In 2024 Solana became the most popular blockchain network thanks to the frenzy around memecoins—the calling card of the current bull market. That has led some analysts to suggest that the native token, SOL, could overtake ETH by market capitalisation.

Oleg Cash Coin examines how well such forecasts stack up.

SOL’s performance

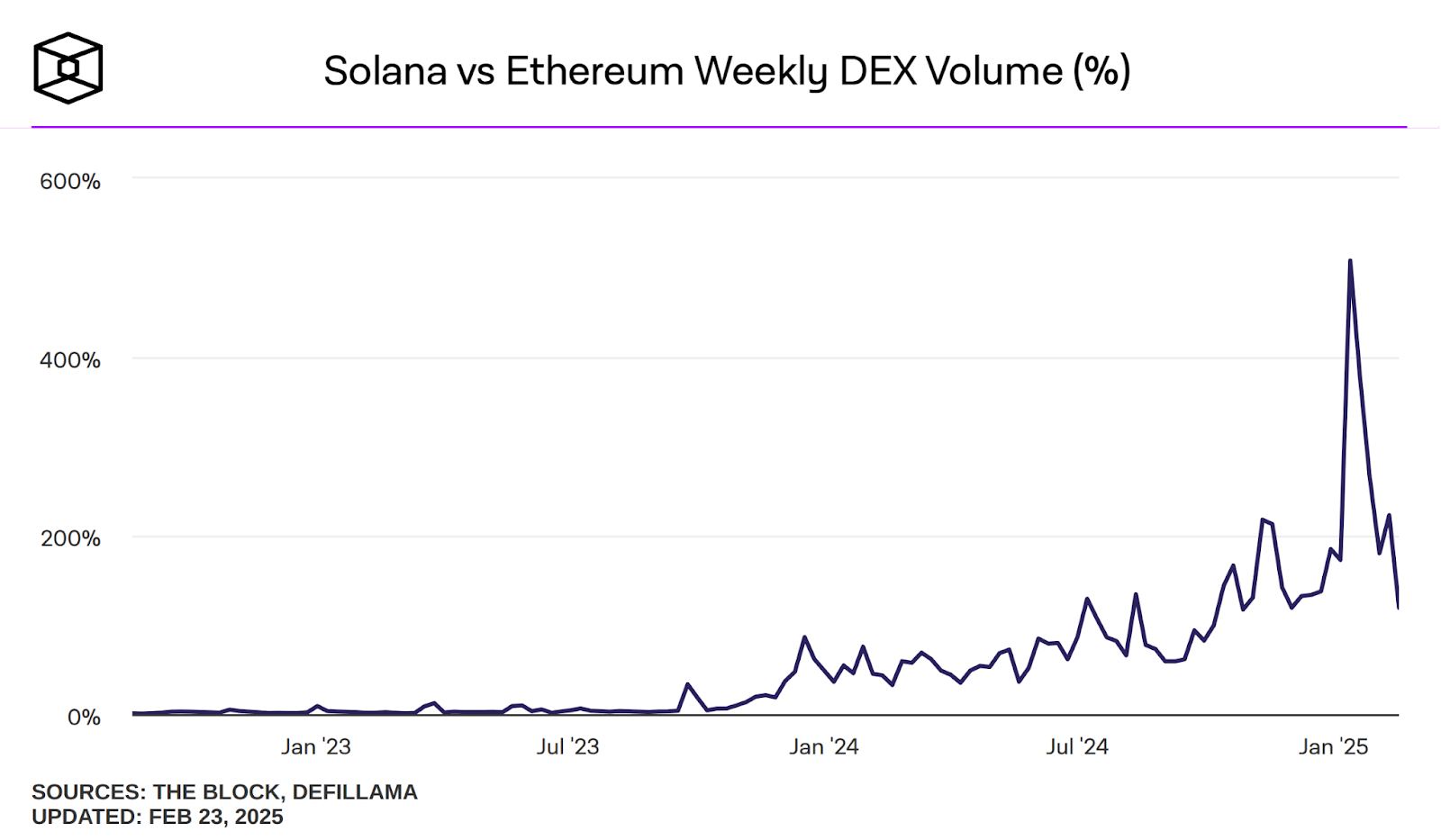

At one point Solana surged to the top by trading volume on decentralised exchanges (DEXs), depriving Ethereum of its monopoly over DeFi and smart contracts.

