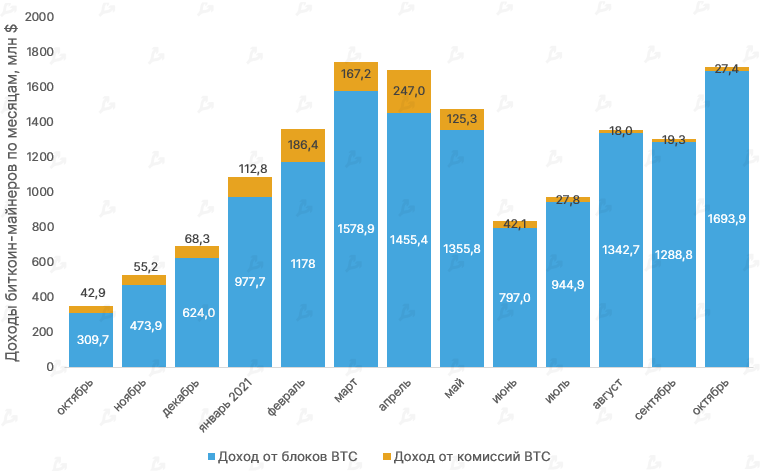

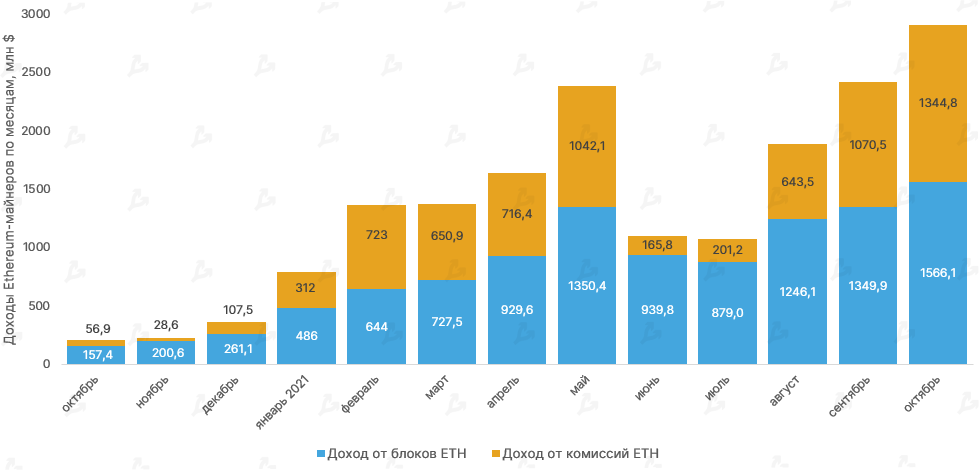

- Bitcoin miners approached peak earnings, while Ethereum posted a record $2.9 billion.

- The market capitalization of stablecoins reached $125 billion. Tether’s USDT capitalization stands at $70 billion.

Leading asset dynamics

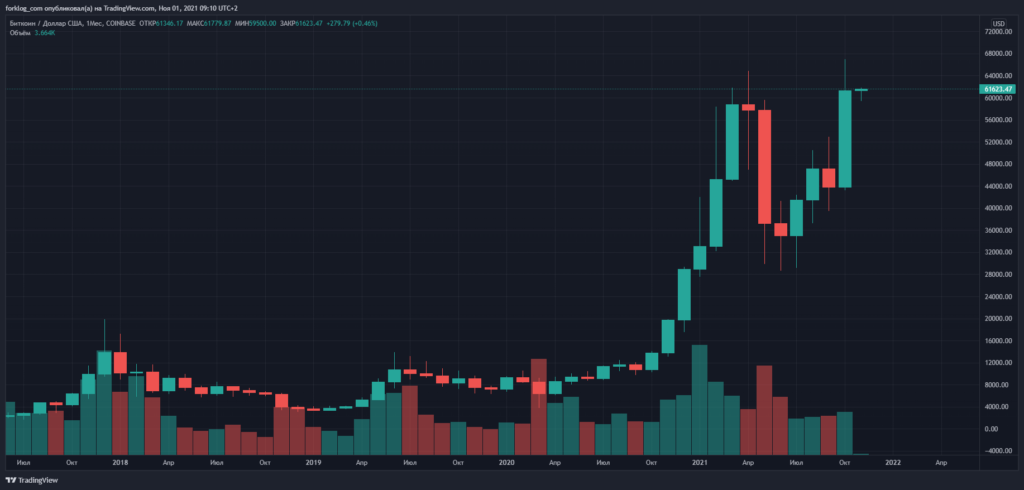

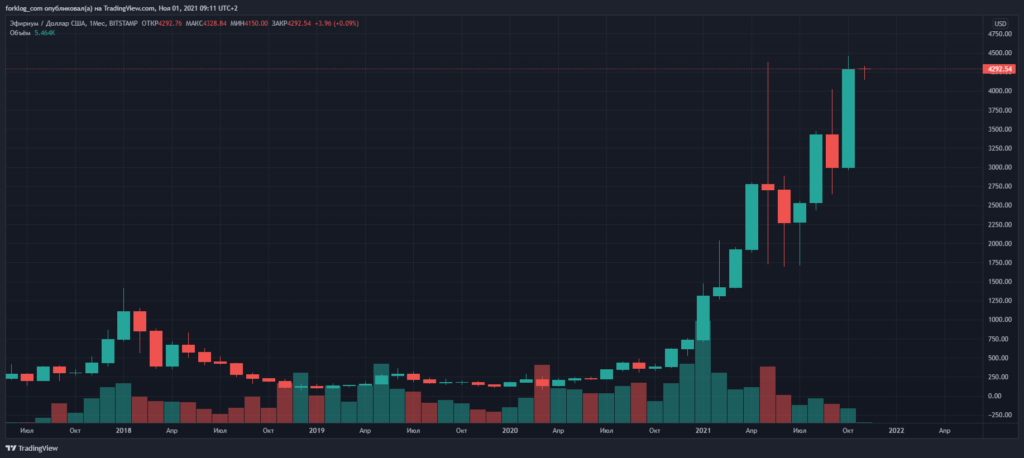

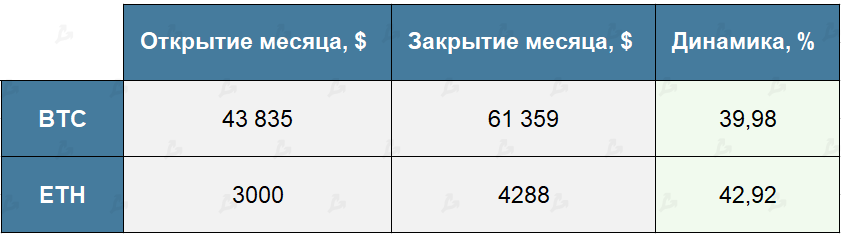

In October Bitcoin and Ethereum hit all-time highs above $67,000 and $4,400 respectively.

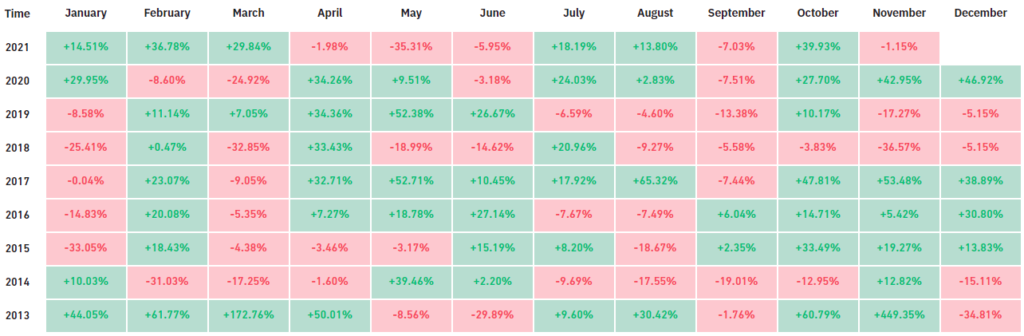

- Bitcoin rose 39.9% for the month, and Ethereum 42.9%.

- A historically favorable year-end is ahead within the bull market.

