Survival Game: What Happened to the Mining Industry in 2022

Paradoxical rise in Bitcoin hash rate amid price collapse and stagnation, Ethereum’s transition to Proof-of-Stake, and the first major bankruptcy of a mining company.

We look back at what else defined 2022 for the industry.

- Russia fell out of the top three in Bitcoin hash rate share.

- The share of public companies in network computing power reached 25%.

- Rising difficulty, falling prices and an energy crisis crushed miners’ revenues.

- The industry faced its first major bankruptcy and the threat of more to come.

- Ethereum abandoned mining with its transition to the Proof-of-Stake algorithm.

Bitcoin hash rate hit new highs, despite the bear market

From the start of the year, Bitcoin’s hash rate rose by about 58% — from 172.8 EH/s to a November peak of 272.4 EH/s. Since then the indicator has corrected modestly.

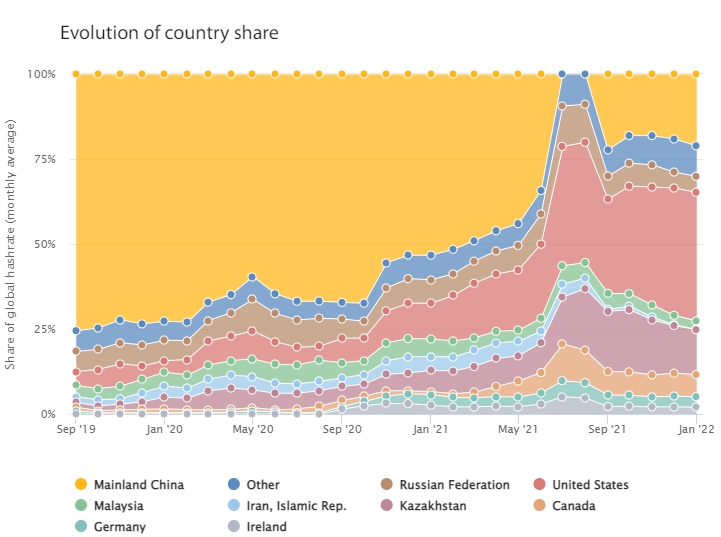

The United States remained the leader by share of computing power, lifting its lead to 37.8%, according to data from the Cambridge Centre for Alternative Finance (CCAF).

Contrary to the organization’s earlier findings, Chinese authorities failed to ban mining entirely. As early as September 2021, CCAF experts recorded a return of relevant hash rate to the network, reaching 21.1%.

In second place was Kazakhstan — 13.2%. Russia dropped out of the top three (4.7%), yielding to Canada (6.5%).

Specialists from the organization presented the geographic distribution as of January 2022. Therefore one can only speculate how subsequent events and trends affected hash rate migration.

Miners operating in the United States and Canada actively expanded capacity. Kazakhstan faced a significant outflow of industry players due to power-supply issues and proposed amendments to tax legislation. The relocation of up to 30% of equipment from the country was discussed.

Russian companies’ activities were touched by sanctions, though at year-end experts noted an uptick in demand for mining rigs.

In terms of pools, Foundry USA remained the leader, increasing its share of Bitcoin hash rate from 17% to 26.45% over the year. The structure continued to dominate, despite the financial problems at its parent company Digital Currency Group.

Following them were AntPool, F2Pool and Binance Pool. These platforms also expanded. For example, AntPool’s share increased by almost 5% since January. As a result, the top four pools controlled 75% of Bitcoin’s hash rate.

Analyst Jaran Mellerud of Hashrate Index attributed the paradoxical growth to public miners’ investments in equipment during the previous bull cycle. The share of such players in the hash rate over 12 months increased from 10% to 25%.

Founder of Capriole Investments Charles Edwards offered a different view. The expert argued that the hash rate peaks in such unfavorable market conditions are explained by the tacit entry of large oil and gas companies into mining.

As the network’s capacity rose to new record highs, mining difficulty rose in tandem. By late November, the indicator reached an all-time high of 36.95 T.

