What is Aave?

Note: This article is outdated and awaiting an update.

Aave is a lending DeFi-protocol that lets users lend and borrow cryptoassets with variable and stable interest rates.

Who created Aave, and when?

The creator of Aave is Finnish programmer and Master of Laws Stani Kulechov.

While studying at the University of Helsinki, Kulechov became interested in blockchain technology and Ethereum and set out to build a decentralised crypto‑lending platform.

On May 1, 2017, Kulechov founded ETHLend. In November 2017 ETHLend launched the ETHLend.io P2P lending platform and held an ICO that raised $16.2m. The project sold 1bn LEND utility tokens; 300m (23%) went to the founder and team.

Amid the bear market, the protocol faced a liquidity crunch. In September 2018 ETHLend.io rebranded to Aave. In Finnish, Aave (pronounced “ah-veh”) means “ghost”. The team says the name reflects how “the brand continues to intrigue users with innovative technologies and aims to create a transparent and open infrastructure for decentralised finance”. ETHLend became a subsidiary of Aave.

In October 2019 the public testnet of Aave V1 went live.

On January 8, 2020, the mainnet of Aave’s first version launched on Ethereum.

In October 2020 the native AAVE token was issued and the LEND→AAVE migration took place at a 100:1 ratio.

In December 2020 the Aave V2 mainnet went live.

How does lending and borrowing work on Aave?

The platform initially used a peer-to-peer model (P2P), where users interacted via smart contracts. The drawback was that suitable counterparties and liquidity were not always available for efficient execution. The team therefore moved to a peer‑to‑contract (P2C) model, which most DeFi protocols use.

On a P2C platform, funds are deposited into a special contract that allows users to borrow assets instantly and pay interest for using the credit.

The platform has two types of participants: borrowers and lenders.

Borrowing

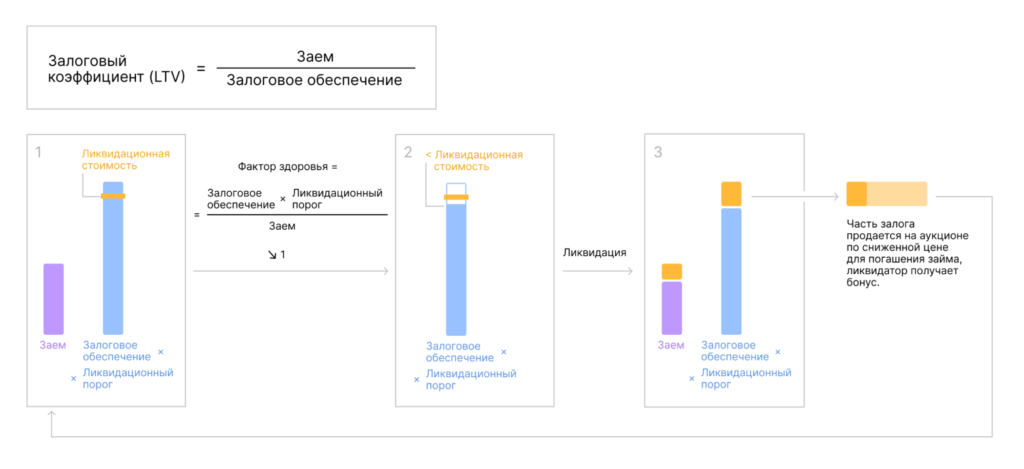

Users deposit assets into Aave as collateral. In return they can borrow a smaller amount, determined by the loan‑to‑value (LTV) ratio. LTV represents the maximum borrowing power against a given collateral.

Borrowing is overcollateralised to keep Aave solvent. The collateral’s value must exceed the value of the borrowed asset in line with its LTV, which depends on the collateral’s volatility and other risk parameters.

If, for example, the LTV is 80%, a user who posts 1 ETH as collateral can borrow at most the equivalent of 0.8 ETH. The LTV is set individually per collateral asset and is expressed as a percentage.