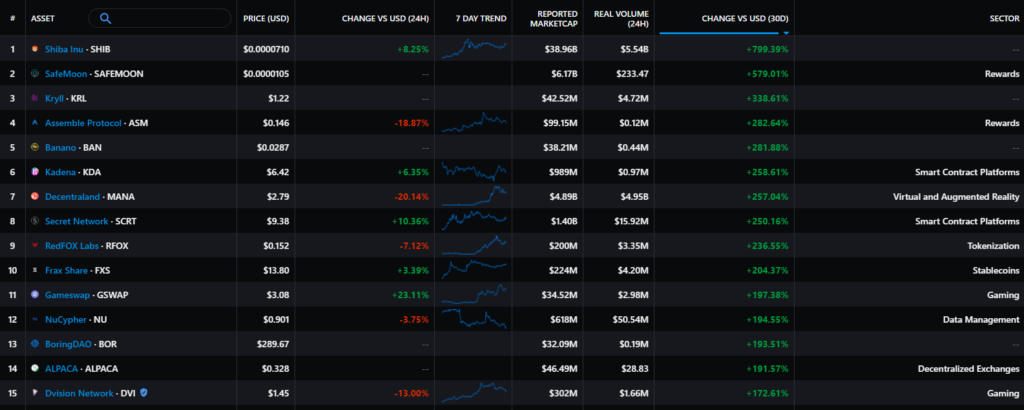

- Meme tokens led the October rally, as did NFT/metaverse native coins. Shiba Inu (SHIB) briefly surpassed its closest competitor Dogecoin by market cap, and the Safemoon DeFi protocol’s native token also featured among October’s top performers.

- Positive momentum was also seen in native metaverse, NFT, and GameFi coins, for example Decentraland (MANA) and Sandbox (SAND), amid the rebranding of Facebook to Meta.

- Separately, the meme-token trend surged. In addition to Shiba Inu, other dog-themed tokens — Dogecoin (DOGE), Floki Inu (FLOKI), Dogelon Mars (ELON), YooShi (YOOSHI) and Baby Doge Coin (BABYDOGE) — rallied sharply last month.

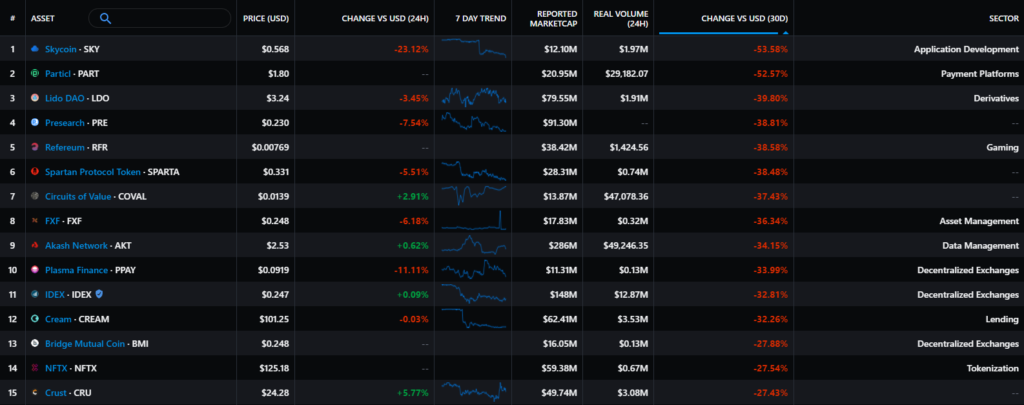

- The native token of the Cream Finance DeFi protocol showed negative momentum after another hack, in which the attacker stole $130 million.

Equities of cryptocurrency-related companies

MicroStrategy (MSTR):

+16.15%

Coinbase (COIN):

+37.15%

Bakkt (BKKT):

+351%

Galaxy Digital (GLXY):

+64.44%

Crypto- and mining-related equities performance

Canaan (CAN):

+33.91%

Ebang International (EBON):

+7.43%

Riot Blockchain (RIOT):

+0.07%

Hut 8 (HUT):

+48.72%

Marathon Digital (MARA):

+53.51%

Crypto- and mining-related stocks delivered strong results in October alongside Bitcoin’s positive momentum. Bakkt’s shares stood out in particular — despite a muted start to trading on 18 October, they surged 351% over two weeks on the back of a partnership with Mastercard.

Macro backdrop

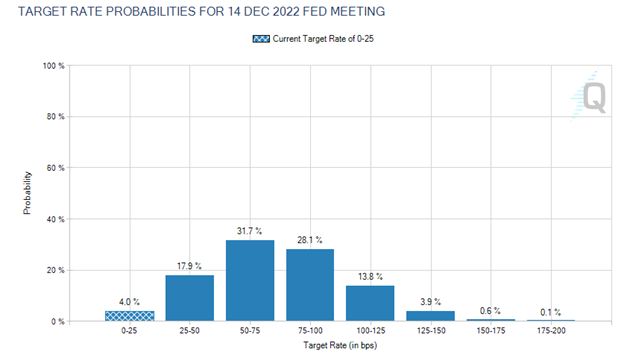

- November 3 will see a Federal Reserve meeting. The decision could signal the start of tapering asset purchases at a pace of $15 billion per month, beginning in mid‑November.

- Normalization of monetary policy is driven by concerns about rising inflation expectations. Ongoing supply-chain issues and high energy prices could keep consumer price inflation elevated.

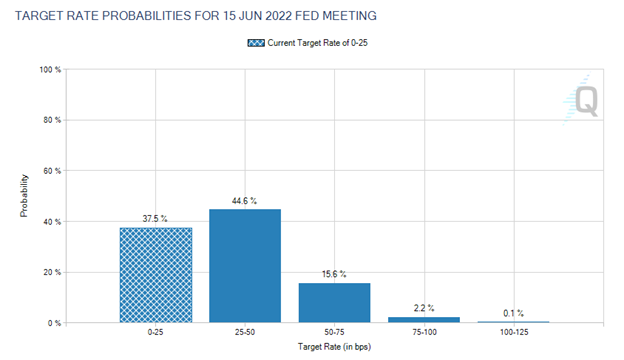

- The futures market prices in a 62.5% probability of the first Fed rate hike in June 2022. By that point the Fed will have fully unwound its asset purchases. A month ago the odds were only 1 in 4.

- The October rise in inflation expectations boosted the probability of three rate hikes in 2022 — from 7.3% a month ago to 46.4%. At the September 22 meeting, half of Fed participants projected one hike next year, while another half looked to 2023.

- Flattening of the U.S. yield curve became a signal of potential loss of Fed control over inflation. Investors started to entertain a scenario where policymakers would tighten sharply in 2022, potentially slowing the economy.