Miners faced a debt-servicing challenge

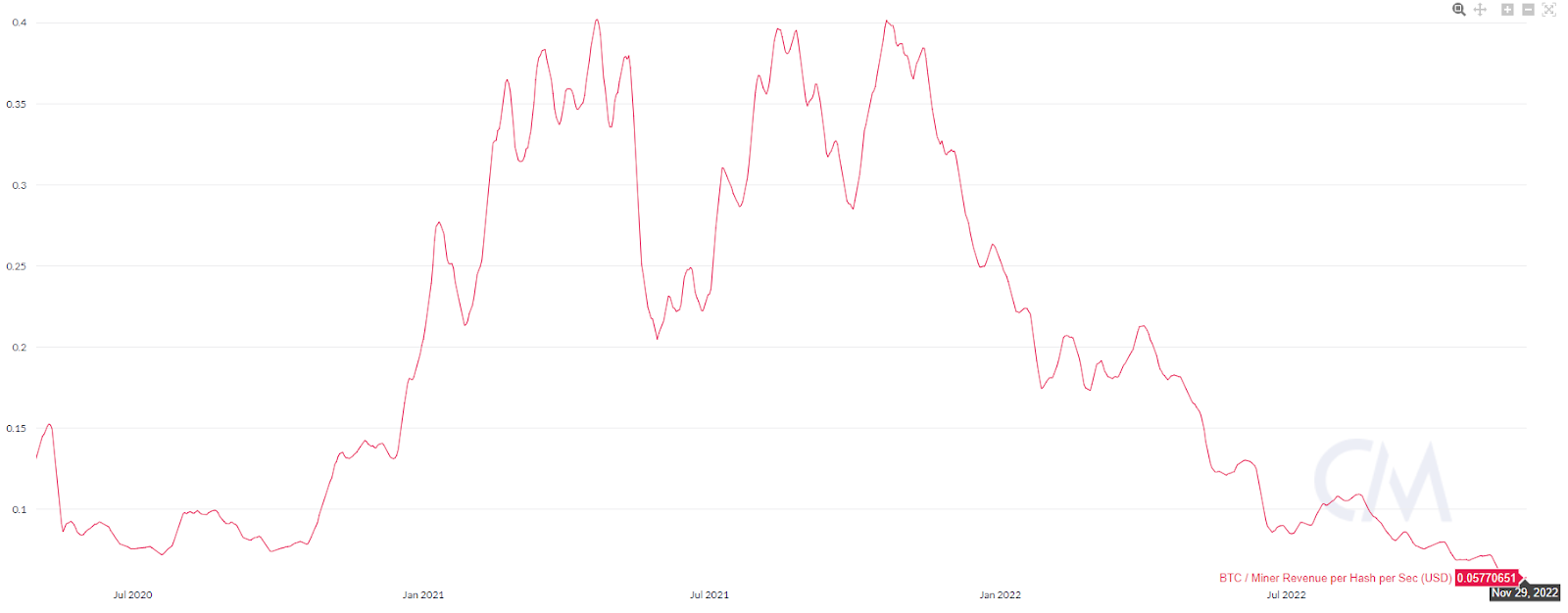

Rising difficulty, a fall in Bitcoin’s price and higher tariffs due to the energy crisis put serious pressure on mining profitability over the year. Sector revenues by November fell to $461 million (vs. $1.2 billion in January).

In November, the hashprice hit an historical low near $0.058 per 1TH/s. The metric measures miners’ revenue per unit of expended computing power.

At the start of summer, public miners liquidated a substantial portion of their crypto reserves. Nevertheless, Arcane Research deemed their financial position resilient.

In September, the industry faced its first major bankruptcy. A bankruptcy filing was filed by a private mining company and the infrastructure provider Compute North.