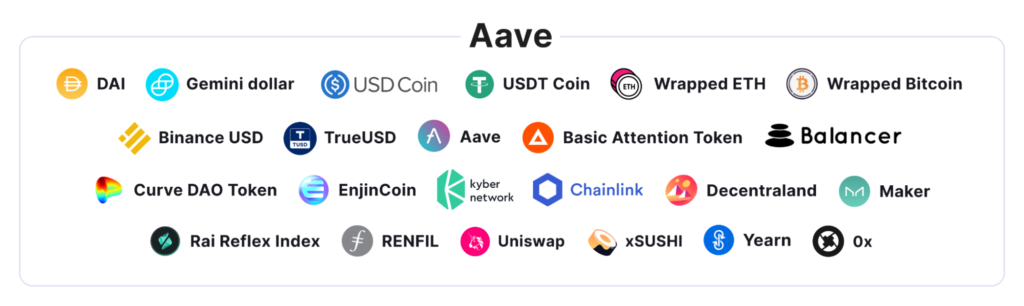

Users can post any token available on the platform as collateral:

Aave was the first lending platform to let users borrow and lend USDT. This stablecoin, along with Binance’s BUSD, Synthetix’s sUSD and Gemini’s GUSD, cannot be used as collateral because their governance introduces a potential single point of failure.

The AMM Liquidity Pool allows Uniswap and Balancer liquidity providers to use their LP tokens as collateral in the Aave Protocol. The Uniswap aDAI pool is the largest source of aToken liquidity outside Aave.

In total, Aave supports 22 assets in V1, 26 in V2 and 21 in the AMM Market. By contrast, the main rival, Compound, offers only 11 assets.

Lending

Users deposit assets into Aave and receive aTokens at a 1:1 ratio to the underlying. aTokens are akin to deposit certificates that accrue interest.

As long as protocol liquidity is available, aTokens can be redeemed 1:1 for the underlying. The aToken balance grows according to the protocol’s current interest rate.

- Lenders/liquidity providers deposit assets into Aave and receive ERC‑20 aTokens 1:1 (100 DAI ⇒ 100 aDAI).

- Borrowers deposit collateral assets to gain borrowing power. To avoid liquidation, they must keep their position “healthy” relative to its LTV.

- Lenders/liquidity providers can redeem aTokens 1:1 for the deposited asset. The aToken balance grows with the interest paid by borrowers. Liquidity providers also earn fees from flash loans.

- To repay, users must return the borrowed asset plus interest. Until repayment, the collateral remains locked in the protocol.

How does the liquidation mechanism work?

Aave’s liquidation mechanism hinges on the Health Factor.

The Health Factor (HF) measures the safety of a user’s position relative to the borrowed amount and the underlying value. The higher the HF, the safer the position.

- HF ≤ 1: up to 50% of the debt can be liquidated.

- HF > 1: the collateral’s value relative to the debt can change according to (1−HF)/HF.

For example, at HF = 2 the debt is liquidated when the collateral’s value relative to the loan drops by 50%.

HF formula:

HF = Σ(collateral value × liquidation threshold) / debt (in ETH)

Thus, when HF rises as collateral appreciates, the liquidation risk falls. If HF drops sharply, the user can repay all or part of the loan, or add collateral. A lower HF can result not only from falling collateral prices but also from rising prices of borrowed assets.

Price data come from Chainlink oracles.

Liquidation bonus is the premium applied to collateral acquired by liquidators when a position hits its liquidation threshold.

Liquidation threshold is the level at which a loan is deemed undercollateralised and becomes eligible for liquidation. If the liquidation threshold is 80%, the loan is liquidated when debt equals 80% of collateral value. The threshold is set per collateral and expressed as a percentage.

Liquidators can repay up to 50% of a borrower’s debt. In return, they receive the corresponding amount of collateral plus a bonus.

The bonus depends on the asset. For example, it is 5% for ETH and 15% for YFI, and so on.

Example 1: Single‑collateral asset

- User A deposits 10 ETH as collateral and borrows DAI worth 5 ETH.

- HF falls below 1 — the loan becomes eligible for liquidation.

- Liquidators can repay up to 50% of the borrowed amount — DAI worth 2.5 ETH.

- The liquidator may choose to receive ETH as collateral (with a 5% bonus).

- The liquidator receives 2.5 + 0.125 ETH for repaying DAI worth 2.5 ETH.