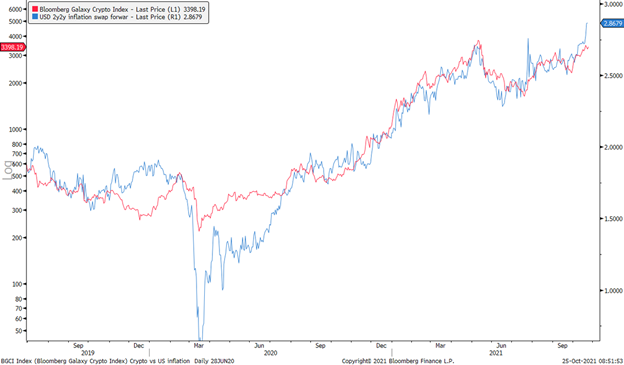

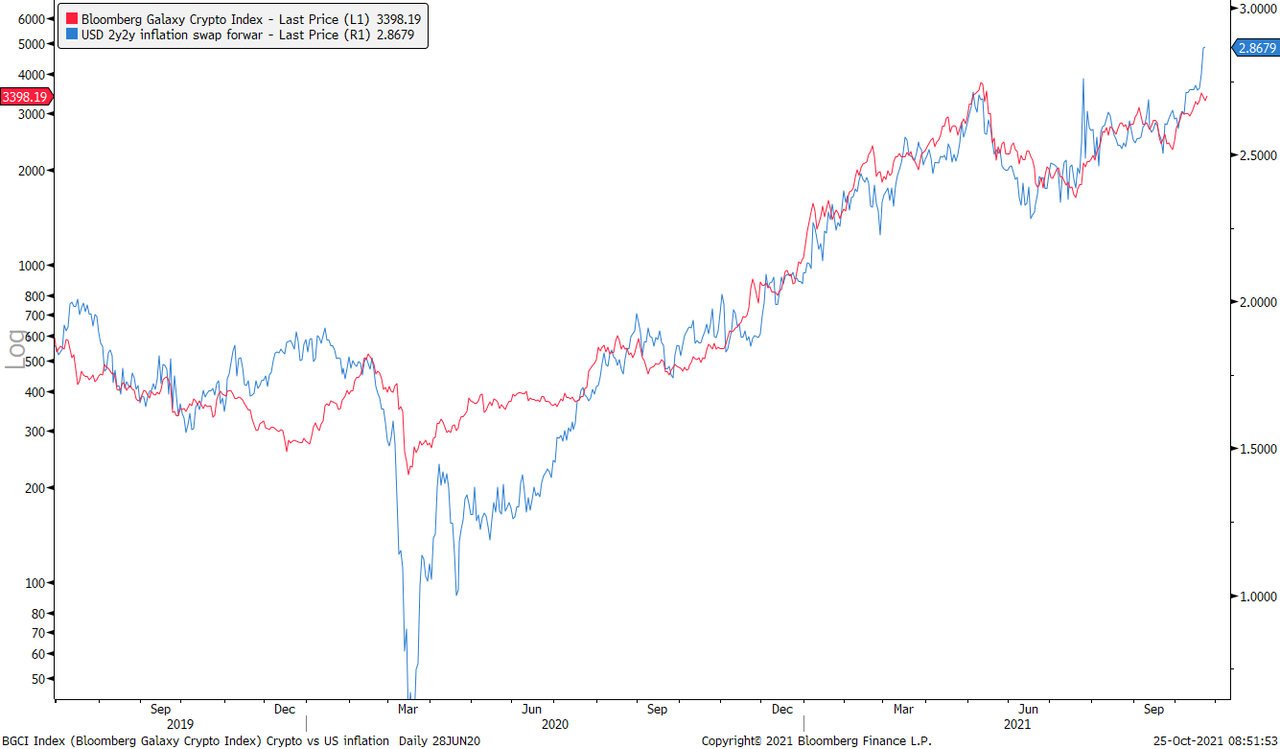

- Starting the return to normal monetary conditions could trigger stress in financial markets. In anticipation of the launch of the Bitcoin futures ETF, the first cryptocurrency began to be viewed more as an inflation hedge. Goldman Sachs has taken note of this relationship.

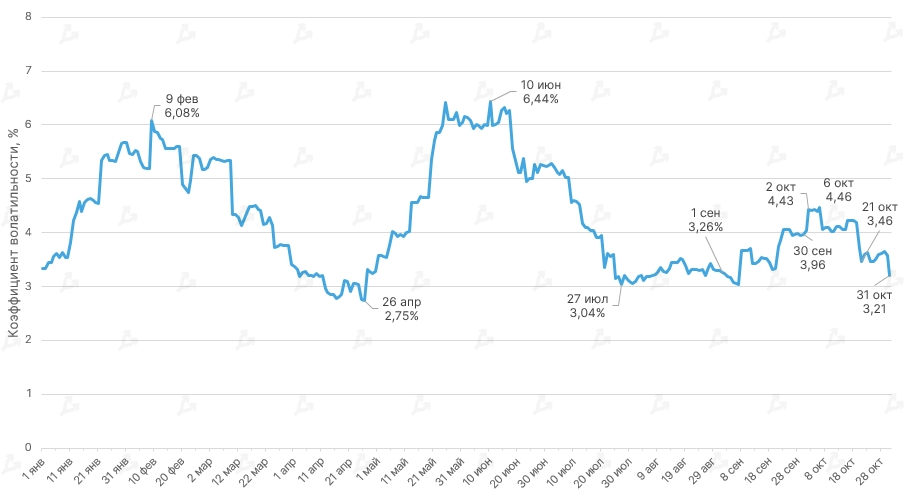

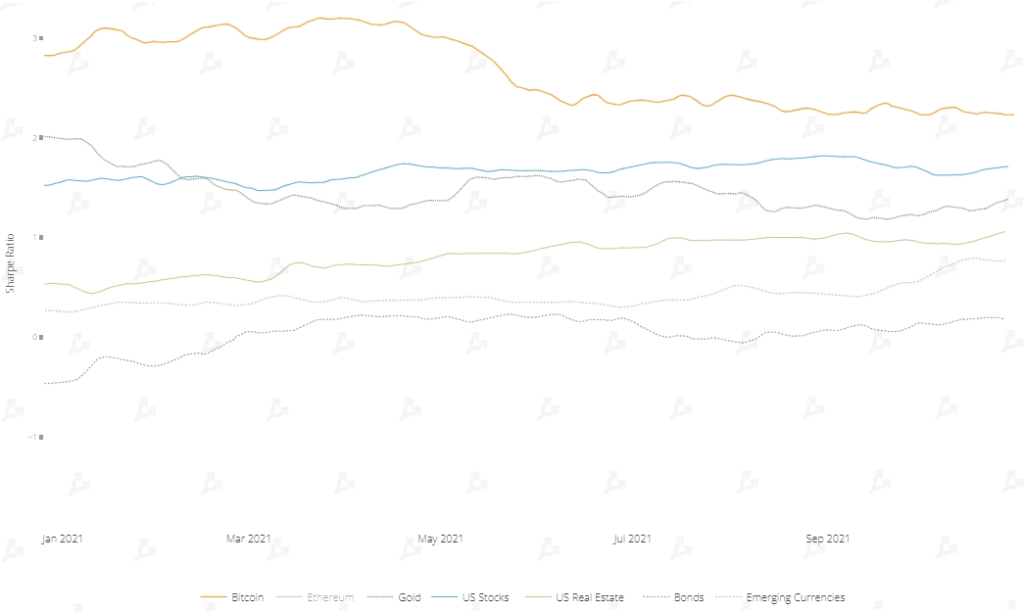

Market mood, correlations and volatility

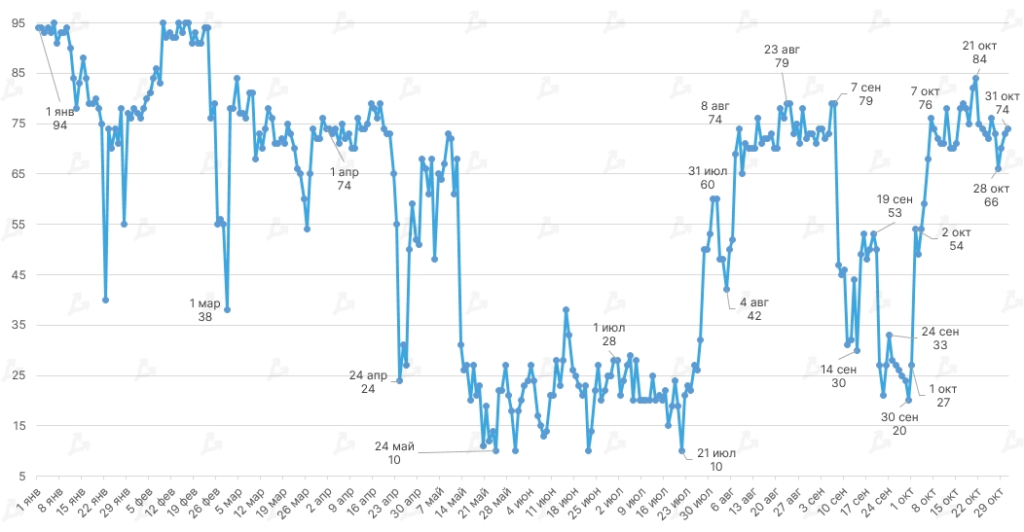

In October, bulls dominated the market. The fear-and-greed index, lifted substantially since the start of the month, signals growing investor optimism.

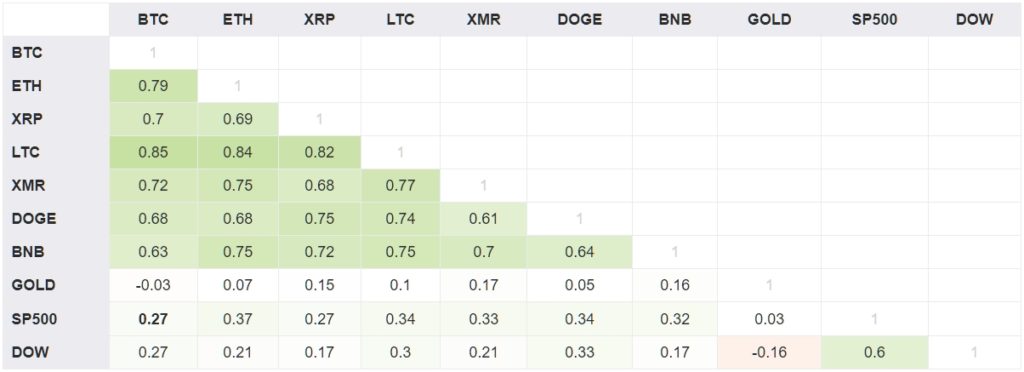

- Bitcoin and gold prices moved largely in opposite directions, but the correlation was a modest negative (-0.03). The correlation of Bitcoin with the S&P 500 and Dow Jones remained positive, strengthening versus September (0.27 vs 0.17).