Most modern networks are both fast and cheap, making technological advantages marginal. What matters instead are network effects, ease of user experience and the depth of liquidity.

The era of breakthrough blockchain mechanics likely ended in 2017–2020. Today most things are built atop ready-made solutions, dressed up in shifting narratives.

“Some smart people tell me that Solana has a serious community of smart developers, and now that the awful money opportunists have been washed out, the chain has a bright future. It’s hard for me to tell from the outside, but I hope the community gets its fair chance to thrive,” — wrote on December 30, 2022, Ethereum’s founder Vitalik Buterin.

A few days earlier the first meme token on Solana—Bonk—had appeared. It became the starting point for a whole trend in the bear cycle that followed the collapse of FTX. Notably, the failed exchange was among the largest investors in Solana tokens and held more than 58m SOL (~$8bn at today’s price).

Not everyone believes that the network’s fundamental changes, Sam Bankman-Fried’s interest and the token’s rise from $8 to $250 were merely coincidental. Among the sceptics is Binance’s founder, Changpeng Zhao (CZ).

“Memecoins were incredibly popular during [2024]. Major exchanges did not benefit from this trend the same way blockchain platforms did, especially on Solana. There are suppositions about the reasons for what is happening, although I cannot confirm the details. Solana had close ties with FTX. After its collapse, many people who lost money received no support and turned to Pump & Dump schemes,” — said CZ in an interview with Wu Blockchain.

He also noted that Solana, like other blockchains, still suffers from congestion during traffic spikes. Even so, the exchange’s founder acknowledged that Solana proved an ideal platform for memecoins, being in the right place at the right time.

“It is similar to how Binance benefited from the ICO boom in 2017,” CZ concluded.