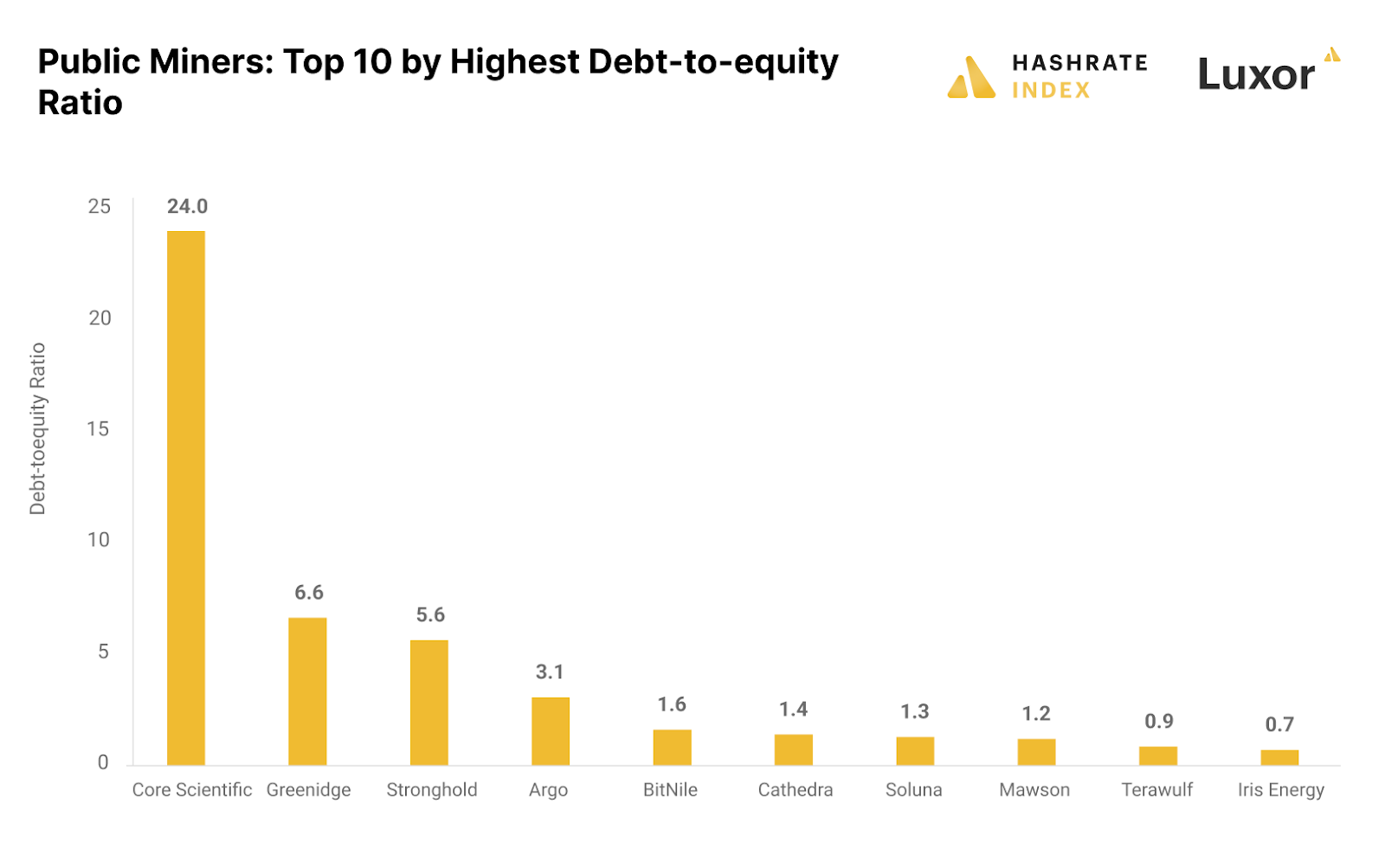

By October, publicly listed Core Scientific warned of risk of exhausting its reserves by year-end and possible bankruptcy. In December, the company filed for Chapter 11 for business reorganization.

Hashrate Index noted that the firm’s problems were broadly explicable. Analysts examined the debt-to-liquid-assets ratio among the largest public miners. For Core, the figure was considerably higher than for others — 24.

British Argo Blockchain also disclosed a potential halt in operations due to financing shortfalls. Its metric stood at 3.1. The metric indicates that Greenidge and Stronghold could be at risk.

During the 2021 bull market, companies actively borrowed to buy equipment, often secured against it. Bloomberg estimated the volume of debt at risk of liquidation at $4 billion.

According to the agency, the largest creditors were NYDIG, Celsius Network, BlockFi, Galaxy Digital and Foundry. Over the year, some miners began pulling back tens of thousands of installations, unable to service the debt.