- The rising correlation between Bitcoin and equities may be linked to the launch of crypto‑ETFs in the US. As the asset class is embraced by institutional investors, this relationship could intensify.

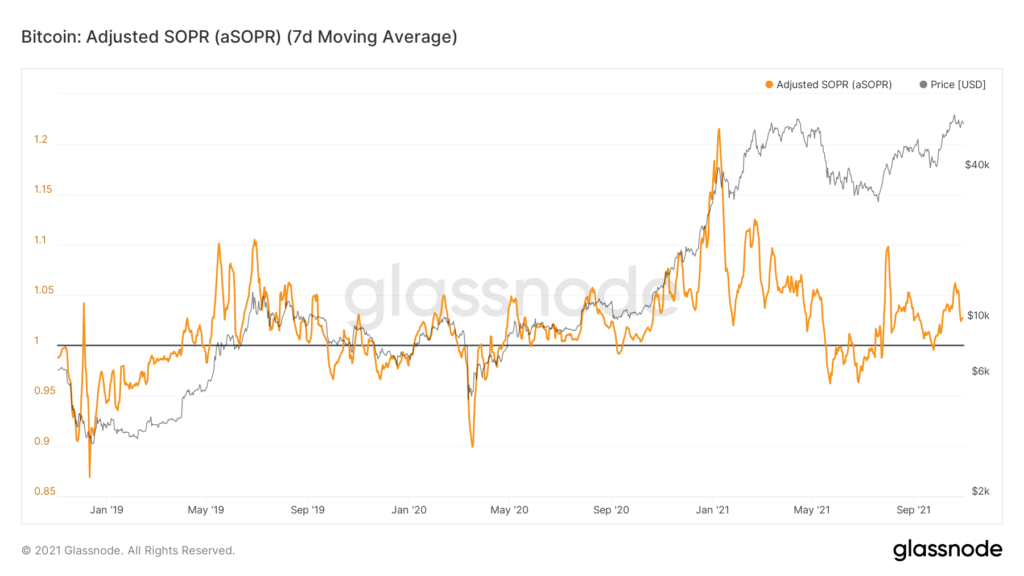

- In October the historical volatility indicator aSOPR remained above 1. This signals improving market sentiment and that most investors are taking profits rather than selling at a loss.

- The Stock-to-Flow Deflection indicator sits well below 1, implying Bitcoin is undervalued according to the PlanB stock‑to‑flow model. However, since mid‑July the indicator has risen, suggesting an approaching market-cycle shift.

- Throughout October the aSOPR indicator stayed above 1, signalling improving sentiment and that most investors take profits rather than selling at a loss.

- The Stock-to-Flow Deflection indicator sits well below 1, suggesting Bitcoin is undervalued per the PlanB model. Since mid‑July, the indicator has risen, implying an approaching cycle shift.

On-chain data

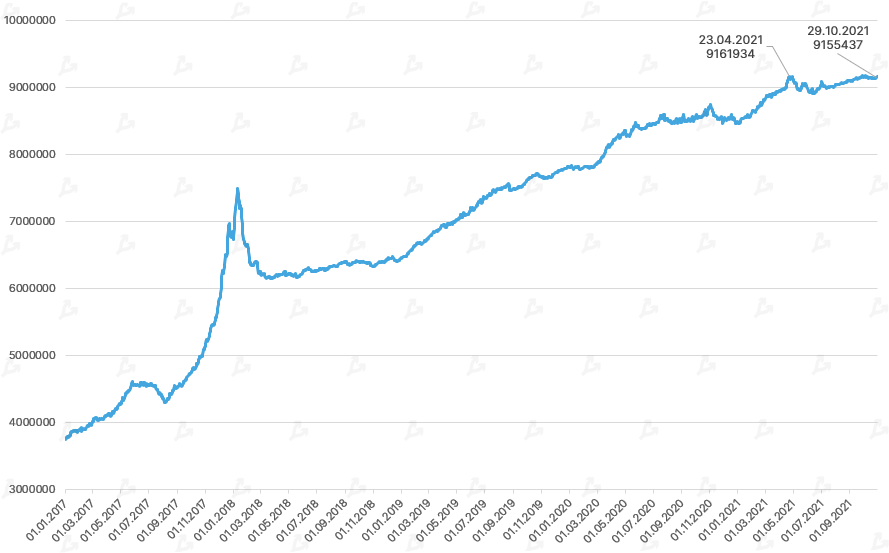

- The number of addresses with a balance of 0.01 BTC or more in October approached the historical high reached in April at 9,161,934.

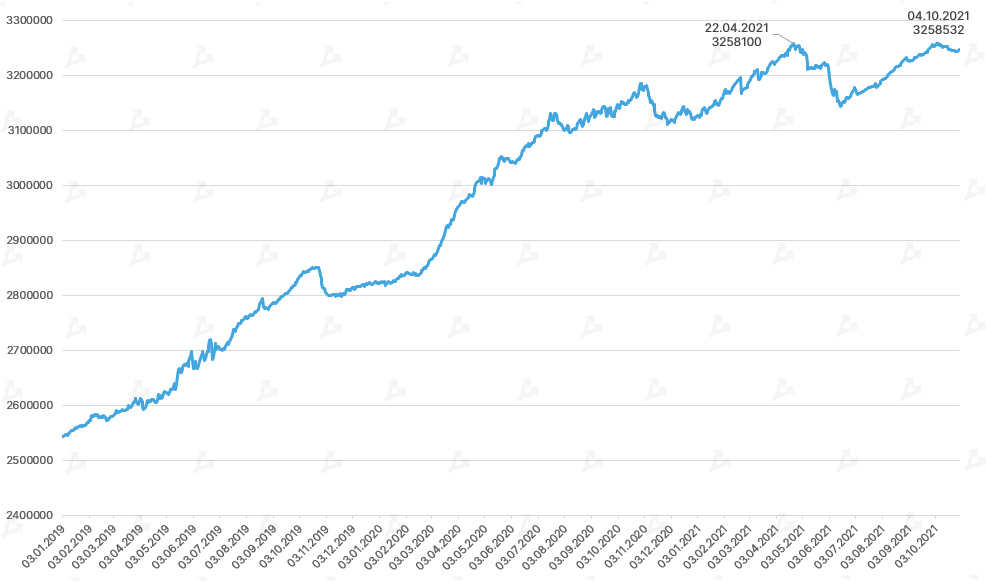

- The 0.1 BTC+ category hit a October high of 3,258,532. The previous peak was 3,258,100 on 22 April.

- Throughout October the historical volatility indicator aSOPR remained above 1. This signals improving market sentiment and that most investors take profits rather than sell at a loss.

- The Stock-to-Flow Deflection indicator sits well below 1. This implies Bitcoin is undervalued according to PlanB’s stock-to-flow model. Since mid‑July values have risen, signaling a forthcoming market-cycle shift.

Values of the MVRV Z-Score metric are still far from the overbought zone (highlighted in red). Therefore, the bull market is not yet over.

Ethereum

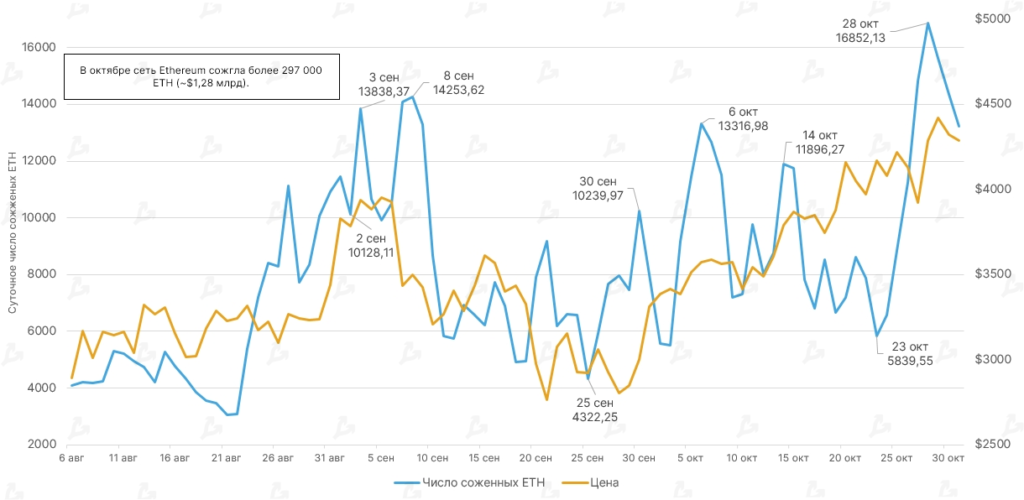

- Since the activation of EIP-1559 in August, the network burned more than 712,000 ETH (about $3 billion) — of which over 297,000 ETH in October (about $1.28 billion).

- Daily burned supply remains correlated with price: on October 29 Ethereum hit a fresh high above $4,400 — a day earlier the network burned a record amount (16,852.13 ETH).

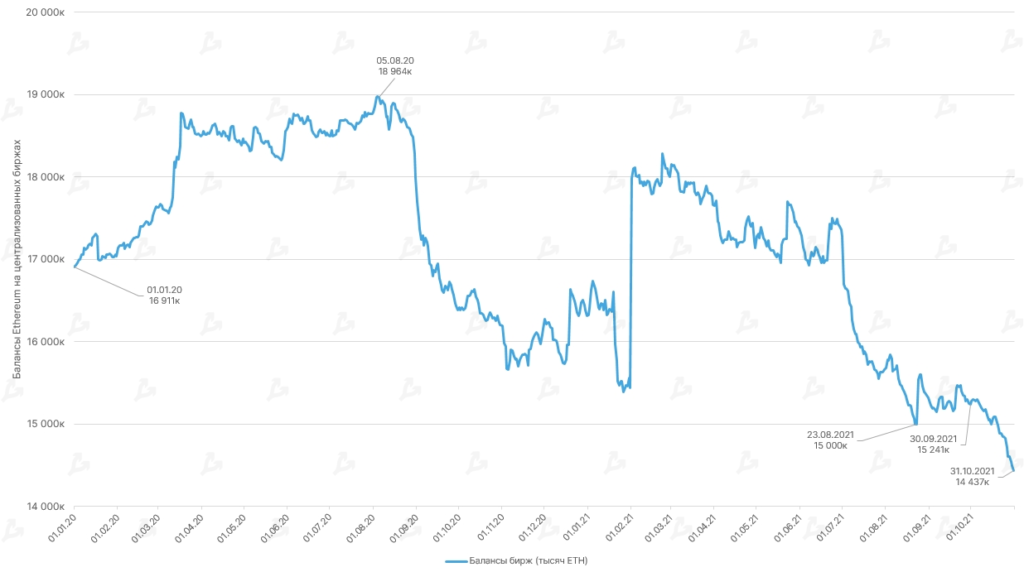

- The trend toward shrinking Ethereum balances on centralized exchanges strengthened: since the start of October, ETH supply on these platforms fell 5.52% and 11.57% year‑to‑date.

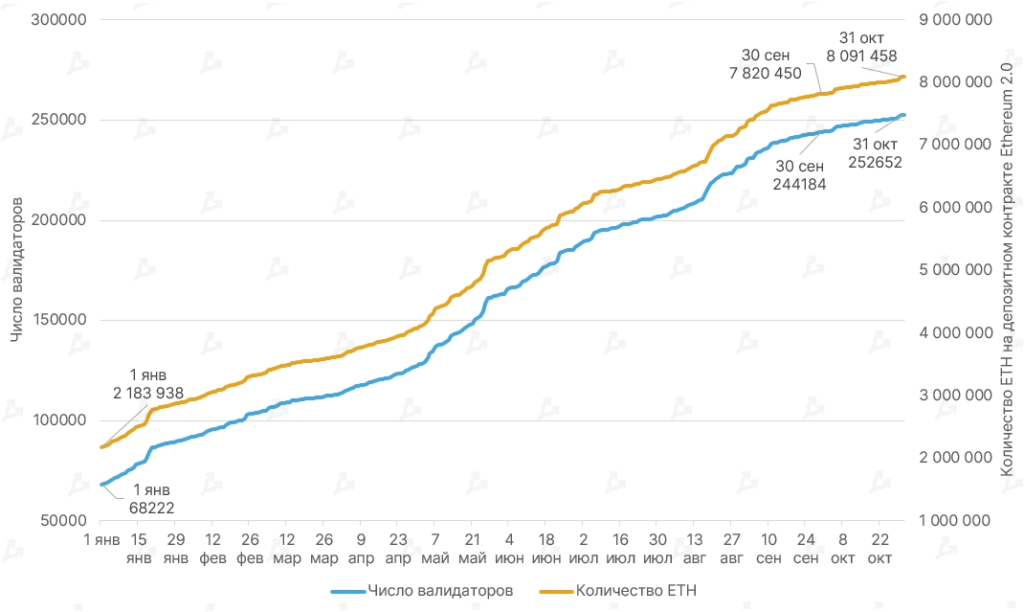

- In October the number of validators on the Beacon Chain exceeded 250,000 for the first time, rising 3.3% month‑over‑month.

- The number of ETH on the deposit contract continued to grow — by the end of October it exceeded 8 million. The market capitalization is now around $35 billion.

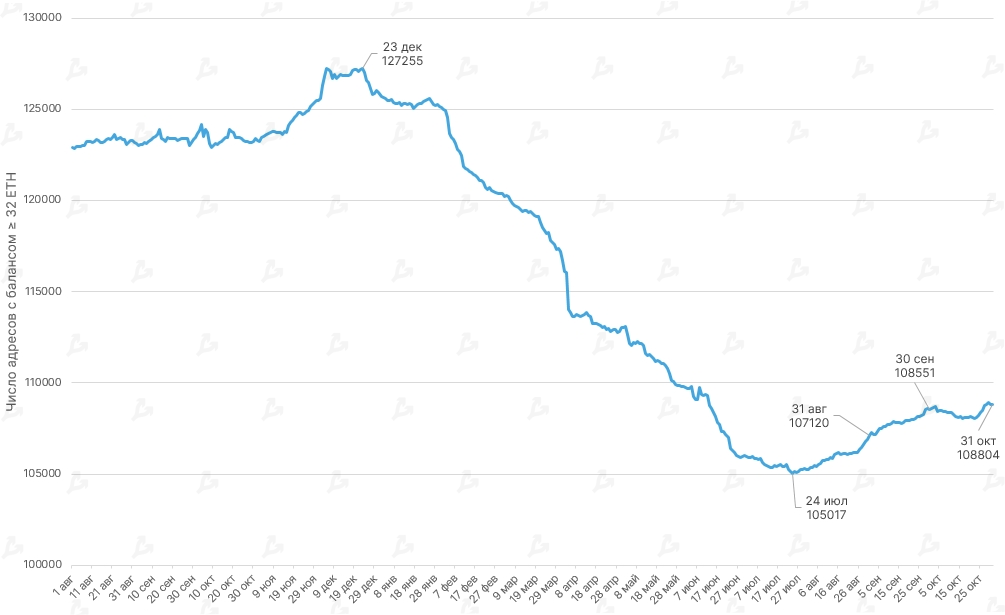

- The number of addresses with balance ≥ 32 ETH has been rising for the third month in a row, reaching 108,804 on 31 October.