Liquidity, unlocks, inflation

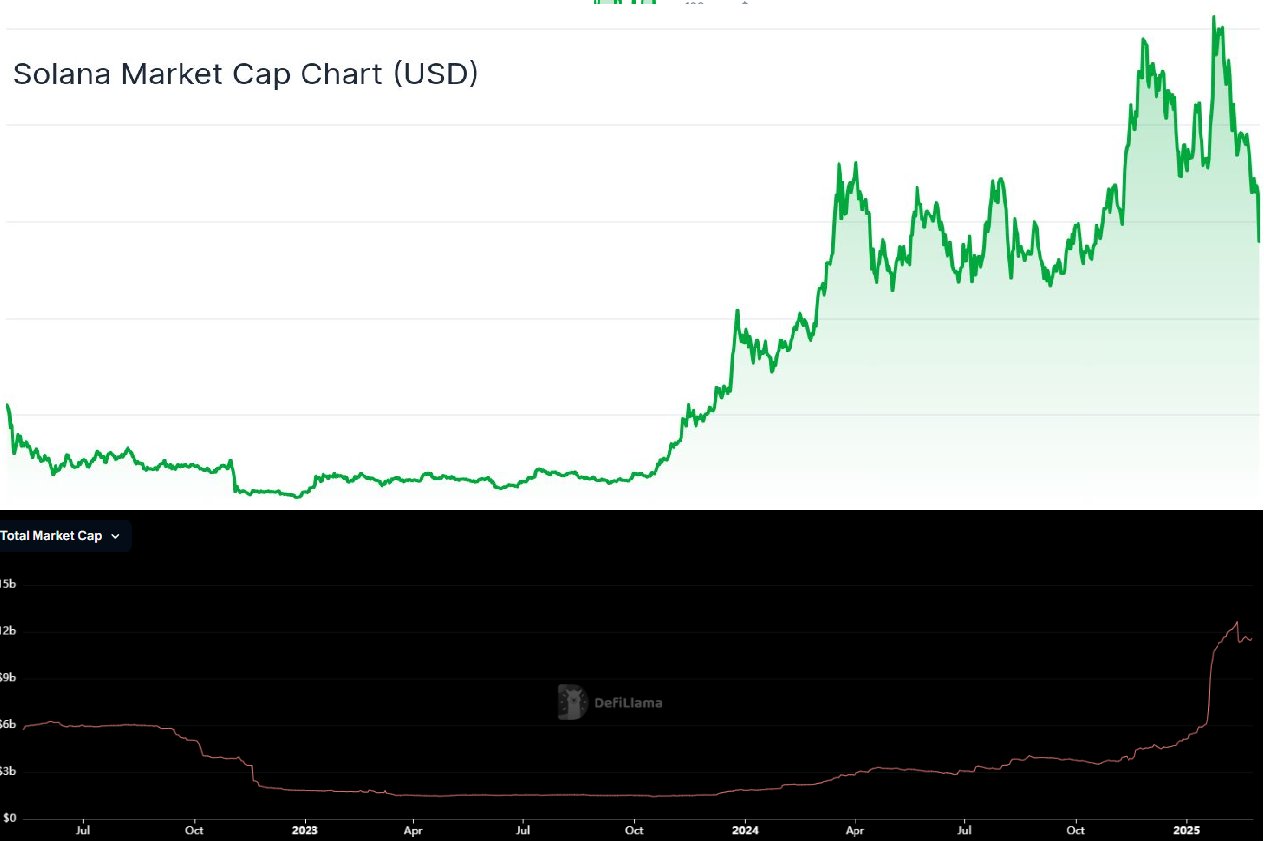

But the story may not be about memes at all. One of the largest asset managers, VanEck, forecasts Solana at $520 by end-2025 solely on the basis that the US is expected to see an increase in the M2 money supply.

Analysts reckon this will channel liquidity into risk assets, including cryptocurrencies. In the same outlook, VanEck casts Solana as one of the leading smart-contract platforms. With one important caveat: circulating supply is modelled at 486m SOL, implying a market value of $252bn.

Yet by late February 2025 the actual figure already exceeds 494m. By the end of March, unlocks of around 10m SOL are scheduled on the network, with a further 15m SOL before year-end.

Although exact unlock amounts are not specified, monthly investor allocations will continue at least until 2028. One should also factor in SOL’s sizeable programmed inflation of 4.7% a year.

15.725M of SOL ($3,066,430,575) will be unlocked over the next 3 months (Feb-Apr), much of that coming from the FTX estate holdings from transactions they did with the Solana foundation in 2020.

FTX / Alameda and Solana Labs / Solana fdn entered into 5 transactions, in total the… pic.twitter.com/BI19GtWitD

— R? (@Ren_gmi) February 16, 2025

On a back-of-the-envelope basis, that would put SOL’s supply at around 526m by the end of 2025.

In this respect Solana resembles late-stage Ethereum before the move to Proof-of-Stake, when inflation hovered around 4% and higher before falling towards zero. SOL also has similar coin-burning mechanics.

From this angle, Solana and Ethereum are indeed comparable. Technologically they may differ, but economically the parallels are easy to draw.

Back to VanEck’s forecast. Contrary to common belief, liquidity is not the fuel for a token’s price appreciation on any given chain; it is more often a by-product of gains already achieved. You can see this on smaller L2 networks that depend entirely on outside capital inflows.

One reason to mint new USDT is the lack of liquidity to sell crypto after prices rise, not the other way round. For larger networks the stablecoin-cap charts will be less spiky than ARB’s, but the pattern is similar.

The ARB and SOL charts show that most liquidity forms on-chain after price appreciation has already occurred, not beforehand. One can infer that the “arrival of money” often reflects profit-taking during periods of elevated demand.

Ethereum displays the same dynamics and correlation seen across most blockchain networks. In general their behaviour is similar, aside from sharp jumps on stablecoin charts.

Returning to Solana, one of the most important metrics for any further positive price action is the level of liquidity in the system.

Rather than a rising native token, it is growth in stablecoin capitalisation within SOL that will signal interest in the project. And this is, of course, a macro indicator unrelated to trading.