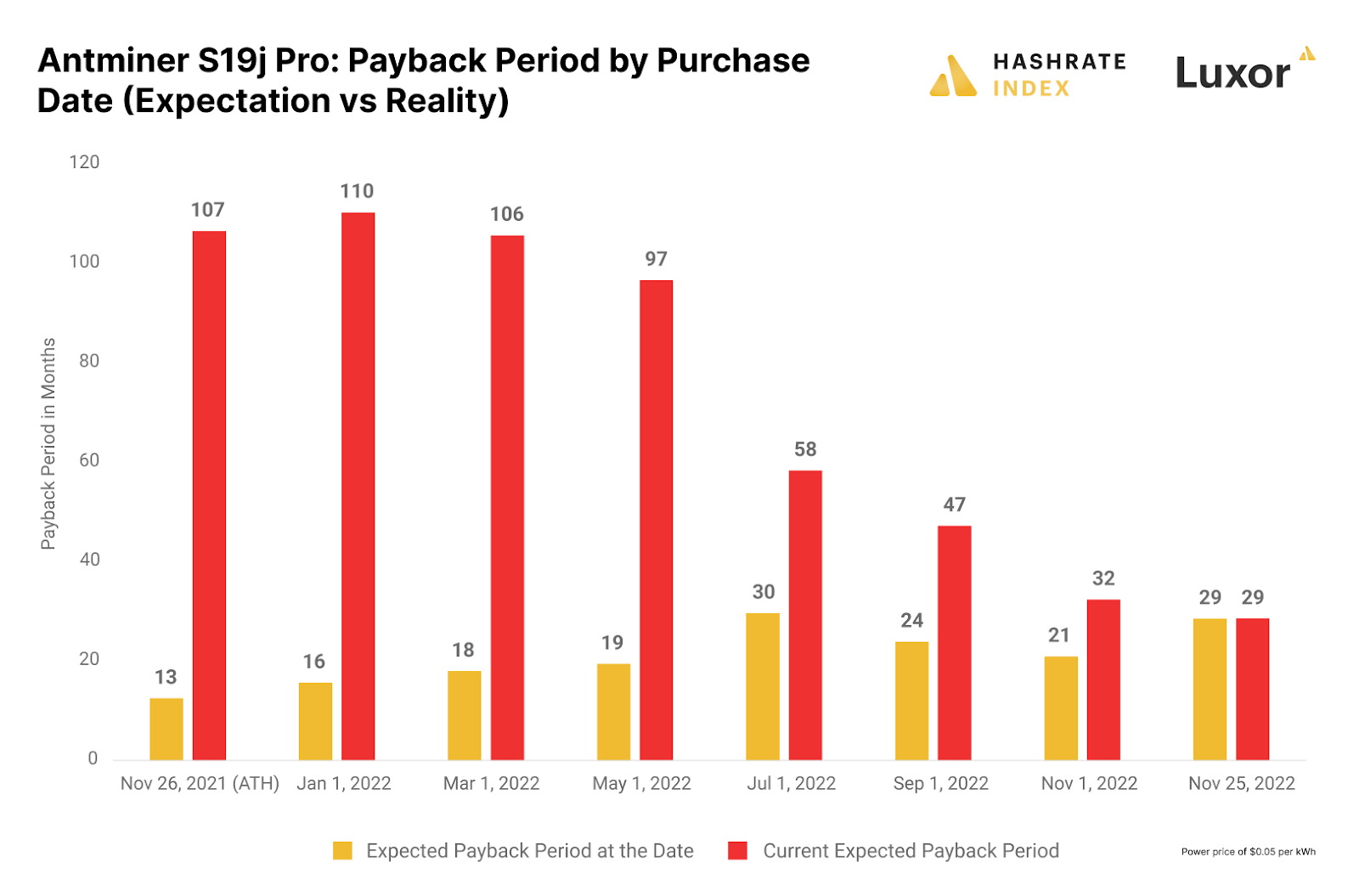

The events unfolded against a backdrop of a swift drop in equipment prices — more than 80% over the year. Hashrate Index reported that in January devices with energy efficiency above 38 J/TH cost about $101; by year-end the figure had fallen to $18. Foundry confirmed this assessment.