Lightning Network

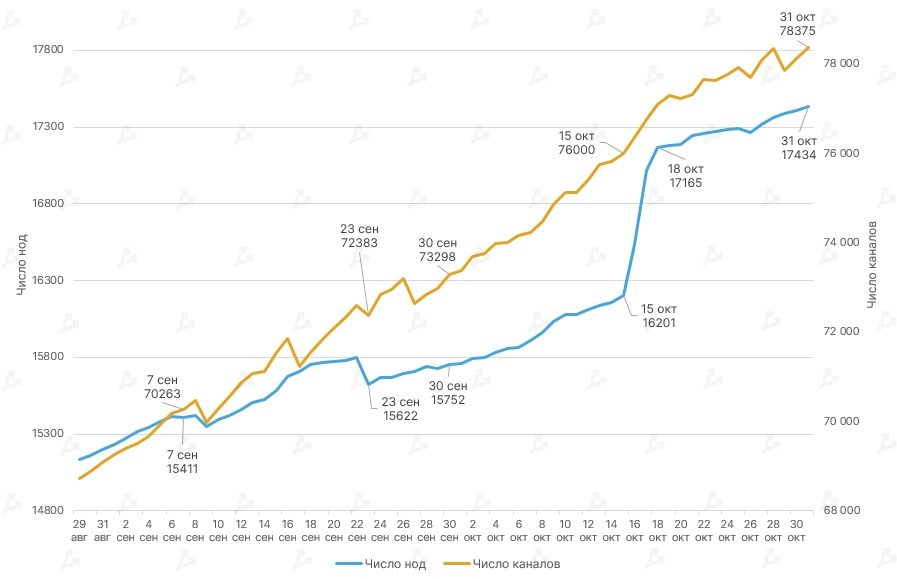

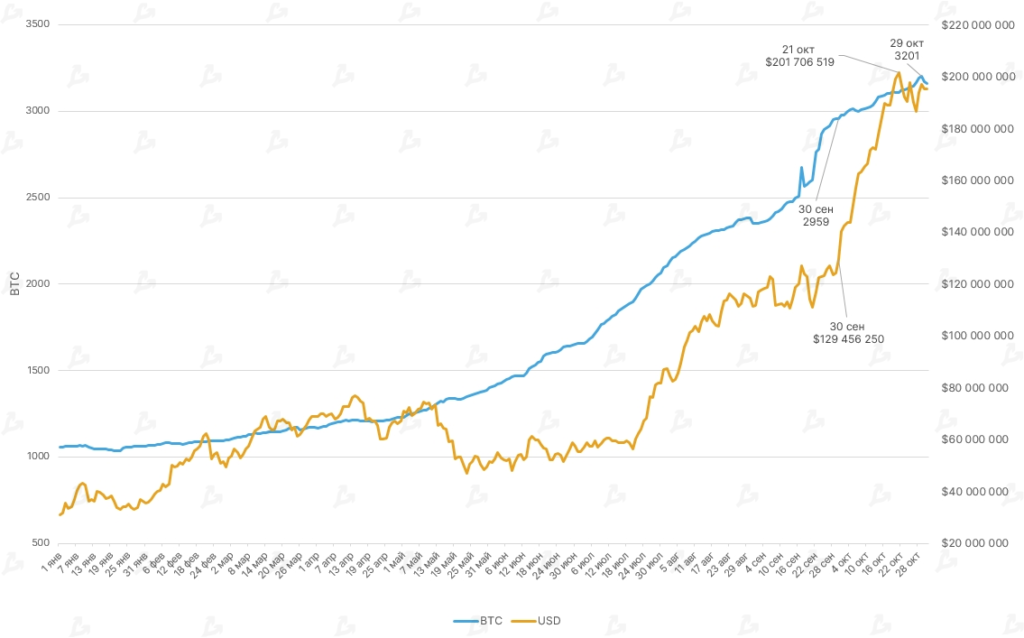

- With the appearance of simpler, more powerful node‑operators for the Lightning Network (LN), and its growing adoption in El Salvador, October saw a 10.5% rise in nodes and 7% more channels, reaching record levels. The LN capacity grew 6.9%, from 2959 BTC to 3162 BTC. September’s figure rose by 25%.

Mining, hash rate, fees

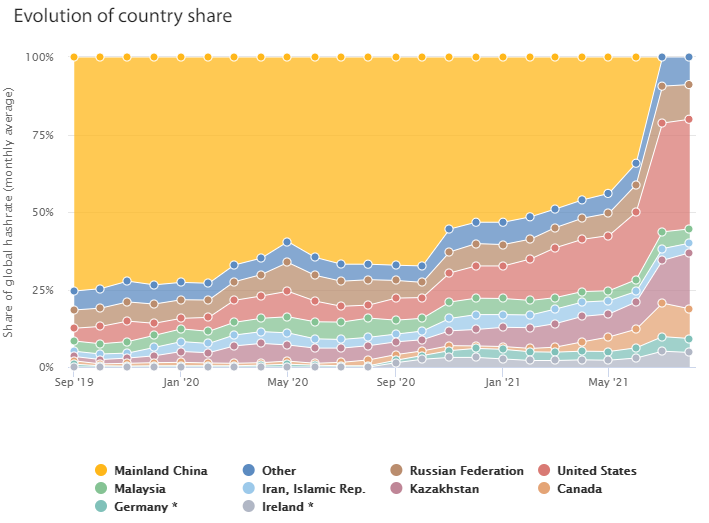

- In October the United States led in the share of Bitcoin hash rate (35.4%), up from to China’s exit. Russia remained around 11.2% and Kazakhstan about 18.1%.

- Hash-rate leadership in the US reflected the country’s broader role in the crypto market.

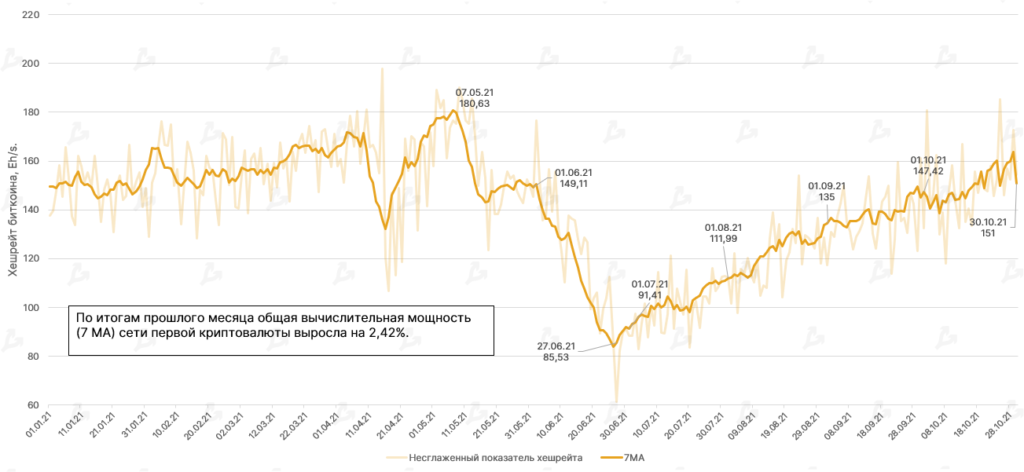

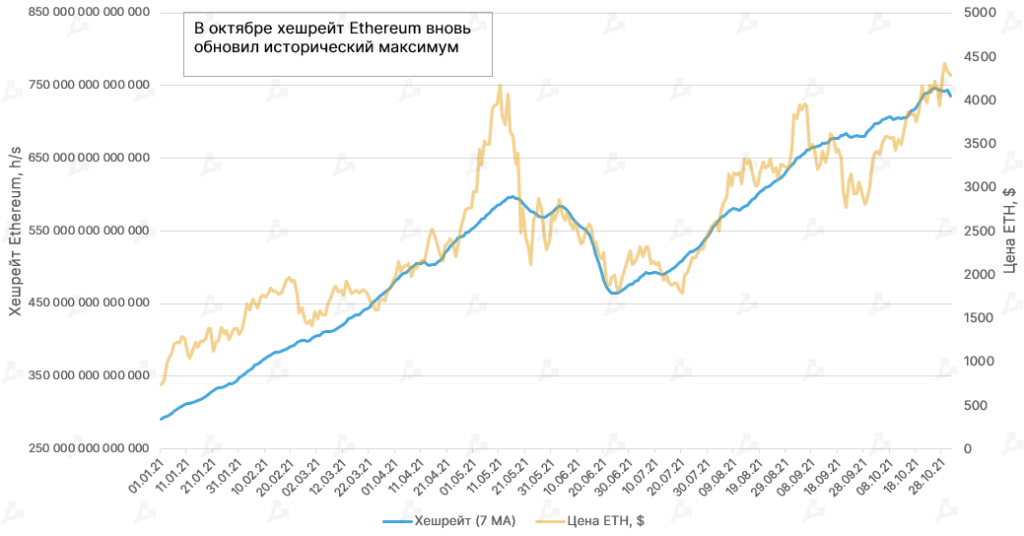

- The hash rate of Ethereum also hit new highs. Over the past month the correlation with price rose by 6%, with a record high of 746.12 TH/s on October 25.

- Against the NFT hype and DeFi growth, the average Ethereum transaction fee exceeded $50 again. The last time it was at these levels was early September, and before that — in May.

- Bitcoin’s average transaction fee mostly hovered around $3–$4. It will be interesting to observe after the Taproot soft fork, expected mid‑November, which should enhance privacy and scalability.

- Bitcoin miners earned $1.72 billion, roughly on par with the record $1.74 billion in March.

- October mining revenue from Ethereum miners reached a record $2.9 billion, including $1.34 billion in transaction fees (46.2% of total revenue).

- One clear driver of increased miner revenues is the rapid rise in prices.

Trading volumes

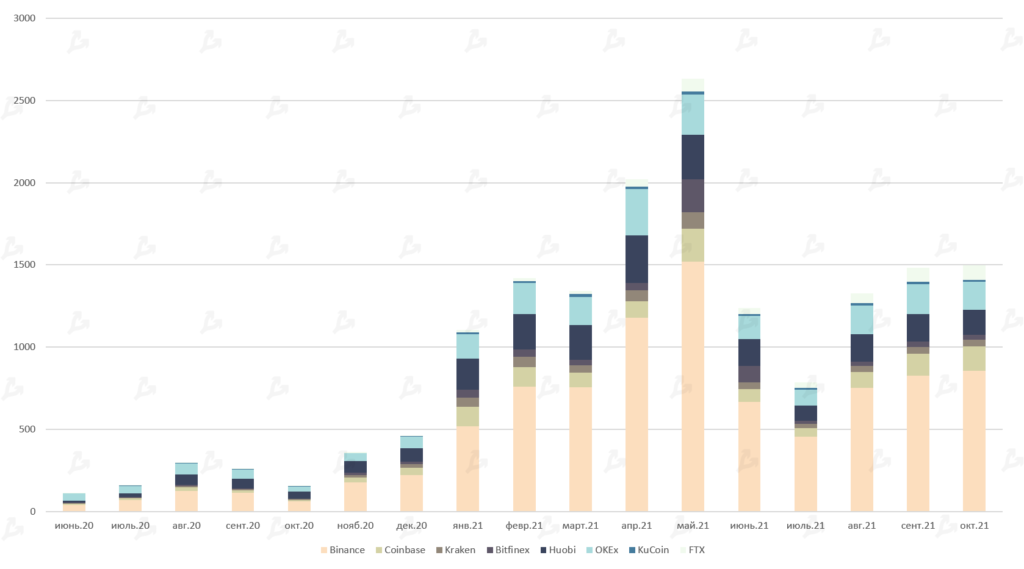

- Trading volume on leading spot platforms reached $1.497 trillion in October — the third-largest figure in 2021.

- The three leaders remain Binance ($856 billion), OKEx ($173 billion) and Huobi ($149.6 billion).

Futures and options

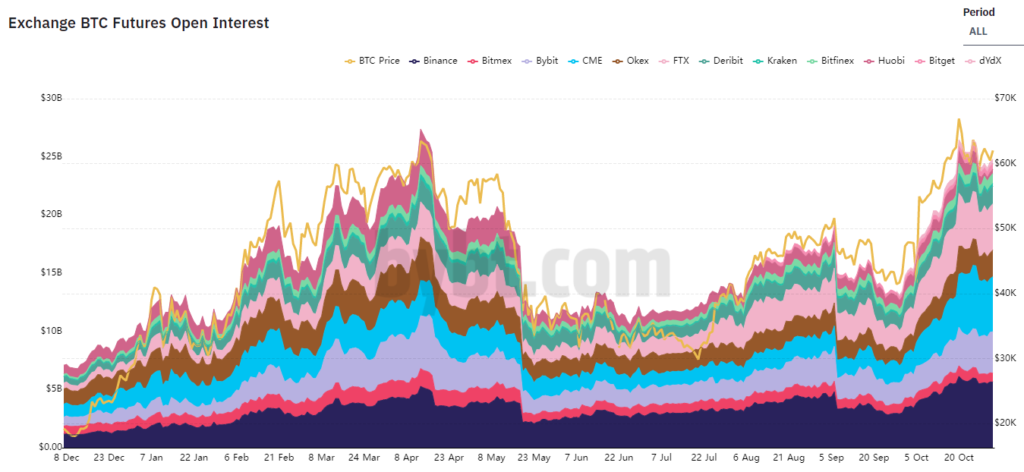

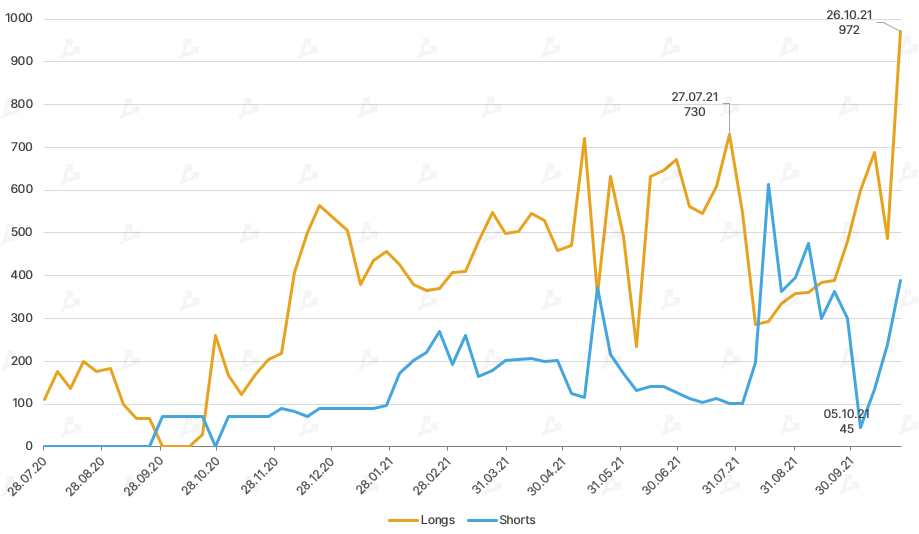

- Open interest (OI) in Bitcoin futures in October neared an all‑time high — peak 21 October saw $26.4 billion. Bitcoin itself hit a price high above $67,000. For the month, volume traded was $1.9 trillion.

- On CME, total open positions rose by 216% — from $1.72 billion to $5.45 billion. Rising Bitcoin prices were aided by demand from large investors, including institutions. OI on FTX and Binance also hit record highs at $4.5 billion and $6.1 billion respectively.

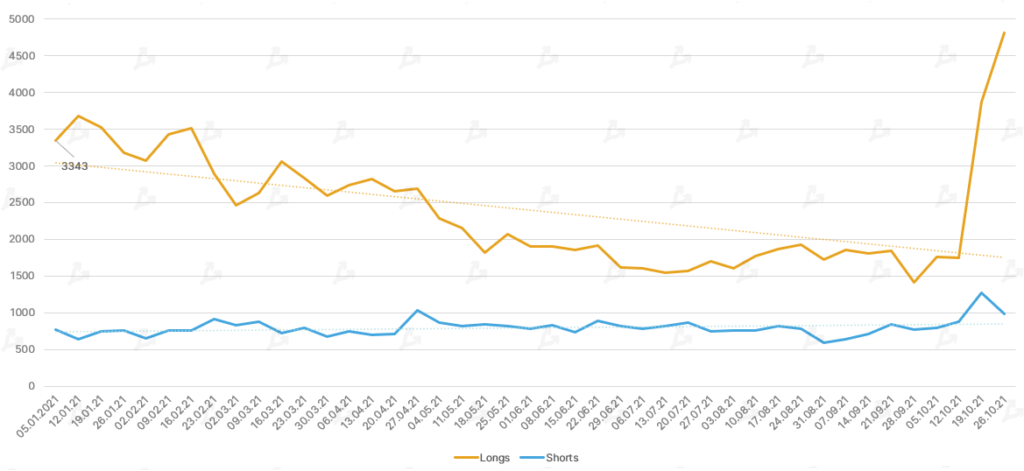

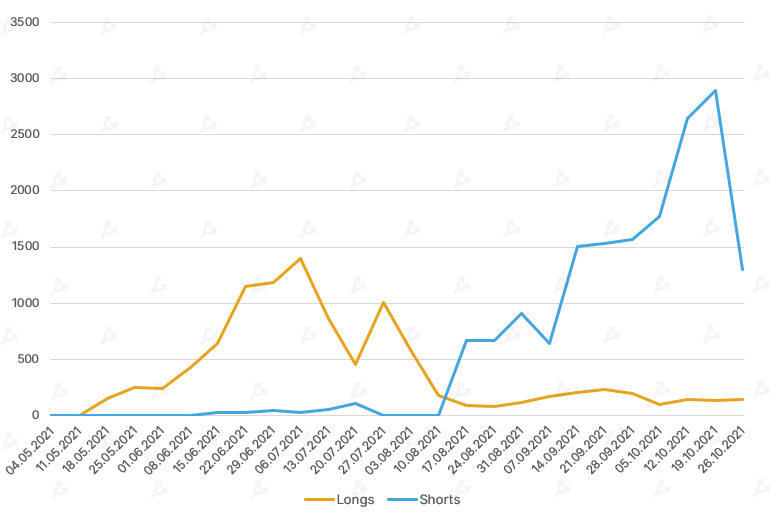

- Large Commercial players became even more dominant in the Non‑Commercial category; in contrast, Nonreportable and especially Commercial players increased long positions.

