Strategy has established a $1.44bn reserve to ensure “stable and uninterrupted” dividend payments should the price of the first cryptocurrency fall, CEO Phong Le said.

The fund was built by selling MSTR shares over the past nine days. The aim is to secure at least a year’s cover for obligations to shareholders and, over time, to expand the safety buffer to more than two years of payouts.

“The nature of bitcoin implies volatility. Our task is to create a digital debt instrument for investors who are sensitive to market swings, and to guarantee them complete independence of dividend payments from fluctuations. It is precisely to secure this guarantee that we formed a fund in US dollars,” said Strategy founder Michael Saylor.

At the same time, management confirmed it is ready to sell digital gold if needed. Le allowed for such a scenario if mNAV drops below 1.

“There is some scepticism around our approach: some believe that we lack the ability, willingness or resolve to sell part of our bitcoin holdings to finance the dividend policy. This narrative is periodically used to create a negative perception of the company, and our task is to dispel it completely,” Saylor added.

According to him, the reality is the opposite: the firm not only has the right and ability to sell cryptocurrency, but can also realise assets that have appreciated significantly. After such operations, Strategy will retain the capacity to increase its bitcoin reserve each quarter — “that process can be infinite,” the founder said.

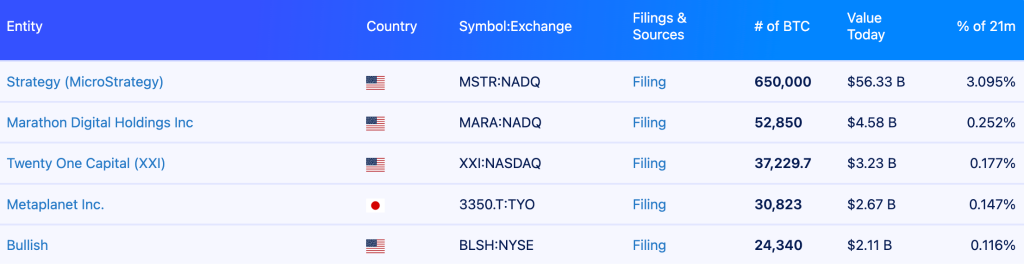

Strategy is currently the largest corporate holder of the first cryptocurrency. It manages 650,000 BTC worth about $56bn, roughly 3.1% of the total supply of digital gold.

Between 17 and 30 November, Strategy acquired another 130 BTC for about $11.7m. The average purchase price was $89,960.

Since the start of its bitcoin accumulation, Saylor’s cardinal rule was never to sell it. The company’s current strategy suggests a rethink.

The shift is driven by a fundamental requirement of Strategy’s business model: the company must generate dividends for shareholders. The primary funding mechanism is issuing shares, but that instrument is effective only if mNAV exceeds 1, management said.

The community is uneasy about a potential sale of bitcoin by Saylor’s firm. Gold advocate and crypto sceptic Peter Schiff again declared an “approaching end of Strategy”.

Today is the beginning of the end of $MSTR. Saylor was forced to sell stock not to buy Bitcoin, but to buy U.S. dollars merely to fund MSTR’s interest and dividend obligations. The stock is broken. The business model is a fraud, and @Saylor is the biggest con man on Wall Street.

— Peter Schiff (@PeterSchiff) December 1, 2025

“Today is the beginning of the end of MSTR. Saylor was forced to sell stock not to buy bitcoin, but merely to buy US dollars and cover MSTR’s interest and dividend obligations. The stock has collapsed. The business model is fraud, and Saylor is the biggest con man on Wall Street,” he said.

Earlier, Schiff had already accused Strategy of fraud and even challenged its founder to a debate.

Outlook for Strategy

On the latest news, MSTR shares fell almost 6% to $171.42. They now trade 70% below the all-time high of $543.

Even so, the investment bank Benchmark remains optimistic about Strategy’s prospects. Analyst Mark Palmer said the company’s shares still offer “an attractive way to gain exposure to the crypto market”, Decrypt reported.

Palmer stressed that sceptics “clearly do not understand” Saylor’s operating model. He rejected the notion of potential financial strain, saying such a scenario would be possible only if bitcoin fell to $12,700.

“While drawdowns of more than 80% have indeed occurred in bitcoin’s history, we believe that repeating such a scenario in current conditions would require the simultaneous impact of several large macroeconomic shocks,” he noted.

Despite volatility, Benchmark reaffirmed its “buy” rating on Strategy with a $705 price target. The call assumes the first cryptocurrency reaches $225,000 by the end of 2026.

“We view Strategy shares as one of the most effective instruments in global markets. A unique balance-sheet structure, a well-honed capitalisation mechanism and an embedded reflexive link to bitcoin’s dynamics create an unprecedented growth potential unavailable to any other public company,” Palmer concluded.

Undervaluation of the shares

Strategy’s stock has entered an undervaluation zone relative to the value of its bitcoin treasury. In the past, this preceded a sustained price recovery, said CryptoQuant analyst Carmelo Aleman.

Strategy Is Worth More Than Its Current Price

“Strategy’s decline has been deeper than the loss in the value of its Bitcoin holdings, widening the relative discount.” – By @oro_crypto pic.twitter.com/yAAYJMiRLd

— CryptoQuant.com (@cryptoquant_com) December 1, 2025

At the current bitcoin price, the company’s unrealised profit is about 22%. Yet its shares have fallen more than the value of the crypto reserve and reached the lower bound of the range that CryptoQuant defines as a “zone of historical undervaluation”.

In Aleman’s view, in previous cycles reaching this level has been a strong signal of a pricing mismatch. A subsequent correction towards fair value followed as market sentiment normalised.

“If the historical model repeats, the current level of undervaluation could become one of the most significant turning points in recent years,” he wrote.

In late November, investors accused JPMorgan of a coordinated attack on Strategy.