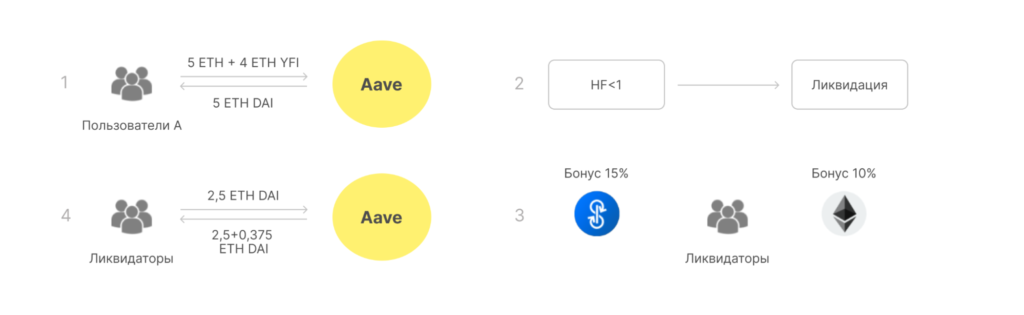

Example 2: Multi‑collateral assets

Aave: liquidation with multiple collaterals. Source: Coin 98 Insights.

- User A deposits 5 ETH and YFI worth 4 ETH, and borrows DAI worth 5 ETH.

- HF falls below 1 — the loan becomes eligible for liquidation.

- Liquidators can repay up to 50% of the borrowed amount — DAI worth 2.5 ETH.

- This time the liquidator opts for YFI, which pays a higher bonus (15% versus 5%), instead of ETH.

- The liquidator receives YFI worth 2.5 + 0.375 ETH for repaying DAI worth 2.5 ETH.

No more than 50% of a user’s position can be liquidated, which has pros and cons.

- Pro: users retain part of the position. They do not lose everything, can wait for a rebound in collateral value, repay the debt and withdraw the remainder.

- Con: if the collateral price continues to fall, or the borrowed asset continues to rise, the risk of losing the remaining 50% increases.

How does the risk‑mitigation mechanism work?

If liquidation does not fully resolve a position, loans can become undercollateralised and turn into bad debt.

The risk‑mitigation framework includes the Safety Module — Aave’s insurance mechanism.

It maintains an insurance fund for cases where an asset reserve faces a shortfall event. A precedent is “Black Thursday” in March 2020, when MakerDAO investors lost $8.325m. In a shortfall, AAVE holders can vote to recapitalise the pool.

Users stake AAVE into the Safety Module and receive Stake AAVE (StkAAVE) in return. When they unstake, AAVE is returned and StkAAVE is burned. Up to 30% of StkAAVE can be used to cover a shortfall. In exchange for the risk of losing part of their StkAAVE, users receive Safety Incentives. A total of 550 StkAAVE is distributed daily among all Stake AAVE holders in the module.

There is a ten‑day cooldown period during which users can withdraw StkAAVE and the incentives paid in the same asset. This helps avoid a panic run before the protocol triggers the shortfall coverage process via governance. The decision to trigger coverage is taken by holders of AAVE and/or StkAAVE through a joint vote. Voting weight is proportional to the number of tokens held.

During shortfalls, funds needed for coverage are sold via auction, with proceeds directed to the One Backstop Module. Users deposit stablecoins or ETH into it prior to sale on open markets.

If the shortfall is not covered, users can vote for a Recovery Issuance of AAVE tokens. These are auctioned to replenish the backstop, then sold on open markets.

The project’s treasury holds the Aave Ecosystem Reserve and funds collected by ecosystem collectors. As of July 2021, the total exceeded $700m.

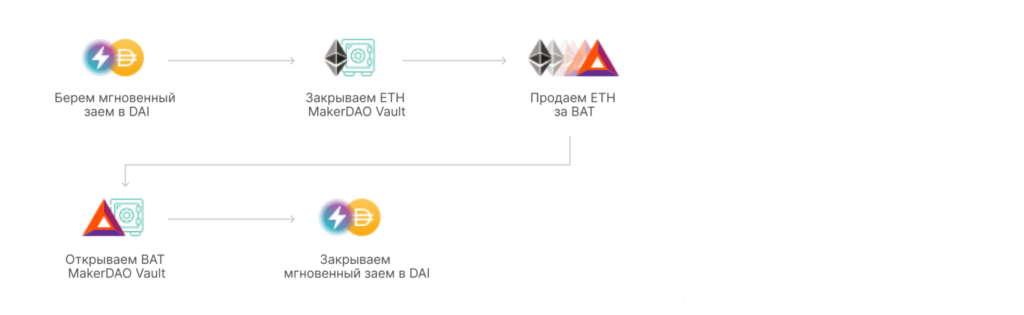

What are flash loans?