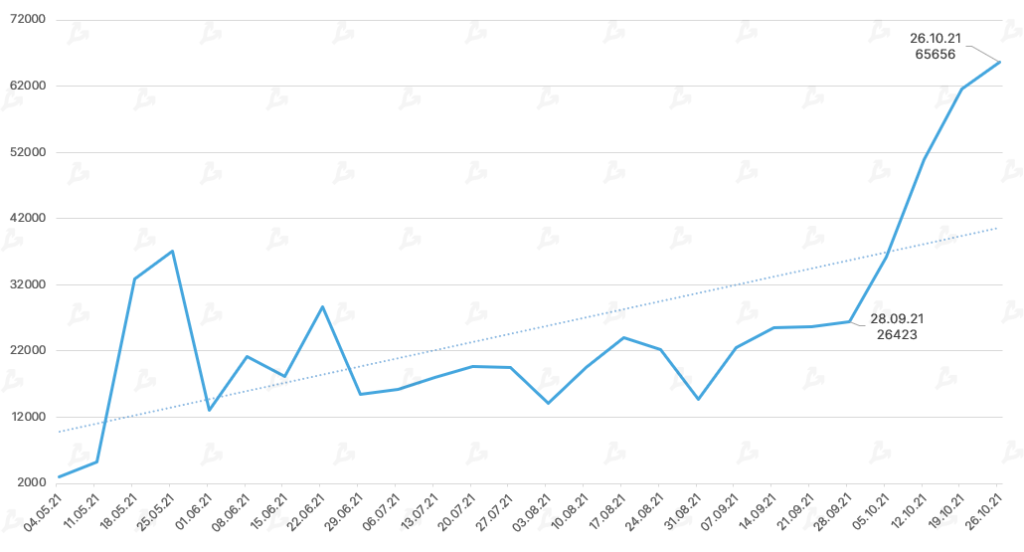

- Notably, open interest in micro Bitcoin futures surged about 150% in October, reaching 65,656 contracts. Each contract represents one-tenth of a Bitcoin.

- Relative to futures, CME terms mirror the broader futures market: long positions dominate among institutional investors, with a different mix elsewhere.

- Open interest in Ethereum futures also rose, with Non‑Commercial traders tending to short positions; Nonreportable and especially Commercials are building long positions.

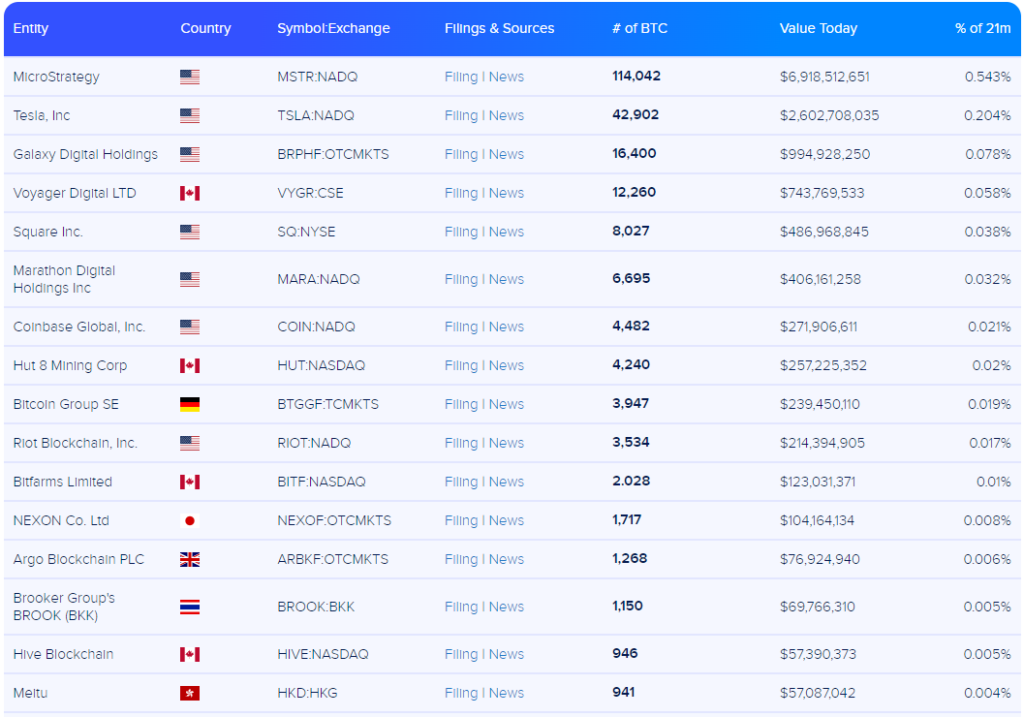

- Across listed companies, crypto reserves were largely unchanged in dollar terms as Bitcoin rose. Riot Blockchain was an exception, with its digital holdings rising from 2687 BTC to 3534 BTC over the month.

- Weekly inflows into crypto funds in October reached a record $1.47 billion, linked to the successful launches of the ProShares and Valkyrie Bitcoin ETFs. Investments in these products totalled $1.24 billion.

Major venture rounds

$700M

Digital Currency Group, the parent company of Grayscale, in a private stock sale to existing shareholders. Valuation placed at $10B.

$420M

Bitcoin exchange FTX in a Series B-1 funding round. Sixty-nine investors participated, valuation reached $25B.

$400M

crypto payments startup MoonPay in a seed round led by Tiger Global Management and Coatue Management. Media reports value the project at $3.4B.

$400M

centralised crypto lending platform Celsius Network in a round led by WestCap and CDPQ. Valuation exceeded $3B.

$298M

TradingView, a financial analytics portal. At the close of the investment round the platform was valued at $3B.

$250M

Alchemy, an infrastructure blockchain platform, in a Series C round. Investors include a16z, Pantera Capital and others; valuation around $3.5B.

$152M

Sky Mavis, developer of NFT game Axie Infinity, in a Series B round. Media reports value the company at $3B.

$100M

CoinList, a platform for token sales, in Series A. Valuation around $1.5B.

$65M

Animoca Brands, a blockchain games provider, valued at $2.2B.

Regulatory highlights

- Russian Duma will consider restricting non‑qualified investors’ crypto exposure.

- Deputy Finance Minister opposed plans to ban buying Bitcoin on foreign exchanges.

- Aksakov proposed legally to set out taxation for miners.

- Zelenskyy reinstated legislation on virtual assets for review.

- The head of the Ukrainian central bank outlined regulator concerns about digital assets.

- SEC will regulate stablecoins in the US.

- US Treasury issued guidelines on sanctions compliance for participants in the crypto industry.

- FDIC chief said regulators are focused on developing guidance for banks’ interactions with crypto markets.

Notable October events

On 19 October NYSE‑listed BITO began trading? an ETF on Bitcoin futures from ProShares. The fund posted the second-best debut by volume.

Banks and merchants will gain the ability to integrate cryptocurrencies into their products. The move includes Bitcoin wallets, crypto-enabled cards, and loyalty programs whose points can be converted into digital assets. Mastercard will be a partner of Bakkt.

The United States has displaced China from the top spot in Bitcoin’s processing power. Since May 2021 the US share rose from 17.8% to 35.4%. Russia sits third at 11.2%, with Kazakhstan at 18.1%.

On 28 October Facebook underwent a large rebrand — the company is now called Meta. This signals commitment to building a metaverse that runs on VR and AR headsets, mobile devices and gaming consoles. From 1 December, shares will trade under the ticker MVRS.

Quotes

{kind=link}