Payback periods for purchases made at peak prices stretched many times over in the current market. Experts calculated that it would take about 9 years to recoup the cost of an Antminer S19j Pro bought in January.

Intel Enters the ASIC-Mining Market

The bear market also hit miners’ equipment makers. For the third quarter, Canaan reported a net profit of $8.6 million. The figure plunged by 90% compared with the prior period.

Chairman and CEO Nangeng Zhao stressed that the revenue decline was due to price corrections on existing contracts — the firm had met the planned physical sales volumes.

During 2022, Canaan rolled out two new Bitcoin miner lines. The flagship 12-series claimed 35 J/TH, while top devices in the 13-series achieved 25 J/TH.

In April MicroBT unveiled the Whatsminer M50. The leading M50S recorded 26 J/TH energy efficiency.

Bitmain continued to expand its S19 line. Its flagship delivers 21.5 J/TH efficiency.

Analysts say the shift to more efficient equipment helped drive Bitcoin’s hash rate growth in 2022. Meanwhile, network power consumption declined from about 9,500 MW to about 8,400 MW, according to Hashrate Index.

In this context, a new potential large player entered the mining-hardware sector — American Intel.

In February the firm unveiled the Bonanza Mine chip for mining the first cryptocurrency. The presentation was purely technical, but experts noted a claimed efficiency of just 55 J/TH.

One of the early customers for the chip was GRIID Infrastructure. In SEC filings, the latter disclosed plans to obtain from Intel devices with much higher specifications — 26 J/TH.

In April Intel confirmed the metric corresponds to the second generation of a device named Blockscale.

In July the company announced the start of deliveries to first customers. Among them were Argo Blockchain, Block and HIVE Blockchain. The latter received its first 262 installations in November.

Ethereum Moves to Proof-of-Stake. Altcoins Could Not Absorb All Miners

On September 15, developers activated the scale upgrade The Merge in the Ethereum network. The blockchain moved to the Proof-of-Stake consensus algorithm (PoS).

According to 2Miners, the network hash rate at that moment stood at around 740 TH/s. Some miners of the second-largest cryptocurrency by market cap understandably shifted to altcoins that can be mined with GPUs.

Ethereum Classic benefited markedly from the influx, its power rose from 55 TH/s to 290 TH/s. Alongside the migration, hash rates for coins like Ravencoin, Ergo and Beam also rose.

However, soon miners began disconnecting equipment from the new networks. It was clear that for many, altcoin mining was not profitable enough to cover costs. By the end of September, media reported a sharp drop in GPU prices in China.

Ethereum Classic’s hash rate from October stabilized in the 150–130 TH/s range, and trended downward. A similar trend was seen in other networks that attracted players after The Merge.

The not-quite-problem-free Ethereum PoW fork proved unattractive for miners. At its peak on September 15, network power reached 68 TH/s; by year-end the figure had fallen below 19 TH/s.

Conclusion

Hashrate Index experts say the current crypto-winter has not proved tougher for Bitcoin miners than prior episodes. For example, during the 2020 bear phase, revenue per kilowatt-hour fell to $0.083. The current minimum is recorded at $0.108 (with a shorter duration of the unfinished cycle).

Analysts expect North American miners to further increase their share of the Bitcoin hash rate. Regional players continue to receive thousands of units of contracted modern equipment and develop infrastructure.

The weight of public companies in the aggregate metric is likely to rise as well. However, this process will slow — since the start of the year, shares of publicly traded firms have fallen by up to 90%. That will hinder their access to additional financing.

But for some firms, the crypto-winter became an opportunity to acquire rivals’ assets (CleanSpark, Crusoe, Foundry and others) at substantial discounts or to increase hash rate at minimal cost through supplier discounts (for example, TeraWulf). This will inevitably lead to consolidation of the industry by stronger players.

Many experts forecast the bear market will end in spring 2023. This is echoed by the duration of similar prior periods. The industry will have time to prepare for the next Bitcoin halving, which is expected in 2024.

Read ForkLog’s Bitcoin news in our Telegram — cryptocurrency news, prices and analysis.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!