Aave offers so‑called flash loans — uncollateralised loans in which borrowing and repayment occur within the same block.

For example, a user who borrowed on Maker might see their Vault approach liquidation as collateral falls. They can sell part of the collateral for DAI to repay the debt, avoiding liquidation on Maker even if they do not hold enough DAI in their wallet.

Flash loans can be used for:

- portfolio rebalancing via multiple operations in a single transaction to optimise fees;

- arbitrage;

- self‑liquidation;

- collateral swaps.

The fee is 0.09% of the borrowed amount, paid to lenders.

There is no dedicated user interface for flash loans yet, but they can be used via Furucombo and similar services.

What is the interest‑rate model?

There are two types of interest rates:

- Stable (fixed) rates that do not change over time;

- Variable rates that change with supply and demand.

Borrowers can switch between variable and stable rates.

In the short term, stable‑rate borrowing behaves like fixed‑rate borrowing, but rates can be rebalanced in the medium to long term if market conditions change abruptly.

What are Aave V2’s features?

Collateral swap (Collateral Swap)

Users can swap their collateral from one token to another — for example, from ETH to DAI if they expect ether’s price to fall.

Batch flash loans (Batch Flash Loans)

Users can borrow multiple assets at once within a single Ethereum transaction.

Debt tokenisation (Debt Tokenization)

In V2, borrowers can receive tokens that represent their debt. This, in turn, enables native credit delegation.

Native credit delegation (Native Credit Delegation)

This feature allows a liquidity provider to deposit funds into the protocol and delegate the right to borrow to another user. The delegate can thus borrow without posting their own collateral.

Loan terms and execution are set either through legally binding agreements or on‑chain via smart contracts.

Compared with V1, Aave V2 is more gas‑efficient. In some cases, users can save up to 50% on fees.

How does Aave’s treasury work?

Aave’s treasury consists of two funds.

The first is funded from three sources:

- Collector (the system that collects a share of protocol revenues);

- Reserve Factor — the protocol’s share of interest;

- One third of flash‑loan fees.

Proceeds from the first fund are used to develop Aave.

The second fund is the ecosystem reserve (3m AAVE). It covers Safety Incentives on short‑term loans, liquidity‑mining rewards, grants and protocol development.

Both funds are governed by the Aave community.

How is Aave evolving?

In July 2020 the company behind Aave received an e‑money institution licence from the UK’s Financial Conduct Authority (FCA). This enables users to buy stablecoins and other digital assets with fiat and use them in the Aave protocol.

In summer 2020 Aave raised $3m by selling LEND tokens to Framework Ventures and Three Arrows Capital.

In October 2020 the project raised $25m from Blockchain Capital, Standard Crypto, Blockchain.com and others.

At the end of 2020 Aave transferred admin keys to LEND holders. The first Aave Improvement Proposal (AIP) put to a vote and approved by the community introduced the AAVE governance token and the 100:1 migration from LEND.

For summer 2021 the launch of the institution‑focused Aave Arc DeFi platform was planned. Initially it would support four assets — bitcoin, Ethereum, Aave and USD Coin (USDC) — and offer the same services as the main platform. Access is limited to “institutions, corporations and fintechs” that pass Fireblocks’ KYC checks. Aave Arc is to move to decentralised governance in future.

In July 2021 Mr Kulechov announced plans to launch a Twitter alternative on Ethereum. The new platform would let users monetise content and take part directly in governance. It could launch by the end of 2021.

aTokens are used as collateral for in‑game characters in Aavegotchi, a game reminiscent of Axie Infinity. An Aavegotchi character is an ERC‑998 NFT that owns a deposit in a DeFi application.

Links: